Methyl Cellulose Market 2025–2034: Pharmaceutical-Grade Expansion, Low-Nitrite HPMC Innovation, and Bio-Based Cleaning Solutions Driving $4.3 Billion Outlook at 4.8% CAGR

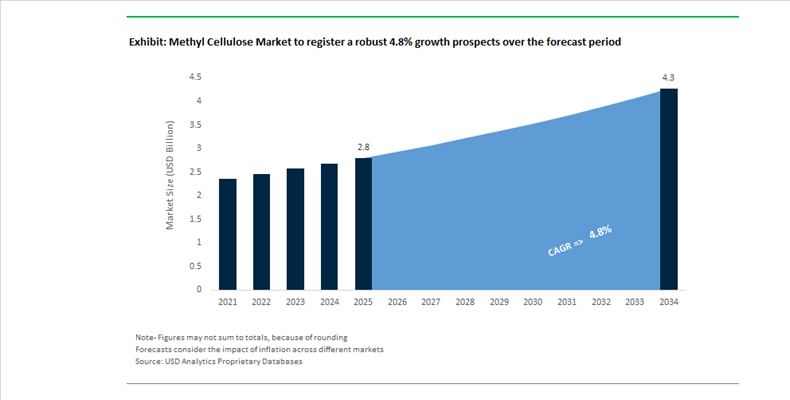

The Methyl Cellulose Market is projected to grow from $2.8 billion in 2025 to $4.3 billion by 2034, registering a CAGR of 4.8%. Growth is supported by rising demand for pharmaceutical excipients, controlled-release drug delivery polymers, food-grade stabilizers, construction additives, and sustainable detergent thickeners. Methyl cellulose (MC) and its derivatives, including hydroxypropyl methylcellulose (HPMC), are critical for rheology control, film formation, binding, and anti-redeposition in diverse end-use industries. Increasing regulatory scrutiny on nitrosamine formation in pharmaceuticals, coupled with global sustainability mandates in home care formulations, is reshaping product innovation strategies.

In April 2024, Shin-Etsu Chemical secured European Pharmacopoeia listing for AQOAT, its hypromellose acetate succinate derivative used in enteric coatings and solid dispersion systems, simplifying regulatory approval pathways across Europe. In October 2024, LOTTE Fine Chemical signed a 10-year global distribution agreement with Colorcon for its AnyCoat pharmaceutical-grade methyl cellulose and HPMC portfolio, reinforcing supply stability in the excipient market. Between October 2024 and February 2026, Shin-Etsu released updated technical guidelines for METOLOSE food and pharmaceutical grades to support high-speed tableting and coating precision. In early 2025, LOTTE Fine Chemical commenced commercial operations at its expanded pharmaceutical cellulose facility following a KRW 263.6 billion investment, strengthening global capacity for high-value drug delivery polymers. In May 2025, Shandong Head Group expanded its strategic distribution partnership with Univar Solutions to broaden MC and HPMC availability across North America and Europe for food, pharma, and construction sectors.

Sustainability and formulation safety drove further innovation through late 2025 and early 2026. In September 2025, Ashland launched the iSolve information portal to provide digital regulatory documentation and technical formulation support for cellulose ethers. In October 2025 at the SEPAWA Congress, Nouryon introduced advanced cellulose-based thickeners for high-efficiency detergents, emphasizing renewable sourcing and carbon footprint reduction. In late 2025, Roquette launched a low-nitrite METHOCEL HPMC grade to minimize nitrosamine risk in sensitive APIs used in controlled-release oral dosage forms. In February 2026, Nouryon announced the global launch of FinnFix PB MAX, the first 100% renewable carbon index CMC, underscoring the broader transition toward bio-based cellulose derivatives in home care. During the same period, Ashland reported softer construction demand while advancing portfolio optimization to focus on high-margin specialty cellulose niches in pharmaceutical and personal care applications.

