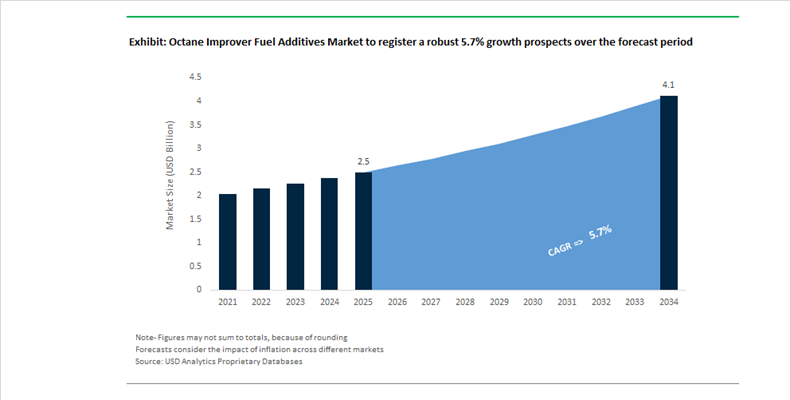

Octane Improver Fuel Additives Market Valued at $2.5 Billion in 2025, Projected to Reach $4.1 Billion by 2034 at 5.7% CAGR Amid GDI Engine Growth and Sustainable Fuel Integration

The Octane Improver Fuel Additives Market is valued at $2.5 billion in 2025 and is forecast to reach $4.1 billion by 2034, expanding at a CAGR of 5.7%. Growth is underpinned by the global shift toward high-compression, turbocharged gasoline direct injection (GDI) engines, stricter deposit control standards, and the integration of bio-based and synthetic fuels into mainstream gasoline pools. Modern engines operating at higher compression ratios require enhanced octane performance, advanced detergency, and oxidative stability to prevent stochastic pre-ignition (SPI), injector fouling, and combustion chamber deposits. Regulatory frameworks such as the revised TOP TIER+™ gasoline standard and evolving EPA additive concentration requirements are raising the performance threshold for gasoline performance additive (GPA) packages across North America, Europe, and Asia-Pacific.

In August 2025, Afton Chemical launched the HiTEC® 65522 series, among the first GPA packages approved under the revised TOP TIER+™ specification. The formulation is engineered to mitigate SPI in high-pressure GDI engines while maintaining injector cleanliness at lower treat rates. In September 2025, BASF introduced the next-generation Keropur® AP 225-20 series, designed to exceed both TOP TIER+™ and EPA Lowest Additive Concentration requirements, with commercial deliveries beginning in the first half of 2026 ahead of 2027 compliance deadlines. In March 2025, BASF also announced expanded aminic antioxidant capacity at its Puebla, Mexico site to enhance gasoline oxidation stability and extend shelf life for high-octane blends.

Sustainability-driven fuel innovation accelerated in 2025. In May 2025, TotalEnergies reported successful offshore trials of Excellium Pro Concentrate in Angola, demonstrating 3% to 5% fuel consumption reductions and measurable injector cleanliness improvements, with compatibility across HVO and bio-based fuels. In June 2025, TotalEnergies powered the 24 Hours of Le Mans using Excellium Racing 100, a mass-balance certified 100% sustainable fuel delivering at least 65% lifecycle greenhouse gas reduction. These initiatives position multifunctional octane boosters and deposit-control additives as enablers of low-carbon fuel pathways without compromising combustion stability.

Regional capacity expansion and supply chain localization remain strategic priorities. In November 2024, Infineum announced a new blending facility in India, commencing trial production in mid-2025 and commercial operations by Q3 2025 to support South Asia’s rapidly expanding automotive market. In January 2026, Infineum entered a framework agreement with Rianlon to strengthen additive supply resilience across Asia-Pacific. In November 2025, BASF and ExxonMobil signed a joint development agreement to advance catalyst and additive technologies targeting lower-carbon high-octane precursors, with industrialization targeted for late 2026.

In April 2025, Chevron Oronite emphasized advanced additive systems for high-compression gasoline engines at the UNITI Congress, aligning formulations with 2030 emission targets. In January 2026, Innospec Inc. reported continued growth in its Fuel Specialties portfolio, focusing on heavy-duty transport and power generation markets in the Middle East and Asia-Pacific. Concurrently, in September 2025, Afton Chemical introduced HiTEC® 12582, the first performance additive for hydrogen internal combustion engines, addressing pre-ignition and lubricant dilution in H2-ICE platforms and signaling a new frontier in combustion-focused additive chemistry.

