Ozone Water Treatment Systems Market Overview – Growth Outlook and Strategic Imperatives for 2025–2034

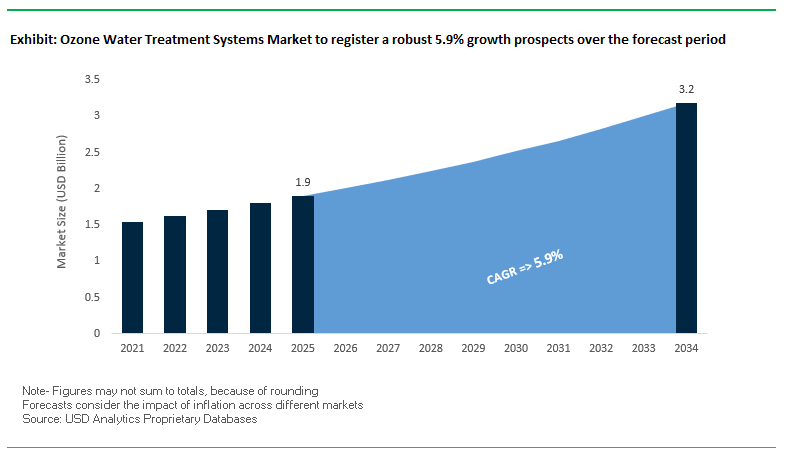

The global ozone water treatment systems market is projected to reach USD 1.9 billion in 2025 and expand to USD 3.2 billion by 2034, reflecting a CAGR of 5.9%. The robust growth trajectory is underpinned by increasing regulatory pressure for chemical-free disinfection, growing public awareness about the risks of disinfection byproducts (DBPs), and the rising prevalence of chlorine-resistant microorganisms such as Cryptosporidium. Ozone, a powerful oxidant, has emerged as a leading solution due to its ability to inactivate a wide range of pathogens without generating harmful residuals associated with traditional chlorine-based treatments.

Technological advancements are accelerating adoption, especially in Advanced Oxidation Processes (AOPs), where ozone is combined with UV or hydrogen peroxide to generate hydroxyl radicals capable of breaking down pharmaceuticals, pesticides, and PFAS (“forever chemicals”). The market is also witnessing a surge in compact, modular, and containerized ozone systems for decentralized municipal facilities, industrial operations, and remote water treatment sites. Meanwhile, the push for enhanced water reuse is making ozonation indispensable in advanced recycling schemes, where it not only disinfects but also improves biodegradability for downstream processes.

Strategic Imperatives for Shareholders:

- Prioritize investments in PFAS-targeted AOP solutions to meet tightening environmental regulations.

- Expand into decentralized and modular system markets, which are growing faster than large-scale municipal segments.

- Partner with utilities and industrial players to integrate ozone in water reuse and recycling infrastructure.

- Leverage digital monitoring platforms to enhance operational efficiency and compliance reporting.

Market Analysis – Key Developments Shaping the Competitive Landscape

The ozone water treatment systems market is evolving rapidly with strategic moves from industry leaders and groundbreaking technological launches. In May 2025, De Nora Water Technologies reported a 17% increase in its water business backlog compared to the end of 2024, signaling robust demand for its Capital Controls® ozone generators. The growth underscores the strengthening global appetite for sustainable disinfection technologies that minimize chemical footprints.

Innovations targeting micropollutants are also setting new performance benchmarks. In October 2024, a SUEZ-led project in Denmark demonstrated an advanced approach by splitting the ozone dosage across biological and tertiary stages, achieving significant micropollutant reduction and enhanced sludge settling. Similarly, Veolia has intensified its R&D push, unveiling its Drop® patented PFAS destruction technology in June 2025, capable of achieving 99.9999% elimination of targeted compounds.

