Plantable Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Plantable Packaging Market Set to Grow Rapidly as Eco-Friendly Alternatives Replace Traditional Plastics

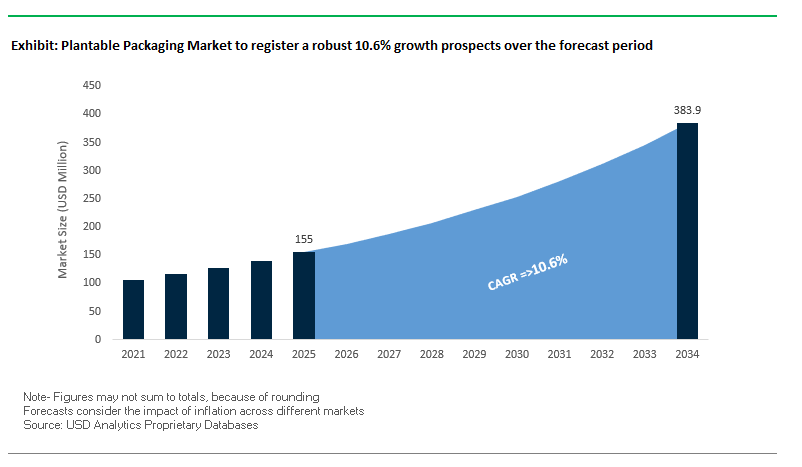

The Global Plantable Packaging Market is projected to expand from $155 million in 2025 to $383.8 million by 2034, reflecting a CAGR of 10.6%. Plantable packaging, made from biodegradable materials embedded with seeds, offers a sustainable solution to plastic waste while simultaneously creating environmental value by growing new plants.

Key Insights for packaging buyers and industry professionals:

- A Sustainable Solution to Plastic Pollution: Plantable packaging directly addresses global plastic waste by biodegrading naturally and contributing to a circular economy.

- Innovation in Materials Accelerates Market Growth: Emerging materials such as seaweed, mushroom mycelium, and bagasse are complementing traditional paper and cellulose, providing faster biodegradability and superior barrier properties.

- Consumer Demand Drives Adoption: Over 90% of consumers prefer brands offering sustainable packaging, with younger demographics willing to pay a premium for eco-conscious products.

- Expanding Industry Applications: Initially used in stationery, plantable packaging is now gaining traction in food and beverage, cosmetics, and industrial products to strengthen brand differentiation and sustainability commitments.

- Regulatory and Brand Alignment: Companies adopting plantable packaging are increasingly aligning with global sustainability goals and eco-certification standards, reinforcing market credibility and consumer trust.

Market Analysis: Plantable Packaging Industry Experiences Strategic Expansion and Breakthrough Innovations

The plantable packaging market has seen multiple strategic developments emphasizing sustainability, material innovation, and global market positioning. In September 2025, Paptic Ltd. received the ScanStar Award for its hygiene packaging innovation and announced a move into the hygiene and feminine care sector with a wood fiber-based plastic alternative. In August 2025, Mondi initiated operations of a €400 million paper machine at Štětí, expanding production capacity for high-barrier, sustainable paper solutions.

Corporate consolidations and global market entries are shaping the industry landscape. In July 2025, Smurfit Kappa and WestRock merged as Smurfit WestRock, debuting on the New York and London Stock Exchanges and establishing a stronger position in paper-based packaging solutions. That same month, Fortis X launched Africa's first biodegradable sugarcane-based packaging in Cape Town, offering compostable alternatives suitable for emerging markets.

Technological and product innovations are also driving market adoption. Graphic Packaging International, in June 2025, introduced the PaperSeal® Pressed MAP Tray, reducing plastic usage by up to 85% in Modified Atmosphere Packaging (MAP) applications. Earlier, in April 2025, Nfinite Nanotechnology partnered with Amcor to validate nanocoatings that enhance recyclability and oxygen barrier performance for compostable packaging. Startups like La Foundary (January 2025) have developed mushroom mycelium packaging, transforming agricultural waste into biodegradable solutions.

