Low-E Glass Market Overview with Emissivity, U-Value and Carbon Payback Metrics

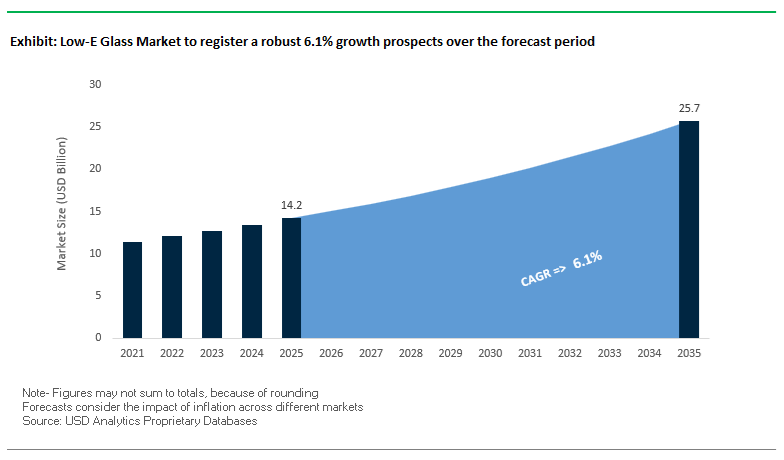

The global Low-E (low-emissivity) glass market is projected to grow from USD 14.2 billion in 2025 to USD 25.7 billion by 2035, registering a robust CAGR of 6.1% (2025–2035). For Low-E glass manufacturers, coaters, and façade system vendors, growth is being driven by stringent building energy codes, net-zero building programs, and the rapid adoption of triple-silver Low-E coatings in both residential and commercial glazing. From a product engineering standpoint, top-tier soft-coat Low-E glass produced via magnetron sputtering vacuum deposition (MSVD) is now delivering emissivity values as low as 0.02, compared with about 0.84 for standard clear float glass, fundamentally changing the energy balance of building envelopes. At the insulated glass unit (IGU) level, combinations of triple-silver Low-E layers with argon-filled cavities are achieving whole-window U-factors near 0.15 BTU/(hr·ft²·°F) or 0.80 W/m²K, improving thermal insulation by up to 85% versus single glazing.

Key low-E glass market insights for manufacturers and vendors:

- Ultra-low emissivity: Premium soft-coat Low-E glass achieves emissivity values near 0.02, delivering >97% reduction versus standard float glass and enabling best-in-class thermal insulation performance.

- High insulation performance: Advanced Low-E IGUs with triple-silver coatings and argon filling reach U-factors around 0.15 BTU/(hr·ft²·°F), meeting or exceeding the strictest global building energy codes.

- UV protection built-in: Low-E coatings can filter up to 78% of UV, protecting interiors, furnishings, and artworks in high-end retail, museums, and residential towers.

- Spectrally selective control: Triple-silver Low-E products deliver high VT (~70%) with low SHGC (~0.25) and LSG > 2.5, a critical specification in hot and mixed climates focused on cooling-load reduction.

- Strong decarbonization narrative: Replacing single glazing with Low-E double glazing offers CO₂ payback in less than a year per m², directly supporting net-zero and low-carbon building commitments.

Market Analysis: Hybrid Furnaces, Triple-Silver Coatings and Green Building Demand

The Low-E glass market is being reshaped by parallel forces in sustainable glass manufacturing, high-performance coating design, and green building regulations. On the production side, AGC Glass Europe’s Volta hybrid furnace R&D project, highlighted in its 2025 sustainability communications, is a flagship example of the industry’s decarbonization strategy. By combining electric melting with oxy-gas combustion, AGC is working toward lower-carbon float glass substrates that will underpin future generations of Low-E coatings. In 2024–2025, AGC also began actively offering low-carbon float glass to customers, providing a lower-embodied-carbon base glass for high-performance Low-E products—a critical differentiation as façade specifications increasingly include both operational energy and embodied carbon metrics. In parallel, industry trend reports in January 2025 pointed to a surge in global demand for Low-E IGUs, driven by the rapid spread of LEED and other green building certification schemes, which are now mainstream in North America, Europe, the Middle East, and parts of Asia.