Octane Improver Fuel Additives Market Trends and Opportunities

Trend: Mandatory Transition to Unleaded Aviation Gasoline Reshapes the High-Octane Additives Landscape

The octane improver fuel additives market is entering a structurally non-discretionary growth phase as the aviation sector moves decisively away from leaded fuels. The Eliminate Aviation Gasoline Lead Emissions initiative has shifted regulatory intent into execution, creating a clear timeline for the phase-out of 100LL avgas and the adoption of high-octane unleaded alternatives by 2030. Unlike prior environmental programs, this transition is backed by fleet-wide certifications, production approvals, and coordinated infrastructure investment, making octane enhancement a mission-critical requirement rather than a performance upgrade. The 100-octane benchmark remains non-negotiable for general aviation piston engines, which operate under extreme detonation sensitivity. As a result, unleaded avgas formulations rely heavily on advanced octane improver chemistries to replicate the anti-knock protection historically delivered by tetraethyl lead.

By early 2025, multiple 100-octane unleaded fuels had moved beyond trial phases into commercial deployment, signaling the start of large-scale displacement of leaded avgas. Refinery-level scaling approvals and ASTM production certifications have removed the primary bottleneck that previously constrained adoption. This has immediate implications for additive suppliers, as unleaded formulations require more sophisticated blending of high-performance octane boosters, metal deactivators, and deposit control agents to ensure valve seat protection, fuel stability, and compatibility across legacy aircraft engines. Parallel to fuel formulation, the aviation ecosystem is investing in logistics modernization, with coordinated rollout strategies across more than 5,000 public-use airports in the United States alone. From a market perspective, this trend locks in long-term, regulation-driven demand for premium octane improvers that can deliver consistent 100-motor-octane performance without environmental or toxicological liabilities.

Trend: High-Compression Small Engines Drive Reformulation of Consumer and Off-Road Fuels

Outside aviation, the octane improver fuel additives market is being reshaped by the rapid evolution of small engine and recreational vehicle design. To meet tightening greenhouse gas and nitrogen oxide emission standards, engine manufacturers are increasingly adopting turbocharging, higher compression ratios, and advanced combustion management systems in motorcycles, marine engines, and outdoor power equipment. These high-efficiency architectures are inherently more prone to pre-ignition and knock, particularly under variable load and temperature conditions. As a result, fuel octane stability has become a critical determinant of engine durability, warranty performance, and emissions compliance.

In 2025, premiumization trends in off-road and specialty fuels accelerated as manufacturers began recommending or requiring higher anti-knock index fuels for optimal performance. This shift is reinforced by broader fuel economy mandates, which indirectly favor downsized, high-stress engines that depend on robust octane improver packages. At the same time, renewable fuel policies are altering the composition of the gasoline pool. Regulatory targets for advanced biofuels are incentivizing the use of ethanol and other oxygenates as primary octane contributors, increasing the need for additive systems that stabilize blends, mitigate phase separation, and protect fuel system components. For additive producers, this trend is expanding the addressable market beyond traditional automotive gasoline into factory-fill fuels, aftermarket boosters, and specialty blends tailored for high-load, high-temperature operating environments.

Opportunity: Bio-Derived High-Octane Additives Accelerate Sustainable Motorsports and Performance Fuels

Motorsports is emerging as a high-margin innovation engine for next-generation octane improvers, particularly bio-derived and carbon-neutral additives. The sector’s move toward fully sustainable fuels by 2026 is creating an urgent demand for octane enhancement solutions that deliver performance parity with fossil-based aromatics while meeting strict carbon neutrality criteria. Racing fuels require octane ratings well above standard consumer gasoline, along with exceptional resistance to knock under extreme compression and thermal stress. Achieving these characteristics without petroleum-derived hydrocarbons has positioned bio-octane chemistry as a strategic growth frontier.

