Metal Aerosol Can Market Overview: Sustainability and Sectoral Growth Driving Expansion

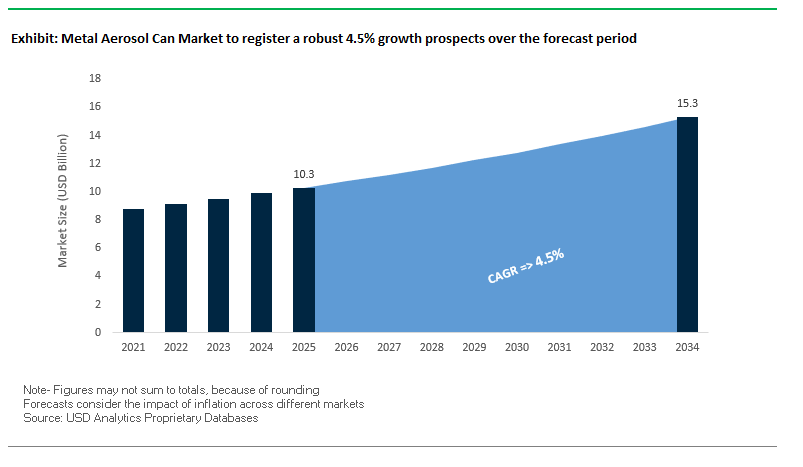

The global metal aerosol can market is valued at $10.3 billion in 2025 and is projected to reach $15.3 billion by 2034, growing at a steady CAGR of 4.5%. This growth reflects the rising importance of sustainable, recyclable packaging solutions across personal care, household, and healthcare applications. The high recyclability of aluminum and steel positions metal aerosol cans as a preferred choice for brands committed to circular economy initiatives. For industry professionals, the market raises important questions: Which sectors are generating the most consistent demand? How does sustainability shift material choices? Where are new growth opportunities emerging?

The dominance of personal care products such as deodorants, hair sprays, and shaving creams ensures a strong baseline of demand. Simultaneously, the home care and DIY sector has seen steady growth since the pandemic, creating sustained demand for aerosol-based cleaning and household products. Emerging niches are shaping future growth trajectories, particularly in medical and pharmaceutical applications, where metal aerosol cans are increasingly used in respiratory therapies and topical drug delivery. For instance, the reliance of asthma inhalers on metal aerosol packaging underscores the sector’s role in life-saving treatments.

Key Insights for Industry Professionals:

- Sustainability as a growth driver: Aluminum aerosol cans are infinitely recyclable without quality loss, meeting consumer and regulatory demand for green packaging.

- Personal care leads adoption: Deodorants, hair sprays, and shaving foams dominate demand across mature markets.

- Home care growth opportunity: Post-pandemic consumer behavior supports strong growth in DIY and cleaning segments.

- Medical packaging expansion: Respiratory and topical drug delivery aerosols create a high-value growth niche.

Market Analysis: Recent Industry Developments Shaping the Aerosol Can Industry

The metal aerosol can industry has been marked by continuous innovation, sustainability commitments, and strategic restructuring in recent years. In January 2025, Ball Corporation showcased its latest sustainable solutions at the Global Aerosol & Dispensing Forum (ADF) in Paris, emphasizing lightweight packaging and renewable energy use. By May 2025, Ball collaborated with Açaí Motion® to launch a natural energy drink can certified by the Aluminum Stewardship Initiative (ASI), reinforcing the role of sustainability certifications as a market differentiator. Later in August 2025, Ball strategically completed the sale of 41% of its ownership interest in its joint venture in Saudi Arabia, underscoring its focus on core aluminum packaging operations.

Crown Holdings advanced its decarbonization strategy by receiving SBTi validation for its new net-zero targets in August 2025, confirming its leadership in sustainable packaging. At the same time, Ardagh Metal Packaging (AMP) reported 16% revenue growth in Q2 2025, fueled largely by strong demand across the Americas. This was preceded by its forecast in February 2025 projecting robust volume growth, particularly in beverage and aerosol packaging. In a similar move to highlight sustainability, Trivium Packaging published its 2024 Sustainability Report in April 2025, noting a 2% reduction in Scope 1 and 2 GHG emissions and that nearly 47% of its 2024 revenue came from eco-designed products.

