Market Overview: Ultra-Low Friction, 2D Semiconductor Potential, and High-Purity Catalysts Drive the Global Mos₂ Market Outlook

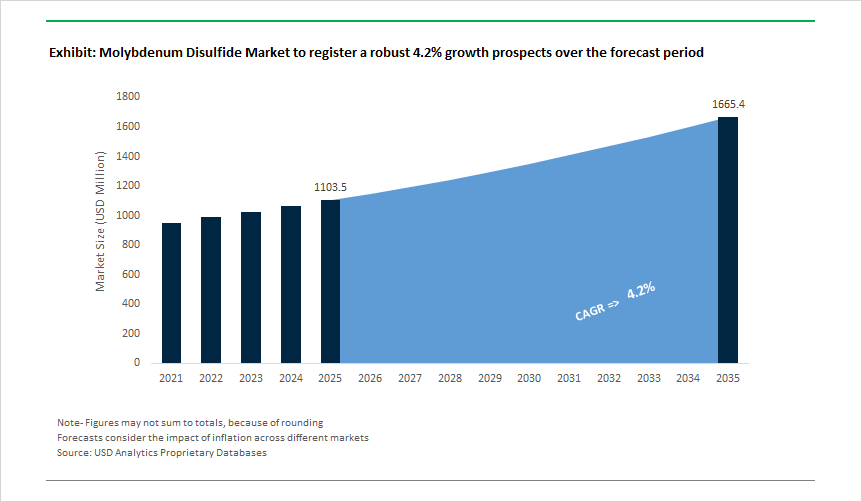

The Global Molybdenum Disulfide (MoS₂) Market is valued at USD 1.10 billion in 2025 and is projected to reach USD 1.67 billion by 2035, growing at a 4.2% CAGR as MoS₂ continues to occupy a rare dual position: a mission-critical industrial material with entrenched demand, and a future-facing functional material with upside optionality. Unlike many advanced materials markets that rely on speculative adoption, MoS₂’s growth is anchored in applications that already justify procurement at scale.

At its core, the market is sustained by industrial reliability requirements. MoS₂ has long been specified in automotive, heavy machinery, aerospace, mining, and defense because it delivers consistent performance under conditions where conventional lubricants fail-high load, extreme pressure, vacuum, and wide temperature ranges. For OEMs and operators, MoS₂ is not a performance upgrade; it is a risk-mitigation material that reduces wear, extends maintenance intervals, and protects critical components. This explains why over 40% of machinery and automotive manufacturers continue to specify MoS₂-based formulations despite the availability of alternative additives.

A second, structurally stable demand pillar comes from energy and refining infrastructure. High-purity MoS₂ is embedded in hydrodesulfurization (HDS) catalysts, which are essential for meeting global fuel sulfur regulations. These catalysts are not discretionary: they are required for regulatory compliance and refinery uptime. As fuel quality standards tighten and refining assets operate longer, demand for ≥99.9% purity MoS₂ remains predictable and recurring, providing a steady baseline for the market independent of industrial cycles.

Where MoS₂ becomes strategically interesting is in its technology optionality. In recent years, MoS₂ has attracted sustained R&D investment as a 2D semiconductor and advanced functional material, opening potential pathways into flexible electronics, coatings, sensors, and next-generation energy storage. While these segments are not yet volume drivers, they represent asymmetric upside: relatively small adoption can materially lift market value because of higher margins and tighter specifications. For suppliers, this creates a barbell market structure-stable cash flows from industrial uses on one side, and higher-risk, higher-value innovation on the other.

Battery and energy-storage research further reinforces this optionality. MoS₂ is increasingly evaluated as an enabling material in advanced battery architectures and protective coatings, not because it replaces incumbent materials overnight, but because it improves system performance at the margin-a pattern consistent with how many materials scale into commercial relevance over time.

Market Analysis: Nano-Mos₂ Commercialization, Catalyst Supply Security, and 2D Electronics Innovation Accelerate Progress

The Molybdenum Disulfide market experienced notable momentum, with commercialization of nanomaterials, advancements in semiconductor manufacturing, and significant supply-chain policy actions. In December 2025, a major global chemical supplier launched next-generation Nano-MoS₂ dispersions designed for enhanced stability in synthetic oils-an important step toward integrating MoS₂ into advanced automotive powertrains and e-mobility platforms. Breakthrough semiconductor innovations were reported in November 2025, when MIT scientists announced a new CVD method enabling large-scale MoS₂ placement in flexible electronic circuits, signaling major progress toward manufacturable 2D semiconductor devices. Chinese industrial policy further reshaped supply dynamics in September 2025, when the Ministry of Industry and Information Technology emphasized accelerated investment in domestic molybdenum refining, targeting secure feedstock for HDS catalyst production.