Emerging Trends and Growth Opportunities in the Plantable Packaging Market

Strategic Adoption by Premium and Mission-Driven Brands for Storytelling

The plantable packaging market is gaining traction as premium brands and eco-conscious companies increasingly adopt it as a storytelling tool to differentiate themselves and reinforce their sustainability missions. A notable case study comes from Pangea Organics, which pioneered the concept with its skincare line marketed under the slogan “Coming from the earth and going back to it.” By embedding organic herb seeds directly into its packaging, the company allowed consumers to plant their used boxes, transforming waste into living plants. This not only reinforced Pangea’s zero-waste ethos but also created a unique consumer experience that resonated with environmentally conscious buyers. Luxury apparel brands are also embracing this packaging trend. Pangaia, for example, leverages plantable hangtags embedded with wildflower seeds, giving customers a tangible, interactive experience that ties into its eco-friendly brand image. These strategic adoptions demonstrate how plantable packaging functions as more than just a material innovation—it has become an emotional and symbolic branding tool, enabling companies to build consumer loyalty by connecting sustainability with product experience.

Material Science Innovation Focusing on Seed Viability and Printability

Material science breakthroughs are central to scaling plantable packaging solutions, as manufacturers must balance functionality during the supply chain with seed viability post-use. Innovations in biodegradable binders and paper blends are addressing these challenges. Companies are experimenting with recycled pulp, cotton rags, and agricultural waste fibers as raw material inputs, ensuring packaging remains durable during printing, shipping, and handling, yet still decomposes easily once planted. Low-heat drying techniques are being refined to protect delicate seeds from damage during production. Research in academic journals such as ResearchGate emphasizes the importance of balancing durability with regeneration—ensuring materials remain moisture-resistant for transit but break down naturally to enrich the soil. Such developments not only enhance performance but also increase the biodiversity benefits of plantable packaging. By embedding seeds in functional, printable substrates, innovators are ensuring that packaging can both carry a brand’s identity and serve as a regenerative product that actively contributes to environmental restoration.

Development for the Horticulture and Agri-Business Supply Chain

The horticulture and agriculture sectors represent a high-potential application area for plantable packaging, with opportunities to replace traditional plastics in propagation and seed distribution. Plantable pots, trays, and seed pods are being designed to eliminate the need for plastic transplant containers, enabling growers to place seedlings directly into the soil, reducing both waste and transplant shock. For commercial growers, this innovation offers operational efficiency, while home gardeners benefit from simplified planting processes. Beyond functionality, seed packaging is evolving to include traceability features. Companies are embedding QR codes into plantable seed packets and labels, giving farmers digital access to sowing instructions, seed origin, and viability data. This dual functionality—combining sustainable packaging with smart agriculture technologies—creates transparency, enhances crop management, and supports the broader digitalization of the agriculture supply chain. By addressing both sustainability and productivity needs, plantable packaging is positioned as a valuable tool for agri-business growth.

Integration with Corporate “Re-Greening” and CSR Initiatives

Plantable packaging is also emerging as a symbolic and tangible tool for corporate social responsibility (CSR) strategies, enabling companies to align internal culture and brand communication with sustainability goals. Organizations are increasingly using plantable paper for invitations, promotional materials, and employee engagement initiatives. For instance, companies distributing plantable seed cards or event materials empower employees and customers to directly contribute to local biodiversity efforts by planting packaging waste. A case study from Terra Tag demonstrated how plantable badges and lanyards used at an event saved approximately 60kg of CO₂ emissions, while simultaneously transforming disposable event materials into a long-term environmental legacy. Such initiatives create what companies call a “living legacy,” reinforcing sustainability credentials and leaving measurable ecological impact. For businesses, this integration of plantable packaging into CSR campaigns goes beyond compliance; it strengthens brand authenticity, engages employees and customers alike, and positions the company as a leader in environmental stewardship.

Competitive Landscape: Top Players Are Shaping the Plantable Packaging Market Through Sustainability and Material Innovation

The global plantable packaging industry is led by companies leveraging innovative materials, strategic mergers, and sustainable solutions to meet growing consumer and regulatory demand.

Mondi Group: Pioneering High-Barrier Paper Solutions as a Stepping Stone to Plantable Packaging

Mondi is a leader in paper and flexible packaging, with its FunctionalBarrier Paper Ultimate providing ultra-high barrier properties. In August 2025, Mondi ramped up production of this paper-based solution as an alternative to unrecyclable plastics. The company emphasizes monomaterial designs, fiber-based innovations, and sustainability-driven growth, aligning closely with plantable packaging principles.