Consolidation and expansion are also shaping the market landscape. Sonoco Products Company made a significant move in June 2024 by acquiring Eviosys, strengthening its global footprint in metal food and aerosol packaging. Meanwhile, JPFL Films announced in July 2025 a ₹700 crore investment to expand its Nashik plant in India, signaling a strategic shift toward flexible packaging. While not directly in metal aerosols, such moves are reshaping the competitive landscape, with cross-segment competition influencing pricing and sustainability strategies.

Emerging Trends and Strategic Opportunities Driving the Metal Aerosol Can Market

Strategic Capacity Expansion for Hydrocarbon and DME Propellant-Based Personal Care Products

The global metal aerosol can market is witnessing a strong wave of investments as brands shift away from compressed gas propellants toward Hydrocarbons (HCs) and Dimethyl Ether (DME), particularly in the personal care segment. Products such as deodorants and hair sprays demand finer mist quality and compatibility with water-based formulations, which has positioned HCs and DME as the preferred options. According to the U.S. Environmental Protection Agency (EPA), these propellants have largely replaced high-GWP alternatives in non-medical consumer aerosols, a change that gained momentum after the phaseout of chlorofluorocarbons (CFCs).

The unique characteristics of DME—such as 35 wt% water solubility and a 4.5 bar vapor pressure at 20°C—make it ideal for homogeneous water-based solutions but necessitate aerosol cans with specifically engineered coatings and pressure resistance. This shift is forcing manufacturers to retrofit and expand their production lines, with European plants announcing capacity expansions in late 2024 to serve this growing demand. However, the use of flammable HCs and DME requires stringent compliance with safety guidelines from agencies like the UK HSE, pushing companies to invest heavily in infrastructure, ventilation, and explosion-proof equipment.

Adoption of Super-Compliant and Varnish-Free Internal Coatings

The transition to BPA-free and varnish-free internal coatings is transforming the aerosol packaging sector, especially for cans used in food and sensitive personal care applications. The European Food Safety Authority (EFSA) recently reduced the tolerable daily intake of BPA to just 0.2 nanograms/kg body weight—a drastic cut of 20,000 times compared to earlier limits—prompting the European Commission Regulation (EU) 2024/3190 to enforce a full ban on BPA in food contact materials.

Leading companies are already moving ahead of regulation. For example, Trivium Packaging announced in late 2024 its readiness to convert most internal lacquers to BPA non-intent formulations. Simultaneously, innovators such as AkzoNobel are launching new coatings free not only from BPA but also from other controversial substances such as styrene and formaldehyde. These next-generation coatings promise high chemical resistance, durability, and compliance with NIAS regulations, ensuring that aerosol cans meet the safety standards required for global food and cosmetic applications.

Development of Aerosol Platforms for Next-Generation Eco-Friendly Propellants (HFOs & CO₂)

The demand for eco-friendly propellants is unlocking a significant opportunity for manufacturers to redesign aerosol can platforms. With growing pressure to lower the Global Warming Potential (GWP) of propellants, Hydrofluoroolefins (HFOs) and compressed CO₂ are emerging as the next frontier. HFO-1234ze(E), now listed by the EPA as an acceptable alternative, offers a GWP of less than 1, making it a sustainable replacement for older hydrofluorocarbons (HFCs).

Unlike HCs and DME, CO₂ requires cans that can withstand pressures of 100 psi or more, necessitating the use of thicker metals or reinforced structures. This is opening a niche market for advanced material R&D and specialized engineering designs. Organizations such as the EFCTC are pushing adoption of non-flammable HFOs for technical aerosols, which demand custom internal coatings to prevent chemical interactions. Manufacturers that adapt early with next-generation can linings and robust structures will position themselves as leaders in the sustainable aerosol packaging segment.

Integration of Digital Printing for Limited Edition and Personalized Packaging

A major opportunity is emerging from the digital transformation of packaging, where digital printing on aerosol cans is enabling short runs, personalization, and rapid design shifts. Unlike traditional lithography, which requires costly plates and weeks of setup, digital printing supports on-demand production with consistent per-unit costs, even at volumes under 100,000 units.

Competitive Landscape: Leading Companies Defining the Global Metal Aerosol Can Market

The global metal aerosol can market is highly competitive, with leadership held by multinational corporations that balance sustainability, scale, and technological innovation. Companies are differentiating themselves through lightweight designs, circularity initiatives, and eco-certifications, alongside strong distribution networks.

