Packaging Inks and Coatings Market Size, Growth Forecast, and Strategic Insights

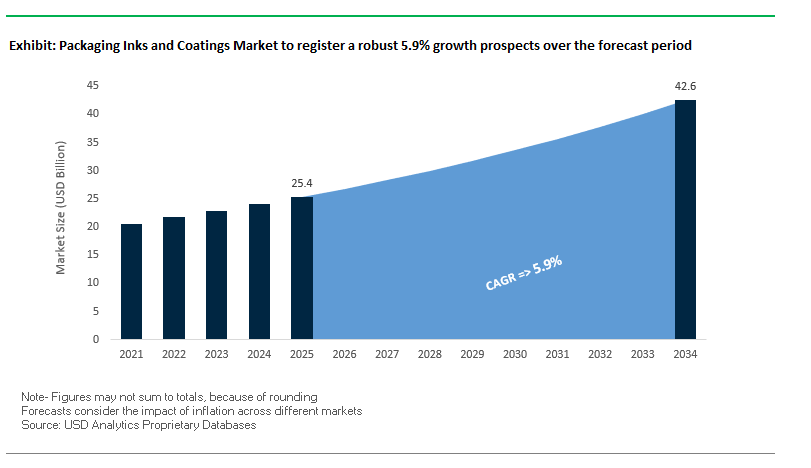

The Global Packaging Inks and Coatings Market is projected to expand from $25.4 billion in 2025 to $42.5 billion by 2034, registering a CAGR of 5.9%. Packaging inks and coatings are essential for enhancing product aesthetics, ensuring safety, and extending shelf life across a broad spectrum of packaging substrates, including flexible films, paperboard, and metal cans. This market is driven by the increasing demand for low-migration, eco-friendly, and high-performance solutions that meet stringent food, beverage, and pharmaceutical regulations.

Key Insights for Industry Stakeholders

- Food and Beverage Safety: Rising demand for low-migration inks and coatings ensures chemical safety and regulatory compliance for food, pharmaceutical, and beverage packaging.

- Sustainability Trends: Transition from solvent-based to water-based, UV-curable, and bio-based formulations reduces VOCs and enables easier recycling and composting.

- Premium Branding and Consumer Experience: High-quality digital printing, soft-touch finishes, and tactile coatings enhance brand differentiation and e-commerce appeal.

- Integration of Smart Packaging: Adoption of color-changing, thermochromic, and conductive inks enables real-time tracking, authentication, and direct brand-consumer communication.

- Circular Economy Focus: Innovations in recyclable and nitrocellulose-free inks are advancing sustainable packaging initiatives, aligning with global ESG goals.

Recent Developments Driving the Packaging Inks and Coatings Market

The Global Packaging Inks and Coatings Industry is highly dynamic, with recent developments reflecting technological innovation, sustainability, and strategic consolidation. In August 2025, Siegwerk Druckfarben AG & Co. KGaA acquired Allinova, a specialty chemicals producer, to strengthen its expertise in water-based coatings. In July 2025, Sun Chemical launched SunCure Advance ECO UV inks for folding carton applications, reducing paperboard waste during the make-ready process, while Amcor and Berry Global’s all-stock combination created a dominant presence in flexibles and rigid containers, indirectly impacting coatings demand.

May 2025 saw Mondi commissioning a €400 million paper machine at its Štětí mill, reinforcing its leadership in sustainable paper and packaging, which drives demand for compatible inks and coatings. In January 2025, Siegwerk introduced a nitrocellulose-free toolbox for flexible packaging, and Sun Chemical rolled out SunStrato AquaLam Gen2, a water-based solution for laminated and retortable packaging, significantly reducing VOC and CO₂ emissions. Earlier, in April 2024, Siegwerk launched a global business unit dedicated to functional coatings, enhancing sustainable packaging innovations aligned with the circular economy.

