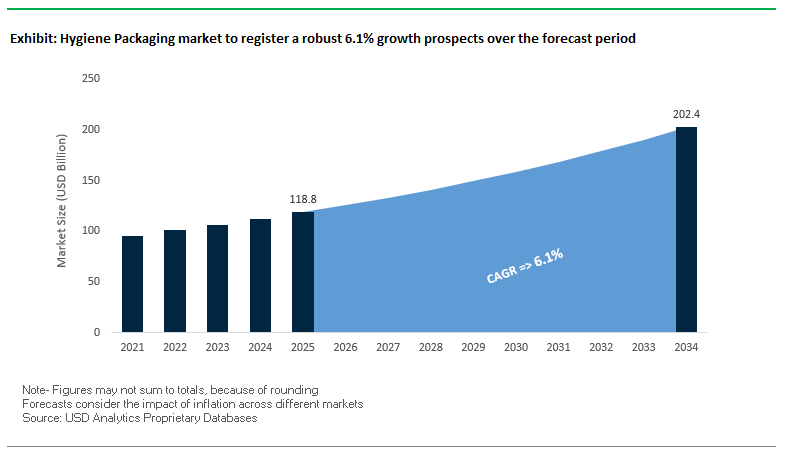

Market Overview: Hygiene Packaging Market to Surpass $202.4 Billion by 2034 with a 6.1% CAGR Driven by Sustainability and E-commerce Growth

The global hygiene packaging market is valued at $118.8 billion in 2025 and projected to reach $202.4 billion by 2034, growing at a robust CAGR of 6.1%. Packaging for hygiene products plays a critical role in contamination prevention, consumer safety, and regulatory compliance, while also adapting to shifting sustainability mandates and online retail growth. Industry buyers are increasingly prioritizing tamper-evident, recyclable, and e-commerce-ready packaging formats, reflecting a convergence of consumer health, sustainability, and operational efficiency.

Key Insights for Industry Stakeholders

- Sustainability leadership: Companies like Procter & Gamble (80% recyclable/reusable packaging) and Unilever (targeting 30% virgin plastic reduction by 2026) are setting global benchmarks.

- Tamper-evident security: Specialized seals and tear strips are now essential for building consumer trust in post-pandemic hygiene product markets.

- E-commerce resilience: Leak-proof pouches and durable bottles dominate demand from direct-to-consumer and online platforms.

- Digital engagement: QR-enabled and smart packaging enhance traceability, transparency, and consumer interaction.

Market Analysis: Sustainability Mergers, Smart Packaging Expansion, and Capacity Scale-Ups (2024–2025)

The past two years have seen the hygiene packaging industry pivot toward sustainability, recycling integration, and automation upgrades. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica to strengthen its presence in medical-grade solutions. The same month, Amcor reported a 43% YoY increase in Q4 net sales, reflecting gains from its Berry Global acquisition (April 2025), which enhanced its hygiene packaging portfolio.

On the consumer goods side, Unilever (August 2025) acquired a stake in Lucro Plastecycle, securing recycled flexible plastics supply, while P&G (August 2025) announced that 80% of its packaging is recyclable or reusable, exceeding FSC-certified paper targets. Earlier, Solenis merged with NCH Corporation (June 2025), creating a stronger water and hygiene solutions portfolio. Sonoco (December 2024) broadened its hygiene sector footprint by acquiring Eviosys, boosting its metal aerosol packaging capacity.

Innovation-led developments are also reshaping the sector. Amcor & Mespack (November 2024) launched a 2L AmPrima recycle-ready stand-up pouch designed for hygiene and home care. Unilever (October 2024) integrated AI-powered vision inspection in its Polish facility, improving accuracy and reducing waste by 22%. Collectively, these developments highlight a strategic industry pivot toward circular economy practices, operational efficiency, and packaging formats tailored for e-commerce durability and brand differentiation.

Trends and Opportunities Defining the Future of the Hygiene Packaging Market

Strategic Investment in Post-Consumer Recycled (PCR) Content Integration

The hygiene packaging market is witnessing a decisive shift as leading chemical producers and packaging converters commit significant capital expenditure to integrate post-consumer recycled (PCR) content into their operations. This move goes beyond brand sustainability pledges, representing a structural change in packaging supply chains.