Trivium Packaging Leads with Circular Economy Focus

Trivium Packaging offers a broad portfolio of infinitely recyclable metal aerosol cans serving personal care, household, and food applications. In April 2025, the company published its 2024 Sustainability Report, highlighting its commitment to a circular economy, including a 47% revenue share from eco-designed products. With lightweighting initiatives and recycled content integration, Trivium’s core strength lies in aligning product design with customer sustainability goals while offering design and technical support for optimized product launches.

Ball Corporation Strengthens Innovation and Core Business Focus

Ball Corporation is a global leader in aluminum packaging solutions, with a strong presence in aerosol cans for beverages, personal care, and household products. Its ReAl alloy aerosol can, launched earlier, contains 50% recycled content and reduces carbon footprint by half compared to standard cans. In August 2025, Ball divested part of its joint venture in Saudi Arabia to sharpen its focus on core operations. With sustainability targets that include 100% renewable electricity by 2030, Ball remains a benchmark for green innovation in metal packaging.

Crown Holdings Commits to Net-Zero through Twentyby30 Program

Crown Holdings operates in 39 countries, offering aluminum and steel aerosol cans across personal care, household, and industrial applications. In August 2025, it secured SBTi validation for its new net-zero targets, reaffirming its sustainability commitments. The company’s Twentyby30 program drives its ESG progress, emphasizing environmental, social, and governance pillars. Crown’s competitive advantage lies in its extensive geographic reach and manufacturing expertise, making it one of the most resilient players in global aerosol packaging.

Ardagh Group Accelerates Growth in the Americas

Ardagh Metal Packaging (AMP), part of the Ardagh Group, supplies recyclable aluminum and tinplate cans across diverse markets including personal care and home care. In July 2025, AMP reported 16% year-on-year revenue growth and a 34% jump in adjusted EBITDA in the Americas, signaling operational strength. With a focus on lightweighting and innovative design, Ardagh is targeting high-growth categories such as energy drinks, sparkling water, and premium aerosol packaging. Its diversified product portfolio ensures resilience in fluctuating market conditions.

EXAL Corporation’s Legacy Strengthens Trivium Packaging

EXAL, a recognized leader in aluminum aerosol packaging in the Americas, became part of Trivium Packaging following its merger with Ardagh’s Food & Specialty Metal Packaging business in 2019. Known for its expertise in sustainable aluminum solutions, EXAL provided the foundation for Trivium’s strong position today. Its legacy in customer-focused, innovative design and eco-conscious packaging continues to enhance Trivium’s global capabilities, making the combined entity one of the most influential players in the aerosol can market.

Metal Aerosol Can Market Share Insights

Straight Wall Cans Dominate Market Share by Product Type in the Metal Aerosol Can Industry

Straight wall cans account for 65% of the global metal aerosol can market, making them the clear volume leader due to their unmatched production efficiency and structural reliability. Their simple cylindrical design enables high-speed manufacturing lines to produce millions of units cost-effectively, which is essential for mass-market categories such as air fresheners, disinfectants, deodorants, shaving foams, and hairsprays. The format’s structural integrity is ideal for withstanding internal pressures from compressed gases, ensuring safety and consistency across global supply chains. Furthermore, straight wall cans offer optimal print surfaces for branding, making them a preferred choice for high-volume consumer goods companies. Their dominance is further strengthened by their recyclability and compatibility with modern propellant innovations, particularly compressed gases that are replacing VOCs to meet sustainability regulations in Europe, North America, and Asia.

Personal Care and Cosmetics Lead Market Share by Application in the Metal Aerosol Can Industry

The personal care and cosmetics sector holds 45% of global aerosol can demand, making it the single largest application segment. This dominance stems from the entrenched consumer reliance on aerosol-based products such as antiperspirants, deodorants, hair sprays, and mousse foams, where controlled dispensing and hygienic application are critical. Major beauty and grooming brands continue to prioritize aerosol packaging due to its ability to deliver consistent performance, shelf appeal, and premium branding opportunities. Growth is further supported by innovations in propellants (such as compressed air and nitrogen) that reduce environmental impact, as well as lightweight aluminum designs that enhance sustainability credentials. The increasing penetration of aerosol packaging into emerging beauty categories, including self-tanning sprays, body mists, and men’s grooming products, ensures that personal care will remain the anchor application driving future market expansion.