On the product innovation front, the competitive landscape is being defined by differentiation in triple-silver Low-E coatings and clever system-level design. In late 2025, Viracon launched VNE-53, a new triple-silver Low-E coating delivering a visible light transmittance of about 52% and SHGC of around 0.23 on low-iron glass—designed to balance neutral aesthetics with strong solar control on high-end commercial façades. Also in September 2025, Viracon introduced RoomSide® Low-E, an interior-facing (#4 surface) coating solution that can improve U-value by up to 20%, providing near triple-glazing performance while retaining the simplicity and cost profile of a dual-pane IGU. Guardian Glass, for its part, is showcasing its SunGuard™ SNX 62/27 triple-silver coating across multiple high-profile projects in 2025, demonstrating the commercial scalability of high-selectivity Low-E coatings that combine high VLT with low SHGC in large-format façades.

Environmental and regulatory trends are also feeding directly into coating innovation. In 2025, Guardian Glass emphasized its Bird1st™ UV glass solution, which uses UV-reflective coating technology related to Low-E process know-how to reduce bird collisions and support compliance with bird-friendly building ordinances in North America and Europe. This is broadening the functional scope of Low-E and related thin-film stacks well beyond energy efficiency into biodiversity protection and regulatory risk mitigation. Meanwhile, the broader thin-film equipment ecosystem is evolving: IHI Ionbond’s continued investment in thin-film deposition capacity in Europe in 2024–2025 signals potential technology cross-pollination from hard coating and PVD/CVD equipment into high-throughput, multi-layer soft-coat Low-E production lines, reinforcing the equipment base required for the next wave of sophisticated triple- and even quadruple-silver architectures. Collectively, these developments signal a market that is moving simultaneously toward lower-carbon substrate production, higher-performance Low-E stacks, regulatory-compliant façade solutions, and increasingly complex coating equipment demands.

High-Performance Trends Driving Triple/Quad Glazing Adoption and Dynamic Low-E Technologies

Market Trend 1: Rapid Market Shift Toward Triple & Quadruple Low-E Glazing for Net-Zero and Passive House Building Envelopes

A major trend in the Low-E glass market is the rapid adoption of triple-pane and quadruple-pane glazing systems that use multilayer silver low-E coatings to meet increasingly strict energy efficiency standards. These advanced insulating glass units, often filled with argon or krypton gas, can achieve U-factors as low as 0.8 W/(m²·K), delivering up to four times better thermal insulation than conventional double-pane glass. As a result, triple glazing has become a key solution for reducing space heating demand in cold and temperate regions.

Standards such as Passive House, which require U-factors below approximately 0.8 W/(m²·K), have made high-performance triple glazing essential in modern building envelopes. Manufacturers now combine strong thermal insulation with high visible light transmission of 65% or more, preserving daylight quality. At the same time, advanced low-E coatings reduce solar heat gain, with SHGC values as low as 0.23 to 0.25, blocking most unwanted heat while maintaining clarity. This balance is especially important for large glass façades, and it positions triple and quadruple low-E glazing as a core technology for carbon-neutral construction.

Market Trend 2: Commercial Maturity of Electrochromic and Thermochromic Low-E Glass for Adaptive Energy Control

A second major trend is the commercialization of dynamic low-E glazing that uses electrochromic and thermochromic technologies to actively control solar heat gain. Electrochromic glass can adjust visible light transmission from about 60% in a clear state to below 5% when fully tinted, using very low voltage. This enables automated building façades that respond in real time to sunlight intensity, cooling demand, and occupant comfort, improving energy efficiency throughout the day.

Thermochromic glazing, particularly coatings based on vanadium dioxide, offers a passive alternative by changing near-infrared reflectance as temperatures rise, typically between 20 and 30°C. This allows façades to self-regulate solar heat without sensors or control systems. Studies show that dynamic low-E glazing can cut peak cooling demand by 20 to 25% compared with static low-E glass, while also blocking over 99% of UV radiation. With the growth of smart buildings and AI-enabled energy management, dynamic glazing is increasingly becoming a preferred solution for high-performance commercial construction and smart city applications.

