Methyl Tertiary Butyl Ether Market 2025–2034: Asian Capacity Surge, Methanol Integration, and Export-Driven Trade Flows Shaping $61.6 Billion Outlook at 5.7% CAGR

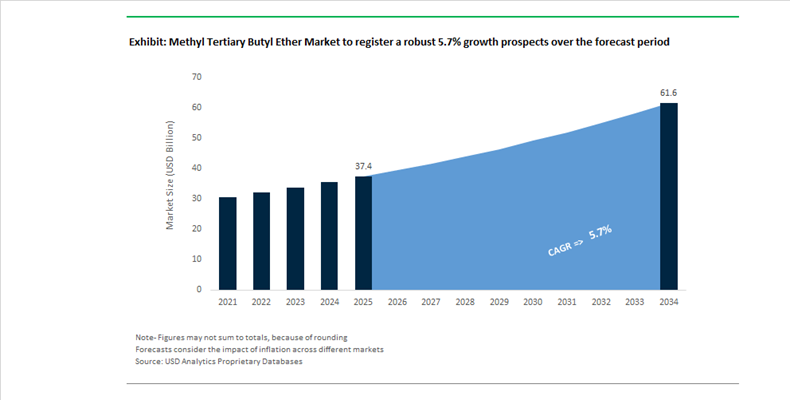

The Methyl Tertiary Butyl Ether (MTBE) Market is projected to expand from $37.4 billion in 2025 to $61.6 billion by 2034, registering a CAGR of 5.7%. Market momentum is being shaped by refinery-to-chemicals integration strategies, methanol feedstock consolidation, and shifting regional fuel blending mandates. MTBE remains a critical gasoline oxygenate used to improve octane ratings and reduce engine knocking, particularly in emerging markets across Asia, Africa, and Latin America. While domestic demand in certain mature markets remains constrained due to environmental regulations, global trade flows are increasingly export-driven, with Asia and the Middle East playing dominant roles in supply expansion.

In 2024, SABIC achieved full utilization of upgraded MTBE units, reinforcing supply into Asia-Pacific and African fuel markets. During the same year, LyondellBasell invested in operational upgrades across its fuel additive facilities to lower carbon intensity and align with ESG objectives. In March 2024, Celanese secured ISCC certification for its carbon capture-based methanol at Clear Lake, creating a pathway for low-carbon MTBE production. In 2025, Reliance Industries commenced operations at its 3.60 mtpa methanol plant in Jamnagar, strengthening India’s upstream methanol security and supporting downstream MTBE blending for improved fuel quality. By late 2025, U.S. Gulf Coast producers exported over 1.1 million metric tons of MTBE, with approximately 84% directed to Mexico, underscoring heavy reliance on export markets amid limited domestic U.S. consumption.

Supply-side expansion intensified in 2025 and 2026. Between September and November 2025, the MTBE FOB China marker declined to $620–$640 per metric ton from over $700 in 2024, reflecting oversupply pressures in Asia. In June 2025, Methanex finalized its acquisition of OCI Global’s methanol business, consolidating upstream feedstock control and enhancing price stability for MTBE producers globally. Throughout 2025 and 2026, European blenders increasingly shifted toward ETBE to comply with biofuel mandates, reducing regional MTBE demand and increasing dependence on imported material for non-mandated blending segments. In early 2026, Zhenhua Petrochemical is scheduled to commission a 660,000 mt/year MTBE plant, while Sinopec Zhongyuan Petrochemical plans an additional 600,000 mt/year capacity by mid-2026, reinforcing China’s refining-to-chemicals pivot and solidifying its position as a dominant exporter in the global MTBE value chain.

Methyl Tertiary Butyl Ether (MTBE) Market Trends and Opportunities

Trend: Geopolitical Rebalancing of MTBE Supply Toward Asia and the Middle East

The global MTBE market is undergoing a decisive geographic realignment as regulatory pressure in Western economies structurally suppresses domestic fuel blending demand. Environmental mandates under the U.S. Clean Air Act and the EU Renewable Energy Directive III have accelerated the phase-down of MTBE usage in gasoline, compelling producers to redirect volumes toward regions where ethanol blending infrastructure remains underdeveloped and octane enhancement is still price sensitive. As a result, Asia Pacific, the Middle East, and select Latin American markets have become the primary growth anchors for MTBE trade flows.