Beyond large-scale plants, the demand for turnkey, containerized ozone systems continues to rise. Veolia’s Ozonia brand has developed fully assembled, plug-and-play units, reducing construction timelines and costs for both municipal and industrial projects. Xylem’s long-standing presence in the sector, marked by its 2016 Werdhölzli plant in Zurich continues to influence market design standards. Additionally, Xylem’s Wedeco GSO series offers high-efficiency, compact solutions for small-to-medium operations, catering to the growing decentralized treatment segment.

Mergers and acquisitions are also shaping competitive synergies. In April 2025, Kurita America merged with Avista Technologies to strengthen its integrated water treatment offerings, incorporating ozone as a vital pre-treatment and disinfection component, thus expanding its competitive reach across industrial and municipal markets.

Trends and Opportunities in Ozone Water Treatment Systems Market

Trend 1: Ozone Gains Popularity in Food & Beverage Industries for Chemical-Free Sanitation

The ozone water treatment systems market is witnessing substantial adoption in the food and beverage sector due to increasing demand for chemical-free sanitation solutions. Ozone serves as a powerful sanitizer that decomposes into oxygen, leaving no harmful residues, making it an ideal alternative to chlorine and other chemical disinfectants. Its broad-spectrum efficacy enables effective inactivation of bacteria, viruses, and molds at low concentrations, ensuring high food safety standards. Beyond disinfection, ozone enhances product quality and extends shelf life, improving sensory and nutritional characteristics while reducing microbial contamination. Applications range from raw water treatment to sanitization of process equipment through Clean-in-Place (CIP) systems, washing of produce, and even air disinfection in cold storage, making it a versatile, residue-free solution that aligns with clean-label initiatives and regulatory compliance.

Trend 2: On-Site Ozone Generation Systems Reduce Reliance on Bottled Gas Supply

Industrial and municipal facilities are increasingly transitioning to on-site ozone generation systems, driven by safety, cost, and operational advantages. Producing ozone from an oxygen feed gas eliminates the need to store hazardous chemicals like chlorine, reducing liability and safety risks. On-site generation also offers cost savings by minimizing chemical purchases and disposal concerns while providing a sustainable and environmentally friendly alternative. Ozone’s high disinfection efficiency approximately 3,000 times greater than chlorine combined with short contact times ensures rapid pathogen inactivation. The on-demand generation model allows for precise, safe, and eco-friendly water treatment in facilities ranging from wastewater plants to food processing units, enhancing both operational control and regulatory compliance.

Opportunity 1: Ozone-Biofiltration Hybrid Systems for Enhanced Organic Contaminant Removal

Hybrid systems combining ozonation with biologically active filtration (BAF) present a high-potential opportunity for removing micropollutants such as pharmaceuticals and pesticides. Ozonation breaks down complex, non-biodegradable molecules into simpler, biodegradable compounds, which are then efficiently degraded by the microbial communities in biofilters. The multi-barrier approach achieves high removal rates (pilot studies report up to 90% elimination of endocrine disruptors and pharmaceuticals in municipal wastewater). The ozone-BAF process also reduces disinfection byproducts (DBPs), improves effluent quality, and offers a cost-effective alternative to reverse osmosis for water reuse where salinity reduction is not critical, supporting sustainable and high-quality water management practices.

Opportunity 2: Ozone Nanobubble Technology for Aquaculture & Hydroponics Water Treatment

Ozone nanobubble technology represents a transformative opportunity in water treatment for aquaculture and hydroponics. These microscopic bubbles increase dissolved oxygen levels and improve ozone transfer efficiency, resulting in healthier aquatic ecosystems and enhanced plant growth. Nanobubbles maintain prolonged presence in the water column, enhancing oxygen utilization by up to 60% in recirculating aquaculture systems. Their strong oxidative and pathogen-killing capabilities ensure effective disinfection while remaining chemical-free. Additionally, nanobubble treatment improves water clarity by promoting flocculation and settling of suspended particles, maintaining high water quality over extended periods. The innovative approach aligns with sustainable aquaculture practices and supports high-value water treatment applications where water quality is critical.