Emerging Opportunities in BIPV Energy Harvesting and Retrofit Low-E Coating Applications

Market Opportunity 1: Integration of Transparent Photovoltaics with Low-E Structures for Building-Integrated Photovoltaic (BIPV) Facades

Transparent photovoltaic integration is emerging as a high-value opportunity in the Low-E glass market, allowing buildings to generate renewable electricity while preserving strong thermal and optical performance. Recent advances in perovskite and organic photovoltaic technologies enable transparent PV layers to reach power conversion efficiencies of 7 to 15% while maintaining visible light transmission in the 20 to 50% range, making them suitable for façade and window applications.

When combined with low-E coatings, transparent PV layers can be engineered to maintain neutral architectural color while also delivering effective solar control, often achieving SHGC values below 0.4. In high-rise buildings with large glazed areas, building-integrated photovoltaic window systems have the potential to supply 10 to 20% of total electricity demand, supporting net-zero energy objectives. As material stability and large-scale manufacturing improve, TPV-integrated low-E glass is positioned to become a core element of next-generation sustainable building design.

Market Opportunity 2: Development of High-Durability Low-E Window Films for Global Retrofit Markets

A major opportunity in the Low-E glass market is the retrofit window film segment, which allows older buildings to achieve near-modern thermal performance without the cost and disruption of full window replacement. High-performance low-E films applied to single-pane glass can reduce U-factors by 20 to 30% and cut solar heat gain by more than 75 percent, bringing single-pane windows close to, or even beyond, the performance of many older double-pane systems.

These films work by sharply lowering glass emissivity, typically from about 0.84 to as low as 0.08 to 0.15, which significantly limits radiant heat transfer. Modern retrofit films are designed for long service life of 10 to 15 years or more, with resistance to bubbling, peeling, and coating degradation under intense sunlight. They also block over 90% of near-infrared radiation while maintaining optical clarity. With governments accelerating building retrofit programs to reduce emissions, durable low-E window films offer a scalable and cost-effective path to rapid energy efficiency improvements across existing building stock.

Low-E Glass Market Share Analysis

Market Share by Coating Type: Soft-Coat (MSVD) Low-E Glass Leads High-Performance Architectural Glazing

Soft-coat Low-E glass, produced through Magnetron Sputter Vacuum Deposition (MSVD), accounts for the largest share of the global Low-E glass market—approximately 70% in 2025—due to its superior thermal insulation and customizable optical properties, which align directly with the tightening global energy-efficiency mandates driving façade and window system design. Its ultra-low emissivity levels (typically 0.02–0.05) result from multi-layer silver-based coatings applied in a controlled vacuum environment, enabling exceptional U-factor improvement and precise tuning of Solar Heat Gain Coefficient (SHGC) profiles. These features make MSVD Low-E glass indispensable for energy-optimized building envelopes in both cold and warm climates, supporting advanced thermal management in passive and net-zero energy buildings. Although soft-coat layers require encapsulation within insulated glazing units (IGUs) for durability, this characteristic aligns perfectly with global construction trends, as double and triple glazing have become the normative standard for high-performance building design. The ability to produce double-silver and triple-silver configurations further strengthens its dominance, allowing architects and façade engineers to balance daylighting, solar control, glare management, and energy savings across commercial offices, residential towers, institutional facilities, and high-end architectural glazing systems. As sustainability regulations intensify and low-carbon construction becomes a global priority, the MSVD-based soft-coat segment remains the preferred solution for high-efficiency glazing, sustaining its significant lead over pyrolytic hard-coat alternatives.

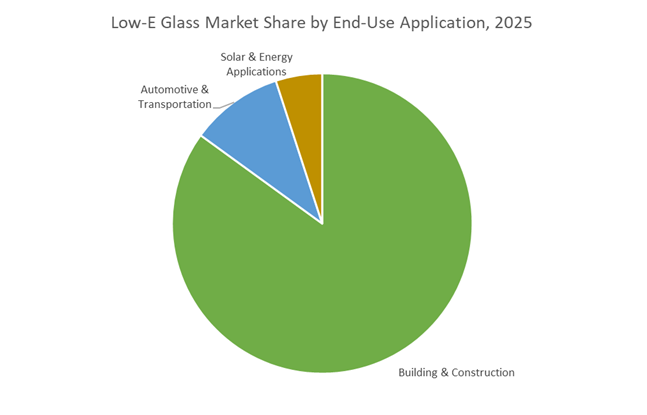

Market Share By End-Use Industry: Building & Construction Drives Over 85% of Low-E Glass Consumption