Trends and Opportunities Reshaping the Packaging Inks and Coatings Market

Mandated Elimination of Per- and Polyfluoroalkyl Substances (PFAS) in Food Contact Inks and Coatings

The global packaging inks and coatings market is being redefined by sweeping regulatory frameworks targeting the elimination of PFAS chemicals, which are widely used in food contact applications for their grease- and moisture-resistant properties. The European Chemicals Agency (ECHA) has proposed one of the most extensive restrictions ever under REACH, explicitly citing “printing and sealing applications.” This signals a direct challenge to PFAS usage across packaging inks and coatings, with compliance deadlines set to reshape supplier formulations. In the U.S., the EPA’s PFAS Strategic Roadmap is laying the groundwork for restrictions that extend beyond water and soil contamination to include consumer-facing products. The fragmented regulatory environment is further complicated by state-level actions, such as Washington’s PFAS ban in food packaging, requiring brand owners and converters to transition to compliant alternatives across different jurisdictions. Corporations are moving proactively: Clariant announced in November 2024 the completion of its PFAS-free additive portfolio, setting a benchmark for suppliers under pressure to reformulate. The trajectory is clear—PFAS-free packaging inks and coatings are moving from niche sustainability initiatives to mandatory compliance-driven global standards.

Rapid Adoption of UV-LED Curable Inks for Sustainability and Operational Efficiency

The transition to UV-LED curable inks is reshaping sustainability and efficiency benchmarks in the packaging sector. Unlike conventional mercury-vapor curing systems, UV-LED technology reduces energy consumption by up to 80% and offers instant on/off switching, eliminating standby energy waste. These inks are 100% solids, solvent-free, and VOC-free, making them a clear solution for companies pursuing Scope 2 carbon reduction targets. The technology also extends print versatility, enabling high-speed printing on heat-sensitive substrates such as flexible plastic films without warping. Press manufacturers are investing aggressively: HP Indigo has introduced UV-LED compatible presses, while Sun Chemical launched its “SunCure EcoPlast” and “SunCure Advance ECO UV” ink lines, optimized for flexible packaging and folding cartons. Beyond sustainability, UV-LED curing delivers improved image sharpness and consistent curing quality, which translates into higher throughput, reduced rejects, and superior shelf appeal. This dual benefit of operational performance and sustainability compliance is making UV-LED inks one of the fastest-growing technology adoptions in the market.

Development of High-Performance Bio-Based Inks and Varnishes

The push for bio-based inks and varnishes represents a major growth avenue in packaging sustainability. A standout example is Living Ink Technologies’ algae-based black pigment, which transforms discarded algae cells into a carbon-negative alternative to carbon black, one of the most widely used ink ingredients. Academic research supports further innovation—soy protein isolate-based inks have been engineered with rheological properties suitable for both conventional and 3D printing, with potential to be enhanced through biopolymer blends. The key advantage lies in end-of-life compatibility: unlike petroleum-based inks, bio-based inks do not disrupt paper recycling or composting streams, aligning with circular economy goals. Market adoption is accelerating in niche applications such as compostable food packaging and organic-certified products, where consumer-facing sustainability credentials are a competitive differentiator. As infrastructure for compostable packaging grows, bio-based inks and varnishes are poised to expand from niche segments into mainstream adoption, driven by brand-owner commitments to renewable raw materials.

Integration of Functional and Smart Inks for Brand Protection and Engagement

The integration of functional and smart inks is moving packaging beyond protection into an era of interactivity, traceability, and security. The HolyGrail 2.0 initiative has validated the use of digital watermarking inks, achieving over 90% sorting efficiency and SKU-level identification of more than 6,000 product types during German industrial trials. This capability is critical for creating high-quality recycled streams and fulfilling EPR obligations. Parallel innovations in conductive inks are unlocking applications in printed electronics—Henkel has advanced RFID antennas and temperature sensors that can be printed directly on packaging substrates, offering real-time monitoring and connectivity. In brand protection, NanoMatriX’s security inks change color under UV light or with temperature shifts, providing a cost-effective safeguard against counterfeiting in pharmaceuticals and luxury goods. Consumer engagement is also being redefined through thermochromic inks that indicate freshness or optimal consumption conditions, and interactive conductive inks that trigger digital content. These solutions are transforming packaging into a data-rich, consumer-facing platform, while delivering operational benefits in traceability and supply chain transparency.

