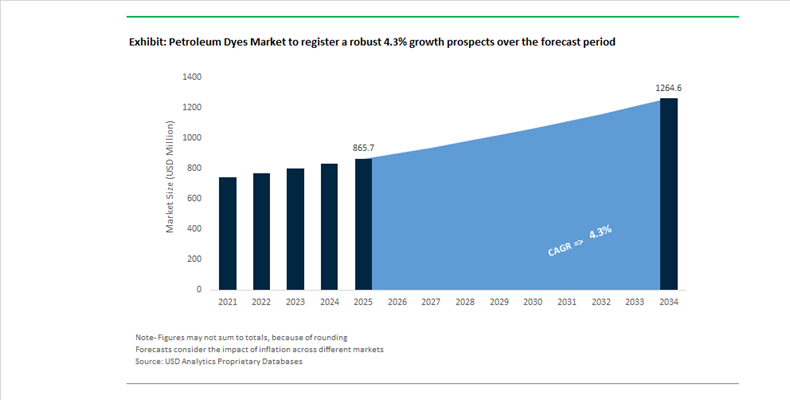

Petroleum Dyes Market Size 2025–2034: $865.7 Million to $1,264.5 Million at 4.3% CAGR Driven by Fuel Marker Modernization and Sustainability Compliance

The global petroleum dyes market is projected to grow from $865.7 million in 2025 to $1,264.5 million by 2034, registering a CAGR of 4.3%. Growth is being shaped by regulatory modernization of fuel marking systems, expansion of lubricant and specialty solvent coloration, and tightening environmental compliance standards across downstream oil and gas value chains. Petroleum dyes, including solvent dyes, fuel markers, and tracer chemicals, are critical for fuel authentication, tax enforcement, brand differentiation, and performance monitoring in refined petroleum products such as diesel, gasoline, aviation fuel, and industrial lubricants.

A structural inflection point in Europe was completed in 2024 with the full transition to the new Euromarker, Accutrace™ Plus, across 28 countries following the European Commission’s earlier mandate. The replacement of Solvent Yellow 124 established a more advanced molecular marker system designed to resist fuel laundering and illegal tax diversion. This regulatory upgrade reshaped procurement specifications for oil marketers and required reformulation of dye packages by leading suppliers. Momentum continued in January 2026 when Norway officially adopted Accutrace™ Plus as its national fuel marker for off-road diesel, reinforcing a broader European enforcement strategy centered on traceability and chemical resilience. In parallel, updated UK fuel marking rebate regulations implemented by HMRC in January 2024 tightened dye concentration and testing thresholds, compelling suppliers to enhance compliance verification protocols for tax-marked fuels.

Industry consolidation and R&D investment are strengthening competitive positioning. In November 2024, John Hogg Technical Solutions completed its acquisition of Avocet Dye and Chemical Company, with integration finalized by late 2025. This transaction expanded John Hogg’s solvent dye portfolio serving lubricants, industrial fuels, and specialty petroleum applications. Earlier in July 2024, the company inaugurated a new R&D laboratory in Manchester focused on next-generation fuel markers and high-purity solvent dyes tailored for aviation fuel and renewable diesel specifications. ISO 14001 certification achieved in late 2024 further enhanced its qualification profile for long-term contracts with global oil majors requiring certified environmental management systems.

Global pigment supply consolidation accelerated in March 2025 when Sudarshan Chemical Industries completed its $500 million acquisition of the Heubach Group, forming the world’s second-largest pigment producer. This consolidation strengthens supply continuity for organic pigments and dyes used in greases, lubricants, and petroleum coatings. In the same month, Innospec Oilfield Services launched the LaZuli™ product line designed for subsea production environments, incorporating specialized dyes and markers engineered to remain stable under extreme pressure and temperature conditions encountered in deepwater oilfields.

Sustainability reporting and digital transparency are influencing dye selection criteria. In February 2026, Sun Chemical upgraded its digital Pigment Finder platform to include Product Carbon Footprint statements, enabling petroleum and lubricant formulators to align dye procurement with corporate ESG reporting mandates. This development reflects growing integration of lifecycle carbon accounting into chemical sourcing decisions. In September 2025, BASF introduced Keropur® AP 225-20 under its gasoline performance additive series to align with emerging U.S. TOP TIER+™ standards, ensuring compatibility with advanced fuel markers for commercial rollout beginning in 2026.