Smurfit WestRock: Forming a Global Leader Through Strategic Merger and Sustainable Paper-Based Solutions

Formed by the merger of Smurfit Kappa and WestRock in July 2025, Smurfit WestRock provides a wide range of corrugated and containerboard products. The merger strengthened the company’s global footprint and next-generation packaging capabilities, with a strong focus on recycled and renewable materials to reduce environmental impact.

Graphic Packaging International: Reducing Plastic Waste with Fiber-Based Packaging Innovations

Graphic Packaging International focuses on fiber-based consumer packaging solutions. In June 2025, it launched the PaperSeal® Pressed MAP Tray, reducing plastic use by 85%. Its Better by 2030 initiative emphasizes sustainability, recyclability, and plastic reduction, while products like Boardio™ and KeelClip™ highlight innovative approaches to eco-friendly packaging.

Notpla: Driving Plastic-Free Packaging Through Seaweed-Based Materials

Notpla produces edible and biodegradable packaging from seaweed, designed to replace single-use plastics in food service. Its Notpla Coated Board offers grease-proof, water-resistant packaging, and its Oohos edible bubbles demonstrate innovative solutions for liquids. The company focuses on creating a plastic-free circular economy, directly supporting plantable packaging principles.

Paptic Ltd.: Expanding Sustainable Packaging Horizons with Wood Fiber Innovations

Paptic produces wood fiber-based, recyclable, and reusable packaging materials. In September 2025, it won the ScanStar Award for hygiene packaging innovation and announced expansion into the feminine care sector. With a €27.5 million financing round, Paptic is scaling production and providing eco-friendly alternatives to plastics across multiple applications, including bags, mailers, and flexible pouches.

Plantable Packaging Market Share Insights, 2025-2034

Flower Seeds Dominate Plantable Packaging Market Share by Embedded Seed Type

By embedded seed type, flower seeds account for the largest share of the plantable packaging market in 2025, driven by their widespread appeal, visual impact, and ability to enhance consumer engagement with packaging sustainability. Flower seed–embedded cartons, sleeves, and tags are popular across cosmetics, food, and premium gifting industries, where brand storytelling and eco-friendly messaging are key differentiators. Vegetable seeds represent the next significant segment, particularly favored by food and beverage brands that align with farm-to-table and edible gardening trends, offering packaging that directly connects with healthy lifestyles. Herb seeds are gaining traction among personal care, tea, and specialty food brands, appealing to consumers seeking functional, small-space gardening options. Tree seeds, though smaller in volume, carry strong symbolic and CSR value, often used in limited-edition campaigns, luxury products, or corporate gifting where long-term environmental impact is emphasized. The leadership of flower seeds demonstrates how aesthetics and brand marketing converge with sustainability, while the growth of vegetable and herb seeds reflects consumer demand for utility-driven, eco-conscious packaging.

Boxes and Cartons Lead Plantable Packaging Market Share by Packaging Type

By packaging type, boxes and cartons dominate the plantable packaging market in 2025, as they provide ample surface area for seed embedding, branding, and storytelling while maintaining structural durability. Bags and pouches follow as a high-growth segment, offering lightweight and versatile options for food, apparel, and accessories, especially in e-commerce and retail where sustainable alternatives to plastic are in demand. Wrappers and sleeves also capture a notable share, commonly adopted in confectionery, cosmetics, and small consumer goods where visual branding and eco-differentiation drive impulse purchases. Labels and tags serve a unique role as add-on packaging elements, providing sustainability credentials and marketing value without replacing the primary package, making them a popular choice for apparel, beverages, and luxury goods. Molded pulp and inserts represent a growing segment, combining protective functionality with seed-embedding for electronics, fragile items, and premium gifting. The dominance of boxes and cartons emphasizes the market’s reliance on structural, brand-forward solutions, while the rise of flexible and modular formats underscores the broader consumer shift toward sustainable, experiential packaging.

United States Plantable Packaging Market Strengthened by USDA Regulations and E-Commerce Growth

The United States plantable packaging market is being shaped by USDA and Federal Seed Act (FSA) regulations, which enforce strict truth-in-labeling requirements to ensure the seeds embedded in packaging are authentic, non-invasive, and viable for germination. This is crucial for consumer trust and compliance in both domestic and international shipments. The market is witnessing significant innovation, with companies such as Mango Materials developing PHA biopolymers from methane and Cruz Foam creating compostable foams from seafood waste, offering scalable alternatives to single-use plastics.