Competitive Landscape: Leading Players Shaping Packaging Inks and Coatings Innovation

The Global Packaging Inks and Coatings Market is driven by key players leveraging advanced materials science, sustainable manufacturing, and functional design to deliver high-performance, safe, and eco-friendly solutions for diverse packaging applications.

Siegwerk Druckfarben AG & Co. KGaA: Expanding Expertise in Water-Based and Low-Migration Inks

Siegwerk is a leading global supplier of printing inks and coatings, with a strong focus on food-safe, low-migration, and sustainable solutions. In August 2025, it acquired Allinova to expand its capabilities in functional and water-based coatings. The company also introduced a nitrocellulose-free toolbox for flexible packaging, supporting recyclable and high-performing solutions. Siegwerk’s portfolio includes inks for flexographic, gravure, and offset printing, catering to flexible plastics, paper, and metal cans. The strategic focus is on circular economy solutions, enhanced recyclability, and product safety.

Sun Chemical Corporation (DIC Group): Innovating Sustainable and Water-Based Packaging Solutions

Sun Chemical, part of the DIC Group, is the world’s largest producer of printing inks and pigments, emphasizing R&D-driven sustainable solutions. In July 2025, it launched SunCure Advance ECO UV sheetfed inks for folding cartons, and in January 2025, rolled out SunStrato AquaLam Gen2, a water-based solution reducing VOC and CO₂ emissions. The company offers a comprehensive portfolio for flexible packaging, folding cartons, and metal containers, including water-based, solvent-based, and UV/EB-curable inks. Sun Chemical focuses on environmentally friendly, high-performance coatings that improve recyclability and meet global sustainability goals.

Flint Group: Providing Broad Spectrum and Food-Safe Packaging Inks

Flint Group is a global supplier of printing inks and plates, specializing in conventional and energy-curable formulations for packaging. The company has been developing low-migration, food-safe inks and sustainable solutions for flexographic, gravure, and digital printing. Flint Group’s offerings include functional and protective coatings across various packaging substrates. Its strategic focus lies in innovation, operational excellence, and sustainable growth, ensuring its inks meet evolving global packaging demands.

Artience (formerly Toyo Ink SC Holdings Co., Ltd.): Leading with Functional Coatings and Logistics Efficiency

Artience, based in Japan, specializes in advanced functional inks and coatings for flexible packaging, labels, and metal cans. In July 2025, it initiated a joint delivery program with other ink manufacturers to improve logistics efficiency. Artience emphasizes high-performance adhesives, resins, and coatings with environmental compliance. Its strategic focus, based on the “artience” philosophy, is on creating value through the fusion of art and science, expanding global presence, and driving sustainable product development.

PPG Industries, Inc.: Delivering High-Performance Sustainable Packaging Coatings

PPG Industries is a global leader in paints and coatings, including packaging applications. Its core strength is in innovation-driven, sustainable coatings for metal, plastic, and glass packaging in food, beverage, and personal care markets. Recent reports highlight strong growth in packaging coatings, driven by technological advancements and sustainability initiatives. PPG offers waterborne, solvent-based, and UV/EB-curable coatings, focusing on improving recyclability, reducing environmental impact, and strengthening its global packaging footprint.

Packaging Inks and Coatings Market Share Insights, 2025-2034

Coatings Dominate Market Share by Product Type in the Packaging Inks and Coatings Industry

Coatings represent 55% of the global packaging inks and coatings market, underscoring their indispensable role in functional packaging performance. Unlike inks, which primarily serve branding and communication purposes, coatings are required across virtually every package to deliver essential properties such as moisture resistance, grease protection, scuff durability, sealability, and finish control (gloss or matte). Their dominance is directly linked to the rising demand for functional packaging in food, beverage, pharmaceutical, and industrial sectors, where coatings extend shelf-life, protect product integrity, and ensure regulatory compliance. Furthermore, advanced coatings such as heat-seal varnishes for flexible packaging, soft-touch coatings for premium personal care goods, and barrier coatings replacing plastic laminates are gaining traction due to sustainability mandates. While inks remain vital for branding and consumer engagement, coatings secure the larger share because they are non-negotiable for product protection, safety, and performance across all packaging substrates.

Flexography Leads Market Share by Printing Technology in the Packaging Inks and Coatings Industry

Flexography commands 40% of the packaging inks and coatings market by printing technology, making it the industry’s workhorse due to its cost efficiency, substrate versatility, and continuous improvements in plate-making and ink chemistry. Its dominance is particularly evident in corrugated packaging, flexible films, and labels, where long and medium-run print jobs require both speed and adaptability. Advancements in UV-flexo inks, water-based systems, and higher-definition plates have significantly improved flexographic print quality, allowing it to compete with offset and gravure for graphics-intensive packaging. Rotogravure maintains strength in very high-volume, premium-quality runs, while digital printing is rapidly gaining share in short-run, variable-data applications aligned with e-commerce and personalized marketing. However, flexography continues to hold the top share because it balances economy of scale, speed, and regulatory compliance, positioning it as the most commercially viable printing method in global packaging operations.

Food & Beverage Packaging Accounts for the Largest Market Share by End-Use in the Packaging Inks and Coatings Industry

The food and beverage industry represents 52% of the global packaging inks and coatings demand, making it the undisputed leader in end-use consumption. This dominance is fueled by the sheer volume of flexible packaging, folding cartons, and labels required to serve one of the world’s largest and most fast-moving supply chains. The sector’s influence extends beyond scale: strict global food safety regulations drive adoption of low-migration inks, functional coatings, and recyclable barrier technologies to ensure consumer safety and regulatory compliance. The sector is also shaping innovation, as brand owners increasingly require inks and coatings that support sustainability goals, improved recyclability, and high-definition shelf appeal. While pharmaceutical and healthcare packaging demands higher-value specialized inks and coatings, and personal care focuses on aesthetics and premium finishes, food and beverage remains the core engine of demand, dictating the majority of material and technology advancements across the industry.

United States Packaging Inks and Coatings Market Shaped by FDA Oversight and Sustainability Shift

The United States packaging inks and coatings market is experiencing rapid regulatory evolution as the FDA intensifies oversight of food contact substances. A major development under consideration is the reform of the “Generally Recognized As Safe” (GRAS) determination process, which could subject all inks and coatings for packaging to more rigorous review. This potential shift would significantly impact food and beverage packaging companies, requiring greater compliance and documentation. Additionally, state-level policies are expanding the patchwork of regulations, compelling converters and brand owners to prioritize safer and recyclable formulations.

From a technology perspective, the U.S. is advancing eco-friendly ink and coating systems, including water-based, bio-based, and UV-curable formulations that reduce VOC emissions. Functional barrier coatings are gaining traction, enabling the production of recyclable mono-material packaging while ensuring food safety. Corporate initiatives are reinforcing this momentum: brands are investing in deinkable inks that simplify recycling and support circular economy goals. Key applications are concentrated in food, beverages, pharmaceuticals, and consumer goods, where advanced inks deliver not only safety and compliance but also brand differentiation and anti-counterfeiting functions.

Germany Packaging Inks and Coatings Market Driven by EU PPWR and Circular Economy Standards

Germany’s packaging inks and coatings market is directly shaped by the European Union’s Packaging and Packaging Waste Regulation (PPWR), which sets ambitious recyclability and reuse targets. Under this framework, German producers are innovating deinkable and low-contamination inks that improve recycling efficiency. The PPWR and the amended German Packaging Act also promote the minimization of ink use, compelling the industry to re-engineer printing processes with sustainability at the core.

German companies are leading in circular economy-compatible inks and coatings, developing durable inks that withstand multiple wash cycles in reusable packaging systems. Simultaneously, easy-to-remove inks are being designed for variable data like batch coding to facilitate efficient recycling. Investments are aligning with Germany’s high-tech packaging machinery sector, where digital printing and direct-to-shape printing technologies require inks that are both sustainable and compatible with advanced lines. Key applications are strongest in food, beverages, and cosmetics packaging, where compliance with EU safety standards and premium-quality branding are equally critical.

China Packaging Inks and Coatings Market Accelerated by VOC Regulations and E-Commerce Expansion

The packaging inks and coatings market in China is being reshaped by government-led sustainability measures tied to dual-carbon targets of 2030 (carbon peaking) and 2060 (carbon neutrality). In April 2021, mandatory national standards for VOC limits in printing inks came into force, directly driving innovation toward water-based and eco-friendly formulations. Moreover, the National Health Commission (NHC) has introduced the first specific standards for food-contact inks, requiring compliance with good manufacturing practices and food safety criteria.

Chinese manufacturers are also investing in automation and smart manufacturing systems to strengthen domestic production of advanced inks and coatings, aligned with the Made in China 2025 policy that targets 70% domestic content in key materials. Demand is booming across consumer goods, e-commerce, and electronics packaging, with the scale of China’s production requiring efficient, high-volume, and environmentally compliant inks. The sector is strategically critical for enabling traceability, safe branding, and sustainable packaging at massive scale.

India Packaging Inks and Coatings Market Reinforced by Toluene Ban and Industry Investments

India’s packaging inks and coatings market is undergoing significant transformation under the Bureau of Indian Standards (BIS) regulation that prohibits toluene-based inks for food packaging. This landmark decision under IS15495 has pushed the market toward safer alternatives, promoting water-based, PVC-free, and toluene-free inks that align with global sustainability standards. The regulatory shift is also encouraging adoption of eco-friendly coatings for food contact applications, strengthening consumer safety and recycling potential.

Corporate and international investments are driving growth. Siegwerk has committed INR 350 crore (US$42 million) to expand operations across India over the next three years, enhancing its Global Innovation and Capability Center (GICC) and expanding production facilities. Companies like Siegwerk and DIC are pioneering solutions such as low-VOC, recyclable, and food-safe inks, catering to rising demand in India’s food processing, pharmaceuticals, and e-commerce packaging sectors. With supermarkets and online retail expanding, packaging inks and coatings are becoming essential for brand presentation, safety, and protection.

Japan Packaging Inks and Coatings Market Evolving Under Positive List Rules and Bio-Based Innovation

The Japanese packaging inks and coatings market is adapting to the positive list system for food-contact materials, which took effect on June 1, 2025. This regulation strictly defines permissible substances, compelling manufacturers to reformulate inks and coatings to meet food safety standards. It has also catalyzed innovation in barrier coatings for packaging films, as well as inks that align with Japan’s regulatory and consumer safety priorities.

Technology development is closely tied to Japan’s sustainability goals of cutting GHG emissions 46% by 2030 and achieving net zero by 2050. Companies are investing in bio-based and recyclable ink solutions, aiming to balance high-quality performance with eco-compliance. Advanced coatings that extend shelf life while supporting recyclability are also in focus. Key applications are concentrated in ready-to-drink beverages, snack foods, and premium consumer packaging, where Japanese manufacturers emphasize lightweight, durable, and aesthetically superior packaging enhanced by safe and sustainable inks.

Brazil Packaging Inks and Coatings Market Shaped by ANVISA Food Safety Rules and PNRS Recycling Goals

Brazil’s packaging inks and coatings market is strongly influenced by the Brazilian Health Regulatory Agency (ANVISA). In April 2024, ANVISA issued a resolution revising standards for metallic food-contact materials, with direct implications for the coatings used on cans and packaging lines. This regulation elevates the importance of sanitary compliance and safety testing in packaging coatings, particularly for the food and beverage sector.

Sustainability goals are reinforced by Brazil’s National Solid Waste Policy (PNRS), which obligates companies to recycle a growing share of packaging waste. This regulatory push is driving demand for inks and coatings compatible with recycling processes and aligned with international food safety standards. Manufacturers are increasingly turning toward bio-based coatings and low-VOC ink systems to meet global export requirements. With Brazil being a leading producer of canned goods and beverages, the market shows strong reliance on safe barrier coatings and advanced inks that ensure product integrity while meeting evolving consumer and environmental expectations.

Packaging Inks and Coatings Market Report Scope

Packaging Inks and Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.4 Billion

|

|

Market Size (2034)

|

$42.5 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Product Type (Inks, Coatings), By Ink Type (Solvent-based, Water-based, UV-cured, Others), By Printing Technology (Flexography, Rotogravure, Offset Lithography, Digital Printing), By Substrate (Flexible Packaging, Paper & Paperboard, Rigid Plastics, Metal, Glass), By End-Use Industry (Food & Beverage, Personal Care & Cosmetics, Pharmaceutical & Healthcare, Industrial, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DIC Corporation, Siegwerk Druckfarben AG & Co. KGaA, Flint Group, Sun Chemical Corporation, AkzoNobel N.V., The Sherwin-Williams Company, Jotun A/S, Sakata INX Corporation, Toyo Ink SC Holdings Co., Ltd., T&K Toka Co., Ltd., Hubergroup, PPG Industries, Inc., Zeller+Gmelin GmbH & Co. KG, KAO Corporation, Resil Chemicals Private Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Inks and Coatings Market Segmentation

By Product Type

By Ink Type

- Solvent-based

- Water-based

- UV-cured

- Others

By Printing Technology

- Flexography

- Rotogravure

- Offset Lithography

- Digital Printing

By Substrate

- Flexible Packaging

- Paper & Paperboard

- Rigid Plastics

- Metal

- Glass

By End-Use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Pharmaceutical & Healthcare

- Industrial

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Inks and Coatings Market

- DIC Corporation

- Siegwerk Druckfarben AG & Co. KGaA

- Flint Group

- Sun Chemical Corporation

- AkzoNobel N.V.

- The Sherwin-Williams Company

- Jotun A/S

- Sakata INX Corporation

- Toyo Ink SC Holdings Co., Ltd.

- T&K Toka Co., Ltd.

- Hubergroup

- PPG Industries, Inc.

- Zeller+Gmelin GmbH & Co. KG

- KAO Corporation

- Resil Chemicals Private Limited

* List Not Exhaustive

Methodology

The research methodology for the Global Packaging Inks and Coatings Market integrates both primary and secondary research techniques to deliver precise, actionable insights for industry professionals. USDAnalytics conducted extensive primary research by engaging with key stakeholders, including packaging engineers, ink chemists, sustainability experts, regulatory authorities, and executives from leading market players such as Siegwerk, Sun Chemical, Flint Group, PPG Industries, and Artience across North America, Europe, and Asia-Pacific. Secondary research involved an in-depth analysis of company annual reports, patents, regulatory databases, sustainability disclosures, trade publications, and verified industry journals. Advanced data triangulation was applied to validate market sizing, CAGR, and product-specific growth trends, incorporating macroeconomic indicators, raw material costs, technological adoption rates, and regional regulatory frameworks such as the EU PPWR, U.S. FDA regulations, China VOC standards, and India’s toluene ban. Both top-down and bottom-up forecasting approaches were employed, while regional insights were contextualized against policy mandates, circular economy initiatives, and emerging e-commerce and consumer trends. This rigorous methodology ensures that USDAnalytics provides fact-based, high-confidence insights on market dynamics, competitive strategies, and sustainable innovation opportunities within the packaging inks and coatings industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.