Regulatory changes in adjacent sectors are also reshaping production allocation. In April 2025, the U.S. FDA announced a phased initiative to eliminate several petroleum-based synthetic food dyes. While directed at the food industry, the decision prompted chemical manufacturers to redirect petroleum-dye capacity toward industrial, lubricant, and fuel-marking applications where regulatory pressure is comparatively lower and traceability demand is increasing.

Regulatory, Security, and Energy-Transition Forces Redefining Petroleum Dyes Demand

Regulatory-Driven Adoption of High-Stability Dyes for ULSD and Biofuel Blends

The petroleum dyes market is undergoing a structural upgrade as fuel specifications tighten across conventional, low-sulfur, and renewable fuel systems. The shift toward Ultra-Low Sulfur Diesel and biofuel blending has reduced aromatic content in fuels, fundamentally altering solvent polarity and dye solubility behavior. As a result, fuel marketers and regulators are moving away from legacy powder dyes toward high-purity, liquid-phase dye concentrates that remain stable in modern fuel matrices.

In aviation, the implementation of the ReFuelEU Aviation mandate from January 1, 2025 has created a new compatibility requirement for dyes used in Sustainable Aviation Fuel. Synthetic paraffinic kerosene lacks the solvency characteristics of conventional Jet A-1, making dye precipitation a material risk. This is accelerating the specification of aviation-grade dyes engineered for long-term stability in SPK blends, particularly as SAF volumes scale across EU airports. The need for chemically inert, non-reactive dyes is no longer optional but embedded within fuel certification workflows.

In road transport fuels, ULSD specifications limiting sulfur to 10 ppm in the EU and 15 ppm in the United States have exposed the limitations of older solvent dyes, which can precipitate or migrate in low-polarity environments. Advanced formulations such as Innospec Oil Red B4 AS are increasingly favored because they maintain full solubility and color integrity, preventing filter clogging and downstream maintenance issues. This shift is reinforcing a premium segment within petroleum dyes tied directly to fuel system reliability and compliance.

Emerging markets are reinforcing this trend through stricter fiscal enforcement. In November 2025, India strengthened kerosene marking protocols to prevent diversion into the transport fuel pool. These programs rely on high-intensity dyes capable of delivering forensic-level visibility at extremely low treat rates, ensuring tax-exempt fuels remain unmistakably identifiable throughout the distribution chain. As fuel taxation gaps narrow, dye performance is becoming a direct enabler of government revenue protection.

Integration of Invisible Covert Markers for Advanced Anti-Adulteration

Visible coloration alone is no longer sufficient to counter increasingly sophisticated fuel adulteration networks. Governments and fuel suppliers are now deploying layered security architectures that combine traditional petroleum dyes with invisible molecular markers embedded at trace concentrations. These covert markers cannot be removed through laundering or chemical treatment, fundamentally altering the economics of fuel fraud.

National fuel integrity programs provide clear evidence of this shift. As highlighted by Authentix and Serbia’s National Alliance for Local Economic Development, the deployment of CHON-based molecular markers has generated more than €1.4 billion in incremental tax revenue by eliminating large-scale fuel dilution. These markers combust cleanly, leave no engine residue, and can be detected at parts-per-billion levels, making them ideal complements to visible petroleum dyes.

Operationally, the market is moving toward real-time authentication. The rollout of portable analyzers such as the Authentix LSX series in 2025 has enabled field verification of fuel integrity in under two minutes. This transition from laboratory-based testing to point-of-sale validation is reshaping enforcement models, allowing authorities and brand owners to intervene directly at terminals and retail stations.

The same traceability logic is now extending into biofuels. In August 2024, the Global Centre for Maritime Decarbonisation successfully demonstrated the use of organic MSX tracers to validate B30 biofuel blends across maritime supply chains. These trials confirmed that covert markers are essential for verifying renewable content, supporting sustainability claims, and enabling participation in carbon-credit mechanisms tied to proof-of-origin requirements.