In 2025, significant R&D investment has been directed toward synthesizing high-octane molecules from second-generation biofeedstocks, carbon capture pathways, and green hydrogen. These efforts have demonstrated that bio-derived isooctane and advanced oxygenates can match or exceed the anti-knock performance of traditional toluene and xylene blends. The commercial success of sustainable racing fuels in extreme competitive environments has de-risked these technologies and accelerated their evaluation for broader applications, including premium consumer fuels and sustainable aviation fuel blending. From a market standpoint, motorsports provides both a profitability premium and a technology validation platform, enabling additive suppliers to transfer proven high-octane solutions into regulated aviation and automotive segments.

Opportunity: Multi-Functional Additives for Strategic Reserve and Military Fuels

A distinct opportunity is emerging at the intersection of energy security, defense logistics, and long-term fuel storage. Military and emergency fuel systems increasingly operate under “single-fuel” doctrines, where one fuel must reliably power aircraft, ground vehicles, and generators under extreme conditions. This has elevated the role of octane improver additives that also deliver thermal stability, oxidation resistance, and materials compatibility. Modern military fuel specifications require additive packages capable of increasing thermal stability margins by up to 100 degrees Fahrenheit, preventing deposit formation in high-heat engine zones while preserving anti-knock performance.

Strategic fuel reserves further amplify this requirement. Fuels held for 24 to 60 months must retain octane integrity despite prolonged exposure to trace metals, oxygen, and temperature fluctuations. This creates sustained demand for advanced antioxidant systems, metal deactivators, and stabilizers that protect octane-enhancing components such as olefins and oxygenates during long-term storage. As defense organizations integrate synthetic and bio-based fuels into their supply chains, additive systems must also compensate for reduced aromatic content by restoring lubricity and seal compatibility. Collectively, these requirements position octane improver fuel additives as a core enabler of resilient, multi-use fuel strategies, supporting steady, high-value demand insulated from short-term consumer fuel volatility.

Octane Improver Fuel Additives Market Share and Segmentation Insights

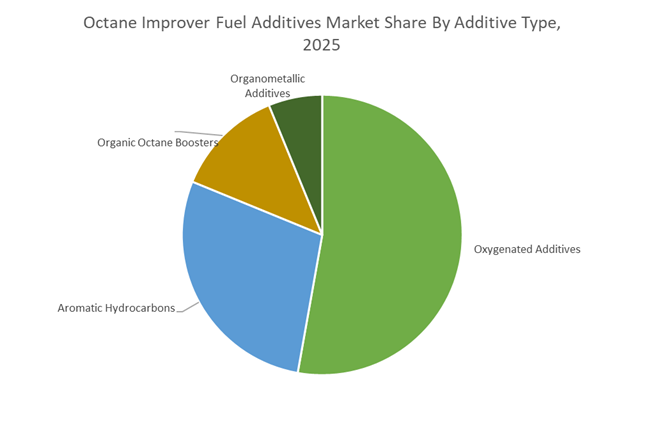

Oxygenated Additives Lead Octane Enhancement Driven by Ethanol Blending Mandates

Oxygenated additives accounted for 52.80% of the Octane Improver Fuel Additives Market by additive type in 2025, supported by the widespread use of ethanol as the primary octane booster in gasoline blending. Ethanol provides high octane value and oxygen content, enabling improved combustion efficiency and compliance with renewable fuel standards. It is widely used in global fuel markets to meet regulatory mandates and performance requirements. Oxygenated additives are critical for achieving higher octane ratings required in modern engines. In 2025, increasing demand for high-octane fuels in GDI engines is strengthening ethanol consumption, supporting efficient combustion and higher compression ratios in advanced gasoline engine technologies.

Refinery Blending Dominates Market with Large-Scale Integration of Octane Enhancers

Refinery blending accounted for 68.40% of the Octane Improver Fuel Additives Market by application in 2025, reflecting the central role of refineries and fuel terminals in integrating octane enhancers into gasoline before distribution. Large scale blending operations ensure fuels meet required octane specifications for different markets and engine types. Ethanol and other additives are incorporated during refining and terminal operations to optimize fuel performance and cost efficiency. This centralized blending approach supports consistent product quality across supply chains. In 2025, real-time ethanol blend optimization is becoming standard practice, enabling refiners to balance octane value, volatility requirements, and cost efficiency in fuel formulation processes.

Octane Improver Fuel Additives Market Competitive Landscape

The octane improver fuel additives market in 2026 is driven by GDI/TGDI engine optimization, SPI mitigation, and injector cleanliness under TOP TIER+™ and Euro 7 standards. Competition centers on multi-functional additives, non-metallic octane boosters, and Asia-Pacific localization to support high-octane gasoline demand and unleaded aviation fuel innovation.