Ozone Water Treatment Systems Market Share Insights

Industrial and Municipal Systems Dominate Market Adoption

Industrial-scale ozone water treatment systems account for 40.4% of the market in 2025, representing the largest segment by value due to high-capacity, custom-engineered solutions for food & beverage, pharmaceuticals, and high-purity industrial water. Municipal systems (30.6%) follow closely, driven by primary disinfection needs, advanced oxidation for micropollutants, and taste/odor control in public water supply. These systems are essential for Cryptosporidium inactivation, emerging contaminant removal, and regulatory compliance, establishing ozone as a core technology for municipal water and wastewater treatment. Commercial and residential systems represent niche but growing segments, focusing on Legionella control in hotels, restaurants, and luxury homes as well as whole-home oxidation solutions for taste and odor remediation.

Corona Discharge Technology Leads, While UV and Electrolytic Solutions Expand

Corona Discharge (CD) ozone generators dominate with 80.4% market share, reflecting their status as the industrial and municipal standard. CD systems efficiently produce high ozone concentrations, making them cost-effective for medium to large-scale water treatment projects. Ultraviolet (UV) ozone generators serve small-scale residential and aquarium applications, providing simplicity and low operational cost but lower output. Emerging technologies such as electrolytic and cold plasma ozone generation offer direct-in-water production and energy efficiency improvements, gaining attention for specialized industrial applications, though adoption remains limited compared to the established CD technology.

.png)

Disinfection and Organic Contaminant Oxidation Drive Core Applications

Disinfection & pathogen control (30.7%) remains a primary strength, with ozone providing superior efficacy against bacteria, viruses, and protozoa without producing harmful disinfection byproducts (DBPs). Organic contaminant oxidation (25.4%) is a key driver in advanced water treatment, targeting micropollutants such as pesticides, pharmaceuticals, and endocrine disruptors. Taste and odor removal remains a classic application, particularly in municipal systems challenged with geosmin and MIB compounds, while color removal serves industrial and aesthetic purposes, especially in pulp & paper operations and high-clarity water production. Cooling tower treatment provides biofilm and Legionella control, replacing traditional biocides to improve operational efficiency and reduce chemical usage.

Ozone Generators and Contact Chambers Constitute Core System Components

Ozone generators (35.6%) are the technological heart of the system, producing high-concentration ozone with advanced dielectric and electrode design. Contact chambers (24.3%) are where the oxidation and disinfection processes occur, requiring optimal mass transfer and sufficient contact time to achieve target water quality. Control panels and monitoring systems act as the system brain, enabling real-time performance tracking, ozone level monitoring, and operational safety compliance. Destruct units ensure safe decomposition of excess ozone to protect operators, while other components such as air dryers and venturi injectors support reliable system operation.

Hybrid Integration Becomes the Preferred Treatment Approach

Hybrid ozone systems (60.7%) dominate due to enhanced efficiency and versatility, combining ozone with biological filtration, UV, or hydrogen peroxide for advanced oxidation processes (AOP). Standalone ozone systems (39.5%) remain relevant for specific oxidation-only tasks, including certain cooling water, wastewater disinfection, and industrial applications. Hybrid solutions provide higher overall treatment efficacy, improved byproduct management, and optimized operational performance, which are increasingly demanded by municipalities and industrial facilities seeking regulatory compliance and high water quality standards.

Water & Wastewater, Food & Beverage, and Pharmaceuticals Drive End-Use Demand

Water and wastewater treatment (34.9%) remain foundational markets, as municipalities implement ozone for drinking water disinfection, taste/odor control, and effluent polishing. Food & beverage (25.8%) represents a high-value industrial adoption, using ozone for process water sanitation, produce washing, and shelf-life extension without chemical residues. Pharmaceuticals rely on ozone to produce highly purified water (HPW) and sanitize systems, with the benefit of leaving no residual chemicals that could compromise product integrity. Other sectors, including aquaculture and pulp & paper, leverage ozone for recirculating system disinfection and effluent treatment, highlighting its versatility across industrial and environmental applications.