Dyes and Markers for Hydrogen and Ammonia Energy Systems

As hydrogen transitions from an industrial input to a traded energy vector, a new class of marking and safety identification requirements is emerging. While the industry is gradually shifting from color labels toward quantified carbon intensity metrics, interim marking solutions remain critical for shared infrastructure and transitional fuels.

Germany’s hydrogen standardization roadmap published by DIN and VDE in November 2025 identifies a clear need for identification systems in pipelines and storage networks. This has opened early-stage demand for dyes and odorants compatible with Liquid Organic Hydrogen Carriers, enabling differentiation between green and grey hydrogen in repurposed gas infrastructure.

Ammonia, increasingly positioned as a hydrogen carrier for maritime transport, presents a parallel opportunity. The high alkalinity and corrosive nature of ammonia require chemically robust dyes that remain stable without interfering with engine performance. Chemical majors are actively prototyping ammonia-compatible markers to prevent cross-contamination in dual-fuel marine engines and port storage facilities.

Public investment is accelerating this opportunity set. With the U.S. Department of Energy allocating billions of dollars to hydrogen hubs during 2024–2025, the need for detectable leak markers in large-scale storage caverns is emerging as a niche but strategically important market. Unlike natural gas systems dominated by mercaptans, hydrogen infrastructure will require new detection chemistries where petroleum dye expertise can be repurposed.

High-Value Lubricant, Marine Fuel, and Equipment Protection Applications

Beyond fuels, petroleum dyes are gaining importance in specialty lubricants and marine energy systems, where differentiation, compliance, and asset protection are critical. The expansion of Sulphur Oxide Emission Control Areas under IMO regulations has intensified the need to clearly distinguish compliant marine fuels. Following the designation of the Mediterranean Sea as a SOx-ECA effective May 1, 2025, suppliers are increasingly using dyes to differentiate Ultra-Low Sulfur Fuel Oil from non-compliant grades, reducing enforcement risk and commercial disputes at bunkering points.

In industrial and automotive systems, dye usage is increasingly tied to preventive maintenance. The rapid adoption of R-1234yf refrigerants in electric vehicle HVAC systems has driven demand for ultra-sensitive fluorescent dyes capable of detecting leaks as small as 0.65 ounces per year. These dyes play a critical role in protecting battery thermal management systems, where refrigerant loss can trigger cascading failures and high warranty costs.

Finally, brand protection is emerging as a quiet but lucrative application. High-performance lubricant producers are using proprietary color signatures to deter counterfeiting in industrial turbines, marine engines, and aerospace applications. Distinctive shades such as Oil Purple RS85 act as visual authentication tools, ensuring that premium synthetic oils are not substituted with lower-grade alternatives in high-stress equipment. As machinery complexity increases, petroleum dyes are evolving from simple identifiers into strategic tools for compliance, security, and value protection across the energy ecosystem.

Petroleum Dyes Market Share and Segmentation Insights

Liquid Petroleum Dyes Lead Market Adoption in Automated Fuel Blending and Pipeline Injection Systems

Liquid dyes accounted for 58.60% of the Petroleum Dyes Market by type in 2025, reflecting their widespread use in fuel distribution infrastructure and blending operations. Liquid petroleum dyes provide operational advantages in refineries, terminals, and pipeline systems because they can be precisely injected into hydrocarbon streams during loading or transfer operations. Their rapid solubility in gasoline, diesel, and heating fuels allows consistent coloration without the handling challenges associated with powder dyes. In 2025, compatibility with automated fuel dye dosing systems is driving product development, with liquid dye formulations designed for precise metering in automated blending equipment that ensures uniform color strength and regulatory compliance across fuel distribution networks.