The surge in e-commerce adoption is accelerating the use of plantable packaging as a customer engagement tool, with brands leveraging interactive unboxing experiences that reinforce sustainability credentials. Retail giants and food service leaders, including McDonald’s, are phasing out plastic packaging in favor of fiber-based, biodegradable, and plant-embedded alternatives. Certification and transparency are key trends, with retailers demanding PFAS-free, seed-certified, and clearly labeled packaging to strengthen consumer confidence and meet global sustainability targets.

Europe Plantable Packaging Market Driven by PPWR and Seaweed-Based Innovations

The Europe plantable packaging market is guided by the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025 and will set minimum standards for recyclability, reuse, and compostability by 2030. European companies are focusing on home-compostable and industrially compostable solutions that comply with strict food safety standards while meeting the EU’s circular economy objectives. Notable startups such as Notpla and FlexSea are pioneering seaweed-based materials that naturally decompose, offering sustainable alternatives to traditional plastics.

While the PPWR is a strong regulatory driver, debates persist over its exclusive focus on reusability, with organizations like the Alliance for Sustainable Packaging calling for a balance between reusable and compostable systems. The European Commission has announced upcoming implementing acts to make sustainable packaging mandatory in public procurement. Demand is surging for food-contact safe, PFAS-free, and plantable packaging solutions, positioning Europe as one of the most advanced regions for eco-innovations in packaging.

China Plantable Packaging Market Supported by June 2025 Regulations and Green Product Certification

The China plantable packaging market is undergoing rapid transformation due to the June 2025 packaging regulation targeting the reduction of excessive wrapping and promoting the use of recycled and reusable systems, especially in the booming e-commerce sector. With billions of express parcels delivered annually, this regulation addresses environmental pollution and packaging waste reduction. Local companies such as Jingxing Packaging Materials Co. are setting examples by establishing closed-loop recycling systems that utilize leftover scraps to manufacture new packaging.

China’s positive list system for food-contact materials and new adhesive standards implemented in February 2025 are shaping the development of plantable food-grade packaging. Over 100 companies are pursuing “green product” certification, reflecting growing consumer demand for sustainable and safe packaging. Innovations in high-quality biodegradable films and plantable paper materials highlight China’s commitment to both circular economy goals and next-generation eco-friendly packaging technologies.

India Plantable Packaging Market Accelerated by EPR Framework and Startup Innovations

The India plantable packaging market is advancing through the draft packaging waste management rules of February 2025, which introduced an Extended Producer Responsibility (EPR) framework for paper, glass, and metal, holding producers accountable for their packaging lifecycle. This has spurred demand for biodegradable and plantable alternatives across sectors. Startups are at the forefront, with Dharaksha Ecosolutions securing funding in September 2024 to scale its agricultural waste-based packaging solutions, showcasing how domestic innovation is meeting sustainability goals.

The Food Safety and Standards Authority of India (FSSAI) is actively consulting on sustainable packaging standards for food businesses, creating opportunities for plantable and biodegradable packaging. Indian companies are increasingly adopting plantable paper for promotional materials like business cards and calendars, tapping into eco-conscious consumer segments. Coupled with government incentives and the Make in India initiative, the country is positioning itself as a global hub for sustainable and plantable packaging solutions while reducing plastic dependency.

United Kingdom Plantable Packaging Market Reinforced by EPR and Seaweed-Based Materials

The United Kingdom plantable packaging market is being shaped by the Extended Producer Responsibility (EPR) framework, which transfers waste management costs to producers and incentivizes recyclable, compostable, and plantable packaging formats. The country has seen rising investment in biodegradable innovations, with startups like FlexSea commercializing seaweed-derived plastics that align with both sustainability regulations and consumer expectations.

Growing consumer demand for low-impact packaging is pushing brands to adopt plantable and compostable options across retail, food service, and e-commerce. At the same time, companies are researching solutions to recycle complex multi-material packaging, ensuring compliance with evolving national sustainability standards. This regulatory and consumer-driven momentum is positioning the UK as a leader in next-generation plantable and circular packaging markets.