The Building & Construction sector accounts for nearly 85% of all Low-E glass demand, reflecting the material’s critical role in reducing heating and cooling loads in modern buildings and supporting stringent energy-efficiency regulations worldwide. With buildings responsible for an estimated 30–40% of total global energy consumption, Low-E glazing has emerged as one of the most impactful and widely mandated solutions for improving building-envelope performance, lowering HVAC costs, and meeting carbon-reduction targets. Rapid urbanization, the surge in high-rise commercial towers, and the widespread use of structural glazing and curtain walls have intensified the need for high-performance thermal control materials that enable daylighting without compromising energy efficiency. Soft-coat Low-E IGUs are now standard in new construction across developed economies and are increasingly adopted in emerging markets as building codes evolve. Additionally, the massive global retrofit and renovation wave—driven by aging building stock and policy incentives for energy-efficient upgrades—continues to accelerate demand for Low-E replacement windows. These dynamics collectively reinforce the construction sector’s overwhelming dominance in Low-E glass consumption, positioning it as the cornerstone of market growth and the largest contributor to long-term adoption across residential, commercial, and institutional building segments.

Country Analysis: Global Drivers in the Low-E Glass Ecosystem

United States: Advancements in Vacuum Insulating Glass (VIG), Low-Embodied Carbon Materials, and High-Performance Coating Validation

The United States continues to be one of the most influential innovation hubs in the Low-E Glass Market, driven by stringent energy codes, federal procurement standards, and accelerating investment in next-generation insulating technologies. A major milestone occurred in November 2025 when Vitro Architectural Glass entered an exclusive agreement to manufacture VacuMax™ Vacuum Insulating Glass (VIG) in North America. VIG delivers wall-like insulation values—reaching R20 performance—representing a transformative step for ultra-high-efficiency building envelopes. This domestic manufacturing commitment ensures broader market accessibility for VIG across climate-extreme regions, bolstering U.S. net-zero building targets.

Sustainability regulations are also reshaping material selection. As of April 2024, all Vitro architectural glass products meet the Top 20% Low Embodied Carbon (LEC) threshold set by the U.S. General Services Administration (GSA), aligning with federal purchasing mandates under the Inflation Reduction Act. The performance legacy of Vitro’s Solarban® soft-coat low-E portfolio—marking 20 years of Solarban® 70 and 10 years of Solarban® 90—reinforces the long-term reliability of U.S. MSVD (magnetron sputter vacuum deposition) coatings. Further validation comes from the GSA Green Proving Ground program, which selected the Cohen Federal Building in 2024 to test next-generation low-E glazing systems. These initiatives collectively position the U.S. as a leader in commercializing VIG, ultra-efficient solar control coatings, and decarbonized glazing technologies.

European Union (Germany/France): EPBD-Driven Triple Glazing Adoption and Decarbonized Low-E IGU Manufacturing

The European Union—led by Germany and France—remains at the forefront of the Low-E Glass Market due to sweeping decarbonization mandates and aggressive building-energy performance regulations. The revised Energy Performance of Buildings Directive (EPBD) is the strongest market accelerator, requiring deep renovation of the EU’s 75% energy-inefficient building stock and pushing widespread adoption of high-performance triple-glazed low-E IGUs to meet near-zero-energy building standards. Manufacturers across Germany, France, and the Nordics are scaling production of triple glazing incorporating argon and krypton insulating gases, which work synergistically with soft-coat low-E layers to achieve ultra-low U-values.

Europe’s energy crisis from 2022–2023 further reinforced the necessity of high-efficiency glass solutions. As float glass plants in Germany, Poland, and neighboring regions experienced dramatic energy cost increases, stakeholders prioritized materials offering rapid energy savings and compelling payback periods—driving strong demand for MSVD soft-coat low-E products. Companies such as Saint-Gobain and AGC continue to innovate in spectrally selective solar control coatings, optimized for both retrofit and new-build applications, as the EU intensifies climate targets and accelerates low-carbon building material adoption.