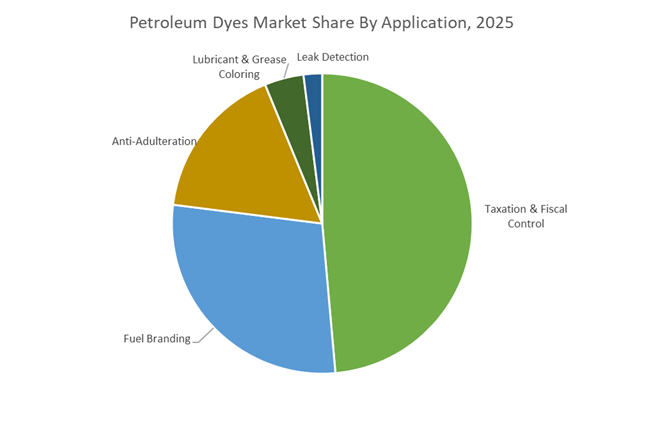

Taxation and Fiscal Control Programs Drive Petroleum Dye Demand in Fuel Identification Systems

Taxation and fiscal control represented 48.60% of the Petroleum Dyes Market by application in 2025, reflecting the critical role dyes play in government fuel identification programs. Many countries require color coding of fuels to distinguish tax classes such as off-road diesel, heating oil, aviation fuel, and taxed on-road transportation fuels. Petroleum dyes allow regulators to visually identify fuel misuse and support enforcement of fuel tax regulations. In 2025, integration of molecular marker technologies with visible petroleum dyes is enhancing enforcement capabilities, enabling regulators to combine visual identification with laboratory detection methods that verify fuel authenticity and detect adulteration or tax evasion within fuel supply chains.

Petroleum Dyes Market Competitive Landscape

The Petroleum Dyes Market is consolidating around high-security fuel markers, anti-adulteration technologies, and bio-based dye innovation. Regulatory mandates across APAC, EMEA, and North America are driving demand for traceable, low-toxicity fuel colorants, with leading players focusing on digital detection, sustainable chemistries, and global supply chain control.

BASF strengthens fuel marker dominance through Verbund integration and digital detection technologies

BASF SE maintains leadership in the petroleum dyes market through its integrated Verbund model and high-purity azo dye portfolio. The company reported €6.6 billion EBITDA in 2025, with stable performance in its Industrial Solutions segment. Its strategic divestiture of decorative paints enables a sharper focus on performance chemicals and fuel additives. BASF’s Sudan® dye range remains a benchmark for tax-rebated fuel marking, now enhanced with digital markers detectable via portable field devices. The company is also advancing premium fuel branding using interference pigments and liquid-metal effects. This combination of scale, innovation, and regulatory alignment reinforces BASF’s global dominance.

Innospec drives high-margin growth with invisible fuel markers and sustainable aviation dye solutions

Innospec Inc. is a key innovator in fuel specialty chemicals, delivering strong financial performance with a 12% increase in operating income to $144.8 million in 2025. The company is accelerating commercialization of eco-certified dyes for Sustainable Aviation Fuel (SAF), designed for high detectability at low treat rates. Its growing portfolio of invisible fuel markers supports national anti-adulteration programs. Innospec’s strong net cash position of $292.5 million enables continued investment in next-generation technologies. The company differentiates through integrated dosing systems that optimize refinery operations. This focus on performance and sustainability strengthens its competitive positioning.

Sudarshan emerges as global pigment powerhouse following Heubach acquisition and portfolio integration

Sudarshan Chemical Industries Ltd. has transformed into the second-largest global pigment player following its acquisition of the Heubach Group. This integration adds 19 manufacturing sites and significantly enhances its global supply capabilities. The company is establishing a Global Capability Center in 2026 to accelerate R&D in solvent dyes and dispersions for petroleum applications. Its expanded portfolio covers oil-soluble dyes for fuels, lubricants, and greases, combining cost efficiency with advanced European technology. The “One Sudarshan” strategy focuses on unlocking synergies across global operations. This scale and integration position Sudarshan as a major competitive force.

John Hogg advances anti-adulteration leadership with Accutrace deployment and global regulatory footprint

John Hogg Technical Solutions is a niche leader specializing in fuel marking and regulatory compliance across more than 70 countries. Its Accutrace™ Plus marker was adopted as Norway’s national standard in 2026, highlighting its strength in anti-laundering technologies. The acquisition of Avocet Dye expanded its solvent dye capabilities and technical reach. The company’s Dyeguard® and Sudan® brands are widely used to combat fuel fraud and protect tax revenues. Sustainability credentials, including ISO 14001 certification and EcoVadis recognition, enhance its market credibility. This regulatory expertise and focused innovation reinforce its niche leadership.