Battery materials also gained attention: in July 2025, Plansee Group partnered with a European battery manufacturer to scale high-purity MoS₂ production for solid-state battery protective interlayers, a niche where MoS₂’s mechanical resilience and chemical stability provide competitive value. Similarly, in May 2025, a specialty coatings company introduced MoS₂/WS₂ hybrid coatings, combining the extreme pressure resistance of MoS₂ with the thermal stability of WS₂ for heavy-duty machinery applications. The electronics sector advanced further in March 2025, when a leading South Korean firm filed patents for monolayer MoS₂ integration in flexible transistor arrays-a key milestone toward commercial 2D material devices. Global standardization followed in January 2025, with the International Tribology Council issuing updated certification standards for Nano-MoS₂ aerospace greases, formalizing purity, morphology, and particle-size requirements.

Supply chain strengthening was also evident. In November 2024, Freeport-McMoRan expanded processing capabilities in Chile and the U.S. to increase output of molybdenite concentrates-a critical precursor for MoS₂ production.

Molybdenum Disulfide Market Trends and Opportunities

Trend 1: Solid Lubricant Integration in Long-Life Space Mechanisms

Space agencies and aerospace OEMs are increasingly standardizing molybdenum disulfide (MoS₂) as a mission-critical solid lubricant for deployable space mechanisms, reflecting a broader shift away from organic oils that cannot survive vacuum, radiation, and extreme thermal cycling. Technical reviews published during 2024–2025 consistently demonstrate that MoS₂ coatings deliver an exceptionally low coefficient of friction—typically ranging from 0.002 to 0.2 under high-vacuum conditions—while remaining structurally stable at temperatures approaching 1,000°C. This performance profile makes MoS₂ indispensable for actuators, bearings, antenna gimbals, and reaction-wheel assemblies designed for 15–20+ year mission lifetimes, where re-lubrication is impossible. A critical advancement supporting wider adoption has been the qualification of doped MoS₂ variants, co-sputtered with elements such as titanium, nickel, or gold. These dopants significantly suppress oxidation and humidity-driven degradation during ground handling and pre-launch storage, preserving the layered crystal structure that enables low-shear behavior once deployed in orbit. By 2025, aerospace coating standards had converged around tightly controlled sputtered film thicknesses—typically 50 to 250 micro-inches—applied to precision components manufactured from 440C stainless steel and high-strength aluminum alloys. This level of process control is now considered essential for zero-failure operation in systems such as ISS flywheel assemblies and deep-space probe mechanisms, anchoring MoS₂’s position as a non-substitutable lubricant material in the space economy.

Trend 2: Wafer-Scale 2D MoS₂ Films for Sub-1nm Logic Transistors

In parallel with its mechanical applications, MoS₂ is emerging as a strategic electronic material as the semiconductor industry confronts the physical limits of silicon scaling. During 2025, multiple research groups reported decisive progress in 300 mm wafer-scale synthesis of monolayer MoS₂ using atmospheric-pressure chemical vapor deposition (CVD), overcoming one of the most persistent barriers to industrial adoption. These processes have demonstrated uniform thickness and electrical consistency across full wafers, meeting the baseline manufacturability thresholds required for pilot-line integration. Equally important, the thermal budget for MoS₂ growth has fallen below 300°C, enabling direct deposition on completed CMOS stacks without damaging underlying interconnects—an essential requirement for back-end-of-line compatibility. Electrical characterization of these films shows current on/off ratios exceeding 10⁶ and carrier mobility sufficient for sub-1 nm gate-all-around (GAA) architectures, positioning MoS₂ as a credible successor channel material where silicon FinFETs fail due to leakage and short-channel effects. Foundry engagement has moved beyond academic proof-of-concept. Throughout 2024–2025, leading manufacturers have published data on contact engineering strategies—such as bilayer alloy contacts and phase-controlled interfaces—that reduce contact resistance to approximately 98 Ω·μm, addressing the long-standing injection barrier challenge associated with 2D materials. Collectively, these advances indicate that MoS₂ is transitioning from a research novelty to a foundry-relevant semiconductor material, directly aligned with next-generation logic roadmaps.