China: Large-Scale Low-E Glass Production Capacity and Rapid Uptake Across Construction and Automotive Segments

China is the world’s largest producer and consumer of flat glass, and its regulatory momentum continues to accelerate the adoption of both hard-coat (pyrolytic) and soft-coat (MSVD) low-E products. Rapid modernization and expansion of commercial building stock—especially glass-intensive façades in Tier 1 and Tier 2 cities—continue to drive massive volume demand. Large domestic manufacturers such as Xinyi Glass and CSG Holding are expanding production capacity across multiple coating lines to meet rising requirements under China’s strengthened green building standards, which increasingly mandate low-E glazing for public, commercial, and high-rise residential construction.

Beyond buildings, China’s booming EV industry is emerging as a new high-growth segment for low-E glass adoption. Automakers are integrating solar-control low-E glazing to reduce cabin heat gain, improve HVAC efficiency, and extend EV driving range—benefits that align closely with national electrification targets. As battery thermal efficiency becomes a competitive differentiator, the use of coated glazing in windshields, panoramic roofs, and side windows is expanding rapidly. China’s scale advantage, integrated supply chains, and expanding regulatory pressure position it as both a volume leader and a strategic innovator in low-E glass technologies.

Japan: Mandatory 2025 Energy-Efficiency Standards and Integration of Smart, Spectrally-Selective Low-E Coatings

Japan’s Low-E Glass market is being reshaped by stringent national efficiency mandates and advanced R&D in spectrally selective glazing technology. Starting in 2025, universal energy-efficiency standards for all new housing make high-performance glazing with low-E coatings an essential compliance pathway for builders, significantly increasing demand across residential construction. These mandates reflect Japan’s broader push to reduce energy consumption in buildings while maintaining high daylighting levels in dense urban environments.

Innovation remains a central pillar, with leading manufacturers such as Nippon Sheet Glass (NSG) investing in spectrally selective low-E coatings engineered to admit maximum visible light while sharply blocking near-infrared heat. These coatings enable improved occupant comfort and reduced cooling load, particularly in high-rise towers where façade performance is critical. As Japan advances smart glass adoption—incorporating electrochromic and sensor-enabled glazing—low-E layers serve as foundational performance components within next-generation smart building envelopes.

India: ECBC-Driven Low-E Demand and Strong Market Preference for Solar-Control Low-E Glass

India’s Low-E Glass Market is expanding rapidly due to the sustained growth of commercial construction and nationwide enforcement of the Energy Conservation Building Code (ECBC). ECBC guidelines strongly prioritize the use of solar-control low-E glazing to reduce cooling loads in large commercial buildings, hospitals, IT parks, and airports—sectors that dominate new urban development. The regulatory structure encourages developers to adopt low-E glass with favorable Solar Heat Gain Coefficient (SHGC) parameters to offset rising air-conditioning demand in India’s warm-humid and composite climate zones.

Given India’s predominantly hot climate, the market overwhelmingly favors solar-reflective low-E coatings, rather than passive low-E solutions tailored for heating-dominant regions. These coatings significantly decrease solar radiation penetration, supporting substantial energy cost reductions for end users. With rapid urbanization and increasing commercial glazing area per project, India’s demand for advanced low-E IGUs and high-performance façade systems is expected to remain strong, driven by both regulation and rising energy-efficiency expectations among developers.

Competitive Landscape: Strategic Positioning of Leading Low-E Glass Manufacturers

The global Low-E glass market is concentrated around a group of vertically integrated glass and coating specialists that control float glass production, coating technology, and often downstream fabrication. AGC, Guardian Glass, Saint-Gobain, Vitro Architectural Glass, and Viracon are shaping the technology roadmap through investments in low-carbon float glass, triple-silver Low-E coatings, bird-friendly glass, and large-format IGU fabrication. Their competitive strategies center on combining energy performance, optical quality, sustainability credentials, and regulatory compliance into complete façade and window solutions. For façade consultants, developers, and system fabricators, these companies set the performance baseline for emissivity, U-value, SHGC, and LSG, as well as the availability of specialized solutions such as room-side Low-E coatings and bird-collision mitigation glass.

AGC Inc.: Volta Hybrid Furnace and Low-Carbon Low-E Glass Leadership

AGC Inc. is a global Low-E glass leader with a broad architectural portfolio built around its Stopray® and Planibel® families, covering both soft-coat MSVD and pyrolytic hard-coat technologies for residential and commercial applications. Under its “Blue Planet” value creation pillar in the 2025 Integrated Report, AGC is heavily investing in decarbonizing glass production, with the Volta hybrid furnace R&D project aimed at combining electric melting and oxy-gas combustion to significantly cut CO₂ emissions in float glass manufacturing. This low-carbon float glass acts as the substrate for its premium Low-E coatings, allowing AGC to offer high-performance, low-embodied-carbon glazing solutions. Its Low-E glass is widely specified in high-profile green building projects across Europe, Asia, and the Americas, where custom configurations are engineered to meet local energy codes, climate conditions, and net-zero carbon targets.