Sun Chemical expands sustainable pigment capacity and low-toxicity dye systems for global fuel applications

Sun Chemical, part of DIC Corporation, is leveraging its global pigment infrastructure to advance sustainable petroleum dye solutions. The company invested $10 million in 2026 to expand high-performance pigment production in the U.S., following capacity growth in Germany. It is leading the development of SVHC-free colorants and low-VOC dye carriers aligned with stringent EU regulations. Sun Chemical is also exploring natural colorant integration and alternative binder systems for safer industrial applications. Its PantoneLIVE™ platform enables precise color standardization for fuel branding across regions. This combination of sustainability, scale, and customization strengthens its competitive position.

United States – Regulatory Displacement and Fiscal Dye Intensification

The U.S. petroleum dyes industry is undergoing a structural reset driven by regulatory intervention and fiscal enforcement priorities. In April 2025, the FDA announced a definitive plan to phase out petroleum-based synthetic dyes from the food supply by the end of 2026. While this mandate is not directly targeted at fuels, it has materially redirected R&D capital away from food and cosmetic colorants toward industrial-grade petroleum dyes and molecular markers. As a result, U.S. dye manufacturers are accelerating innovation in high-purity, non-migratory dyes specifically designed for fuels, lubricants, and specialty hydrocarbons where clean-label constraints do not apply but regulatory scrutiny is intensifying.

Fiscal policy changes are reinforcing demand for higher-strength fuel markers. From January 1, 2026, gas tax increases in states such as New Jersey and Florida have widened the tax differential between on-road and off-road fuels. This has triggered a measurable increase in demand for higher-concentration Red 26 and related solvent dyes used for tax enforcement and fuel laundering prevention. Concurrently, the exit of 3M from PFAS-related manufacturing by the end of 2025 has constrained the availability of certain fluorinated extreme-environment fuel tracers. This supply gap is being absorbed by players such as Innospec and Chemours, both of which are expanding non-PFAS and molecular-marker alternatives. In parallel, John Hogg has expanded deployment of its Accutrace™ Plus non-extractable molecular markers across North America, addressing persistent fuel laundering risks that conventional dyes cannot mitigate. Aviation fuel deregulation in Florida from January 2026 has further shifted marking requirements away from fiscal dyes toward purity-verification systems at regional storage terminals.

United Kingdom – Compliance-Driven Product Proliferation and Detection Innovation

The UK petroleum dyes market is being reshaped by post-Brexit regulatory finality and enforcement modernization. Effective January 1, 2026, all petroleum additives and chemical products sold in Great Britain must carry the UKCA mark, ending the long-standing labeling easement for EEA imports. This has compelled suppliers to revalidate technical documentation and reformulate labeling practices, disproportionately impacting smaller importers while favoring established domestic and multinational dye manufacturers with strong compliance infrastructure.

Strategically, UK-based John Hogg announced in late 2025 the development of more than 20 new products designed to align with evolving EU-wide fuel marking legislation. This reflects the UK’s role as a regulatory and technical bridge between EU and non-EU fuel markets. At the same time, detection technology is becoming a competitive differentiator. UK firms, led by Innospec, are pioneering near-infrared detection systems. The 2025 OIM 1020 series specifications demonstrate field-testing markers that require no extractant chemicals, materially reducing the environmental footprint and operational cost of roadside fuel inspections while improving enforcement reliability.

India – Refining Expansion and Export-Led Scale-Up

India’s petroleum dyes industry is entering a scale-driven expansion phase anchored in refining capacity growth and export momentum. The Rajasthan Refinery Limited project, scheduled for commercial operation by March 31, 2026, represents one of the most consequential structural developments. With an investment exceeding ₹52,877 crore, the refinery integrates dedicated fuel blending and additive injection units, positioning it as a major domestic consumption and testing hub for petroleum dyes used in gasoline, diesel, and specialty fuels.