Japan Plantable Packaging Market Focused on E-Commerce and Positive List Regulations

The Japan plantable packaging market is guided by its positive list system for food-contact materials, which came into effect in 2025, reshaping how companies develop eco-friendly packaging. Japanese manufacturers are prioritizing high-performance biodegradable and recyclable materials that comply with the country’s stringent food safety standards.

Government-backed initiatives for waste reduction and recycling are creating opportunities for circular economy packaging solutions, particularly in plantable formats. With the rapid expansion of e-commerce and home delivery services, there is a rising demand for robust yet sustainable packaging options that can be safely composted or planted. Japan’s unique focus on safe, smart, and sustainable packaging is making it an important market for plantable packaging technologies tailored to consumer convenience and environmental stewardship.

Plantable Packaging Market Report Scope

Plantable Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$155 Million

|

|

Market Size (2034)

|

$383.8 Million

|

|

Market Growth Rate

|

10.6%

|

|

Segments

|

By Material (Paper-Based, Bio-based Polymers, Other Plant-based Materials), By Embedded Seed Type (Flower Seeds, Vegetable Seeds, Herb Seeds, Tree Seeds), By Packaging Type (Boxes & Cartons, Bags & Pouches, Wrappers & Sleeves, Labels & Tags, Molded Pulp, Inserts), By End-Use Industry (Cosmetics & Personal Care, Food & Beverage, E-commerce & Retail, Apparel & Fashion, Greeting Cards & Stationery, Home & Garden)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Botanical PaperWorks Inc., Living Ink, Pangea Organics, Inc., Plantable, Seed Paper Promotions, Gmund Paper GmbH, Shepherd's Bookbinders, The Gifting Tree, Pukka Herbs Ltd., Two Sides Ltd., Eco-Plastics Ltd., New Leaf Paper, Greenvelope, Inc., Wildlense Eco Foundation, Ukhi

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plantable Packaging Market Segmentation

By Material

- Paper-Based

- Bio-based Polymers

- Other Plant-based Materials

By Embedded Seed Type

- Flower Seeds

- Vegetable Seeds

- Herb Seeds

- Tree Seeds

By Packaging Type

- Boxes & Cartons

- Bags & Pouches

- Wrappers & Sleeves

- Labels & Tags

- Molded Pulp

- Inserts

By End-Use Industry

- Cosmetics & Personal Care

- Food & Beverage

- E-commerce & Retail

- Apparel & Fashion

- Greeting Cards & Stationery

- Home & Garden

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plantable Packaging Market

- Botanical PaperWorks Inc.

- Living Ink

- Pangea Organics, Inc.

- Plantable

- Seed Paper Promotions

- Gmund Paper GmbH

- Shepherd's Bookbinders

- The Gifting Tree

- Pukka Herbs Ltd.

- Two Sides Ltd.

- Eco-Plastics Ltd.

- New Leaf Paper

- Greenvelope, Inc.

- Wildlense Eco Foundation

- Ukhi

* List Not Exhaustive

Methodology

USDAnalytics employs a robust and comprehensive methodology to deliver accurate and actionable insights into the Plantable Packaging Market. Our approach integrates extensive primary research through interviews with key stakeholders including packaging manufacturers, material innovators, sustainability consultants, and leading end-use companies across cosmetics, food & beverage, e-commerce, and apparel sectors. This is complemented by secondary research from industry reports, regulatory filings, patent databases, academic studies, and verified company disclosures. Market sizing and CAGR estimations are calculated using both top-down and bottom-up approaches, analyzing segmentation by material type, embedded seed type, packaging format, and end-use industry. We examine technological trends such as bio-based polymer innovations, seaweed and mushroom-based materials, seed viability and printability optimization, and smart packaging solutions for horticulture and CSR applications. Regional analyses consider regulatory frameworks including the EU Packaging and Packaging Waste Regulation (PPWR), India’s EPR framework, USDA/FSA regulations in the U.S., China’s green product certifications, Japan’s positive list system, and the UK’s EPR initiatives. Competitive benchmarking evaluates strategic mergers, material innovations, and sustainability initiatives by leading players such as Mondi Group, Smurfit WestRock, Graphic Packaging International, Notpla, and Paptic Ltd., providing industry professionals with a holistic view of market dynamics, growth opportunities, and evolving eco-conscious packaging trends.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.