Corporate commitments are driving this transformation. Unilever aims to achieve 100% recyclability for its rigid plastic packaging by 2030 while halving its use of virgin plastic. Similar initiatives from other CPG leaders are placing upward pressure on the availability and quality of PCR plastics. Regulatory mandates reinforce this momentum: Washington State’s PCR law requires that household cleaning and personal care product containers contain 15% PCR by 2025, with stepwise increases in subsequent years. This creates a legally binding demand signal for recyclers and converters.

To meet these requirements, manufacturers are investing in recycling infrastructure and circularity initiatives. A European flexibles division of a major packaging group reported a 36% year-on-year increase in PCR polyethylene (PE) use in 2024, reflecting enhanced sourcing and reprocessing capabilities. Certification programs like the Association of Plastic Recyclers (APR) PCR Certification are providing third-party assurance, cited in California’s SB54, to ensure recycled content claims are credible. This convergence of regulation, brand demand, and infrastructure investment is firmly establishing PCR integration as a defining trend in hygiene packaging.

Refill and Reuse System Pilots Gaining Corporate Investment

Alongside PCR adoption, hygiene packaging is experiencing a strategic pivot toward refill and reuse systems, shifting away from linear single-use formats to circular models. FMCG companies are piloting a variety of reusable systems, ranging from refill stations to direct-to-consumer (DTC) models, as they seek to scale sustainable consumption patterns.

Unilever has already tested 50+ refill pilots globally, including over 1,000 refill stations in Indonesian warungs (small shops), which saved more than 6 tonnes of plastic by selling 91,000 liters of product. DTC disruptors like Blueland have built entire businesses on refillable, plastic-free cleaning tablets, supplying over 1 million households with compostable-packaged refills. In Europe, initiatives like WRAP’s reuse “Blueprint” are targeting systemic change by developing multi-brand and multi-retailer solutions that normalize reusable packaging in mainstream retail.

These pilots highlight how refill and reuse strategies are moving from niche experiments to scaled corporate investments. The implications for hygiene packaging are profound, requiring innovations in container durability, logistics, and infrastructure to accommodate repeated use and circularity.

Development of Monomaterial and Recyclable Flexible Pouches

The rise of concentrated and unit-dose hygiene products such as laundry pods, detergent sheets, and refill liquids is driving the use of flexible plastic pouches. However, the industry faces a recyclability challenge, as most of these pouches are made from multi-laminate structures. This creates a major opportunity to develop high-barrier monomaterial pouches that meet functional demands while being compatible with drop-off or curbside recycling systems.

Mondi Group’s RetortPouch exemplifies this innovation, offering a mono-polyolefin high-barrier film designed for recycling in existing streams. ProAmpac’s ProActive Recyclable range similarly advances mono-PE pouches designed for household and personal care applications. By reducing polymer complexity, these solutions address recyclability head-on while meeting technical requirements like moisture, oxygen, and chemical resistance. Strategic R&D is further accelerating adoption, enabling brands to comply with regulations and market products as “recycling-ready.”

This opportunity positions monomaterial pouches as the next-generation standard in hygiene packaging functional, sustainable, and aligned with regulatory mandates.

Smart Packaging for Supply Chain Efficiency and Consumer Engagement

The integration of digital technology into hygiene packaging is emerging as a high-value opportunity, transforming labels and containers into interactive platforms that serve both supply chain and consumer functions. By embedding QR codes, RFID tags, or unique identifiers, packaging evolves beyond containment into a node of real-time information.

From a supply chain perspective, smart packaging enhances transparency by providing real-time lifecycle data including carbon footprint and recycling instructions. This helps brands align with corporate ESG reporting requirements and regulatory traceability mandates. For consumers, digital engagement features are increasingly expected. A quick QR scan can deliver ingredients, safety guidelines, usage instructions, and promotional offers, reinforcing brand loyalty.

Competitive Landscape: Global Leaders Driving Sustainable, Secure, and Smart Hygiene Packaging

The hygiene packaging market is dominated by multinational packaging giants, FMCG leaders, and specialized firms, with competition centered on sustainable materials, tamper-proof designs, and advanced dispensing solutions. Players differentiate themselves through R&D in recyclable and bio-based materials, mergers to expand capacity, and integration of smart packaging technologies.