Opportunity 1: Dry Film Lubricants for Green Hydrogen Electrolyzer Assembly

The rapid scale-up of green hydrogen infrastructure is creating a volume-driven opportunity for MoS₂ as a non-contaminating dry film lubricant in electrolyzer manufacturing. Proton exchange membrane (PEM) and alkaline electrolyzers rely on high clamping forces during stack assembly, where metal-to-metal contact between bipolar plates, fasteners, and frames can lead to galling and uneven torque distribution. MoS₂ coatings are increasingly specified at these interfaces because they provide consistent friction behavior without introducing organic residues that could poison platinum-group metal catalysts. Unlike conventional greases, MoS₂ remains chemically inert in the highly acidic environments typical of PEM electrolyzers and retains both lubricity and electrical conductivity after thousands of operational hours. This stability is critical as manufacturers pursue longer stack lifetimes and higher current densities to meet aggressive cost-reduction targets for hydrogen production. From a manufacturing perspective, the shift toward burnished and resin-bonded MoS₂ coatings supports high-speed, automated assembly lines by delivering repeatable torque–tension relationships, directly improving seal integrity and reducing leak-related rework. As electrolyzer production moves from bespoke fabrication to gigawatt-scale industrialization, MoS₂ is becoming embedded as a process-enabling material rather than a discretionary coating choice.

Opportunity 2: Functional Cathode and Anode Additive for Next-Generation Batteries

Engineered MoS₂ is also opening high-value opportunities in next-generation battery chemistries where conventional carbon materials struggle to meet durability and kinetic requirements. In lithium–sulfur (Li–S) systems, one of the primary commercial barriers is the polysulfide “shuttle effect,” which causes rapid capacity decay. Research published during 2024–2025 demonstrates that metallic 1T-phase MoS₂ nanosheets act as strong chemical anchors for soluble polysulfides, reducing capacity fade to as little as 0.052% per cycle over 800 cycles—a performance level approaching commercial viability for batteries targeting >400 Wh/kg energy density. In sodium-ion batteries, MoS₂’s naturally expanded interlayer spacing offers a structural advantage over graphite. Nano-engineered MoS₂ morphologies with interlayer distances around 0.66 nm enable efficient sodium-ion intercalation, delivering discharge capacities of ~350 mAh/g and strong rate capability under fast-charging conditions. Further performance gains are being realized through MoS₂/graphene heterostructures, which enhance electronic conductivity and mitigate mechanical stress during repeated cycling. These hybrids are particularly attractive for flexible and wearable electronics, where electrodes must endure thousands of deformation cycles without electrical failure. Together, these developments position MoS₂ as a multifunctional electrochemical material, bridging energy density, cycle life, and mechanical resilience across emerging battery platforms.

Market Share Analysis: Molybdenum Disulfide (MoS₂) Market

Market Share by Product Form: Powder-Grade MoS₂ Anchors Performance-Critical Lubrication Demand

Powder-grade molybdenum disulfide commands approximately 45% of global market share because it is the most adaptable and performance-reliable format for extreme-pressure lubrication, grease compounding, and solid-film coatings across heavy industry. Its leadership is rooted in consistency and controllability at scale: flagship products from Climax Molybdenum deliver ~98% purity, a threshold buyers treat as non-negotiable for predictable tribological behavior under boundary and mixed-lubrication regimes. Market momentum in 2025 is concentrated in Super Fine and Technical Fine powders (D50 ≈ 0.9–1.6 μm), which disperse uniformly in synthetic oils and enable thinner, defect-free coatings for aerospace and precision machinery—applications where agglomeration directly translates into wear risk. Pricing stability reinforces adoption: Centerra Gold reported an average realized molybdenum price of $21.59/lb (Q3 2025) alongside higher roasting volumes, signaling supply adequacy for powder-based downstream products despite broader metals volatility. Critically, powder-grade MoS₂ offers thermal resilience up to ~450°C in air (and far higher in inert conditions), a property validated by suppliers such as Tribotecc. This “thermal insurance” keeps powder-grade MoS₂ entrenched ahead of graphite or PTFE in high-load gearboxes, compressors, and steel processing lines—explaining why it remains the market’s industrial default rather than a specialty alternative.