BASF advances multi-functional gasoline additives with Keropur® platform and Asia-Pacific supply expansion

BASF is strengthening its position through the launch of Keropur® AP 225-20, a next-generation gasoline performance additive engineered for TOP TIER+™ compliance and enhanced injector cleanliness in GDI engines. The formulation meets EPA LAC requirements and is progressing toward CARB certification, ensuring regulatory alignment in stringent markets. BASF’s new Asia-based production facility enhances supply security for high-octane additives in India and Southeast Asia. Its integrated Verbund system supports cost efficiency and consistent quality across fuel additive portfolios. A broader 2026 pricing strategy reflects margin protection amid feedstock volatility. BASF’s focus on emissions compliance and engine protection reinforces its leadership in advanced octane chemistry.

Afton Chemical leads GDI optimization and hydrogen combustion additives with HiTEC® innovation platform

Afton Chemical is driving innovation with its HiTEC® 65522 GPA series, specifically designed to prevent stochastic pre-ignition (SPI) and injector fouling in turbocharged GDI engines. The additive meets TOP TIER+™ standards and successfully passes GM LHU Rev G testing protocols, validating performance in modern engines. Afton has also introduced the industry’s first additive for hydrogen internal combustion engines, positioning itself at the forefront of next-generation fuel technologies. Its global technical support network enables refiners to meet localized fuel specifications efficiently. The company’s strategy emphasizes high-performance additives for both conventional and emerging powertrains. This dual focus strengthens Afton’s technological leadership in fuel chemistry.

Innospec delivers cost-effective octane enhancement with organometallic and non-metallic booster flexibility

Innospec is a key player in refinery-level octane improvement, offering Octaburn™ (manganese-based) and PLUTOcen® (ferrocene-based) additives for cost-efficient RON enhancement. These organometallic solutions remain widely used for achieving octane targets with minimal blending cost. For regions with metal restrictions, Innospec’s IOB-3000 and 5000 series provide non-metallic alternatives capable of increasing RON by up to 6 points. The company’s additives enable refiners to utilize lower-quality naphtha streams while maintaining fuel performance standards. Strong growth in its Fuel Specialties segment underscores demand for flexible, high-margin additive solutions. Innospec’s diversified portfolio ensures adaptability across varying regulatory environments.

Lubrizol strengthens regional innovation with hybrid fuel additives and Asia-focused R&D infrastructure

Lubrizol is advancing its “Local-for-Local” strategy through its Shanghai Innovation Center, focusing on fuel additives tailored for Asia-Pacific markets and hybrid vehicle requirements. Its TOP TIER+™ certified additive packages provide robust protection against deposits in GDI engines, which account for a growing share of fuel additive demand. Expansion into Southeast Asia via its Bangkok office enhances regional technical support and market penetration. Lubrizol is also developing additives for alternative fuels such as CNG, LNG, and hydrogen, aligning with evolving energy transition requirements. Its focus on regional customization and hybrid fuel stability strengthens its competitive positioning.

Infineum builds Asia-Pacific supply resilience and low-emission fuel technologies through strategic partnerships

Infineum is enhancing its global footprint through a strategic partnership with Rianlon, integrating manufacturing assets in China and Malaysia to strengthen Asia-Pacific supply chains. The company is focusing on fuel additives that improve combustion efficiency, reduce emissions, and extend engine durability under its Sustainable Transportation strategy. Its research showcased at ISFL highlights advancements in low-emission fuel technologies aligned with energy transition goals. Infineum’s additives support both light-duty and heavy-duty applications, including marine decarbonization. Backed by Shell and ExxonMobil, the company leverages deep integration and R&D strength to maintain leadership in high-performance fuel additives.

United States – Regulatory-Driven Innovation and Premium Fuel Optimization

The United States octane improver fuel additives market is being reshaped by a convergence of tighter regulatory thresholds, premium gasoline demand, and advanced engine protection requirements. In September 2025, BASF introduced the Keropur® AP 225-20 series, engineered to exceed the revised TOP TIER+™ detergent gasoline specification while complying with the U.S. Environmental Protection Agency Lowest Additive Concentration framework. This launch reflects a broader shift toward multifunctional octane improver additives that simultaneously address knock resistance, injector cleanliness, and particulate emissions compliance. Complementing this, Afton Chemical rolled out HiTEC® 65522 in August 2025, targeting stochastic pre-ignition mitigation in modern gasoline direct injection engines. The focus on SPI protection is increasingly critical as OEMs push higher compression ratios to meet fuel economy mandates without sacrificing performance.