Methyl Cellulose Market Trends and Opportunities

Trend: Thermoreversible Gelation Optimization for Next-Generation Plant-Based Meat

The methyl cellulose market is being structurally reinforced by its critical role in next-generation plant-based meat formulations, where clean-label positioning and sensory authenticity are now decisive competitive factors. Unlike alternative hydrocolloids, methyl cellulose exhibits thermoreversible gelation, remaining soluble at low temperatures and forming a stable gel upon heating. This property enables plant-based burgers and nuggets to maintain structural integrity during cooking while retaining moisture, directly addressing consumer complaints around dryness and texture collapse.

In early 2025, cross-disciplinary research leveraged by food technology developers demonstrated that a 3 g per 100 g methyl cellulose solution can function as the sole binding agent in soybean-based burger formulations. This breakthrough allows manufacturers to eliminate modified starches and phosphates, aligning with the accelerating clean-label trend across North America and Europe. Industrial benchmarks now show methyl cellulose inclusion rates of 0.2% to 2.0% in commercial meat analogues, where it simultaneously stabilizes fat-water emulsions and prevents syneresis during frozen storage and reheating cycles.

Equally important is the strategic collaboration between European food-tech innovators and cellulose ether producers formed in late 2024 to engineer fat-mimicking methyl cellulose variants. These systems are designed to replicate the melt and release behavior of animal fat, particularly in poultry and beef analogues, closing the mouthfeel gap that has historically limited repeat purchases in plant-based categories. As foodservice adoption expands, methyl cellulose is becoming a non-substitutable ingredient in scalable meat analogue production.

Trend: Asia-Pacific Localization and Capacity Expansion to De-Risk Supply Chains

Geopolitical uncertainty and rising demand from construction and pharmaceuticals are driving a decisive shift toward localized methyl cellulose production across the Asia-Pacific region. Governments and manufacturers are prioritizing domestic capacity to reduce dependence on Western imports and ensure continuity in strategic end-use sectors.

China’s 14th Five-Year Plan has catalyzed infrastructure investment exceeding USD 4.2 trillion, significantly boosting demand for domestically produced methyl cellulose used in tile adhesives, mortars, and cement modifiers. These additives improve water retention, workability, and open time, making them essential for large-scale urban construction and prefabrication projects. In parallel, India’s construction sector is projected to reach USD 1.4 trillion by 2025, creating strong internal demand that incentivizes local producers to expand R&D and capacity rather than rely on volatile import channels.

On the global trade front, Shandong Head Group entered a strategic distribution agreement with Univar Solutions in May 2025. This partnership extends the reach of Asian-manufactured high-performance methyl cellulose into North America and Europe, intensifying competition with established incumbents while improving supply resilience for downstream customers. Collectively, these moves indicate a long-term rebalancing of the methyl cellulose supply landscape toward Asia-led production hubs.

Opportunity: High-Performance Rheology Control for 3D Concrete Printing

Automated construction and 3D concrete printing are creating a high-value growth avenue for methyl cellulose as a rheology modifier capable of delivering rapid buildability and structural stability. Unlike conventional admixtures, methyl cellulose enables high green strength, allowing freshly printed layers to support subsequent layers without deformation or collapse.

Recent 2025 academic studies indicate that cellulose-modified concrete formulations can achieve approximately 7 kPa green strength within 75 minutes, a critical threshold for continuous 3D printing without auxiliary reinforcement. Research published in August 2024 further demonstrated that incorporating at least 0.3% cellulose-based additives significantly enhances interlayer bonding and flow control, reducing print defects and material waste in automated housing projects.

Beyond terrestrial construction, space agencies including NASA are evaluating methyl cellulose-fortified eco-concrete for lunar and Martian infrastructure. Its ability to deliver mechanical stability with minimal labor input positions methyl cellulose as a cornerstone material for off-world additive manufacturing, expanding its relevance far beyond traditional construction markets.

Opportunity: Ultra-Pure GMP-Grade Methyl Cellulose for Advanced Drug Delivery

Pharmaceutical demand is shifting toward ultra-pure, GMP-compliant methyl cellulose grades for use in orally disintegrating tablets, controlled-release matrices, and sensitive biologic formulations. This trend is driven by stricter regulatory scrutiny and the need for excipients that ensure consistent drug release without microbial or endotoxin contamination.

