Microspheres Market Overview: Size, CAGR, and Strategic Insights

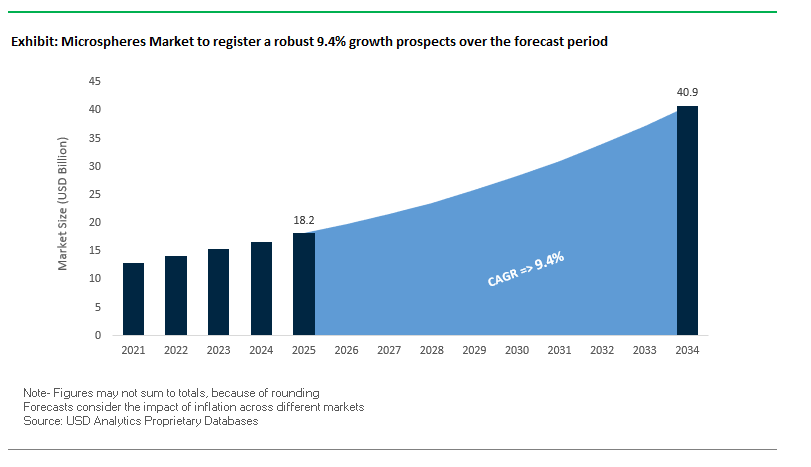

The global Microspheres Market is projected to grow from $18.2 billion in 2025 to $40.9 billion by 2034, representing a CAGR of 9.4%. This growth is fueled by the increasing use of microspheres in lightweight composites, medical technology, and functional fillers. Hollow glass microspheres and polymer variants are widely adopted in automotive, aerospace, construction, and biomedical applications, offering significant advantages in weight reduction, durability, and precision.

Key Insights for Industry Professionals:

- Lightweighting for fuel efficiency: Hollow microspheres reduce material density while maintaining strength, supporting automotive and aerospace sectors in reducing carbon emissions.

- Medical and biotech applications: Microspheres are critical in drug delivery, diagnostics, and tissue engineering, due to their uniform size, high surface area, and biocompatibility.

- Functional fillers in coatings and composites: Ceramic and polymer microspheres enhance paint durability, insulation, and VOC reduction while enabling improved structural performance in construction and industrial applications.

- Sustainable and biodegradable materials: Growing focus on biodegradable microspheres for medical, cosmetic, and packaging applications addresses environmental regulations and reduces plastic waste.

- Cross-sector versatility: Applications span automotive interiors, aerospace composites, electronics, personal care, and oil & gas, highlighting the broad relevance and growth potential of microspheres.

Microspheres Market Analysis: Recent Industry Developments

The microspheres industry has witnessed significant innovations and strategic expansions to meet growing demand across diverse sectors. In August 2025, a Nano Letters study introduced an inhibitor-modified ALD strategy for ultrathin iridium and platinum films, demonstrating potential impacts on next-generation microsphere formulations for electronics. By July 2025, metallized film converters invested in faster, wider coating lines, while material innovators prioritized recycling-ready structures, reflecting a push toward sustainable microsphere integration in advanced materials.

April 2025 marked a major innovation by 3M, which introduced ultra-lightweight polymer microspheres for aerospace-grade composites, enabling significant weight reduction without compromising structural integrity. Earlier in March 2025, 3M launched high-strength glass microspheres for automotive and aerospace applications, further highlighting the focus on lightweight, durable materials. In January 2025, Thermo Fisher Scientific unveiled a next-generation line of polymer-based microspheres for diagnostics and biomedical research, engineered for high surface area and uniformity, improving performance in immunoassays and cell sorting.

Strategic capacity expansions and sustainable innovations have also shaped the market. In November 2024, Nouryon expanded production for expandable polymer microspheres at its Stenungsund, Sweden site, targeting automotive, construction, and packaging applications. In September 2024, Sigmund Lindner GmbH developed biodegradable microspheres for cosmetics and personal care, supporting environmental compliance. Earlier, in January 2024, 3M launched glass microspheres from recycled materials, emphasizing sustainability and energy reduction in automotive and industrial applications.