From a supply-side perspective, infrastructure investment is reinforcing domestic availability of advanced blending components. Innospec expanded production capacity at its Pleasanton, Texas facility in March 2025, with new proprietary additive lines scheduled to be operational by Q4 2025. Refinery blending strategies continue to favor MTBE and ETBE to optimize 91 and 93 octane grades, while several organometallic octane boosters are progressing through EPA approval pipelines for potential commercialization in early 2026. Parallel R&D momentum is visible in sustainable aviation, where U.S.-based developers are accelerating work on lead-free 100LL replacement additives, positioning octane improver technologies as enablers of the general aviation sector’s planned lead phase-out by 2030.

Brazil – Ethanol-Centric Octane Enhancement and Infrastructure Scaling

Brazil’s octane improver fuel additives landscape is structurally distinct due to its aggressive ethanol integration strategy. In September 2025, the National Agency of Petroleum, Natural Gas and Biofuels approved an amendment increasing the minimum gasoline Research Octane Number to 94, reinforcing the country’s emphasis on higher-octane fuel pools. This regulatory adjustment coincided with the mid-2025 increase in mandatory anhydrous ethanol blending to E30, up from E27, materially elevating baseline octane levels across retail gasoline. To safeguard fuel quality, ANP also revised minimum density standards to 688.9 kg/m³, ensuring that higher ethanol content does not dilute energy performance.

These shifts are generating incremental demand for secondary octane and performance additives that address ethanol’s hygroscopic behavior. Fuel distributors are increasingly deploying stabilizers and phase-separation inhibitors to protect distribution networks, particularly in humid coastal regions. Policy support remains a defining market driver. Under the RenovaBio framework, distributors leveraging advanced additive solutions to reduce lifecycle carbon intensity continue to earn decarbonization credits, reinforcing commercial incentives for high-octane, low-emission fuel formulations. Infrastructure expansion at the Port of Santos, including dedicated ethanol-gasoline blending terminals, is further strengthening Brazil’s position as a large-scale testbed for ethanol-compatible octane improver technologies.

India – Policy-Backed Ethanol Expansion and Premium Fuel Standardization

India’s octane improver fuel additives market is advancing rapidly under the Ethanol Blended Petrol Programme, with the country reaching an average blending rate of 19.93 percent by July 2025, approaching the E20 target for the 2025–26 ethanol supply year. A decisive policy shift in late 2025 removed restrictions on ethanol production from sugarcane juice and molasses, enabling distilleries to operate at full capacity and stabilize the supply of high-octane blending components. Government performance assessments published in August 2025 validated that E20 fuels deliver superior acceleration and ride quality, driven by ethanol’s significantly higher octane number relative to base petrol.

Economic considerations are reinforcing this trajectory. The EBP programme generated foreign exchange savings of approximately ₹1,44,087 crore between 2014 and July 2025, strengthening the macroeconomic case for domestically produced, high-octane fuels. On the technical front, Indian oil marketing companies are increasingly incorporating antiknock index improvers to achieve consistent RON 95 levels for Bharat Stage VI compliant premium fuels. Feedstock security is also being addressed through the allocation of 5.2 million metric tonnes of surplus rice for ethanol production in the 2025–26 cycle, underlining how agricultural integration is indirectly shaping demand for octane improver additives in India.

China – Emissions Compliance and Catalysis-Led Additive Development

China represents one of the most strategically important markets for octane improver fuel additives due to its scale, regulatory rigor, and technological depth. Enforcement of China VI-b emission standards is accelerating the adoption of high-performance deposit control additives that preserve octane quality while minimizing injector fouling. With the world’s largest gasoline direct injection vehicle fleet, the country serves as a critical proving ground for detergency-driven octane improvers designed to sustain combustion efficiency under high thermal stress.