In April 2025, Shin-Etsu Chemical announced a 10 billion yen investment to expand its pharmaceutical cellulose operations, including capacity upgrades at its Naoetsu plant and the construction of a new facility in Germany. This move reflects rising global demand for high-compliance excipients and the strategic importance of supply assurance for multinational drug manufacturers.

Similarly, a 10-year partnership signed in October 2024 between LOTTE Fine Chemical and Colorcon aims to scale AnyCoat® pharmaceutical-grade cellulose derivatives for premium tablet coating and binding applications. The market is also transitioning toward Endotoxin Controlled Excipient portfolios, with ultra-pure methyl cellulose grades becoming essential for advanced drug delivery systems where even trace contamination can compromise efficacy. Together, these developments position pharmaceutical-grade methyl cellulose as a high-margin, structurally resilient growth segment within the broader market.

Methyl Cellulose Market Share and Segmentation Insights

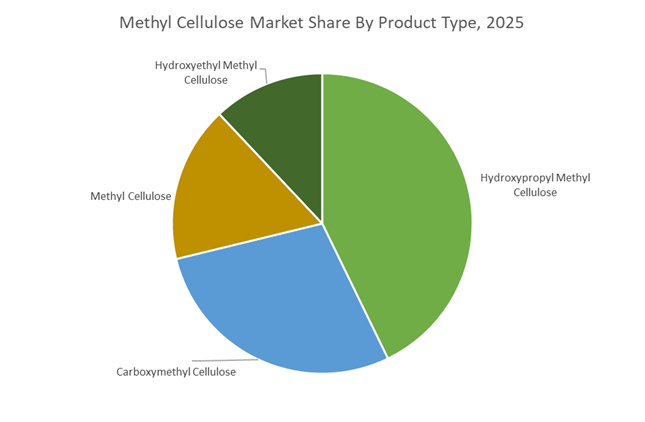

Hydroxypropyl Methyl Cellulose Dominates Methyl Cellulose Market Due to Multifunctional Performance in Construction and Pharmaceutical Applications

Hydroxypropyl Methyl Cellulose (HPMC) accounted for 42.80% of the Methyl Cellulose Market share in 2025, establishing it as the most widely used cellulose ether across industrial and pharmaceutical formulations. HPMC offers a highly versatile functional profile including water retention, viscosity modification, film-forming capability, surface activity, and thickening performance, making it indispensable for both construction chemicals and pharmaceutical excipients. In the construction sector, HPMC is extensively used in tile adhesives, cement-based mortars, plasters, renders, self-leveling compounds, and dry-mix building materials, where it improves workability, adhesion strength, and water retention required for proper cement hydration. Pharmaceutical manufacturers also rely on HPMC for tablet coating, capsule shells, and controlled drug release matrices, where the polymer ensures consistent dissolution behavior and dosage performance. In 2025, rising adoption of modern construction application systems such as mechanized plastering equipment and large-format tile installations has increased demand for higher-performance HPMC grades that deliver extended open time, improved slip resistance, and consistent rheological behavior across large-scale building projects.

Construction Industry Drives the Largest Demand for Methyl Cellulose-Based Additives

Construction accounted for 42.80% of the Methyl Cellulose Market share in 2025, making building materials the largest end-use industry for methyl cellulose derivatives. Cellulose ethers such as HPMC play a critical role in cement-based and gypsum-based dry-mix mortar formulations, where they regulate water retention, enhance workability, and provide improved adhesion in applications including tile adhesives, wall putties, plastering compounds, grouts, and self-leveling floor systems. The rapid growth of urban infrastructure development, residential construction, and commercial building activity has significantly increased the consumption of dry-mix construction chemicals that depend on methyl cellulose additives. In 2025, the construction sector has also experienced increasing demand for green building materials and sustainable construction systems, where methyl cellulose enables the development of lightweight mortars, improved insulation plasters, and factory-produced dry formulations that reduce construction waste and improve material efficiency. These additives also support compatibility with recycled aggregates and alternative cement binders, making them increasingly important in sustainable construction material innovation.