Trends and Opportunities Driving the Microspheres Market

Strategic Shift to Hollow Glass Microspheres for Automotive and Aerospace Lightweighting

The microspheres market is undergoing a strategic transformation as hollow glass microspheres (HGMs) become integral to automotive and aerospace lightweighting initiatives. In electric vehicles (EVs), where battery packs add significant weight, HGMs provide 10–30% weight savings in composites, dashboards, bumpers, and door panels, directly improving range and energy efficiency. A study revealed that replacing conventional fillers with HGMs achieved a 13% component weight reduction, a crucial benefit for extending EV driving range.

Beyond lightweighting, HGMs enhance thermal and dimensional stability, reduce shrinkage, and provide sound and heat insulation—features highly valued in EV interiors. In aerospace, HGMs are used in syntactic foams and composites for aircraft interiors, satellite structures, and fuselage components, leveraging their high strength-to-weight ratio to lower overall aircraft mass and fuel consumption. Additionally, their low thermal conductivity and flame-retardant properties have made HGMs increasingly relevant for EV battery insulation, where delaying thermal runaway has become a critical safety requirement.

Adoption of Engineered Polymer Microspheres for Sustainable Cosmetic Formulations

The cosmetics sector is driving another major shift in the microspheres market with the adoption of engineered biodegradable polymer microspheres as sustainable alternatives to banned plastic microbeads. Following the EU Commission Regulation (EU) 2023/2055, which began phasing out intentionally added microplastics in rinse-off cosmetics from October 2023, brands are turning to bio-based and naturally derived microspheres.

Corporate initiatives predate regulation: leading beauty companies eliminated polyethylene microbeads as early as 2017, replacing them with ground almond shells, oatmeal, and cocoa husks. Biodegradable polymer microspheres now provide similar sensory, exfoliation, opacity, and controlled-release properties without environmental risks. Scientific reviews further note their ability to enhance sunscreen efficiency, preventing deep skin penetration of UV filters while improving skin coverage. With transitional deadlines extending to 2035 for some categories, the industry is in an accelerated phase of reformulating cosmetics with compliant biodegradable microspheres, making this a major growth driver.

Development of Radioembolization Microspheres for Targeted Cancer Therapy

One of the most promising opportunities lies in the healthcare segment, specifically radioembolization microspheres for cancer therapy. These are precisely engineered glass or resin microspheres embedded with yttrium-90 (Y-90), which are delivered directly to tumors via arteries supplying blood to the cancer. Known as Selective Internal Radiation Therapy (SIRT), this technique ensures radiation penetrates just a few millimeters, providing a high dose to the tumor while sparing healthy tissue.

Clinical evidence underscores its efficacy. Boston Scientific’s TheraSphere™ Y-90 Glass Microspheres demonstrated in the TARGET study (2021) that higher radiation doses to tumors correlated with better survival outcomes. Already FDA-approved for hepatocellular carcinoma (HCC), this therapy is expanding to other cancers, making it a high-value niche. With increasing cancer incidence globally and rising adoption of interventional oncology, demand for radioembolization microspheres is set to accelerate, creating a premium growth segment in the microspheres market.

Utilization of Expandable Microspheres as a Blowing Agent in Sustainable Construction Materials

In construction, expandable microspheres are opening opportunities for sustainable building materials by replacing conventional chemical blowing agents. These polymer-based spheres expand when heated, reducing density and introducing closed-cell structures that enhance thermal insulation. Even a 0.5–4.0% addition by weight can significantly reduce the density of plasters, mortars, and wood-plastic composites, making them lighter and easier to transport.

The closed-cell morphology improves energy efficiency in buildings by lowering heat transfer, aligning with sustainability regulations and green building certifications. Furthermore, the ball-bearing effect of microspheres enhances workability, producing mortars and plasters with a “creamy, butter-like consistency” that are easier to spread, sand, and finish, ultimately reducing labor costs. As construction industries worldwide shift toward low-carbon, lightweight, and energy-efficient solutions, expandable microspheres are emerging as a key material for the next generation of sustainable construction products.

Competitive Landscape: Leading Players in the Global Microspheres Market

The microspheres market is characterized by advanced material innovation, lightweighting solutions, and sustainability initiatives, with leading companies driving growth through product development, capacity expansion, and application diversification.