United States Metal Aerosol Can Market Driven by EPA Regulations and Recycling Initiatives

The United States metal aerosol can market is shaped by a strict regulatory environment led by the Environmental Protection Agency (EPA) and the Department of Transportation (DOT), alongside state-level measures like California’s circular economy and Extended Producer Responsibility (EPR) laws. These policies are accelerating demand for highly recyclable aluminum and steel aerosol cans, pushing manufacturers to invest in sustainable production methods. A landmark initiative is the Aerosol Recycling Initiative launched by the Can Manufacturers Institute (CMI) and the Household & Commercial Products Association (HCPA) with support from over 20 companies, aiming to boost the recycling rate of aerosol cans to 85% nationwide.

Technological advancements such as lightweighting with advanced aluminum alloys are reducing both material usage and shipping emissions, making cans more cost-effective and environmentally friendly. The market is further supported by Ball Corporation’s aluminum end manufacturing facility in Kentucky, which strengthens domestic supply chains. With strong demand from the personal care, hygiene, and household cleaning sectors, and with home hygiene trends fueling air freshener and disinfectant usage, the U.S. remains a global leader in sustainable metal aerosol packaging innovation.

Germany Metal Aerosol Can Market Accelerated by EU Circular Economy and Recycled Content Use

The Germany metal aerosol can market operates under the European Union’s Circular Economy Action Plan and the Packaging and Packaging Waste Regulation (PPWR), which prioritize recyclability and high-value secondary materials. These frameworks encourage the adoption of aluminum and tinplate cans that are easy to recycle and integrate into a closed-loop system. German manufacturers are at the forefront of custom can shaping technologies, such as “can contouring” that enables brands to create ergonomic, asymmetrical packaging for better consumer appeal.

Sustainability is a major differentiator, with 25% of European aluminum supply sourced from recycled scrap, and the German aerosol industry being one of the biggest users. The personal care segment, especially deodorants and hairsprays, drives consumption in Germany, where per-capita aerosol usage is among the highest in Europe. With strong regulatory pressure and a culture of innovation, Germany remains a benchmark for sustainable and premium-quality metal aerosol cans in Europe.

China Metal Aerosol Can Market Expands with High-End Manufacturing and Digital Printing

The China metal aerosol can market is expanding rapidly under government initiatives to boost domestic high-end manufacturing and reduce reliance on imports. Supportive industrial policies and infrastructure projects are creating a fertile environment for aerosol can growth. Chinese manufacturers are investing heavily in automation and digital printing technologies, enabling on-demand, customizable can designs that cater to the branding needs of global FMCG companies.

Global players are strengthening their local presence, with multinational FMCG firms investing in local can production and filling facilities to shorten supply chains and meet China’s growing consumer demand. Applications are diverse, ranging from personal care and household products to automotive and insecticide packaging, with growth underpinned by rising hygiene awareness. With rapid adoption of eco-friendly packaging materials driven by China’s regulations on single-use plastics, the market is transitioning toward sustainable yet high-performance aerosol can solutions.

India Metal Aerosol Can Market Strengthened by Make in India and Growing Middle Class Demand

The India metal aerosol can market is gaining momentum from government-backed policies like the “Make in India” initiative and the National Medical Devices Policy 2023, which are aimed at enhancing domestic manufacturing capacity. The industry is witnessing a clear technological shift with the adoption of two-piece lightweight aerosol cans, engineered with improved safety and performance features to meet the needs of a growing consumer base.

Key applications in India include the personal care sector, particularly deodorants, which dominate aerosol demand. Additionally, household insecticides and food applications are expanding rapidly, fueled by rising disposable incomes and the burgeoning middle-class consumer base. Major paint and coatings companies, including Asian Paints’ backward integration projects, also reinforce packaging growth indirectly by securing raw material supply chains. With expanding industrial parks and a favorable investment climate, India is emerging as a fast-growing hub for aerosol can manufacturing and innovation.

Brazil Metal Aerosol Can Market Supported by Regulatory Standards and Industrial Growth

The Brazil metal aerosol can market is driven by regulations from the National Health Surveillance Agency (Anvisa), including the national UDI system for medical labeling and certification, which indirectly impacts aerosol packaging compliance. Technological advancements in steel aerosol cans, valued for their rigidity and pressure resistance, address the challenges of Brazil’s diverse climate and long-distance logistics.

Corporate investments are reshaping the sector, with Crown Holdings opening a new beverage can facility in Rio Verde and domestic firms like Cerviflan Embalagens Metalicas modernizing equipment to produce higher-quality steel cans. Demand is strongest in personal care, chemical, and automotive applications, with rising demand for insecticides and repellents following health-related outbreaks. Brazil’s combination of regulatory reforms, industrial investment, and consumer-driven demand is solidifying its role as a leading metal aerosol can market in Latin America.