Country Analysis of the Ozone Water Treatment Systems Market

United States: Modernizing Water Infrastructure with Advanced Ozone Systems

The United States market for ozone water treatment systems is being propelled by the Bipartisan Infrastructure Law, which allocates over $50 billion for essential water and wastewater upgrades, driving the modernization of municipal disinfection processes. The EPA’s tightening of PFAS regulations is fostering innovations in advanced oxidation processes (AOPs), integrating ozone with technologies like UV to break down persistent contaminants. Technological advancements in high-efficiency ozone generation, such as corona discharge systems, are enhancing scalability for large municipal and industrial applications. The market is also witnessing a surge in hybrid systems combining ozone with UV disinfection or membrane filtration for comprehensive water treatment. Increasing demand for decentralized and on-site water treatment solutions, especially in rural and small communities, along with the bottled water industry’s use of ozone for enhanced purification and extended shelf life, is further boosting market growth in niche segments.

China: Scaling Ozone Disinfection Through National Water Safety Initiatives

China’s Water Ten Plan and Beautiful China initiative are driving massive government investments in water infrastructure, creating a robust environment for ozone water treatment systems. With a target of 95% wastewater treatment in county-level cities, there is strong demand for ozone-based municipal and industrial water disinfection technologies. Companies like Qingdao Guolin Technology Group have advanced manufacturing for ozone generators ranging from 1 kgO₃/h to 500 kgO₃/h, supporting both municipal and industrial applications. Ozone is widely preferred for its ability to degrade macromolecular organic matter and reduce wastewater toxicity, benefiting industries such as printing, dyeing, pharmaceuticals, and chemicals. Chinese officials are also promoting containerized treatment plants for on-site water reuse, addressing both pollution and scarcity with compact, high-efficiency ozone solutions.

India: Driving Rural and Decentralized Water Safety Through Ozone Technology

India’s Jal Jeevan Mission is expanding the use of ozone water treatment systems by providing safe tap water to rural households, creating demand for on-site and decentralized disinfection technologies. The CPCB’s stringent discharge standards for Sewage Treatment Plants are pushing adoption of advanced ozone systems capable of regulatory compliance. Programs like the Namami Gange Mission are promoting decentralized wastewater treatment in smaller cities and rural areas, where ozone serves as a reliable final-stage disinfection solution. Companies such as Otsil have demonstrated the effectiveness of ozone in large-scale projects, including converting tertiary-treated STP water for potable reuse and treating over 200 swimming pools in a single gated community, highlighting ozone’s role in advanced water reuse applications.

Japan: Pioneering Hybrid Ozone Systems and Microbial Control in Advanced Water Treatment

Japan is at the forefront of ozone water treatment technology, with companies like Toshiba developing highly efficient and durable ozone generators (TGOGS™ series) for disinfection, odor control, and THM reduction. Hospital studies demonstrate ozone-based continuous flow systems effectively inactivate antimicrobial-resistant bacteria, supporting the One Health approach. Ozone is also extensively used in municipal sewage treatment for water reclamation and advanced disinfection, with research on hybrid systems combining ozone with UV-LED technology to combat pathogenic microorganisms like SARS-CoV-2. Japan’s strict emissions control policies and incentives for ecological technologies continue to drive market adoption and innovation.

Germany (Europe): Integrating Ozone with Advanced Tertiary Treatment and Smart Systems

Germany’s adoption of ozone water treatment systems is influenced by the EU Urban Wastewater Treatment Directive, which expands treatment requirements to communities above 1,000 population-equivalents. Extended Producer Responsibility mandates pharmaceutical and cosmetics companies to finance advanced micropollutant removal, promoting AOP-based tertiary treatment solutions incorporating ozone. Collaborations such as Fraunhofer ISIT with CONDIAS GmbH have led to miniaturized ozone generators with integrated sensor technology for domestic and industrial applications. Germany’s regulatory framework, including state-specific self-monitoring ordinances, ensures operational safety and long-term compliance, fostering adoption of advanced ozone disinfection technologies in municipal and industrial water systems.