Amcor PLC Expanding scale with Berry acquisition and recyclable innovation

Amcor delivers flexible and rigid hygiene packaging including pouches, bottles, and films. With its Berry Global acquisition (April 2025), Amcor significantly boosted its operational scale in hygiene packaging. The company leads in sustainable packaging, launching paper-based sachets and recycle-ready laminates, and leverages its global network to serve top FMCG and personal care brands.

Berry Global, Inc. PCR innovation for hygiene bottles and closures

Now under Amcor, Berry Global specializes in plastic bottles, closures, and specialty containers for wipes and sanitizers. It has introduced post-consumer recycled (PCR) polymers into non-contact-sensitive packaging and drives the “More Together” circularity initiative, advancing recyclability and bio-based resin integration.

Sonoco Products Company Strengthening metal aerosol packaging portfolio

Sonoco produces rigid paper, flexibles, rigid plastics, and metal containers widely used in hygiene. With its Eviosys acquisition (Dec 2024), Sonoco expanded into metal aerosol cans for air fresheners and sanitizers. Its consumer packaging division grew 110% in Q2 2025, and procurement-driven efficiency programs delivered $15M in savings, boosting competitiveness.

Kimberly-Clark Corporation Advancing FSC-certified and recycled packaging

Kimberly-Clark, a hygiene product leader, focuses on sustainable and efficient in-house packaging for tissues, wipes, and personal care. In 2025, it highlighted progress in FSC-certified fibers and recycled content integration, alongside compact formats to cut material use. Its portfolio includes paper-based and recyclable packs, aligned with sustainability commitments.

Unilever Scaling refill and recycled plastic strategies

Unilever integrates packaging into its 30% virgin plastic reduction goal (by 2026). In 2025, it invested in Lucro Plastecycle (India) to secure recycled flexible plastics. Its innovations include paper-based flexible packs and higher PCR content bottles, while refill and reuse pilots align with its global plastic footprint reduction strategy.

Procter & Gamble (P&G) Circular packaging pioneer with 80% recyclability milestone

P&G is a top consumer of hygiene packaging, setting global precedents in sustainability. In August 2025, it confirmed 80% of its packaging is recyclable/reusable and cut virgin petroleum resin use by 21% (from 2017 baseline). Its focus spans lightweighting, recycled materials, and plastic-free packaging systems, such as razor packs transitioned to recyclable cardboard boxes with 50%+ recycled fiber.

Hygiene Packaging Market Share Insights

Flexible Packaging Leads Hygiene Packaging Market Share by Type

In 2025, flexible packaging secures 50% of the global hygiene packaging market, establishing itself as the clear leader in this high-volume sector. Its dominance is fueled by widespread adoption across feminine hygiene, baby diapers, adult incontinence products, and medical disposables, where lightweight formats reduce shipping costs and barrier films maintain sterility. Flexible formats also align with sustainability transitions, with brands increasingly deploying bioplastics and recyclable films to meet ESG mandates. Rigid packaging retains a significant share, particularly in bottles, tubs, and tubes for liquid soaps, wipes, and premium hygiene products where structure, protection, and brand perception are non-negotiable. Aerosol packaging holds a smaller but specialized role, primarily in medical sprays, antiseptic applications, and personal care items like deodorants, reflecting demand in niche, performance-driven categories despite higher costs and recycling challenges. This segmentation illustrates how flexible packaging dominates for scale and efficiency, rigid formats defend premium positioning, and aerosols sustain specialized value niches.

Personal Care & Cosmetics Dominate Hygiene Packaging Market Share by Application

By application, personal care and cosmetics account for 45% of the hygiene packaging market in 2025, cementing their position as the volume and value anchor. This segment thrives on consistent global demand for daily hygiene products such as wipes, diapers, oral care items, and sanitary protection, where cost-efficient flexible packaging and sustainable material innovation are central. Medical and healthcare packaging follows as a major growth driver, supported by stringent sterility requirements, tamper-evidence features, and regulatory compliance in surgical kits, sterile disposables, and medicated hygiene products. Meanwhile, home care and toiletries maintain a steady share, reflecting essential demand for cleaning wipes, toilet paper films, and refillable liquid soap packaging. The overarching theme across applications is the dual imperative of sustainability and safety, with personal care leading in volume, medical use driving growth, and home care representing stable, essential consumption.

