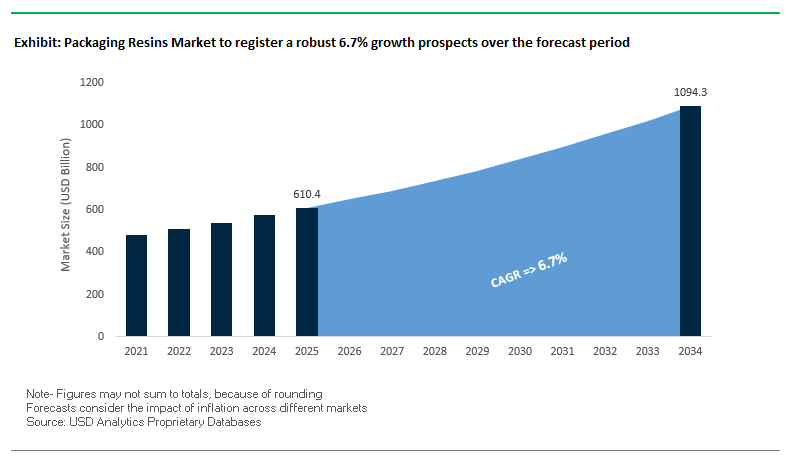

Packaging Resins Market to Expand from $610.4 Billion in 2025 to $1,094.2 Billion by 2034 Driven by Sustainability and Circular Economy Initiatives

The Global Packaging Resins Market is projected to grow from $610.4 billion in 2025 to $1,094.2 billion by 2034, reflecting a CAGR of 6.7%. The industry underpins modern packaging by supplying polyethylene terephthalate (PET), high-density polyethylene (HDPE), polypropylene (PP), and other polymer resins, which provide durability, lightweight design, and versatility for food, beverage, medical, and consumer products. As a backbone of circular and sustainable packaging, the sector addresses both regulatory compliance and consumer expectations for eco-friendly solutions.

Key Insights for Industry Professionals:

- Post-Consumer Recycled (PCR) and Bio-Based Polymers Are Rising: Companies increasingly adopt recycled and bio-based resins to meet sustainability mandates and Extended Producer Responsibility (EPR) laws.

- Lightweighting Trends Reduce Material Use and Carbon Footprint: Advanced resin grades allow thinner yet stronger packaging, optimizing transportation efficiency and material consumption.

- Barrier Performance is Critical for Food and Beverage Packaging: Resins engineered for oxygen, moisture, and light protection extend shelf life and reduce food waste.

- Digital Traceability is Transforming the Resin Value Chain: Innovations such as QR-coded batch tracking and digital watermarking enhance recycling efficiency and compliance.

- Sustainability Drives Innovation Across the Industry: Leading players are developing advanced recycling, chemical recycling, and circular economy solutions to reduce environmental impact.

Recent Strategic Developments in Global Packaging Resins Highlighting Sustainability and Circular Innovations

The Packaging Resins Industry is witnessing a series of technological innovations, strategic acquisitions, and regulatory milestones that are reshaping global production and product offerings. In August 2025, LyondellBasell's GXLYB joint venture received FDA clearance for recycled PP and HDPE resins, enabling food-contact applications and reinforcing the demand for circular polymers. In the same month, SABIC launched its LNP™ THERMOCOMP™ platform, supporting large thermoplastic part manufacturing across multiple industries. Also in August, U.S. lawmakers introduced a bill directing the FDA to study microplastics, signaling potential future regulatory requirements for plastic packaging.

July 2025 marked several milestones: Dow Inc. launched its INNATE TF 220 resin designed for high-performance, recyclable flexible packaging. The Amcor-Berry Global all-stock merger closed, creating a dominant consumer packaging entity and influencing resin demand for rigid and flexible packaging. Additionally, Braskem completed its first sale of circular polyethylene (PE) in South America, reinforcing its leadership in chemical recycling initiatives.

Earlier developments include May 2025, when the State of Maryland passed an Extended Producer Responsibility (EPR) law, reflecting the growing regulatory landscape for sustainable packaging.

Trends and Opportunities Reshaping the Packaging Resins Market

Legislative Mandates Driving Unprecedented Demand for Post-Consumer Recycled (PCR) Resins

The most influential force reshaping the packaging resins market is the global wave of recycled content legislation. The European Union’s Single-Use Plastics Directive requires PET beverage bottles to contain at least 25% rPET by 2025 and 30% by 2030, creating a binding demand signal for recycled resins. This legislative mandate is being amplified by corporate commitments—Coca-Cola, for instance, aims for 50% recycled content in all bottles and cans by 2030, while Unilever has set a 25% target by 2025.