Saudi Arabia: Accelerating Sustainable Water Reuse Through Ozone Disinfection

Saudi Arabia’s Vision 2030 and $80 billion investment in water projects prioritize sustainable water management, driving adoption of ozone water treatment systems for municipal and industrial wastewater treatment. The country aims for 100% reuse of treated urban wastewater by 2025, requiring ozone-based disinfection to meet stringent quality standards. Public-private partnerships for wastewater treatment plants are underway, with eight new projects valued at $8 billion. The National Water Company (NWC) is upgrading water supply networks, reservoirs, and pipelines with advanced treatment stages incorporating ozone. The ongoing capital projects portfolio, including $3.29 billion for 86 wastewater treatment plant initiatives, underscores the critical role of ozone systems in sustainable and reliable water infrastructure.

Competitive Landscape – Strategic Moves of Key Industry Leaders

The ozone water treatment systems sector is characterized by a mix of global conglomerates and specialized solution providers, each leveraging unique technological strengths and geographic footprints to gain market share.

Xylem Inc. – Driving Energy-Efficient Ozone Innovation

Xylem’s ozone business, anchored by its Wedeco brand, focuses on delivering smart, energy-optimized oxidation and AOP systems to both municipal and industrial clients. Its product range spans compact pilot units to custom-engineered large-scale plants, with landmark projects like the Zurich Werdhölzli facility underscoring its leadership in micropollutant removal. The company’s integration of digital platforms, such as Rivo™ I, enables real-time monitoring and optimization of ozone systems, ensuring high performance and compliance.

De Nora – Expanding Electrochemical Expertise into Ozone Disinfection

With a core competency in electrochemical solutions, De Nora offers a comprehensive water disinfection portfolio, including its Capital Controls® ozone generators and AOP configurations. The company’s Q1 2025 growth reflects market confidence in its reliable, on-site generation technologies, which are especially relevant for utilities seeking chemical-free alternatives. De Nora’s commitment to emerging contaminant treatment is evident in its complementary PFAS removal technologies, positioning it as a holistic provider of water purification solutions.

Veolia Environnement S.A. – Integrating Ozone into Ecological Transformation

Veolia, through its Ozonia brand, delivers a full spectrum of ozone solutions from large municipal plants to modular containerized systems. Its Drop® PFAS destruction technology, launched in June 2025, represents a milestone in addressing “forever chemicals” via AOP integration. Leveraging its Hubgrade digital platform, Veolia offers AI-powered performance optimization across water infrastructure, reinforcing its position as a sustainability-focused leader in ozone treatment.

SUEZ (Part of Veolia) – Advancing Multi-Barrier Ozone Applications

Prior to its integration into Veolia, SUEZ was known for resilient, regulation-driven water solutions, particularly in ozonation. Its Denmark micropollutant project (October 2024) exemplified a multi-barrier approach by strategically splitting ozone dosage for optimal results. While now under Veolia’s umbrella, SUEZ’s technical expertise and proven projects remain central to the group’s competitive edge in advanced disinfection.

Ozone Water Treatment Systems Market Report Scope

Ozone Water Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2034)

|

$3.2 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By System Type (Industrial-Scale Systems, Municipal Systems, Commercial Systems, Residential Systems), By Ozone Generation Technology (Corona Discharge (CD) Systems, Ultraviolet (UV) Ozone Generators, Electrolytic Ozone Generators, Cold Plasma Generators), By Application (Disinfection & Pathogen Control, Taste & Odor Removal, Color Removal, Organic Contaminant Oxidation, Cooling Tower Treatment), By Component Type (Ozone Generators, Contact Chambers, Destruct Units, Control Panels, Monitoring Systems), By Integration Type (Standalone Ozone Systems, Hybrid Systems), By End-Use Industry (Water & Wastewater Treatment, Food & Beverage, Pharmaceuticals, Aquaculture, Pulp & Paper)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., SUEZ, Mitsubishi Electric Corporation, Toshiba Corporation, Primozone Production AB, Ozonia (a Veolia brand), De Nora S.p.A., Metawater Co., Ltd., ESCO International, Ozonetech Systems OTS AB, Industrie De Nora S.p.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ozone Water Treatment Systems Market Segmentation