Despite declining domestic consumption, the United States continues to play a critical role as an export hub. In the first half of 2024, U.S. MTBE exports surged to nearly 0.9 million metric tonnes, reflecting a 45% year-on-year increase. These shipments are increasingly destined for Southeast Asia and Latin America, where refiners rely on MTBE to meet Euro 4 and Euro 5 equivalent fuel specifications without the logistical complexity of ethanol. Parallel to this, the Middle East is expanding its role as a structurally advantaged supplier. Petrokemya is executing a major debottlenecking project at its Al Jubail complex, scheduled for completion in Q4 2025, which is expected to lift MTBE capacity by roughly 30%. In Asia, Wanhua Petrochemical has reinforced regional supply stability by restarting its Shandong MTBE operations in 2025, underscoring China’s continued reliance on MTBE as a gasoline blendstock. Collectively, these shifts are consolidating MTBE supply around low-cost, regulation-resilient hubs while increasing trade dependency in importing regions.

Trend: MTBE Cracking as a Strategic Pathway to High-Purity Isobutylene

To offset long-term uncertainty in the fuel additives segment, producers are accelerating investments in MTBE cracking technologies that unlock high-purity isobutylene as a downstream growth lever. MTBE decomposition enables the recovery of isobutylene at purities approaching 99.99 percent, positioning it as a critical feedstock for butyl rubber and methyl methacrylate value chains that are expanding on the back of automotive, construction, and specialty polymer demand.

Technology alliances are central to this transition. In late 2024, Axens entered an exclusive collaboration with ExxonMobil to commercialize MTBE decomposition technology capable of delivering ultra-high-purity isobutylene. This development directly targets a global isobutylene market projected to reach multi-billion-dollar scale by the mid-2030s. Captive integration is gaining traction in Asia as well. In China, Huizhou Boeko Materials selected Lummus Technology’s CATOFIN® platform to support large-scale isobutylene production dedicated to downstream polymers. India is following a similar trajectory, with Reliance Industries and Vinati Organics collectively operating around 230 kilotonnes of MTBE cracking capacity. This structural pivot is redefining MTBE from a terminal fuel additive into a flexible intermediate that underpins higher-margin chemical derivatives.

Opportunity: Repurposing MTBE Assets for Bio-Ether and Bio-Isooctene Production

The extensive global MTBE asset base represents a compelling brownfield opportunity as refiners and chemical producers pursue decarbonization without incurring full replacement costs. By integrating bio-based feedstocks such as bio-methanol or bio-isobutene, existing MTBE units can be retrofitted to produce Bio-MTBE or bio-isooctene, enabling compliance with Low Carbon Fuel Standards and emerging carbon intensity benchmarks.

Momentum around green methanol is accelerating this pathway. In May 2025, European Energy commissioned the Kassø e-methanol facility, the world’s first large-scale commercial plant of its kind, supplying renewable methanol suitable for etherification. On the refining side, LyondellBasell has advanced flexible PO/TBA platforms in the United States that can swing between MTBE and ETBE production, allowing rapid alignment with regional renewable mandates. Industry-wide, strategic assessments highlighted by Accenture point toward hub-and-spoke models, where modular biomass-to-methanol units are co-located near MTBE plants. This approach minimizes capital expenditure while enabling producers to introduce low-carbon molecules into established process chains, materially extending the economic life of MTBE infrastructure.

Opportunity: High-Purity MTBE as a Specialty Pharmaceutical Solvent

Beyond fuels and polymers, MTBE is emerging as a high-value specialty solvent in pharmaceutical manufacturing. Its low water solubility, chemical stability across acidic and basic environments, and comparatively favorable safety profile are driving substitution away from traditional ethers such as diethyl ether and tetrahydrofuran in complex synthesis routes. This shift is particularly pronounced in India, which has become a global hub for bulk drug and API production.

Pharmaceutical-grade MTBE now accounts for roughly one-fifth of India’s domestic MTBE demand, with monthly consumption reaching approximately 3,000 tonnes by late 2024. Pricing in key production clusters such as Mumbai and Hyderabad has climbed to ₹101–115 per kilogram, reflecting the premium associated with multi-stage purification required to eliminate sulfur and trace contaminants. The economics of this segment are further reinforced by volatility in methanol feedstock prices, which have elevated the cost base for ultra-pure ether production. From a process perspective, MTBE’s controlled evaporation rate and reduced peroxide formation risk make it well suited for multi-step reactions and high-performance polymer intermediates. As pharmaceutical manufacturers increasingly prioritize solvent stability and regulatory compliance, high-purity MTBE is positioned as a resilient niche growth avenue within an otherwise transitioning MTBE market.

Methyl Tertiary Butyl Ether Market Share and Segmentation Insights

Industrial Grade MTBE Leads the Methyl Tertiary Butyl Ether Market Due to Large-Scale Gasoline Blending Demand

Industrial grade methyl tertiary butyl ether (MTBE) accounted for 68.40% of the Methyl Tertiary Butyl Ether Market share in 2025, reflecting its dominant role as a gasoline blending component used to improve fuel octane ratings and combustion performance. Industrial grade MTBE typically contains 95–98% purity, which meets the quality requirements for fuel blending in refinery operations and gasoline distribution systems. Refineries use MTBE primarily as a high-octane oxygenate additive, enabling gasoline producers to enhance octane levels while improving combustion efficiency and reducing engine knocking in spark-ignition engines. Because gasoline production volumes remain extremely large worldwide, industrial grade MTBE continues to represent the highest consumption category within the MTBE value chain. In 2025, the MTBE market exhibits strong regional divergence in usage patterns. While North America has reduced MTBE consumption due to ethanol blending mandates and environmental restrictions, Asia-Pacific and Middle Eastern fuel markets continue to rely heavily on MTBE as a cost-effective octane booster, sustaining global industrial-grade demand and maintaining refinery integration for MTBE production.

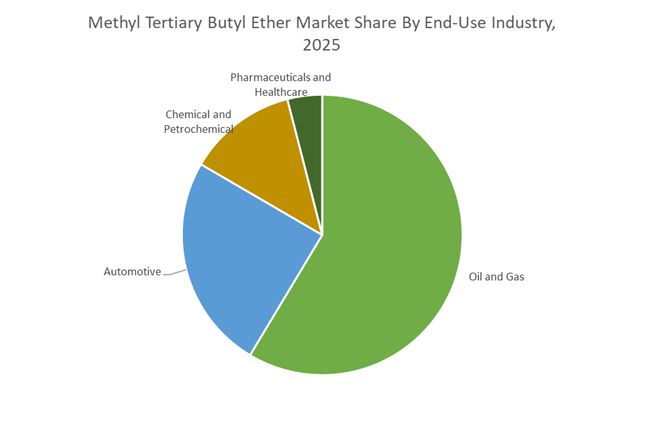

Oil and Gas Industry Drives the Largest Demand for Methyl Tertiary Butyl Ether

Oil and gas accounted for 58.60% of the Methyl Tertiary Butyl Ether Market share in 2025, making petroleum refining the largest end-use sector for MTBE consumption. The compound is widely used in gasoline blending operations within refinery complexes, where it functions as an oxygenated additive that increases octane number and improves combustion efficiency in transportation fuels. MTBE production is commonly integrated into refinery infrastructure through the use of isobutylene derived from fluid catalytic cracking (FCC) units, which reacts with methanol to produce MTBE in dedicated etherification units. This integration allows refineries to convert byproduct streams into valuable fuel components while improving overall refinery economics. In 2025, refiners are increasingly adopting refinery–petrochemical integration strategies, enabling MTBE production units to operate flexibly depending on fuel demand and petrochemical market conditions. In certain markets, MTBE may be sold as a petrochemical intermediate or solvent, while in fuel-intensive regions it continues to serve primarily as a gasoline blending component, linking MTBE demand closely with global gasoline production and refinery throughput levels.

Methyl Tertiary Butyl Ether Market Competitive Landscape

The methyl tertiary butyl ether (MTBE) market in 2026 is shaped by Asian capacity expansion, refinery-petrochemical integration, and biofuel substitution trends. Competitive dynamics center on export arbitrage, C4 stream optimization, and ETBE transition strategies, with demand driven by high-octane gasoline blending in Latin America and Southeast Asia.

SABIC scales world’s largest MTBE unit with feedstock integration and export resilience

SABIC has reinforced its leadership in the global MTBE market through large-scale capacity expansion and deep integration with Saudi Aramco’s upstream operations. Its flagship MTBE unit, expanded to 1 million t/y, is now the world’s largest single-unit facility, delivering unmatched economies of scale. The company’s access to cost-advantaged isobutylene and methanol ensures stable production economics despite global feedstock volatility. Strategic maintenance turnarounds in 2026 are enhancing long-term operational reliability and energy efficiency. SABIC is leveraging its Energy Resilience framework to sustain high-volume exports into Asia and Europe amid rising competition. Its scale, integration, and supply chain strength position it as the benchmark supplier in the MTBE market.

Sinopec drives global MTBE trade flows through aggressive capacity expansion and export strategy

Sinopec is at the center of the global MTBE supply surge, driven by large-scale capacity additions and state-backed refinery integration. Its Zhongyuan Petrochemical expansion alone adds 600,000 mt/year, contributing to China’s 3.9 million t/y capacity increase in 2026. Facing domestic oversupply, Sinopec has aggressively expanded exports, with China’s MTBE shipments reaching 4.99 million tons in 2025, up 100.7% year-on-year. The company is prioritizing refinery utilization rates to maintain dominance in aromatics and gasoline additives despite margin pressure. Anti-involution policies are consolidating production into high-efficiency, integrated complexes. Sinopec’s scale and export agility make it a dominant force in global MTBE trade flows.

LyondellBasell optimizes MTBE production through efficiency gains and co-product integration

LyondellBasell (LYB) is executing a value-driven MTBE strategy focused on process optimization and high-margin derivative integration. Its Cash Improvement Plan delivered $800 million in savings in 2025, with a $1.3 billion target set for 2026, enabling reinvestment into core assets. The company is streamlining its European footprint, divesting non-core assets to focus on efficient PO/TBA co-production units. Advanced process upgrades have improved MTBE production efficiency by 15%, enhancing isobutene conversion and reducing energy intensity. LYB leverages MTBE as a feedstock for MMA and other specialty intermediates, strengthening downstream value capture. Its focus on operational excellence and integration supports устойчив growth in specialty chemical markets.

Eni accelerates transition from MTBE to bio-based ETBE and renewable oxygenates

Eni, through its Ecofuel division, is repositioning itself as a leader in bio-oxygenates and sustainable fuel additives. Under its Enilive strategy, the company is actively converting traditional MTBE assets toward ETBE and HVO production to comply with EU RED III mandates. Its legacy expertise, anchored by the Ravenna plant, supports ongoing development of Bio-MTBE and renewable ether technologies. Strong 2025 financial performance, with €12.5 billion in operating cash flow, is funding this transition and expanding upstream integration. Strategic alliances with Petronas are securing feedstock supply for Asian operations. Eni’s pivot toward renewable oxygenates positions it at the forefront of decarbonized fuel blending solutions.

Reliance Industries leverages Jamnagar scale for export-driven MTBE dominance

Reliance Industries Limited (RIL) is a major exporter in the MTBE market, utilizing its Jamnagar refinery’s unmatched scale and complexity to capitalize on global arbitrage opportunities. The company played a key role in supplying over 1.115 million mt of MTBE to Mexico through August 2025, highlighting its strength in export logistics. Its O2C segment continues to deliver high throughput and strong margins for premium gasoline blendstocks despite market volatility. Advanced C4 recovery systems enable flexible production between MTBE, alkylates, and other derivatives. RIL is also investing ₹75,000 crore in a green energy complex, signaling future integration of bio-based ethers. Its scale, flexibility, and export focus underpin its leadership in global MTBE trade.

Saudi Arabia: Export-Oriented Scale, Feedstock Synergies, and Low-Carbon Positioning

Saudi Arabia continues to anchor global MTBE supply through scale expansion, integrated feedstock access, and capital discipline. In November 2025, SABIC brought its Petrokemya MTBE expansion at Jubail online ahead of schedule, adding one million metric tons of annual capacity and reinforcing the Kingdom’s role as a merchant exporter to Asia and Europe. This capacity addition is underpinned by deep operational synergies with Saudi Aramco, with captured value reaching SAR 10.6 billion by mid-2025. Optimization of C4 streams and methanol integration has improved unit economics and reliability across MTBE operations.

Capital allocation further strengthens competitiveness. SABIC earmarked $3.0–$3.5 billion in 2025 capital expenditure under its Transformation Program, targeting recurring EBITDA improvements through refining integration and asset efficiency. Middle Eastern producers, led by Saudi Arabia, expanded MTBE capacity by 30% over the past five years, leveraging abundant butane and methanol to sustain leadership in merchant trade. Parallel low-carbon initiatives are emerging, with pilot programs for lower-carbon methanol introduced in Q3 2025 to support sustainable-grade MTBE for European and Asian buyers focused on lifecycle emissions.

China: Domestic Efficiency Gains and Integrated Refinery-Petchem Utilization

China’s MTBE landscape is characterized by operational efficiency gains and deepening refinery–petrochemical integration. Production reached 16.02 million metric tons with an operating rate of 61% in recent cycles, the strongest utilization in over six years. Growth is supported by vehicle fleet expansion and demand for high-octane gasoline blends. The SABIC Fujian Petrochemical Complex remains on track for 2026 milestones, embedding MTBE within an integrated C4 and oxygenates platform that aligns with long-term demand resilience.

Policy support remains decisive. The Ministry of Industry and Information Technology 2025–2026 work plan prioritizes green and efficient beneficiation, including MTBE unit upgrades to reduce sulfur and improve isobutylene capture by up to 18%. Price consolidation in December 2025 reflected inventory management and lower crude benchmarks, establishing a pragmatic procurement base for 2026. Tier-1 refiners such as Sinopec and CNPC have lifted refinery–petchem integration to 50%, allocating MTBE internally to premium octane programs that now represent a substantial share of gasoline output.

United States: Export Realignment and Regulatory Certainty

The United States is repositioning MTBE as an export-led oxygenate while maintaining domestic production competitiveness. In August 2025, Mexico surpassed Canada as the largest destination for U.S. MTBE exports, with Gulf Coast refiners responding to Mexico’s growing appetite for high-octane gasoline components. Feedstock volatility eased late in 2025 as acetone and methanol prices declined modestly, supporting competitive export pricing across the Western Hemisphere.

Regulatory clarity is improving planning horizons. The U.S. Environmental Protection Agency finalized a compliance extension to November 2026 for Workplace Chemical Protection Programs affecting high-volume solvents and ethers, including MTBE used in chemical synthesis. Production remains anchored in steam cracker routes, supported by abundant shale-derived NGLs, ensuring consistent availability for export and specialty uses despite shifting domestic fuel additive preferences.

India: Rising Octane Demand and Specialty Feedstock Applications

India’s MTBE trajectory reflects rising octane demand alongside a longer-term clean energy transition. Government targets to lift the share of natural gas and cleaner fuels in the energy mix to 15% by 2030 are translating into steady growth in demand for octane-enhancing additives. MTBE remains integral to this transition in the near term, supporting fuel quality upgrades across the refining system.