These goals are already materializing into capital investments across the recycling value chain. In 2025, Coca-Cola HBC inaugurated its first company-owned packaging collection hub in Nigeria, designed to process 13,000 tonnes of PET bottles annually. Simultaneously, Unilever is investing in digital R&D tools at its Global Packaging Centre to improve PCR color and performance prediction, accelerating adoption.

The result is an unprecedented surge in demand for high-quality PCR resins, particularly rPET, creating both opportunities and supply-chain bottlenecks. As PCR adoption becomes non-negotiable for compliance and brand image, resin suppliers and recyclers capable of guaranteeing food-grade quality and scale will command premium value in the global market.

Strategic Shift to Monomaterial Polyolefin Resin Formulations for Recyclability

Another major trend is the accelerated transition toward monomaterial polyolefin structures, which simplify recycling compared to multi-material laminates. In 2024, Mars China launched a Snickers bar packaged in mono-material PP, demonstrating a large-scale commercial redesign aligned with “Designed for Recycling” principles.

This shift is underpinned by resin innovation. ExxonMobil’s Exceed S PE resins combine stiffness and toughness, enabling durable monomaterial solutions that previously required multi-resin blends. Likewise, SABIC’s TRUCIRCLE portfolio, derived from chemically recycled plastics, is being deployed in partnerships with Nestlé and Unilever to achieve circular packaging solutions.

The strategic importance lies in reducing contamination in recycling streams. Unlike PET-PE laminates, mono-PE or mono-PP packaging can be efficiently sorted, producing cleaner and more valuable PCR. For resin producers, this trend unlocks new demand for high-performance, recyclable polyolefins, supported by partnerships between brand owners, converters, and chemical companies.

Commercialization of Advanced Purification Technologies for Food-Grade PCR

A persistent bottleneck in the packaging resins market is the limited availability of food-grade PCR. Advanced purification technologies, such as depolymerization and solvent-based recycling, are unlocking new pathways for producing virgin-quality resins. Loop Industries has commercialized PET depolymerization technology, transforming low-value waste into food-grade rPET. Similarly, PureCycle Technologies raised $300 million in June 2025 to expand its solvent purification plants for polypropylene in Belgium and Thailand, targeting global demand for high-quality rPP.

Securing reliable feedstock remains critical. Joint ventures like Cyclyx (ExxonMobil, LyondellBasell, and Agilyx) are building “circularity centers” capable of processing 136,000 tonnes of plastic waste annually to supply both mechanical and chemical recycling. These collaborations ensure stable input streams for advanced recycling, reducing dependence on volatile virgin resin supply.

As food brands face stricter regulations and consumer pressure for sustainable packaging, suppliers of food-grade PCR at scale will occupy a premium position in the value chain. The successful commercialization of purification technologies is thus a high-value growth avenue reshaping global resin flows.

Development of Bio-Based and Biodegradable Resins for Targeted Applications

Beyond recycling, the market is experiencing rapid innovation in bio-based and biodegradable resins, designed for applications where recovery and recycling remain impractical. For instance, Futamura’s NatureFlex™ films, made from wood pulp, are certified home-compostable and ideal for food-contact formats like candy wrappers and tea bags.

New-generation biopolymers are also scaling. Danimer Scientific has launched commercial PHA biopolymer production, offering materials biodegradable in soil and marine environments. Similarly, FKuR’s Bio-Flex® product line provides compostable plastics engineered as drop-in resins compatible with existing processing machinery, reducing barriers to adoption for converters.

The demand for low-carbon, biodegradable alternatives is particularly strong in markets influenced by bans on single-use plastics and consumer preference for compostable solutions. As governments introduce extended producer responsibility (EPR) schemes, bioplastics that deliver performance parity with fossil resins will capture a growing share in premium, sustainability-driven segments.

Competitive Landscape Highlighting Leaders Advancing Sustainable and High-Performance Packaging Resins

The global packaging resins market is dominated by key players leveraging innovative polymer technologies, advanced recycling, and sustainability strategies. These companies are pivotal in driving circular economy solutions, lightweighting innovations, and high-performance packaging.