Export performance is reinforcing India’s role as a global supplier. During April–July 2025, India’s dye and dye intermediate exports reached USD 824.77 million, with petroleum-specific dyes recording accelerated shipments to the Middle East and Africa. This momentum has been amplified by strategic consolidation. The March 2025 acquisition of Germany’s Heubach Group by Sudarshan Chemical created a globally integrated platform spanning 19 manufacturing sites, strengthening India’s access to advanced formulations and regulated markets. On the policy front, enhanced Quality Control Orders implemented in February 2025 now require BIS-aligned certification for imported petroleum dyes, shielding domestic producers from substandard imports and tightening compliance expectations across the supply chain.

China – Efficiency Mandates and Environmental Surveillance Pressure

China’s petroleum dyes market is being reshaped by fuel efficiency regulation and real-time environmental oversight. From January 1, 2026, the enforcement of GB 27999-2025 fuel efficiency standards is increasing formulation complexity for gasoline and diesel used in high-efficiency engines. These requirements demand petroleum dyes with superior thermal stability and solubility to ensure performance consistency under higher combustion temperatures and tighter emission tolerances.

Environmental compliance is exerting parallel pressure. China’s new Regulation on Ecological Environment Monitoring, also effective January 2026, mandates continuous tracking of chemical pollutants, accelerating the transition toward low-VOC solvent-borne dyes and improved waste management practices. Additionally, export controls introduced in December 2025 on synthetic graphite and related chemical goods are indirectly constraining access to certain raw materials used in specialty black fuel markers. As a result, Chinese dye manufacturers are recalibrating sourcing strategies and investing in alternative chemistries to sustain export competitiveness while meeting stricter domestic compliance thresholds.

Comparative Snapshot – Petroleum Dyes Industry by Country

Petroleum Dyes Market County Level Snapshot

|

Country

|

Core Driver

|

Strategic Focus

|

Market Character

|

|

United States

|

Tax enforcement and regulation

|

High-concentration dyes, molecular markers

|

Enforcement-driven, innovation-led

|

|

United Kingdom

|

Post-Brexit compliance

|

Product proliferation, NIR detection

|

Regulation-centric, technology-enabled

|

|

India

|

Refining and exports

|

Scale-up, global acquisitions

|

Capacity-led, export-oriented

|

|

China

|

Efficiency and monitoring mandates

|

Heat-stable, low-VOC dyes

|

Regulation-intensive, reformulation-driven

|

Petroleum Dyes Market Report Scope

Petroleum Dyes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$865.7 Million

|

|

Market Size (2034)

|

$1264.5 Million

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Type (Liquid Dyes, Powder Dyes, Molecular Markers), By Dye Color (Red Dyes, Blue & Green Dyes, Yellow & Orange Dyes), By Application (Fuel Branding, Taxation & Fiscal Control, Anti-Adulteration, Leak Detection, Lubricant & Grease Coloring)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Innospec Inc., John Hogg Technical Solutions, BASF SE, Sudarshan Chemical Industries Limited, Dow Inc., Chemours Company, Authentix Inc., SGS SA, Standard Colors Inc., Sun Chemical Corporation, Orco, A. S. Paterson Company, United Color Manufacturing Inc., Hubei Hiteck Chemical Co. Ltd., Kiri Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Petroleum Dyes Market Segmentation

By Type

- Liquid Dyes

- Powder Dyes

- Molecular Markers

By Dye Color

- Red Dyes

- Blue & Green Dyes

- Yellow & Orange Dyes

By Application

- Fuel Branding

- Taxation & Fiscal Control

- Anti-Adulteration

- Leak Detection

- Lubricant & Grease Coloring

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Petroleum Dyes Industry

- Innospec Inc.

- John Hogg Technical Solutions

- BASF SE

- Sudarshan Chemical Industries Limited

- Dow Inc.

- Chemours Company

- Authentix Inc.

- SGS SA

- Standard Colors Inc.

- Sun Chemical Corporation

- Orco

- A. S. Paterson Company

- United Color Manufacturing Inc.

- Hubei Hiteck Chemical Co. Ltd.

- Kiri Industries Limited

*- List not Exhaustive