Market Share by Product Form, 2025.png)

Market Share by Application: Automotive Demand Sustained by EV-Era Boundary Lubrication

Automotive applications account for around 32% of MoS₂ consumption, sustained not only by legacy internal combustion platforms but increasingly by the mechanical realities of electric vehicles. Contrary to the assumption that EVs reduce lubricant intensity, OEM and Tier-1 requirements now mandate MoS₂-enhanced greases for high-speed bearings, e-axles, and auxiliary systems that operate at higher RPMs and are expected to deliver lifetime lubrication. Performance benchmarks from Molykote demonstrate friction coefficients as low as 0.05 in steering and joint assemblies, translating directly into efficiency gains—fuel economy for ICE vehicles and incremental range for EVs. Product strategy data from 2025 shows a structural pivot: ~36% of new MoS₂ lubricant formulations are EV-specific, reflecting requirements for low noise, low torque loss, and thermal stability under sustained electrical loads. Powder-grade MoS₂ also remains indispensable during cold-start and boundary lubrication events, where oil films are incomplete; OEM testing attributes 15–20% extensions in component life to MoS₂’s ability to prevent metal-to-metal contact in these transient conditions. Together, these factors explain why automotive remains the largest single application segment and why MoS₂ demand is proving resilient—even as propulsion technologies evolve—by aligning directly with durability, efficiency, and total cost of ownership drivers.

Competitive Landscape: Integrated Miners, Nanomaterial Innovators, and Specialty Lubricant Manufacturers Shape Global Mos₂ Leadership

The Molybdenum Disulfide industry is defined by vertically integrated mining companies, high-purity powder producers, and innovators in nanomaterial engineering. Competitive advantages are increasingly tied to advanced purification, particle-size control, surface modification, and the ability to supply tailored MoS₂ for lubricants, catalysts, semiconductor films, and next-generation energy materials. Companies that can bridge mining-scale supply with nano-grade specialization are best positioned for long-term leadership.

Climax Molybdenum - Global Molybdenum Leader Supplying Multi-Grade Mos₂ For Lubricants and Catalysts

Climax Molybdenum, a Freeport-McMoRan subsidiary, is one of the most influential players in the molybdenum value chain, offering Technical, Technical Fine, and Super Fine grades of Molysulfide® MoS₂ with D99 particle sizes between 7.0 μm and 1.6 μm. Its vertically integrated supply-from mine to refined powder-ensures stable and consistent quality, especially for industrial grease and heavy-duty lubrication markets. The company maintains strict impurity thresholds, including Fe content capped at 0.25% for technical grades, supporting performance-critical lubrication. Ongoing R&D focuses on refining MoO₃ intermediates with low impurity content, strengthening its strategic role in HDS catalyst precursor markets.

H.C. Starck Solutions - High-Purity Mos₂ and Nanomaterial Specialist For Electronic and Aerospace Applications

H.C. Starck Solutions is a leading producer of ultra-high-purity MoS₂ powders used in thin-film deposition, advanced tribology systems, and semiconductor applications. The company invests heavily in synthesizing MoS₂ nanomaterials for 2D electronics and flexible optoelectronics. Its development of Molybdenum Tungsten Disulfide (MoWS₂) hybrid powders enhances thermal stability and wear resistance in aerospace coatings. With production facilities across Germany, Canada, and China, H.C. Starck maintains a resilient global supply chain serving high-specification lubricant and electronic material markets.

Jinduicheng Molybdenum Co., Ltd. - China’s Leading Molybdenum Producer Expanding HDS Catalyst Precursor Output

Jinduicheng is one of the world’s largest producers of molybdenite concentrate, supplying essential raw material for MoS₂ manufacturing. The company is expanding its molybdenum chemical division to increase production of HDS catalyst precursors, supporting Asia’s clean-fuel regulations. Beyond catalyst applications, JDC provides MoS₂ powder for industrial lubricants, friction materials, and export markets. Its planned investments in micronization technology aim to provide finer MoS₂ grades tailored for nano-coating and high-performance lubrication applications.

Rose Mill Co. - Specialty Lubricant Formulator Delivering Engineered Mos₂ Dispersions and Pastes

Rose Mill specializes in converting MoS₂ powder into high-performance lubricant pastes, sprays, and grease additives meeting stringent MIL-SPEC and aerospace requirements. The company’s expertise lies in improving MoS₂ dispersion, adhesion, and compatibility with oils and binders. Recent innovation efforts include low-VOC aqueous Nano-MoS₂ dispersions for eco-friendly coatings. Rose Mill’s ability to provide custom blending and particle-size configurations makes it an essential partner for OEMs requiring precise lubrication performance across metalworking, automotive, and aerospace environments.