LyondellBasell: Leading the Circular Economy with Recycled and Renewable Polyolefins

LyondellBasell specializes in polyolefin technologies like Hostalen ACP PE and Purell PP, widely used in food and medical packaging. In July 2025, its GXLYB joint venture received FDA clearance for recycled PE and PP for food-contact applications. The company is investing in a recycling center in Germany to transform plastic waste into high-quality feedstock. Key offerings include Circulen portfolio of recycled and renewable-based polymers, supporting sustainable packaging strategies. LyondellBasell’s strategy focuses on producing 2 million metric tons of recycled and renewable polymers annually by 2030.

Dow Inc.: Innovating High-Performance Resins for Flexible and Circular Packaging

Dow Inc. delivers a broad range of polyethylene and specialty resins engineered for lightweighting, recyclability, and enhanced barrier properties. In July 2025, Dow launched its INNATE TF 220 resin for recyclable flexible packaging and introduced D-PAK cartons made with circular and bio-circular polymers. Its portfolio includes REVOLOOP PCR resins and other solutions for sustainable packaging. Dow’s strategy emphasizes customer-centric, innovative, and circular solutions aligned with global sustainability targets.

SABIC: Driving Advanced Recycling and Circular Polyolefin Solutions

SABIC offers a wide portfolio of high-performance polyethylene and polypropylene resins with a strong focus on circular economy initiatives. In August 2025, the company introduced the LNP™ THERMOCOMP™ platform for large thermoplastic parts and expanded LNP™ ELCRIN™ copolymer resins with higher PCR content. SABIC’s TRUCIRCLE portfolio enables high-quality recycled polymers for rigid and flexible packaging. Its strategy is to leverage advanced recycling technologies and sustainable innovations to reduce environmental impact.

ExxonMobil: Expanding Advanced Recycling to Achieve High-Performance Circular Polymers

ExxonMobil provides high-performance PE and PP grades, including Exceed™ S and Vistamaxx™ brands, designed for recyclability and strength. The Baytown advanced recycling facility, operational since 2022, has processed over 80 million pounds of plastic waste, with expansion plans targeting 1 billion pounds per year. Its offerings enable improved compatibility across plastics and superior stiffness-toughness balance. ExxonMobil focuses on plastics lifecycle expansion through advanced recycling and circular economy initiatives.

TotalEnergies: Integrating Multi-Energy and Sustainable Polymer Production

TotalEnergies supplies a wide range of PE and PP resins for films, containers, and high-performance packaging. Its portfolio includes recycled, renewable, and specialty polymers, supporting circular economy adoption. The company focuses on low-carbon investments and carbon neutrality, leveraging its integrated business model from feedstock to polymer production. TotalEnergies’ strategy is to deliver innovative and sustainable polymer solutions aligned with global energy transition goals.

Braskem: Pioneering Bio-Based and Circular Polyethylene Solutions

Braskem specializes in bio-based polyethylene (PE) through its I’m Green™ brand, produced from sugarcane ethanol. In July 2025, it completed the first sale of circular PE in South America and launched the Cazoolo circular packaging design lab. Braskem aims to sell 1 million tons of recycled content products by 2030, investing in mechanical and chemical recycling technologies. Its strategy emphasizes promoting plastic circularity and sustainable bio-based materials for global packaging solutions.

Packaging Resins Market Share Insights, 2025-2034

PET and PP Dominate Market Share by Resin Type in the Packaging Resins Industry

Polyethylene terephthalate (PET) and polypropylene (PP) together account for more than half of the packaging resins market, underscoring their unmatched versatility and performance across rigid and flexible applications. PET remains the resin of choice for beverage bottles, food trays, and containers, driven by its clarity, mechanical strength, and strong recycling infrastructure (particularly rPET adoption in beverages). PP complements this dominance with its chemical resistance, high melting point, and adaptability for both rigid packaging (tubs, caps, lids) and flexible structures like biaxially oriented polypropylene (BOPP) films, which are critical for snack and confectionery packaging. The polyethylene family (LDPE/LLDPE for flexible films and HDPE for rigid containers) plays a foundational role in pouches, bags, and bottles, ensuring demand resilience. Meanwhile, PVC and PS have seen their shares contract sharply under global regulatory bans and sustainability commitments, replaced by recyclable polyolefins and paper-based substitutes. The continued strength of PET and PP illustrates their strategic positioning as resins balancing cost efficiency, recyclability, and performance in mass-market applications.