Japan Metal Aerosol Can Market Driven by Precision Engineering and Bag-on-Valve Technology

The Japan metal aerosol can market is defined by its focus on precision manufacturing and high-quality materials, with companies like Toyo Seikan and Kansai Paint driving advancements in both aluminum and tinplate cans. Strict oversight from the Pharmaceuticals and Medical Devices Agency (PMDA) ensures aerosol packaging meets stringent safety standards, especially following the May 2025 amendment to the Pharmaceuticals and Medical Devices Act, which emphasized supply stability for drugs and medical packaging.

Japan is a leader in specialty and high-performance aerosol products, with growing adoption of Bag-on-Valve (BoV) technology, which separates the product from the propellant to extend shelf life and broaden applications in food, pharmaceuticals, and cosmetics. Demand is also rising in marine coatings and industrial paints, supported by companies like Chugoku Marine Paints. With a strong focus on sustainability, premium finishes, and functional innovation, Japan continues to lead in value-added aerosol packaging solutions globally.

Metal Aerosol Can Market Report Scope

Metal Aerosol Can Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.3 Billion

|

|

Market Size (2034)

|

$15.3 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Material (Aluminum, Steel & Tinplate, Other Materials), By Product Type (Straight Wall Cans, Necked-In Cans, Shaped Cans, Others), By Propellant Type (Liquefied Gas, Compressed Gas), By Application (Personal Care & Cosmetics, Household Products, Automotive & Industrial, Food & Beverages, Pharmaceuticals & Healthcare, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings, Inc., Ardagh Group S.A., Toyo Seikan Group Holdings, Ltd., Trivium Packaging, Sprea S.p.A., DS Containers, Inc., CCL Container, Technocap S.p.A., Exal Corporation, Nampak Ltd., Colep Packaging, Lindal Group, Nussbaum GmbH & Co. KG, V.I.P. srl

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Aerosol Can Market Segmentation

By Material

- Aluminum

- Steel & Tinplate

- Other Materials

By Product Type

- Straight Wall Cans

- Necked-In Cans

- Shaped Cans

- Others

By Propellant Type

- Liquefied Gas

- Compressed Gas

By Application

- Personal Care & Cosmetics

- Household Products

- Automotive & Industrial

- Food & Beverages

- Pharmaceuticals & Healthcare

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Metal Aerosol Can Market

- Ball Corporation

- Crown Holdings, Inc.

- Ardagh Group S.A.

- Toyo Seikan Group Holdings, Ltd.

- Trivium Packaging

- Sprea S.p.A.

- DS Containers, Inc.

- CCL Container

- Technocap S.p.A.

- Exal Corporation

- Nampak Ltd.

- Colep Packaging

- Lindal Group

- Nussbaum GmbH & Co. KG

- V.I.P. srl

* List Not Exhaustive

Methodology

The methodology used by USDAnalytics to evaluate the global Metal Aerosol Can market combines a multi-layered research approach that integrates primary interviews, secondary data analysis, and advanced forecasting models. Primary research included discussions with key stakeholders, including packaging engineers, sustainability managers, and supply chain directors across personal care, household, pharmaceutical, and industrial sectors to understand emerging trends, material innovations, propellant transitions, and regulatory impacts. Secondary research encompassed regulatory frameworks from the EPA, EU Circular Economy directives, EFSA, Anvisa, and PMDA, alongside company reports, sustainability disclosures, trade journals, and press releases to validate industry growth drivers, technological advancements, and competitive strategies. Market sizing and projections for 2025–2034 were determined using a combination of top-down and bottom-up approaches across product types, materials, propellant types, and applications, with attention to regional market dynamics in the U.S., Europe, China, India, Brazil, and Japan. Analysis also considered recent innovations, including varnish-free coatings, next-generation propellants (HCs, DME, HFOs, CO₂), digital printing capabilities, and eco-design strategies. Competitive benchmarking focused on multinational leaders such as Trivium Packaging, Ball Corporation, Crown Holdings, Ardagh Group, and Toyo Seikan, emphasizing sustainability, technological differentiation, and global expansion. This comprehensive methodology ensures that USDAnalytics provides actionable, data-driven insights for industry professionals seeking to understand market growth, regulatory impacts, and future opportunities in the metal aerosol can industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.