Methyl Cellulose Market Competitive Landscape

The methyl cellulose (MC) and HPMC market in 2026 is driven by low-nitrite pharmaceutical excipients, clean-label food stabilizers, and molecularly tailored cellulose ethers. Demand is rising across drug delivery, plant-based foods, and construction chemicals, with innovation focused on nitrosamine mitigation, thermal gelation, and high-performance rheology modification.

Ashland focuses on low-nitrosamine pharmaceutical excipients and high-margin cellulose additives

Ashland Inc. is advancing its “pure-play” strategy by prioritizing high-value methyl cellulose and HPMC grades for pharmaceutical and personal care applications. Its optimized excipient portfolio, showcased at CPHI Frankfurt and AAPS PharmSci 360, addresses stringent regulatory requirements for low-nitrosamine drug formulations. The divestiture of non-core assets like Avoca has enabled reinvestment into specialty additives with superior binding and film-forming properties. Its exclusive IMCD distribution partnership strengthens North American market penetration for cellulose-based rheology modifiers. Ashland’s strong regulatory support and formulation expertise make it a preferred partner for complex drug delivery systems. The company continues to focus on high-margin, compliance-driven cellulose ether solutions.

Shin-Etsu strengthens global supply chain with vertical integration and high-purity HPMC production

Shin-Etsu Chemical Co., Ltd. maintains global leadership through large-scale vertical integration and feedstock security. Its $3.4 billion investment in U.S. chlor-alkali and VCM capacity ensures a stable supply of key intermediates for cellulose derivatives. METOLOSE® and TYLOPUR® remain industry benchmarks for pharmaceutical and construction-grade methyl cellulose. The company is advancing low-viscosity HPMC grades tailored for high-speed tablet coating and advanced drug delivery. Its manufacturing excellence in Japan and Germany ensures consistent product quality and precise thermal gelation control. With a strong sustainability roadmap and reliable supply chain, Shin-Etsu is a critical supplier for global pharmaceutical and construction industries.

IFF Pharma Solutions leads low-nitrite HPMC innovation for safer drug formulations

IFF Pharma Solutions is setting industry standards with its Low Nitrite METHOCEL™, designed to minimize nitrosamine formation in pharmaceutical products. This innovation directly addresses global regulatory scrutiny from the FDA and EMA, accelerating adoption among major drug manufacturers. Its METHOCEL™ portfolio remains central to sustained-release and matrix tablet formulations. IFF is integrating cellulose ethers with its broader bioscience portfolio to create advanced hydrocolloid systems that enhance API bioavailability. The company also supports the transition to vegan HPMC capsules as alternatives to gelatin. Its “Total Formulation Solution” approach strengthens its position in high-value pharmaceutical excipient markets.

LOTTE Fine Chemical expands plant-based food applications with MECELLOSE and functional HPMC

LOTTE Fine Chemical is accelerating growth in green materials by expanding its MECELLOSE® and AnyCoat® brands across global food and pharmaceutical markets. Its partnership with Caldic enhances distribution reach in North America, targeting plant-based meat and gluten-free bakery applications. MECELLOSE® provides critical thermal gelation, moisture retention, and texture stability in clean-label formulations. The company is investing in production upgrades to increase capacity for high-performance cellulose ethers. With strong revenue performance and a shift toward specialty additives, LOTTE is strengthening its position in functional food and construction segments. Its focus on plant-based innovation aligns with evolving consumer and regulatory trends.

Nouryon advances bio-based cellulose ethers with ISCC-certified sustainable innovation

Nouryon is positioning itself as a leader in sustainable cellulose chemistry through bio-based and biodegradable innovations. The launch of FinnFix® PB MAX highlights its commitment to renewable raw materials and circular chemistry, supporting low-carbon formulations in consumer goods. Its Bermocoll® HPMC portfolio is tailored through global innovation centers in Shanghai and Brazil to meet regional formulation demands. Recognition from Henkel Consumer Brands underscores its role in enabling carbon-neutral ingredient solutions. Nouryon’s ISCC PLUS-certified supply chains provide traceability and compliance for sustainability-focused customers. Its expertise in rheology modification and green chemistry strengthens its competitive position in next-generation cellulose ether markets.