Food and Beverage Industry Commands Over Half of Resin Demand in the Packaging Resins Market

The food and beverage sector consumes 55% of all packaging resins, cementing its role as the largest and most critical end-use industry. This dominance stems from its reliance on the full resin portfolio: PET for carbonated soft drink bottles and trays, PP for rigid tubs and BOPP snack films, HDPE for dairy and household liquids, and LDPE/LLDPE for sealable flexible pouches and stretch films. The sector’s scale is amplified by global demand for packaged foods, ready-to-drink beverages, and frozen meals, where packaging plays a central role in preservation, safety, and convenience. A major driver is the accelerated transition toward sustainable resin solutions, with brands committing to post-consumer recycled (PCR) content such as rPET and rHDPE, alongside innovations in mono-material laminates that simplify recycling. While e-commerce, healthcare, and personal care each contribute high-value demand for specialized resins, the sheer consumption volume and regulatory focus on food-contact safety ensure that food and beverage packaging remains the primary engine of global resin demand.

United States Packaging Resins Market Driven by EPR Laws and Advanced Manufacturing Programs

The United States packaging resins market is undergoing a structural transformation under the influence of state-level Extended Producer Responsibility (EPR) laws. As of 2025, nearly 20% of Americans live in states with EPR regulations, including Maine, Maryland, and Washington. These policies require producers to finance and manage the end-of-life of packaging, driving strong demand for recyclable and high-performance resins that align with circular economy goals.

Government initiatives such as the National Advanced Packaging Manufacturing Program (NAPMP), part of the CHIPS for America program, are injecting up to $1.6 billion in R&D funding into advanced packaging technologies. This accelerates domestic capabilities for semiconductor packaging and precision resins, while corporate initiatives like the US Flexible Film Initiative (USFFI) launched in August 2025 are fostering innovation in flexible plastic recycling. With e-commerce and food packaging continuing to expand, the U.S. market demonstrates robust demand for sustainable, food-grade, and automation-ready resins.

Germany Packaging Resins Market Strengthened by PPWR and High Recycling Targets

Germany’s packaging resins market is driven by the EU Packaging and Packaging Waste Regulation (PPWR), in force since February 2025. This regulation sets ambitious targets for recyclability, reuse, and mandatory recycled content, including bans on certain single-use plastics by 2030 and 2040. Complementing this, the German Packaging Act (VerpackG), expanded in 2022, enforces stringent recycling quotas for paper, glass, and plastics, pushing resin producers to design materials compatible with advanced recycling streams.

German manufacturers are leaders in eco-friendly resin innovation, including bio-based polymers from PLA, PHA, and cellulose, as well as additives that reduce VOC emissions in coatings and laminates. The food, beverage, and cosmetics sectors represent core applications, with brands prioritizing resins that enable safe, recyclable, and visually appealing packaging. Germany’s combination of strict legislation and technological leadership positions it as a benchmark market for sustainable packaging resins in Europe.

China Packaging Resins Market Advanced by Dual-Carbon Targets and New Recycling Standards

The packaging resins market in China is being reshaped by the government’s dual-carbon targets, which aim for carbon peaking by 2030 and neutrality by 2060. A key regulatory milestone came in February 2026, when the State Administration for Market Regulation introduced nine new national standards for the recycled plastics industry. These rules require manufacturers to design packaging with recyclability in mind, reduce reliance on adhesives and labels, and prohibit the use of metals in bottle mouths.

Chinese manufacturers are investing heavily in automation, AI, and smart quality control systems to increase competitiveness and meet rising demand. With more than 175 billion parcel deliveries in 2024, e-commerce and consumer goods industries are fueling unprecedented demand for durable, high-performance resins. Supported by government incentives for green technology and remanufacturing, China is rapidly emerging as a global hub for sustainable and scalable packaging resins production.

India Packaging Resins Market Expanded by Make in India and Global Investments

India’s packaging resins market is benefitting from strong policy support through the Make in India initiative and the Production Linked Incentive (PLI) scheme, which encourage domestic manufacturing. The government’s EPR rules mandating 30% recycled content in rigid plastics by April 2025 are pushing companies to redesign packaging with recyclable resins.

Corporate investments are also reshaping the industry. In May 2025, Indorama Ventures acquired a 24.9% stake in EPL Limited, a global specialty packaging leader based in Mumbai. This deal reflects growing international interest in India’s packaging sector and a strategy to diversify global supply chains. At the same time, automation, robotics, and AI-enabled processes are modernizing packaging lines to enhance efficiency and reduce labor dependency. With the food and beverage sector as the largest end user, India is quickly becoming a high-growth market for recyclable and food-grade packaging resins.