At the innovation layer, catalytic science is playing an increasingly central role. In December 2025, Clariant recognized Prof. Zhang Tao for advances in single-atom catalysis, now being piloted for converting cellulose into intermediates suitable for sustainable fuel additives. Capacity expansion at the BASF-SINOPEC joint venture in Nanjing in July 2025 further enhanced domestic availability of chemical building blocks for performance additives. Export controls on antimony and related materials have prompted additive formulators to accelerate the transition toward titanium-based and organic catalyst systems. Supporting this shift, Clariant’s Shanghai R&D center is intensifying development of low-carbon catalytic solutions tailored to China’s petrochemical and fuels ecosystem.

Germany – Decarbonization, E-Fuels, and High-Performance Collaboration

Germany’s octane improver fuel additives market is closely aligned with broader European decarbonization and fuel efficiency objectives. BASF SE is upgrading manufacturing infrastructure across Europe to support the 2026 rollout of next-generation performance packages designed to enhance fuel economy and reduce lifecycle CO2e emissions. Beyond road transport, maritime integration is emerging as a notable demand vector. Innospec reported that its marine fuel additive solutions enabled the avoidance of more than 20 million metric tonnes of CO2e emissions in 2024, underscoring the role of advanced additives in emissions management for shipping.

Germany is also at the forefront of renewable fuel experimentation. Pilot deployments of power-to-liquid e-fuels are creating niche demand for specialized octane-adjusting additives capable of matching the combustion characteristics of conventional internal combustion engines. Concurrently, ongoing evaluation of REACH compliance for legacy organometallic additives is accelerating the transition toward organic, environmentally compatible octane boosters. Collaboration between German automotive OEMs and chemical suppliers is further reinforcing this trend, particularly in the development of drop-in, high-octane fuels tailored for high-performance and sports vehicle applications.

Comparative Snapshot – Country-Level Strategic Themes

Octane Improver Fuel Additives Market County Level Snapshot

|

Country

|

Regulatory Catalyst

|

Core Octane Strategy

|

Infrastructure and R&D Focus

|

|

United States

|

TOP TIER+ and EPA LAC tightening

|

Premium gasoline and GDI protection

|

Domestic additive capacity expansion and aviation fuel R&D

|

|

Brazil

|

RON 94 mandate and E30 rollout

|

Ethanol-driven octane elevation

|

Blending terminals and ethanol-compatible additives

|

|

India

|

E20 policy acceleration

|

Ethanol and AKI improvers for RON 95

|

Distillery expansion and agricultural feedstock integration

|

|

China

|

China VI-b enforcement

|

Detergency-led octane stability

|

Catalysis innovation and refinery capacity growth

|

|

Germany

|

REACH and decarbonization targets

|

Organic boosters and e-fuel compatibility

|

OEM-chemical collaboration and low-carbon additives

|

Octane Improver Fuel Additives Market Report Scope

Octane Improver Fuel Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.5 Billion

|

|

Market Size (2034)

|

$4.1 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Additive Type (Oxygenated Additives, Organometallic Additives, Aromatic Hydrocarbons, Organic Octane Boosters), By Application (Refinery Blending, Aftermarket Fuel Additives, Specialty Fuels), By Engine Type (Gasoline Direct Injection Engines, Port Fuel Injection Engines, Hybrid Engines), By Functionality (Antiknock Additives, Deposit Control Additives, Fuel Stabilizers)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Afton Chemical, Innospec, BASF, Chevron Oronite, Lubrizol, Clariant, Evonik Industries, LANXESS, Dorf Ketal, Sinopec, TotalEnergies, Eni, Huntsman, Shell, Gulbrandsen

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Octane Improver Fuel Additives Market Segmentation

By Additive Type

- Oxygenated Additives

- Organometallic Additives

- Aromatic Hydrocarbons

- Organic Octane Boosters

By Application

- Refinery Blending

- Aftermarket Fuel Additives

- Specialty Fuels

By Engine Type

- Gasoline Direct Injection Engines

- Port Fuel Injection Engines

- Hybrid Engines

By Functionality

- Antiknock Additives

- Deposit Control Additives

- Fuel Stabilizers

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Octane Improver Fuel Additives Industry

- Afton Chemical

- Innospec

- BASF

- Chevron Oronite

- Lubrizol

- Clariant

- Evonik Industries

- LANXESS

- Dorf Ketal

- Sinopec

- TotalEnergies

- Eni

- Huntsman

- Shell

- Gulbrandsen

*- List not Exhaustive