United States: Digitalization and Sustainability Driving Hygiene Packaging Innovations

The U.S. hygiene packaging market is experiencing rapid transformation, driven by digitalization, sustainability, and e-commerce growth. Companies are increasingly integrating smart features such as QR codes and NFC chips on packaging to provide information on product ingredients, usage instructions, and recycling guidelines, enhancing transparency and consumer trust. Sustainability initiatives are a key market driver, with eco-friendly materials, including post-consumer recycled (PCR) plastics and paper-based alternatives, gaining significant traction. Brands like UMF|PerfectCLEAN have introduced compostable packaging to reduce landfill waste, aligning with broader corporate sustainability goals. The booming e-commerce sector further propels demand for durable and tamper-evident packaging, ensuring product integrity during shipping. Additionally, investments in manufacturing capacity, such as Huhtamaki’s $30 million expansion in Texas for folding cartons, underscore the market’s commitment to scaling production to meet rising demand.

Germany: Regulatory Leadership and Circular Economy Accelerating Market Growth

Germany’s hygiene packaging market is shaped by strict regulations and a strong focus on sustainability. The German Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR) create high demand for eco-friendly packaging materials, driving the adoption of recycled content and designs for easy recyclability. Leadership in the circular economy encourages collaboration between manufacturers and end-users to develop fully recyclable systems. Innovations in antimicrobial packaging are emerging, providing hygienic solutions that extend product shelf life and enhance safety. The market also benefits from advanced automation technologies, as German manufacturers prioritize packaging solutions compatible with automated and semi-automated systems, improving efficiency and reducing labor costs.

China: Governmental Sustainability Initiatives and E-Commerce Fuel Market Expansion

China’s hygiene packaging market is witnessing rapid growth, driven by governmental policies promoting sustainable packaging and the expansion of e-commerce. Plastic bans and waste management regulations are encouraging companies to adopt eco-friendly, reusable, and reduced packaging solutions. The logistics sector is heavily reliant on durable, secure packaging, including tamper-evident seals and tear-resistant films, to meet the needs of the booming delivery ecosystem. Companies are actively reducing over-packaging and promoting the use of original manufacturer packaging to minimize material waste and carbon emissions. Additionally, innovations in smart packaging, such as real-time monitoring with time-temperature indicators and gas sensors, are enhancing product quality, safety, and supply chain transparency.

India: Government Initiatives and Growing Hygiene Consciousness Driving Packaging Demand

India’s hygiene packaging market is being propelled by government initiatives like Swachh Bharat Abhiyan and the Make in India program, which encourage the production and distribution of sanitary and hygiene products. Regulatory compliance, particularly under the Plastic Waste Management (Amendment) Rules, 2022, and the draft Environment Protection (Extended Producer Responsibility for Packaging) Rules, 2024, is driving adoption of eco-friendly alternatives and circular economy practices. Flexible packaging solutions are gaining popularity, offering cost-effective, functional, and sustainable options for personal care and home care products. Rapid urbanization, growing middle-class awareness of hygiene, and increased e-commerce penetration are further fueling demand for high-quality, branded, and visually appealing packaging solutions.

Brazil: Circular Economy Policies and E-Commerce Growth Driving Market Dynamics

The Brazilian hygiene packaging industry is evolving under government policies that support a circular economy. The National Solid Waste Policy of 2010 mandates reverse logistics for packaging waste, enhancing recycling rates and sustainable packaging adoption. Regulatory frameworks from the Brazilian Health Regulatory Agency (Anvisa), including RDC 752/2022, ensure product safety and traceability for personal hygiene, cosmetics, and perfumes. The rapid growth of e-commerce has increased demand for secure, efficient packaging solutions that protect products during transit, while sustainable materials and innovations are being embraced to meet environmental objectives and consumer expectations.

Japan: Small-Format Packaging and Sustainable Material Innovations Leading the Market

Japan’s hygiene packaging market is influenced by demographic trends, such as the high proportion of single-person households, which drive demand for compact and individually packaged products. Strict regulations ensure product safety, hygiene, and quality, prompting manufacturers to produce highly reliable packaging solutions. The Plastic Resource Circulation Act and corporate initiatives, such as Kao Corporation’s commitment to eliminate plastic packaging waste by 2040, support sustainability and recycling. Collaborations like Kirin Holdings and Fancl, which convert brewery waste into packaging materials, exemplify innovative approaches to eco-friendly packaging, reinforcing Japan’s leadership in sustainable hygiene solutions.