United States: Pharmaceutical Risk Mitigation and Food Reformulation Momentum

The United States methyl cellulose market is being reshaped by pharmaceutical safety regulation and food reformulation mandates, driving demand for high-purity, functionally optimized grades. In April 2025, IFF Pharma Solutions launched its Low Nitrite METHOCEL HPMC portfolio, engineered to cap nitrite levels at or below 200 parts per billion. This innovation directly addresses regulatory scrutiny around nitrosamine formation in finished dosage forms, positioning methyl cellulose as a preferred excipient for solid oral formulations and controlled-release systems in the U.S. pharmaceutical pipeline. Adoption has been strongest among generic and specialty drug manufacturers seeking compliance without reformulating entire delivery matrices.

Food and nutrition policy is reinforcing structural demand. The U.S. Food and Drug Administration issued Phase II draft guidance in August 2025, setting sodium reduction targets across 163 food categories for the 2026 horizon. This has accelerated the use of methyl cellulose as a multifunctional dietary fiber that preserves texture, mouthfeel, and water-binding capacity in reduced-sodium processed foods. On the supply side, new tariffs imposed on cellulose derivatives in 2025 triggered a shift toward vertically integrated production and domestic warehousing. Companies such as Ashland and Dow expanded dual-sourcing and inventory strategies to protect pharmaceutical-grade excipient availability through 2026. Ashland’s appointment of Tilley Distribution in October 2025 further strengthened last-mile delivery for food, nutraceutical, and dairy-alternative manufacturers experiencing sustained volume growth.

China: Industrial Scale-Up and Construction-Led Grade Optimization

China’s methyl cellulose market is advancing through industrial stabilization policy, export-oriented grade specialization, and construction sector innovation. Under the 2025 Industrial Stability Work Plan issued by the Ministry of Industry and Information Technology, domestic producers expanded methyl cellulose output to support a 6.5% year-on-year increase in chemical industrial production recorded in late 2025. This policy support has prioritized capacity additions and process efficiency improvements, particularly in large chemical clusters across eastern China.

Export competitiveness remains a defining feature. Manufacturers such as Zhejiang Kehong Chemical have captured more than 43% of Asia-Pacific demand by focusing on high-viscosity methyl cellulose grades for construction additives and industrial coatings. Despite softness in China’s residential manufacturing index during Q3 2025, infrastructure renewal programs planned for 2026 are sustaining demand for advanced construction-grade MC. Chinese producers are deploying one-pot thermal decomposition technologies to improve water retention and workability in high-performance mortars, while parallel investments in closed-loop recovery systems within Jiangsu address fiber security challenges and reduce dependence on imported cellulose feedstocks.

Germany: Regulatory Validation and Energy-Efficient Consolidation

Germany’s methyl cellulose market is characterized by regulatory clarity, premium food applications, and energy-driven production optimization. Following the European Food Safety Authority re-evaluation of celluloses in 2025, which confirmed NOAEL values up to 9,000 mg/kg body weight, German food technology companies expanded the use of methyl cellulose in gluten-free and plant-based bakery products. The ingredient’s thermo-gelling behavior is being leveraged to replicate animal protein textures, supporting clean-label positioning within Europe’s premium food segment.

At the same time, elevated natural gas and electricity prices throughout 2025 have accelerated consolidation and digital optimization among producers. Companies such as SE Tylose and BASF are integrating AI-enabled batch monitoring to reduce energy intensity in pharmaceutical-grade HPMC synthesis. Innovation pipelines are extending beyond traditional applications. In October 2025, BASF entered a strategic collaboration with IFF to advance Designed Enzymatic Biomaterials, targeting next-generation bio-based polymers that enhance performance in personal care and industrial cleaning formulations entering the 2026 market cycle.

South Korea: Pharmaceutical Coatings and Battery Binder Diversification

South Korea is emerging as a dual-focus market for methyl cellulose, anchored in pharmaceutical coatings and battery materials. The long-term alliance signed between Lotte Fine Chemical and Colorcon during 2024–2025 established a ten-year global supply framework for AnyCoat pharmaceutical-grade methyl cellulose. This partnership strengthens availability for enteric-coated and controlled-release tablets, supporting both domestic drug manufacturers and export-oriented formulation hubs.