Guardian Glass: Triple-Silver SunGuard and Bird-Friendly Low-E Innovations

Guardian Glass, part of Koch Industries, is a major global producer of float and coated glass and a key player in the high-performance Low-E glazing market. Its SunGuard® line for commercial applications and ClimaGuard® range for residential projects offer a full suite of solar control and Low-E coatings, with flagship triple-silver products such as SunGuard SNX 62/27. The company’s strategic focus is on spectrally selective coatings that maximize natural daylight while aggressively managing solar heat gain, aligning with global energy codes and occupant comfort requirements. Guardian also addresses environmental regulation with its Bird1st™ UV glass, which uses UV-reflective patterning to reduce bird strikes—an increasingly important criterion in many cities’ façade codes. With control over both float glass production and sputter-coating lines, Guardian provides an integrated Low-E solution from substrate to final coated product through a global network of fabricator partners.

Saint-Gobain: PLANITHERM and COOL-LITE Solutions for Low-E and Solar Control

Saint-Gobain is one of the world’s largest building materials groups and a key reference in Low-E and solar-control architectural glass. Its PLANITHERM® range of Low-E products and COOL-LITE® family of solar-control coatings, including advanced COOL-LITE XTREME triple-silver solutions, are engineered to combine low U-values with high light transmittance and carefully tuned solar selectivity. The company’s core technological strength lies in developing coatings that provide high thermal insulation with minimal visual tint, ensuring daylight quality and façade neutrality, with some double-glazed configurations achieving light transmittance levels near 79%. PLANITHERM products are widely used to satisfy stringent national regulations, such as the UK’s Part L and other European energy directives, becoming a default specification for energy-efficient glazing. Saint-Gobain also quantifies its products’ environmental benefits, emphasizing that the CO₂ generated producing 1 m² of Low-E double glazing can be offset in roughly 3.5 months of use, reinforcing its positioning in the sustainable construction value chain.

Vitro Architectural Glass: Solarban Low-E Products for North American Energy Codes

Vitro Architectural Glass (formerly PPG Glass) is a leading North American supplier of flat glass and high-performance Low-E coatings, known especially for its Solarban® product family. Solarban coatings, including triple-silver and advanced solar-control variants such as Solarban 70, deliver ultra-low emissivity (down to ~0.02) combined with strong solar heat rejection, making them well suited to hot and mixed climates where cooling load reduction is critical. Vitro’s core strength lies in aligning its Low-E glass portfolio with stringent ASHRAE and IECC energy codes prevalent in the U.S. and Canada, making Solarban a standard in high-rise offices, institutional buildings, and healthcare facilities. The company’s float glass production and coating lines are integrated to ensure consistent optical quality and color uniformity, which is crucial for large façades where even minor color shifts are noticeable. As North America accelerates building decarbonization, Vitro’s Low-E offerings play a central role in reducing HVAC energy consumption across new build and retrofit projects.

Viracon: Fabricated IGUs with Triple-Silver and RoomSide Low-E Capabilities

Viracon, a subsidiary of Apogee Enterprises, is a specialist in fabricated architectural glass, focusing on IGUs, laminated, and decorative glazing for complex commercial building envelopes. Its VNE and VRE series Low-E coatings, including the VNE-53 triple-silver product launched in late 2025, target high-end commercial projects that demand a balance of neutral aesthetics, daylight, and solar control. Viracon’s standout innovation is RoomSide® Low-E, introduced in September 2025, an interior-facing (#4 surface) Low-E coating that can improve U-values by up to 20%, offering performance close to triple glazing in a double-pane configuration—highly attractive where weight and façade depth are constrained. The company has invested in manufacturing infrastructure capable of producing very large glass sizes (base dimensions up to around 130" × 236"), enabling “big glass” façade designs without sacrificing coating performance. Viracon’s products are certified by bodies such as the IGCC to ASTM standards, ensuring long-term durability and consistent optical performance for demanding curtain wall and unitized façade systems.