By System Type

- Industrial-Scale Systems

- Municipal Systems

- Commercial Systems

- Residential Systems

By Ozone Generation Technology

- Corona Discharge (CD) Systems

- Ultraviolet (UV) Ozone Generators

- Electrolytic Ozone Generators

- Cold Plasma Generators

By Application

- Disinfection & Pathogen Control

- Taste & Odor Removal

- Color Removal

- Organic Contaminant Oxidation

- Cooling Tower Treatment

By Component Type

- Ozone Generators

- Contact Chambers

- Destruct Units

- Control Panels

- Monitoring Systems

By Integration Type

- Standalone Ozone Systems

- Hybrid Systems

- Ozone + UV

- Ozone + Activated Carbon

- Ozone + Membrane Filtration

By End-Use Industry

- Water & Wastewater Treatment

- Food & Beverage

- Pharmaceuticals

- Aquaculture

- Pulp & Paper

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Ozone Water Treatment Systems Market

- Veolia

- Xylem Inc.

- SUEZ

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Primozone Production AB

- Ozonia (a Veolia brand)

- De Nora S.p.A.

- Metawater Co., Ltd.

- ESCO International

- Ozonetech Systems OTS AB

- Industrie De Nora S.p.A.

* List Not Exhaustive

Research Coverage

This report investigates the Global Ozone Water Treatment Systems Market, presenting detailed analysis reviews of regulatory drivers, technological breakthroughs, and strategic imperatives shaping the industry from 2025 to 2034. Published by USDAnalytics, the study highlights how ozone has become a frontline solution for municipalities and industries facing rising concerns over chlorine-resistant pathogens, PFAS, and disinfection byproducts (DBPs). The report also reviews key developments such as the adoption of hybrid AOP configurations, on-site ozone generation systems, and containerized modular solutions that are redefining water treatment efficiency and sustainability. With coverage of mergers, acquisitions, digital integration, and innovations in nanobubble and biofiltration hybrids, this report is an essential resource for utilities, industrial operators, regulators, and investors seeking to align with the rapid evolution of ozone water treatment technologies.

Scope Includes:

- Segmentation: By Technology (Corona Discharge, UV Ozone, Electrolytic & Emerging), By System Type (Hybrid & Standalone), By Application (Disinfection, Organic Oxidation, Taste & Odor, Color Removal, Cooling Towers), By End-Use (Municipal, Industrial, Food & Beverage, Pharmaceuticals, Commercial, Residential).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic Data: 2021 to 2024, and Forecast Data: 2025 to 2034.

- Companies: Profiles and competitive analysis of 15+ leading players including Xylem, De Nora, Veolia, SUEZ, Kurita, and Qingdao Guolin Technology.

Methodology

The methodology adopted by USDAnalytics integrates primary and secondary research to deliver a comprehensive outlook on the ozone water treatment systems market. Primary data was gathered through interviews with water utilities, regulators, technology developers, and industrial operators to validate technology adoption trends, regulatory impacts, and end-user preferences. Secondary inputs included analysis of scientific publications, government regulations, company filings, and international project databases. Market sizing was determined using top-down and bottom-up modeling, cross-verifying contract values, installation data, and technology penetration rates. Forecasts were stress-tested under scenarios such as accelerated PFAS regulations, rapid uptake of hybrid AOP systems, and expansion of decentralized modular plants, ensuring robust and reliable projections for stakeholders across the value chain.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Ozone Water Treatment Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Shareholders