Beyond pharmaceuticals, South Korean producers are increasingly targeting battery-grade methyl cellulose as a binder for lithium-ion battery electrodes. This diversification aligns with the country’s expanding electric vehicle manufacturing base and the national Energy Storage Systems roadmap for 2026. Battery-grade MC is valued for its rheology control and electrode integrity, positioning South Korea at the intersection of excipient chemistry and energy materials.

Japan: Ultra-Purification and Smart Packaging Integration

Japan’s methyl cellulose market is defined by ultra-purified food grades and advanced material science integration. Shin-Etsu Chemical reported a market capitalization of ¥13.2 trillion in 2024, underpinned by sustained capital investment in its METOLOSE production lines. The company is prioritizing ultra-purified methyl cellulose grades for functional foods and traditional confectionery, where consistency, clarity, and mouthfeel are critical to consumer acceptance.

Research-driven innovation is expanding application scope. In 2025, Japanese R&D institutes successfully piloted nanocellulose-based composites combined with methyl cellulose to create photonic films for smart food packaging. These films exhibit color changes in response to humidity and environmental conditions, signaling freshness and storage integrity. This convergence of nanotechnology and cellulose chemistry positions Japan as a leader in high-value, next-generation methyl cellulose applications beyond conventional food and pharmaceutical uses.

Country-Level Strategic Positioning in the Methyl Cellulose Market

Methyl Cellulose Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Application Drivers

|

Policy or Industry Catalyst

|

Competitive Positioning

|

|

United States

|

Pharma safety and food reformulation

|

Low-nitrite HPMC, sodium reduction

|

FDA guidance, tariff realignment

|

High-purity and supply-chain resilience

|

|

China

|

Construction scale and exports

|

High-viscosity MC for mortars

|

MIIT stability plan, infrastructure renewal

|

Cost-efficient industrial dominance

|

|

Germany

|

Premium food and energy efficiency

|

Gluten-free bakery, pharma HPMC

|

EFSA validation, energy optimization

|

Regulatory trust and process efficiency

|

|

South Korea

|

Pharma coatings and batteries

|

Enteric coatings, EV binders

|

Strategic alliances, ESS roadmap

|

Dual-sector specialization

|

|

Japan

|

Ultra-purified grades and smart materials

|

Functional foods, smart packaging

|

Capital investment, R&D leadership

|

High-value innovation leadership

|

Methyl Cellulose Market Report Scope

Methyl Cellulose Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2034)

|

$4.3 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Methyl Cellulose, Hydroxypropyl Methyl Cellulose, Hydroxyethyl Methyl Cellulose, Carboxymethyl Cellulose), By Grade (Pharmaceutical Grade, Food Grade, Industrial Grade, Cosmetic Grade), By Viscosity (Low Viscosity, Medium Viscosity, High Viscosity), By End-Use Industry (Construction, Food and Beverage, Pharmaceuticals, Personal Care, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shin-Etsu Chemical, Ashland, Dow, International Flavors and Fragrances, Lotte Fine Chemical, Nouryon, BASF, SE Tylose, J.M. Huber, Celanese, Kima Chemical, Zhejiang Kehong Chemical, Colorcon, Daicel

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Methyl Cellulose Market Segmentation

By Product Type

By Grade

- Pharmaceutical Grade

- Food Grade

- Industrial Grade

- Cosmetic Grade

By Viscosity

- Low Viscosity

- Medium Viscosity

- High Viscosity

By End-Use Industry

- Construction

- Food and Beverage

- Pharmaceuticals

- Personal Care

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Methyl Cellulose Market

- Shin-Etsu Chemical

- Ashland

- Dow

- International Flavors and Fragrances

- Lotte Fine Chemical

- Nouryon

- BASF

- SE Tylose

- J.M. Huber

- Celanese

- Kima Chemical

- Zhejiang Kehong Chemical

- Colorcon

- Daicel

*- List not Exhaustive