Japan Packaging Resins Market Driven by Positive List System and Bio-Based Innovation

Japan’s packaging resins market is transforming under the positive list system for food contact materials, effective June 2025. This regulation defines which substances are permissible in packaging directly in contact with food and drink, pushing companies toward compliant and safe resin formulations. The rule is particularly influential in ready-to-eat and beverage packaging, where safety and performance are critical.

The market is also shaped by Japan’s climate commitments, including a 46% reduction in GHG emissions by 2030 and net-zero by 2050. Japanese firms are global leaders in developing bio-based and recyclable resins, with partnerships such as Stora Enso’s paper-based barrier solutions tailored for thermally sensitive packaging. Strong demand in ready-to-drink tea, coffee, and snack markets reflects Japan’s cultural emphasis on quality and design, ensuring ongoing growth for lightweight, durable, and sustainable resin solutions.

Brazil Packaging Resins Market Evolving with Anvisa RDC No. 983/2025 and PNRS Regulations

Brazil’s packaging resins market is undergoing regulatory transformation following Anvisa’s RDC No. 983/2025, which phases out specific substances in food-contact packaging inks and coatings. This complements the National Solid Waste Policy (PNRS), which mandates shared responsibility for waste management and drives the adoption of recyclable resin solutions.

Technological innovation is progressing as companies focus on resins that meet international food safety standards and align with circular economy targets. Brazil’s food and beverage sector, particularly canned goods and processed foods, is the largest consumer of packaging resins. Additionally, the National Commission for Chemical Safety (Conasq) has updated its registry of regulated chemicals in plastics, further encouraging the shift toward safe, compliant, and sustainable resins. Together, these changes position Brazil as a key Latin American market for eco-friendly packaging resins.

Packaging Resins Market Report Scope

Packaging Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$610.4 Billion

|

|

Market Size (2034)

|

$1094.2 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Resin Type (PET, HDPE, LDPE, PP, PVC, PS, Others), By Packaging Type (Rigid, Flexible, Semi-Rigid), By End-Use Industry (Food & Beverage, Healthcare & Pharmaceutical, Personal Care & Cosmetics, E-commerce & Logistics, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., LyondellBasell Industries N.V., SABIC, ExxonMobil Chemical, BASF SE, Chevron Phillips Chemical Company LLC, DuPont de Nemours, Inc., Eastman Chemical Company, Mitsui Chemicals, Inc., Braskem S.A., Repsol, Formosa Plastics Corporation, Hanwha Solutions, TotalEnergies, Ineos Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Resins Market Segmentation

By Resin Type

- PET

- HDPE

- LDPE

- PP

- PVC

- PS

- Others

By Packaging Type

- Rigid

- Flexible

- Semi-Rigid

By End-Use Industry

- Food & Beverage

- Healthcare & Pharmaceutical

- Personal Care & Cosmetics

- E-commerce & Logistics

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Resins Market

- Dow Inc.

- LyondellBasell Industries N.V.

- SABIC

- ExxonMobil Chemical

- BASF SE

- Chevron Phillips Chemical Company LLC

- DuPont de Nemours, Inc.

- Eastman Chemical Company

- Mitsui Chemicals, Inc.

- Braskem S.A.

- Repsol

- Formosa Plastics Corporation

- Hanwha Solutions

- TotalEnergies

- Ineos Group

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver accurate, data-driven insights on the global Packaging Resins Market, integrating both primary and secondary research. Primary research involves direct engagement with key stakeholders, including resin manufacturers, packaging converters, distributors, and industry experts, to validate market trends, technological advancements, and strategic developments. Secondary research encompasses an extensive review of industry reports, regulatory filings, corporate announcements, government policies, and trade publications to understand historical performance and forecast growth trajectories. USDAnalytics leverages advanced statistical models and scenario-based forecasting techniques to calculate market size, growth rates, and segmental trends across resin types, packaging formats, and end-use industries. Geographical analysis includes detailed country-level insights for the U.S., EU, China, India, Japan, and Brazil, ensuring a global perspective. The methodology also incorporates sustainability and circular economy factors, digital traceability innovations, and evolving regulatory frameworks to provide a holistic understanding of the market dynamics, competitive landscape, and emerging opportunities, enabling industry professionals to make informed strategic decisions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.