3M: Innovating Lightweight and High-Performance Microspheres

3M offers a wide portfolio of glass, ceramic, and polymer microspheres, catering to aerospace, automotive, and construction sectors. In April 2025, 3M introduced ultra-lightweight polymer microspheres for aerospace-grade composites, achieving significant weight reduction while maintaining structural integrity. 3M’s products, including 3M™ Glass Bubbles and 3M™ Ceramic Microspheres, enhance durability, reduce density, and improve processability for high-value applications, reflecting the company’s focus on performance and materials science innovation.

Nouryon: Expanding Capacity for Sustainable Expandable Microspheres

Nouryon, formerly AkzoNobel Specialty Chemicals, provides Expancel® expandable polymer microspheres widely used in automotive, packaging, and construction applications. In November 2024, Nouryon expanded production at its Stenungsund, Sweden facility to meet rising demand. The company focuses on sustainable, high-performance solutions, enabling customers to reduce material usage, lower costs, and improve environmental performance.

Thermo Fisher Scientific Inc.: Advanced Microspheres for Life Sciences

Thermo Fisher Scientific offers polymer-based microspheres for diagnostics, biomedical research, and molecular applications. In January 2025, it introduced a next-generation line engineered for high surface area and uniformity, enhancing performance in immunoassays and molecular diagnostics. The company’s portfolio, including Dynabeads™, supports cell isolation, protein purification, and life science R&D, emphasizing precision, reliability, and biocompatibility.

Sigmund Lindner GmbH: Biodegradable Microspheres for Personal Care

Sigmund Lindner GmbH specializes in precision-manufactured glass, ceramic, and biodegradable microspheres. In September 2024, the company launched biodegradable microspheres for cosmetic and personal care applications, addressing environmental regulations and consumer sustainability demand. Its expertise ensures high-quality, customizable microspheres suitable for demanding applications across medical, cosmetic, and industrial sectors.

Momentive: High-Performance Ceramic Microspheres for Industrial Applications

Momentive provides hollow ceramic microspheres for electronics, industrial, and advanced composite applications. In April 2024, the company launched a new line with superior thermal resistance, low dielectric constant, and lightweight properties, ideal for adhesives, sealants, and high-temperature composites. Momentive focuses on innovative solutions for high-tech industries, supporting demand for lightweight, durable, and high-performance materials.

Microspheres Market Share Insights

Hollow Microspheres Dominate Market Share by Type in the Microspheres Industry

Hollow microspheres account for 62% of the global microspheres market, making them the performance and efficiency leader across multiple industries. Their dominance is attributed to the unique hollow-core structure, which delivers ultra-low density while maintaining mechanical integrity, enabling significant weight reduction in composites, plastics, and coatings. This property makes hollow microspheres indispensable in construction composites, lightweight cement, and advanced automotive and aerospace materials, where weight savings directly translate into cost reduction and improved energy efficiency. They also enhance thermal insulation, sound damping, and dimensional stability, making them a preferred solution for both industrial and consumer applications. Solid microspheres, while valued for compressive strength and functional properties in coatings, putties, and medical scaffolds, remain a specialized segment compared to the widespread adoption of hollow microspheres in high-volume lightweighting applications.

Construction Composites Lead Market Share by Application in the Microspheres Industry

Construction composites command 30% of the microspheres market, reflecting the material’s critical role in large-scale infrastructure and building applications. Hollow glass microspheres and cenospheres derived from fly ash are extensively used in lightweight concrete, mortars, wall panels, and FRP composites, delivering improved thermal insulation, reduced density, and enhanced workability. Their use lowers overall material consumption and transportation costs while maintaining structural integrity, aligning directly with global sustainability and cost-efficiency mandates in the construction sector. This segment benefits from massive demand in emerging economies, where urbanization and infrastructure development drive the need for high-performance yet cost-effective building materials. While applications in paints, coatings, and medical technology are technologically advanced and high-margin, the scale and consistency of construction demand cement this segment as the largest contributor to microsphere consumption worldwide.

United States: Regulatory Leadership and Innovation Driving Microspheres Demand

The United States microspheres market is shaped by a strong regulatory framework and rapid technological advancements, particularly in healthcare and advanced manufacturing. Agencies like the Food and Drug Administration (FDA) and Environmental Protection Agency (EPA) play a crucial role, with the FDA accelerating approvals for advanced drug delivery technologies, creating significant opportunities for microspheres in targeted drug delivery, tissue engineering, and medical imaging. The U.S. is also witnessing the emergence of smart microspheres infused with diagnostic and sensor properties, enabling applications in environmental monitoring and manufacturing quality control. In October 2021, Silgan Holdings’ acquisition of Gateway Plastics highlighted how corporate investments are expanding product portfolios with microcellular and microsphere-integrated solutions.

Key end-use industries such as healthcare, biotechnology, automotive, and aerospace are fueling demand, particularly for lightweighting solutions that enhance fuel efficiency and performance. Moreover, sustainability is becoming a central theme in the U.S. microspheres industry, with manufacturers adopting renewable raw materials and advanced formulation technologies to comply with environmental regulations and consumer demand for eco-friendly solutions. These trends position the U.S. as a global leader in both innovation and adoption of microspheres across diverse sectors.

Germany: Stringent Regulations and Industry 4.0 Fuel Microspheres Innovation

Germany’s microspheres market is driven by a stringent regulatory landscape aligned with the European Union’s Circular Economy Action Plan, which emphasizes recyclability and material efficiency. This has pushed manufacturers to adopt circular economy-compatible microsphere technologies designed for sustainability. Complementing this, Germany’s strong commitment to advanced manufacturing under “Plattform Industrie 4.0” has enabled the integration of microspheres into high-tech, automated production systems.

German companies are recognized globally for pioneering advanced foaming and material-shaping technologies. For example, Borealis’ €100 million investment in Burghausen to triple capacity for recyclable foam-based polypropylene demonstrates the country’s commitment to lightweight, high-performance materials that directly overlap with microsphere applications. Supported by over 75 research institutes collaborating with industry, Germany has become a hub of plastics R&D, ensuring continuous innovation across the microspheres value chain. The automotive industry remains the largest consumer, using microspheres in components like jounce bumpers and coil spring isolators, while the construction sector relies on them for insulation and lightweight building materials.

China: Government Support and High-Tech Manufacturing Driving Microspheres Growth

China’s microspheres market is expanding rapidly, underpinned by strong governmental initiatives and industrial policies. Programs like the “Opinions on Further Strengthening the Control of Plastic Pollution” emphasize reducing plastic waste, which is fueling the adoption of advanced, lightweight materials such as microspheres. Governmental support for high-end manufacturing is channeling investments into developing sustainable, high-performance plastics that align with the country’s circular economy goals.

Technological innovation is another critical factor, as Chinese manufacturers integrate automation and artificial intelligence to improve efficiency and precision in microspheres production. The nation’s growing automotive, electronics, and construction industries are primary consumers, while pharmaceutical research partnerships are pushing the development of multifunctional microspheres with targeting, sensing, and controlled release properties. While exact investment figures are not widely disclosed, the scale of government backing and private sector growth highlights robust capital flow into microspheres, ensuring China remains a powerhouse in both production and consumption.

India: Government Policies and Rising R&D Investments Boost Microspheres Market

The Indian microspheres market is benefitting significantly from national initiatives such as “Make in India” and the Production Linked Incentive (PLI) scheme, which are encouraging localized manufacturing of advanced materials. The Central Pollution Control Board (CPCB) has also introduced Extended Producer Responsibility (EPR) mandates for plastic-based medical devices and packaging, indirectly driving demand for sustainable microsphere solutions that align with circular economy goals.

Technological advancements are gaining momentum in India, particularly in paints, coatings, flexible packaging, and consumer electronics. A notable example came in June 2024, when Uflex Ltd. launched a line of barrier-coated, paper-based micro-perforated packaging formats to reduce plastic dependency in food and beverage sachets. On the corporate side, international players are increasing investments, with Potters Industries establishing a facility in India to manufacture hollow glass microspheres for aerospace insulation applications. These developments position India as a fast-emerging hub for microspheres innovation and sustainable adoption, supported by rising domestic demand and international collaborations.

Japan: Automotive Lightweighting and Recycled Plastics Integration Strengthening Microspheres Applications

Japan’s microspheres market is characterized by strong government-industry-academia collaboration. In late 2024, the government launched the Industry-Government-Academia Consortium for Recycled Plastics in Automotive Applications, which is accelerating the use of recycled microsphere-based materials. This initiative aligns with the country’s long-standing focus on reducing plastic waste while maintaining high material performance.

Japanese automakers like Toyota and Honda are spearheading efforts to integrate microsphere-enhanced recycled plastics into vehicles, with Honda and Sumitomo Chemical co-developing polypropylene-based recycled plastics that meet high standards for durability and appearance. Lightweighting remains a dominant trend, as microspheres help manufacturers reduce vehicle weight, improve fuel efficiency, and comply with strict emissions regulations. While automotive remains the largest sector, Japan’s material innovation capabilities ensure that microspheres are also finding applications across medical devices, electronics, and construction materials, solidifying its role as a leader in advanced microsphere utilization.

Microspheres Market Report Scope

Microspheres Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.2 Billion

|

|

Market Size (2034)

|

$40.9 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Type (Hollow Microspheres, Solid Microspheres), By Material (Glass, Ceramic, Fly Ash, Polymer, Metallic, Others), By Application (Construction Composites, Medical Technology, Life Science & Biotechnology, Paints & Coatings, Cosmetics & Personal Care, Oil & Gas, Automotive, Aerospace, Others), By End-User (Automotive Manufacturers, Building & Construction Companies, Healthcare & Pharmaceutical Companies, Paints & Coatings Manufacturers, Cosmetics & Personal Care Companies, Aerospace & Defense Companies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Trelleborg AB, Nouryon Chemicals Holding B.V., Kureha Corporation, Mo-Sci Corporation, Chase Corporation, Matsumoto Yushi-Seiyaku Co. Ltd., Sekisui Chemical Co. Ltd., Luminex Corporation, Bangs Laboratories, Inc., Cospheric LLC, Potters Industries LLC, Shin-Etsu Chemical Co., Ltd., Sigmund Lindner GmbH, Sphere One, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Microspheres Market Segmentation

By Type

- Hollow Microspheres

- Solid Microspheres

By Material

- Glass

- Ceramic

- Fly Ash

- Polymer

- Metallic

- Others

By Application

- Construction Composites

- Medical Technology

- Life Science & Biotechnology

- Paints & Coatings

- Cosmetics & Personal Care

- Oil & Gas

- Automotive

- Aerospace

- Others

By End-User

- Automotive Manufacturers

- Building & Construction Companies

- Healthcare & Pharmaceutical Companies

- Paints & Coatings Manufacturers

- Cosmetics & Personal Care Companies

- Aerospace & Defense Companies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

·Top Companies in Microspheres Market

- 3M Company

- Trelleborg AB

- Nouryon Chemicals Holding B.V.

- Kureha Corporation

- Mo-Sci Corporation

- Chase Corporation

- Matsumoto Yushi-Seiyaku Co. Ltd.

- Sekisui Chemical Co. Ltd.

- Luminex Corporation

- Bangs Laboratories, Inc.

- Cospheric LLC

- Potters Industries LLC

- Shin-Etsu Chemical Co., Ltd.

- Sigmund Lindner GmbH

- Sphere One, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and systematic research methodology to deliver precise, actionable insights into the global Microspheres Market. Our process integrates primary research through interviews with materials scientists, biomedical engineers, automotive and aerospace manufacturers, and chemical industry stakeholders, combined with extensive secondary research from corporate reports, regulatory publications, patent filings, scientific journals, and market databases. We analyze key drivers including hollow glass microspheres for lightweighting, biodegradable polymer microspheres for cosmetics, radioembolization microspheres in healthcare, and expandable microspheres in construction. Market sizing and forecasts are developed using advanced quantitative modeling, incorporating CAGR trends, regional adoption patterns across North America, Europe, and Asia-Pacific, and competitive dynamics involving industry leaders such as 3M, Nouryon, Thermo Fisher Scientific, and Sigmund Lindner. Strategic developments, including technological innovations, sustainability initiatives, and capacity expansions, are carefully assessed to highlight growth opportunities, material-specific performance, and regulatory impacts. This methodology ensures USDAnalytics provides industry professionals with accurate, data-driven intelligence to inform strategic planning, investment decisions, and technology adoption in the evolving microspheres landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.