Hygiene Packaging Market Report Scope

Hygiene Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$118.8 Billion

|

|

Market Size (2034)

|

$202.4 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Material Type (Plastics, Paper & Paperboard, Metal, Glass), By Packaging Type (Flexible Packaging, Rigid Packaging, Aerosol Packaging), By Application (Personal Care & Cosmetics, Medical & Healthcare, Home Care & Toiletries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Group, Inc., Mondi Group, Sealed Air Corporation, Sonoco Products Company, Huhtamaki Oyj, AptarGroup, Inc., DS Smith Plc, Avery Dennison Corporation, International Paper, WestRock Company, Pactiv Evergreen Inc., CCL Industries Inc., Crown Holdings Inc., Gerresheimer AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hygiene Packaging Market Segmentation

By Material Type

- Plastics

- Paper & Paperboard

- Metal

- Glass

By Packaging Type

- Flexible Packaging

- Rigid Packaging

- Aerosol Packaging

By Application

- Personal Care & Cosmetics

- Medical & Healthcare

- Home Care & Toiletries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Hygiene Packaging Market

- Amcor plc

- Berry Global Group, Inc.

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Huhtamaki Oyj

- AptarGroup, Inc.

- DS Smith Plc

- Avery Dennison Corporation

- International Paper

- WestRock Company

- Pactiv Evergreen Inc.

- CCL Industries Inc.

- Crown Holdings Inc.

- Gerresheimer AG

*List not Exhaustive

Research Coverage

This comprehensive report by USDAnalytics investigates the global hygiene packaging market, highlighting breakthroughs in sustainable materials, smart packaging, and e-commerce-ready designs. The analysis reviews historical trends from 2021 to 2024 and provides detailed forecasts through 2034, offering industry stakeholders a deep understanding of market dynamics, growth drivers, and competitive positioning. This report is an essential resource for packaging manufacturers, FMCG leaders, supply chain strategists, and sustainability-focused executives, as it evaluates the adoption of post-consumer recycled (PCR) content, refill and reuse systems, and monomaterial flexible pouches that meet regulatory and consumer demands. The study further highlights innovations in tamper-evident designs, digital engagement via QR and NFC-enabled solutions, and automation-led operational efficiencies, while presenting a thorough assessment of M&A activities, capacity scale-ups, and strategic partnerships. USDAnalytics emphasizes key market insights, including regulatory mandates, circular economy practices, and consumer behavior shifts driving packaging format evolution, ensuring decision-makers can optimize investment, operational, and product strategies for long-term growth.

Scope Highlights:

- Segmentation: By Material Type (Plastics, Paper & Paperboard, Metal, Glass), By Packaging Type (Flexible Packaging, Rigid Packaging, Aerosol Packaging), By Application (Personal Care & Cosmetics, Medical & Healthcare, Home Care & Toiletries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Profiles and analysis of 15+ leading players including Amcor plc, Berry Global Group, Inc., Mondi Group, Sealed Air Corporation, Sonoco Products Company, Huhtamaki Oyj, AptarGroup, Inc., DS Smith Plc, Avery Dennison Corporation, International Paper, WestRock Company, Pactiv Evergreen Inc., CCL Industries Inc., Crown Holdings Inc., and Gerresheimer AG.

Methodology

The research methodology for this hygiene packaging market report combines primary and secondary data sources, ensuring a robust, industry-validated perspective. Primary research involved interviews with senior executives, R&D heads, and supply chain managers across leading packaging manufacturers, FMCG companies, and sustainability consultancies, capturing insights into product innovation, regulatory compliance, and market adoption trends. Secondary research included analysis of company annual reports, press releases, government policies, trade association publications, and credible market databases. Quantitative modeling and statistical analyses were employed to generate market size estimations, growth projections, and segmentation forecasts. USDAnalytics applied triangulation to cross-verify data points and leveraged scenario-based forecasting to account for macroeconomic variables, regulatory shifts, and technological adoption rates. Advanced analytical tools were used to assess regional trends, market share evolution, and the impact of emerging formats such as monomaterial pouches and smart packaging solutions on supply chain efficiency and consumer engagement. This approach ensures actionable insights for strategic planning, investment evaluation, and competitive benchmarking.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.