The United States is repositioning the molybdenum disulfide market around supply chain resilience and defense-grade material security. According to the U.S. Geological Survey, domestic molybdenum mine output reached ~44,600 tonnes in 2024–2025, valued at roughly $800 million, reflecting productivity gains from optimized recovery at primary molybdenum mines and large copper byproduct operations. This production base is increasingly being aligned with downstream upgrading, as federal policy shifts away from exporting concentrates toward 99.9% high-purity MoS₂ powders suitable for aerospace dry-film lubricants and emerging semiconductor applications.

A central industrial anchor remains Freeport-McMoRan, which in late 2025 reaffirmed its multi-year operational strategy following temporary disruptions at its Indonesian assets. The company’s Morenci district in Arizona continues to function as a cornerstone of U.S. molybdenum concentrate supply, feeding domestic refining ambitions. Parallel to mining, Defense Production Act (DPA) programs are actively supporting projects that convert molybdenite into ultra-high-purity MoS₂, signaling a clear U.S. intent to decouple advanced electronics and defense lubrication systems from East Asian refining dependence.

China – Export Retrenchment and Environmental Consolidation

China remains the world’s largest producer and consumer of molybdenum, but its 2025 trajectory reflects a decisive pivot from volume exports to domestic value preservation and regulatory tightening. Customs data from the General Administration of Customs show that cumulative molybdenum product exports fell 22.2% year-on-year (Jan–Nov 2025) to 30,187.77 tonnes, while imports of roasted molybdenum ores and concentrates surged 150.5%. This asymmetry underscores Beijing’s strategy of conserving high-grade domestic reserves while feeding downstream processors with imported raw material.

Environmental consolidation has further reshaped supply. Intensified inspections by the Ministry of Industry and Information Technology in Henan and Shaanxi provinces curtailed output from older, less compliant operations. As a result, global markets have seen firmer price floors for high-purity MoS₂ powders, particularly those used in specialty steel additives, EV greases, and heavy machinery lubrication. Internally, China’s push for green specialty steel continues to absorb large volumes of MoS₂ as a friction-reducing and wear-resistant additive.

Chile – Byproduct Scale and Structural Mining Projects

Chile’s importance in the molybdenum disulfide market is intrinsically linked to its dominance in global copper production, where molybdenum is recovered as a strategic byproduct. In 2025, CODELCO reported a 9.6% year-on-year increase in total output (including affiliates) during H1, despite operational disruptions caused by a seismic event at El Teniente in July. By Q4 2025, approximately 80% of capacity had been restored, stabilizing molybdenum concentrate availability for export and domestic processing.

The Rajo Inca structural project in Salvador reached its final ramp-up phase in late 2025, reinforcing Chile’s role as a long-term, low-cost supplier of molybdenum concentrates for lubricant, catalyst, and metallurgical markets. At the policy level, Chile’s forthcoming Strategic Minerals Strategy—covering 51 mining projects and over $83 billion in planned investment through 2033—signals sustained support for molybdenum as a companion metal essential to future-facing industrial value chains.

Australia – AI-Led Exploration and Critical Minerals Consolidation

Australia is emerging as a high-potential frontier for molybdenum disulfide, driven by technology-enabled exploration and project consolidation. A defining transaction in 2025 was Tivan Ltd’s acquisition of the Molyhil tungsten–molybdenum project for $8.75 million, establishing a vertically integrated critical minerals hub in the Northern Territory. This move aligns with Canberra’s broader strategy of building ex-China supply chains for clean energy and industrial metals.

The Northern Territory alone hosted 19 developing mining projects with a combined CAPEX of $6.6 billion as of October 2025, while total mineral production value reached $4.36 billion in FY 2024–25. Complementing traditional geology, AI-driven explorers such as Earth AI identified new mineralized systems at Willow Glen, illustrating how machine-learning exploration is unlocking molybdenum-bearing deposits previously overlooked—particularly those suited for high-tech, high-purity MoS₂ applications.

Canada – Clean Energy Materials and Recovery Optimization

Canada is reframing molybdenum disulfide as a clean energy enabler, tightly integrated into North America’s battery, wind energy, and semiconductor ecosystems. Through the Critical Minerals Infrastructure Fund, Ottawa is accelerating molybdenum recovery projects that support both renewable energy and advanced manufacturing. In 2025, Canadian copper producers implemented upgraded flotation circuits that improved molybdenum recovery rates by ~15%, enhancing feedstock availability for downstream MoS₂ conversion.

From an application perspective, MoS₂ demand is expanding in wind turbine gearboxes, where dry-film lubricants improve efficiency and reduce maintenance, and in aerospace components, where low-profile solid lubricants are increasingly specified. Canada’s regulatory stability and clean-energy alignment position it as a reliable midstream supplier of high-quality MoS₂ to U.S. and European OEMs.

Indonesia – Grasberg Recovery and Downstream Integration

Indonesia’s role in the molybdenum disulfide market is closely tied to the operational recovery of its copper–gold megaprojects. In November 2025, PT Freeport Indonesia announced plans to restore large-scale production at the Grasberg Block Cave following the September mud rush incident. Phased ramp-up is expected to begin in Q2 2026, with average annual output for 2027–2029 projected to exceed historical levels, reinforcing Indonesia’s byproduct molybdenum supply.

Policy-wise, Jakarta continues to enforce downstream smelting and refining mandates, compelling miners to process concentrates domestically. This approach is gradually transforming Indonesia from a raw-material exporter into a processing hub for molybdenum-bearing intermediates, particularly for electronics, chemical catalysts, and specialty lubricants destined for Asian manufacturing centers.

2025 Strategic Matrix: Molybdenum Disulfide National Benchmarking

Molybdenum Disulfide National Benchmarking

|

Country

|

Primary Strategic Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

United States

|

Supply resilience

|

~44.6 kt mine output (USGS)

|

Defense & aerospace lubricants

|

|

China

|

Regulatory control

|

22.2% export drop / 150.5% ore import surge

|

Specialty steel & EV greases

|

|

Chile

|

Structural mining projects

|

$83B mining investment pipeline

|

Metallurgical & chemical grades

|

|

Australia

|

AI-led exploration

|

Tivan acquisition of Molyhil

|

High-load industrial machinery

|

|

Canada

|

Clean energy transition

|

Infrastructure Fund–backed recovery upgrades

|

Wind turbines & clean tech

|

|

Indonesia

|

Operational recovery

|

Grasberg Block Cave restart planning

|

Byproduct refining & electronics

|

Molybdenum Disulfide Market Report Scope

Molybdenum Disulfide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1103.5 Million

|

|

Market Size (2035)

|

$1665.1 Million

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Product Form (Powder Grade, Dispersions, Granules, Suspensions & Pastes, Sputtered Films & Coatings), By Purity Grade (Technical, High Purity, Electronic Grade), By Application (Lubricants & Greases, Semiconductors & Electronics, Energy Storage, Coatings & Additives, Catalysts, Additive Manufacturing), By End-User Industry (Automotive, Aerospace & Defense, Industrial Machinery, Electronics, Energy)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Climax Molybdenum (Freeport-McMoRan), Molymet, Rio Tinto Kennecott, Jinduicheng Molybdenum Co. Ltd., China Molybdenum Co. Ltd., Centerra Gold Inc., Sumico Lubricant Co. Ltd., Rose Mill Co., Luoyang Tongrun Nano Technology Co. Ltd., Treibacher Industrie AG, Moly Metal LLP, Tribotecc GmbH, American Elements, 2D Semiconductors Inc., Sinopec

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Molybdenum Disulfide (MoS₂) Market Segmentation

By Product Form

- Powder Grade

- Dispersions

- Granules

- Suspensions & Pastes

- Sputtered Films and Coatings

By Purity Grade

- Technical Grade

- High Purity Grade

- Electronic Grade

By End-User Industry

- Automotive

- Aerospace & Defense

- Industrial Machinery

- Electronics

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Molybdenum Disulfide (MoS₂) Market

- Climax Molybdenum (Freeport-McMoRan)

- Molymet

- Rio Tinto Kennecott

- Jinduicheng Molybdenum Co., Ltd.

- China Molybdenum Co., Ltd.

- Centerra Gold Inc.

- Sumico Lubricant Co., Ltd.

- Rose Mill Co.

- Luoyang Tongrun Nano Technology Co., Ltd.

- Treibacher Industrie AG

- Moly Metal LLP

- Tribotecc GmbH

- American Elements

- 2D Semiconductors Inc.

- Sinopec

*- List not Exhaustive