1.3. Global Market Snapshot

2. Ozone Water Treatment Systems Market Outlook (2025–2034)

2.1. Market Valuation and Growth Projections

2.1.1. Current Market Size (2025): $1.9 Billion

2.1.2. Forecasted Market Size (2034): $3.2 Billion at 5.9% CAGR

2.2. Key Drivers and Market Dynamics

2.2.1. Regulatory Pressure for Chemical-Free Disinfection

2.2.2. Rising Awareness of Disinfection Byproducts (DBPs)

2.2.3. Prevalence of Chlorine-Resistant Microorganisms

2.2.4. Technological Advancements in Advanced Oxidation Processes (AOPs)

3. Market Analysis: Key Developments Shaping the Competitive Landscape

3.1. Overview of Strategic Moves and Technological Launches

3.2. Recent Developments of Key Players

3.2.1. De Nora Water Technologies' Growth in Backlog (May 2025)

3.2.2. SUEZ's Advanced Micropollutant Removal Project in Denmark (October 2024)

3.2.3. Veolia's Drop® PFAS Destruction Technology (June 2025)

3.3. Trends in Decentralized and Modular Systems

3.4. Mergers and Acquisitions: Kurita America and Avista Technologies (April 2025)

4. Trends and Opportunities in the Ozone Water Treatment Systems Market

4.1. Trend 1: Ozone Gains Popularity in Food & Beverage Industries

4.1.1. Chemical-Free Sanitation and No Harmful Residues

4.1.2. Enhanced Product Quality and Shelf Life

4.2. Trend 2: On-Site Ozone Generation Systems

4.2.1. Reducing Reliance on Bottled Gas Supply

4.2.2. Cost Savings and Enhanced Safety

4.3. Opportunity 1: Ozone-Biofiltration Hybrid Systems

4.3.1. Enhanced Organic Contaminant Removal

4.3.2. High Removal Rates for Micropollutants

4.4. Opportunity 2: Ozone Nanobubble Technology

4.4.1. Improving Dissolved Oxygen and Disinfection in Aquaculture

4.4.2. Promoting Water Clarity and Healthier Ecosystems

5. Ozone Water Treatment Systems Market Share Insights

5.1. By System Type

5.1.1. Industrial and Municipal Systems Dominate Market Adoption

5.1.2. Commercial and Residential Systems

5.2. By Ozone Generation Technology

5.2.1. Corona Discharge (CD) Technology Leads

5.2.2. UV and Electrolytic Solutions Expand

5.3. By Application

5.3.1. Disinfection and Organic Contaminant Oxidation Drive Core Applications

5.3.2. Taste & Odor, Color Removal, and Cooling Tower Treatment

5.4. By Integration Type and End-Use

5.4.1. Hybrid Integration Becomes Preferred Approach

5.4.2. Water & Wastewater, Food & Beverage, and Pharmaceuticals Drive Demand

6. Country Analysis of the Ozone Water Treatment Systems Market

6.1. United States: Modernizing Infrastructure with Advanced Ozone Systems

6.2. China: Scaling Disinfection Through National Water Safety Initiatives

6.3. India: Driving Rural and Decentralized Water Safety

6.4. Japan: Pioneering Hybrid Ozone Systems and Microbial Control

6.5. Germany (Europe): Integrating Ozone with Advanced Tertiary Treatment

6.6. Saudi Arabia: Accelerating Sustainable Water Reuse

7. Competitive Landscape: Strategic Moves of Key Industry Leaders

7.1. Xylem Inc.: Driving Energy-Efficient Ozone Innovation

7.2. De Nora: Expanding Electrochemical Expertise into Ozone Disinfection

7.3. Veolia Environnement S.A.: Integrating Ozone into Ecological Transformation

7.4. SUEZ (Part of Veolia): Advancing Multi-Barrier Ozone Applications

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. By System Type

8.1.2. By End-Use Industry

8.2. Europe Market Size Outlook to 2034

8.2.1. By System Type

8.2.2. By End-Use Industry

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. By System Type

8.3.2. By End-Use Industry

8.4. South America Market Size Outlook to 2034

8.4.1. By System Type

8.4.2. By End-Use Industry

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. By System Type

8.5.2. By End-Use Industry

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations