Market Overview: Key Growth Insights in Confectionery Packaging Industry

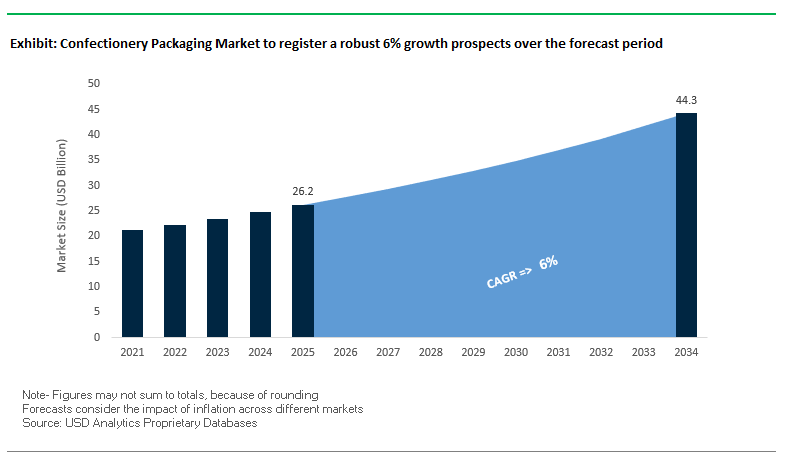

The Global Confectionery Packaging Market is forecasted to reach USD 26.2 billion in 2025 and grow to USD 44.3 billion by 2034, registering a solid CAGR of 6%. The market is witnessing significant transformation as brand owners and packaging manufacturers prioritize sustainability, shelf-life extension, and consumer convenience. Confectionery products such as chocolates, candies, and biscuits are highly sensitive to moisture, light, and oxygen, making advanced packaging solutions critical to ensuring quality and extending shelf stability.

Flexible films, including laminates and multilayer structures, dominate the confectionery packaging segment because of their excellent barrier performance. In parallel, sustainability is reshaping innovation, with rising adoption of recyclable mono-material films and compostable paper-based packaging. Another key growth driver is the rise of on-the-go consumption, which is fueling demand for single-serve and re-sealable formats with zippers and easy-open features. Moreover, the role of visual branding is pivotal, as confectionery remains an impulse-driven purchase category. Brands are increasingly investing in premium aesthetics matte/gloss finishes, advanced printing, and structural creativity to stand out in crowded retail environments.

Key Insights for Industry Professionals:

- Flexible films dominate due to moisture and oxygen barrier properties.

- Sustainable packaging (mono-material and paper-based) is accelerating.

- Single-serve and re-sealable packs fuel on-the-go snacking demand.

- Premium visuals and structural design drive brand differentiation.

Market Analysis: Recent Strategic Developments in Confectionery Packaging

The confectionery packaging market has been highly dynamic, with innovations in sustainability and structural performance shaping its trajectory. In August 2025, Mondi Group launched its FunctionalBarrier Paper Ultimate, a breakthrough in high-barrier paper-based solutions that reflects the accelerating trend toward paperization in flexible packaging. Also in August 2025, Graphic Packaging International launched a child-resistant paperboard pod pack that reinforces the broader shift to fiber-based packaging across industries, with strong spillover into confectionery formats.

In July 2025, Amcor advanced its sustainability agenda with the launch of the Hector CRC closure made from 100% PCR plastic, while expanding its healthcare packaging footprint in Costa Rica and upgrading its UK recycling facility. In the same month, Sonoco Products Company announced a USD 30 million expansion in adhesives and sealants production, a strategic move to strengthen flexible packaging supply resilience. Earlier, in April 2025, The Hershey Company unveiled its packaging strategy at the NCA Sweets & Snacks Expo, showcasing consumer-centric and sustainable design innovations.

Sustainable material advancements are also emerging from coating specialists. In March 2024, Melodea launched VBseal, a coating solution that provides moisture, aroma, and oil resistance with heat-sealing functionality, designed to replace single-use plastics in confectionery wraps. Similarly, in October 2023, Adapa introduced PaperTwister(re), a paper-based twist-wrap for confectionery that operates at industrial-scale speeds of 2,300 pieces per minute. Further back, in March 2023, Parkside launched a recyclable mono-polymer film that combines superior gas, UV, and oil resistance, extending confectionery shelf life and reducing food waste.

Emerging Trends and Strategic Opportunities Shaping the Confectionery Packaging Market

Accelerated Shift to Monomaterial Plastic Structures for Recyclability

The confectionery packaging market is undergoing a significant transformation with brands shifting from multi-material laminates to advanced monomaterial flexible packaging to meet sustainability mandates. Driven by stringent Extended Producer Responsibility (EPR) regulations and rising consumer demand for circularity, these monomaterial structures, often made from polypropylene (PP) or polyethylene (PE), are designed to be fully recyclable while maintaining essential barrier properties for freshness and aroma. Regulatory pressure, such as the EU’s Packaging and Packaging Waste Regulation (PPWR), mandates that all packaging be recyclable by 2030, creating a powerful impetus for the adoption of monomaterial films. Companies like Nestlé and Mars are already implementing this technology Nestlé with its KitKat® products in the UK and Ireland using 75% recycled plastic, and Mars with fully recyclable pouches for pet foods, a technology transferrable to confectionery applications. The transition to monomaterial films requires innovative material science to replicate barrier and mechanical performance previously achieved with multi-layer laminates. This trend represents a high-growth opportunity for suppliers who can deliver high-performance, recyclable films aligned with brand sustainability goals.

Integration of Digital Watermarks for Advanced Sorting and Consumer Engagement

Digital watermarking technology, exemplified by the HolyGrail 2.0 initiative, is being adopted to overcome challenges in sorting small-format flexible packaging. Nearly invisible codes embedded in packaging enable high-speed, precise sorting in recycling facilities using specialized cameras, enhancing material recovery and producing higher-quality recyclates. Beyond sustainability, these digital watermarks offer a platform for consumer engagement, allowing customers to scan packages to access brand stories, sustainability credentials, and recycling guidance. The HolyGrail 2.0 initiative, with over 85 partners including Mondelēz International and Nestlé, has demonstrated over 99% detection accuracy in semi-industrial trials, proving the technology’s scalability. This innovation requires collaboration across the value chain from brand owners and converters to recyclers and provides a new value proposition for the confectionery packaging market by merging recyclability with a connected consumer experience.

Development of High-Barrier Paper-Based Solutions for Premium Chocolate

Premium chocolate brands are driving the need for high-barrier paper-based packaging that eliminates the need for plastic linings while preserving product integrity. These films provide sufficient oxygen and moisture barriers to prevent fat bloom and maintain freshness, catering to environmentally conscious consumers willing to pay a premium for sustainable solutions. Companies like Repaq are leading innovations in paper-based films that are home-compostable and maintain the same protective qualities as traditional plastic laminates. This trend represents a growth avenue in the premium segment of the confectionery packaging market, combining sustainability, aesthetics, and performance. It also demands new collaborations between paper manufacturers, converters, and confectionery brands, as well as investments in specialized converting and sealing technologies, reshaping the value chain toward more sustainable practices.

Adoption of Smart Packaging for Enhanced Traceability and Anti-Counterfeiting

With the premium confectionery segment vulnerable to counterfeiting, smart packaging solutions offer authentication, end-to-end supply chain traceability, and enhanced consumer engagement. Technologies such as NFC chips, QR codes, invisible signatures, and AI-driven anti-counterfeiting systems are being deployed to protect product integrity. Companies like Ennoventure are at the forefront of integrating these solutions into packaging, enabling brands to verify authenticity, communicate product origin, and engage consumers through digital experiences. This opportunity establishes a high-value segment within the confectionery packaging market, enhancing brand protection and fostering consumer trust. Adoption of smart packaging also necessitates cross-industry collaborations and investments in IT infrastructure, transforming the confectionery packaging value chain into a more secure and transparent system.

Competitive Landscape: Leading Companies in Confectionery Packaging Market

The competitive landscape of the global confectionery packaging industry is shaped by multinational packaging leaders, material specialists, and sustainability-driven innovators. Companies are investing heavily in recyclable films, compostable solutions, and fiber-based packaging to align with regulatory pressures and consumer sustainability demands.

Amcor PLC expands sustainable confectionery packaging solutions

Amcor is a global packaging leader with strong expertise in flexible films and laminates for confectionery. In August 2025, it expanded its healthcare packaging network in Costa Rica and upgraded its UK recycling facility, reinforcing its sustainability commitments. Amcor’s target is to make all packaging recyclable or reusable by 2025, with a strong focus on circular economy solutions. Its integration capabilities and global footprint make it a reliable partner for both small confectionery brands and multinational producers.

Constantia Flexibles innovates with digital printing and mono-material laminates

Constantia Flexibles is a global player in flexible packaging, with a strong confectionery presence. In August 2025, the company showcased new technologies at FACHPACK 2025, including a digital printing line in Copenhagen capable of water-based full-surface printing on PET and aluminum substrates. Its Ecolutions line emphasizes recyclable mono-material laminates, balancing sustainability with superior shelf-life performance. Constantia’s laminated and multilayer substrates provide customized solutions for chocolates and candies, integrating both aesthetics and protection.

Mondi Group accelerates paper-based high-barrier packaging

Mondi is a leader in paper-based packaging solutions with strong relevance to confectionery. In September 2025, it launched its FunctionalBarrier Paper Ultimate, offering high oxygen, vapor, and grease protection while remaining recyclable or compostable. Mondi’s strategic focus is on “paperization,” with a goal of 100% reusable, recyclable, or compostable packaging by 2025. Its growing portfolio of stand-up pouches and paper wraps provides a direct substitute for conventional plastics in confectionery markets.

Huhtamaki Oyj strengthens global footprint in sustainable packaging

Huhtamaki is a global packaging specialist with a diversified portfolio spanning flexible materials to paperboard conversion. The company invests significantly in R&D for circular economy solutions, with a focus on innovations that balance convenience, sustainability, and cost-effectiveness. Its global footprint, particularly in emerging markets, allows it to scale packaging innovations rapidly. For confectionery, Huhtamaki provides twist wraps, pouches, and labels that combine high barrier protection with premium branding aesthetics.

Sonoco Products Company invests in adhesives and flexible packaging capacity

Sonoco is a leading supplier of consumer and industrial packaging with growing activity in confectionery. In July 2025, it invested USD 30 million to expand adhesives and sealants capacity, strengthening its flexible packaging performance. Its EnviroSense™ product line includes recyclable rigid paper containers with paperboard ends, designed to replace traditional plastic formats. Sonoco’s strategy “Better Packaging. Better Life.” aligns directly with the sustainability goals of global confectionery brands.

Sealed Air Corporation advances Cryovac high-barrier films

Sealed Air is well recognized for its Cryovac brand, which supplies high-barrier multilayer films used across food and confectionery segments. The company focuses on lightweighting technologies and sustainable material use, while continuously expanding R&D for advanced film solutions. Sealed Air’s expertise in barrier protection and its extensive global network strengthen its position in confectionery, where packaging performance and sustainability are equally critical.

Confectionery Packaging Market Share Insights

Flexible Packaging Commands Market Share by Format in Confectionery Packaging

Flexible packaging secures a 65% share of the confectionery packaging market, underscoring its unmatched efficiency, cost competitiveness, and adaptability to diverse product formats. Flow wraps, pouches, and laminates are ideal for single-serve packs and impulse-purchase products such as candies, chocolates, and mints. The dominance of flexible formats is further strengthened by advances in mono-material PP and PE laminates and recyclable paper-based wraps, which address sustainability regulations without compromising barrier performance. Rigid packaging, while secondary, remains critical in high-value confectionery segments such as premium chocolates and seasonal gift assortments, where aesthetic appeal and structural protection are indispensable. This segmentation reflects a two-speed market: flexible packaging leading in volume-driven, cost-sensitive mass segments, and rigid packaging reinforcing brand positioning in premium niches.

Chocolate Holds the Largest Market Share by Confectionery Type

Chocolate dominates the confectionery packaging industry with a 45% share, driven by its unique technical and commercial requirements. Unlike sugar confectionery or gum, chocolate demands exceptional moisture, oxygen, and light barriers to prevent fat bloom and preserve flavor integrity, pushing the need for high-barrier laminates and foil-based composites. The premiumization trend further amplifies chocolate’s share, as luxury brands rely on rigid boxes, specialty foils, and embossed cartons to reinforce gifting culture and brand prestige. Sugar confectionery, though higher in sales volume, relies primarily on low-cost flexible packaging for impulse and bulk sales, while gum & mints occupy a niche with highly specialized formats such as blister packs, tins, and proprietary dispensers. Emerging confectionery segments including functional candies, nutrition bars, and cannabis-infused confectionery are pioneering sustainable and hybrid packaging formats, but chocolate remains the high-value anchor of the industry due to its dual demand for protection and premium presentation.

United States Confectionery Packaging Market Driven by FDA Regulations and Sustainable Innovation

The U.S. confectionery packaging market is strongly influenced by food safety and labeling regulations enforced by the Food and Drug Administration (FDA), alongside sustainability initiatives like the U.S. Plastics Pact. These programs are encouraging brand owners to adopt recyclable and compostable packaging designs. Technological advancements are focused on enhancing product protection and consumer experience, with innovations in resealable and easy-to-open packaging using advanced flexible films and pouches. Brands are increasingly leveraging “experiential indulgence,” including interactive packaging and pop culture collaborations, to elevate consumer engagement.

Corporate investments exemplify this trend, such as Adapa’s October 2023 launch of the PaperTwister® packaging, designed for high-speed operations while offering sustainability benefits. Key applications span retail, e-commerce, and food service sectors, with online confectionery sales and home delivery driving demand. Sustainability-focused innovation is on the rise, including mono-material designs for simplified recycling and biodegradable or compostable materials. Additionally, smart packaging with embedded sensors and smaller, hygienic pack sizes are being adopted to meet evolving consumer preferences for convenience, portion control, and premium experiences.

Germany Confectionery Packaging Market Strengthened by Circular Economy Compliance and Advanced Technology

Germany’s confectionery packaging market is guided by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating full recyclability or reusability of all packaging by 2030. Stringent quality assurance practices and compliance with Good Distribution Practice (GDP) guidelines ensure the reliability of high-performance packaging systems. Technological innovation includes machinery for sustainable material handling and the production of mono-material films, meeting regulatory and consumer demands.

Key applications focus on food and retail sectors, with a particular emphasis on artisanal and premium products. R&D collaborations between German companies and institutions are creating lighter, stronger, and more sustainable packaging solutions, including digital product passports and watermarks for enhanced material transparency and recycling. The EU PPWR’s exemptions for certain compostable materials are catalyzing the development of home and industrial compostable packaging, while digital printing technologies enable seasonal and influencer-driven packaging designs without extensive setup times, aligning with marketing and consumer engagement trends.

China Confectionery Packaging Market Driven by Green Policies and Domestic Production Expansion

China’s confectionery packaging market is heavily influenced by the government’s “dual carbon” goal and the March 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement,” which encourage the adoption of sustainable materials and recycling practices. Regulatory reforms, including directives from the State Post Bureau for express delivery companies to prioritize eco-friendly, reusable packaging, are shaping market operations.

Technological advancements are focused on automation, AI integration, and “5G plus industrial internet” solutions, optimizing production processes and supporting flexible capacity for complex packaging designs. Domestic manufacturing is being prioritized to reduce reliance on imported technology, ensuring high-quality local production. Rapid growth in e-commerce, fresh food, and food delivery sectors is a key driver, alongside government initiatives to prevent over-packaging through a “whole-chain administration system.” Continuous research and development, supported by a high number of patents, positions China as a leader in innovative confectionery packaging solutions.

United Kingdom Confectionery Packaging Market Accelerated by Plastic Tax and Recycling Initiatives

The UK confectionery packaging market is impacted by the government’s plastic packaging tax and single-use plastic bans, compelling brands to adopt more sustainable solutions. Technological advancements are centered on mono-material films that simplify recycling, exemplified by Parkside’s March 2023 launch of recyclable mono-polymer films with superior barrier performance.

Corporate investments support sustainability goals, including BillerudKorsnäs’ 2020 collaboration with Syntegon Technology to develop recyclable paper-based flow wraps. Key applications include retail and online grocery delivery sectors, where durable and protective packaging is critical to withstand shipping and handling. Consumer trends show rising demand for “free-from” products, such as sugar-free and gluten-free confectionery, requiring specialized packaging to maintain product integrity and prevent contamination. The UK Plastic Pact’s target of 70% recycling or composting by 2025 is further accelerating the adoption of eco-friendly packaging in the confectionery sector.

Japan Confectionery Packaging Market Innovating Through Precision Manufacturing and High-Performance Films

Japan’s confectionery packaging industry is characterized by advanced manufacturing and precision engineering, integrating traditional aesthetics with modern design. Regulatory guidance, such as the Plastic Resource Circulation Act (April 2022), promotes “Design for the Environment” principles and reduction of single-use plastics.

Focus is on high-performance films with superior barrier properties, dimensional stability, and IoT-enabled sensors for real-time monitoring. Functional innovation includes specialty packaging to prevent deformation and maintain quality. Corporate collaborations, including Nestlé and Meiji, are driving new high-performance film development, as seen in Nestlé’s April 2025 KitKat packaging strategy. Academic research further supports sustainability, with biopolymers and natural agents being explored to create innovative, eco-friendly packaging solutions. ITO EN’s October 2024 SIG SmileSmall carton packs for ready-to-drink matcha demonstrate the market’s focus on convenience, sustainability, and consumer-centric design.

Brazil Confectionery Packaging Market Boosted by Regulatory Push and Sustainable Technology Investments

Brazil’s confectionery packaging market is shaped by the National Solid Waste Policy and 2024 legislation targeting single-use plastics, with a 2030 deadline for fully compostable or recyclable packaging. Technological advancements include robotics and AI applications for quality control, and development of biodegradable films using carboxymethyl cellulose (CMC) from sugarcane bagasse.

The sustainable packaging sector is growing rapidly, driven by innovations in materials and green manufacturing. Key applications include food, beverage, and cosmetics packaging, with the expanding food processing industry increasing demand for advanced solutions. Governmental support, including upcoming decrees to enforce recycling targets (30% this year and 50% by 2040), is incentivizing sustainable practices. Corporate initiatives, exemplified by Dengo Chocolates, focus on reusable and eco-friendly packaging designs, highlighting a market-wide shift toward sustainability-oriented innovation.

Confectionery Packaging Market Report Scope

Confectionery Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$26.2 Billion

|

|

Market Size (2034)

|

$44.3 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Packaging Material (Paper & Paperboard, Plastic, Metal, Glass, Others), By Packaging Format (Flexible Packaging, Rigid Packaging), By Confectionery Type (Chocolate, Sugar Confectionery, Gum & Mints, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Smurfit Kappa Group plc, Huhtamaki Oyj, Constantia Flexibles, Sonoco Products Company, DS Smith plc, WestRock Company, Sealed Air Corporation, Silgan Holdings Inc., Berry Global Group, Inc., AR Packaging, Ahlstrom-Munksjö, Uflex Ltd., Cosmo Films Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Confectionery Packaging Market Segmentation

By Packaging Material

- Paper & Paperboard

- Plastic

- Metal

- Glass

- Others

By Packaging Format

- Flexible Packaging

- Rigid Packaging

By Confectionery Type

- Chocolate

- Sugar Confectionery

- Gum & Mints

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Confectionery Packaging Market

- Amcor plc

- Mondi Group

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- Constantia Flexibles

- Sonoco Products Company

- DS Smith plc

- WestRock Company

- Sealed Air Corporation

- Silgan Holdings Inc.

- Berry Global Group, Inc.

- AR Packaging

- Ahlstrom-Munksjö

- Uflex Ltd.

- Cosmo Films Limited

* List Not Exhaustive

Methodology

The findings in this Confectionery Packaging Market report have been prepared by USDAnalytics using a comprehensive methodology that combines both primary and secondary research approaches to ensure accuracy and actionable insights for industry professionals. Primary research involved interviews with key stakeholders, including packaging manufacturers, material suppliers, brand owners, and regulatory authorities, to gather detailed perspectives on emerging trends, material innovations, and market challenges. Secondary research included rigorous analysis of corporate press releases, product launches, patent filings, regulatory updates, industry journals, and sustainability reports, with a particular focus on advancements in flexible films, mono-material laminates, paper-based high-barrier solutions, and smart packaging technologies. USDAnalytics also assessed global regulatory impacts, including EU PPWR, FDA guidelines, Plastic Tax in the UK, and Japan’s Plastic Resource Circulation Act, along with regional market developments in North America, Europe, Asia-Pacific, and Latin America. Quantitative modeling of market sizing, CAGR, and segmentation by material, format, and confectionery type was complemented by qualitative analysis of innovation strategies, partnerships, and consumer trends, including on-the-go consumption, premiumization, and sustainability adoption. This integrated methodology enables USDAnalytics to deliver a comprehensive, forward-looking view of the confectionery packaging market, highlighting opportunities, competitive dynamics, and strategic implications for global stakeholders.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.