Low-E Glass Market Report Scope

Low-E Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.2 Billion

|

|

Market Size (2035)

|

$25.7 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Coating Type (Soft-Coat Low-E Glass, Hard-Coat Low-E Glass), By Coating Function (Passive Low-E Coatings, Solar Control Low-E Coatings, Spectrally Selective Low-E Coatings), By Glazing Configuration (Single Low-E Glazing, Double-Glazed IGU, Triple-Glazed IGU, Vacuum Insulating Glass with Low-E), By Coating Material (Metallic Coatings, Metal Oxide Coatings), By End-Use Application (Building & Construction, Automotive & Transportation, Solar & Energy Applications), By Building Sector (Commercial Buildings, Residential Buildings)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Vitro Architectural Glass, Saint-Gobain, Guardian Glass, AGC Inc., Nippon Sheet Glass, PPG Industries, CSG Holding, Xinyi Glass, Central Glass, Taiwan Glass, SCHOTT AG, Jinjing Group, Technoform Group, Hehr International, Saray Holding

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Low-E Glass Market Segmentation

By Coating Type

- Soft-Coat Low-E Glass (MSVD)

- Hard-Coat Low-E Glass (Pyrolytic)

By Coating Function

- Passive Low-E Coatings

- Solar Control Low-E Coatings

- Spectrally Selective Low-E Coatings

By Glazing Configuration

- Single Low-E Glazing

- Double-Glazed IGU

- Triple-Glazed IGU

- Vacuum Insulating Glass (VIG) with Low-E

By Coating Material

- Metallic Coatings (Silver-Based)

- Metal Oxide Coatings

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Solar & Energy Applications

By Building Sector

- Commercial Buildings

- Residential Buildings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Low-E Glass Market

- Vitro Architectural Glass

- Saint-Gobain

- Guardian Glass

- AGC Inc.

- Nippon Sheet Glass (NSG Group)

- PPG Industries

- CSG Holding

- Xinyi Glass

- Central Glass

- Taiwan Glass

- SCHOTT AG

- Jinjing Group

- Technoform Group

- Hehr International

- Saray Holding.

*- List not Exhaustive

Research Coverage: Low-E (Low-Emissivity) Glass Market

The latest Low-E Glass Market study by USDAnalytics provides a comprehensive, data-backed view of how high-performance coated glazing is transforming building envelopes and transport glazing worldwide. This report investigates the interplay between ultra-low emissivity coatings, advanced insulated glass unit (IGU) configurations, and tightening global energy codes, while mapping technology breakthroughs in triple-silver soft-coat stacks, vacuum insulating glass (VIG), dynamic electrochromic façades, and low-carbon float substrates. It offers detailed analysis reviews of emissivity, U-value, SHGC, LSG ratios, and carbon payback metrics across key applications, and highlights the competitive moves of major float glass producers, coaters, system integrators, and façade specialists as they respond to net-zero and embodied-carbon requirements. With deep coverage of soft-coat versus hard-coat strategies, triple and quadruple glazing adoption, retrofit low-E films, and BIPV-ready glazing, this report is an essential resource for architects, façade engineers, energy consultants, glass processors, and ESG-focused investors seeking to optimize thermal performance, daylighting, and sustainability outcomes in new-build and renovation projects.

Scope Highlights

- Segmentation

- By Coating Type: Soft-Coat Low-E Glass (MSVD), Hard-Coat Low-E Glass (Pyrolytic)

- By Coating Function: Passive Low-E Coatings, Solar Control Low-E Coatings, Spectrally Selective Low-E Coatings

- By Glazing Configuration: Single Low-E Glazing, Double-Glazed IGU, Triple-Glazed IGU, Vacuum Insulating Glass (VIG) with Low-E

- By Coating Material: Metallic Coatings (Silver-Based), Metal Oxide Coatings

- By End-Use Industry: Building & Construction, Automotive & Transportation, Solar & Energy Applications

- By Building Sector: Commercial Buildings, Residential Buildings

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and detailed forecast trends from 2026 to 2034.

- Companies: In-depth analysis and profiles of 15+ leading Low-E glass manufacturers and ecosystem players, including float producers, coaters, and façade glass fabricators.