At the same time, corporate strategy signals diversification. Reliance Industries Limited is progressing toward a multi-gigawatt electrolyser facility by end-2026, indicating future competition from green oxygenates. Specialty chemical players such as Vinati Organics Limited are expanding R&D in isobutylene derivatives, where MTBE serves as a high-purity feedstock for butyl rubber and methyl methacrylate intermediates, reinforcing demand beyond fuels.

Malaysia and Singapore: Trade Governance and Logistics Standards

Malaysia and Singapore function as critical logistics and price discovery nodes for MTBE flows in Southeast Asia. In December 2025, Malaysia’s Ministry of Investment, Trade and Industry revised Strategic Trade Act directives governing the export and transshipment of controlled chemicals, directly impacting MTBE movements through the Straits of Malacca. These measures elevate compliance requirements for traders and terminal operators.

Market transparency and safety oversight are also tightening. S&P Global updated Platts FOB Straits nomination standards in February 2025, affecting cargo nominations for MTBE and gasoline loading across approved terminals. Singapore’s amendments to workplace safety laws in December 2025 introduced stricter occupational exposure monitoring for volatile ethers, shaping operating practices in refinery and blending environments across the region.

Summary of Country-Level Strategic Positioning in the MTBE Market

Methyl Tertiary Butyl Ether Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Demand Driver

|

Policy or Industry Catalyst

|

Competitive Positioning

|

|

Saudi Arabia

|

Scale expansion and export leadership

|

Global oxygenate trade

|

SABIC–Aramco integration, low-carbon methanol pilots

|

Cost-advantaged global exporter

|

|

China

|

Efficiency and internal utilization

|

High-octane gasoline programs

|

MIIT green beneficiation plan

|

Integrated domestic consumption

|

|

United States

|

Export realignment

|

Mexico gasoline demand

|

EPA WCPP extension

|

Hemisphere-focused supplier

|

|

India

|

Octane growth and feedstock use

|

Cleaner fuels and specialty chemicals

|

Energy mix targets, R&D expansion

|

Emerging diversified demand

|

|

Malaysia & Singapore

|

Trade governance and logistics

|

Regional MTBE flows

|

STA revisions, FOB Straits standards

|

Strategic trading hub

|

Methyl Tertiary Butyl Ether Market Report Scope

Methyl Tertiary Butyl Ether Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.4 Billion

|

|

Market Size (2034)

|

$61.6 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Type (Industrial Grade, Derivative Grade), By Manufacturing Process (Steam Cracker Route, Fluid Catalytic Cracker Route, Isobutane Dehydrogenation Route, Methanol-Based Route), By Application (Gasoline Additives, Isobutene Production, Solvents and Extraction, Chemical Synthesis), By End-Use Industry (Oil and Gas, Automotive, Chemical and Petrochemical, Pharmaceuticals and Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SABIC, Sinopec, Reliance Industries, LyondellBasell Industries, Huntsman Corporation, Petronas, Evonik Industries, China National Petroleum Corporation, Emirates National Oil Company, Enterprise Products Partners, Formosa Plastics, Gazprom Neft, Qatar Fuel Additives Company, Vinati Organics, Panjin Hayen Industrial Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Methyl Tertiary Butyl Ether Market Segmentation

By Type

- Industrial Grade

- Derivative Grade

By Manufacturing Process

- Steam Cracker Route

- Fluid Catalytic Cracker Route

- Isobutane Dehydrogenation Route

- Methanol-Based Route

By Application

- Gasoline Additives

- Isobutene Production

- Solvents and Extraction

- Chemical Synthesis

By End-Use Industry

- Oil and Gas

- Automotive

- Chemical and Petrochemical

- Pharmaceuticals and Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Methyl Tertiary Butyl Ether Market

- SABIC

- Sinopec

- Reliance Industries

- LyondellBasell Industries

- Huntsman Corporation

- Petronas

- Evonik Industries

- China National Petroleum Corporation

- Emirates National Oil Company

- Enterprise Products Partners

- Formosa Plastics

- Gazprom Neft

- Qatar Fuel Additives Company

- Vinati Organics

- Panjin Hayen Industrial Group

*- List not Exhaustive