Plastic Packaging Sacks Market Size, Overview, and Growth Outlook (2025–2034)

Global Plastic Packaging Sacks Market Poised to Reach $2 Billion by 2034 with Steady 2.5% CAGR Driven by Industrial and Agricultural Demand

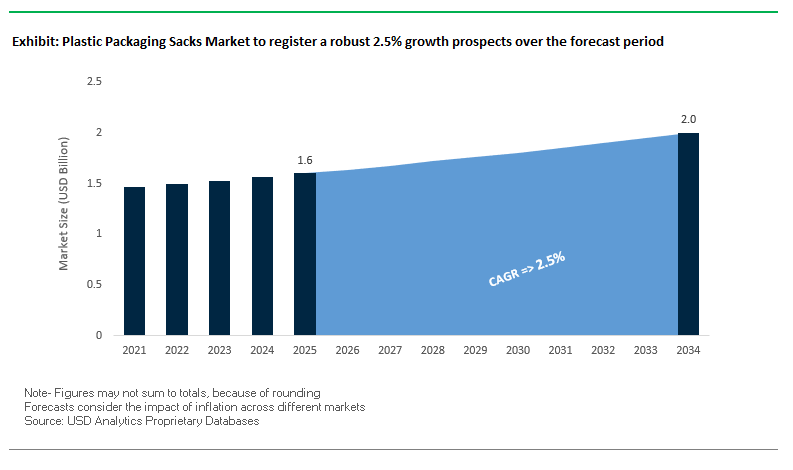

The global plastic packaging sacks market is projected to grow from $1.6 billion in 2025 to $2 billion by 2034, reflecting a CAGR of 2.5%. Growth is largely driven by high demand from industrial and agricultural sectors, where sacks are essential for transporting cement, chemicals, fertilizers, and animal feed. Polypropylene (PP) woven sacks remain the dominant product due to their high strength-to-weight ratio, moisture barrier properties, and tear resistance, making them ideal for heavy-duty applications.

Key Insights for industry professionals and buyers:

- Industrial and Agricultural Segments Lead Growth: Sacks are critical for bulk handling and transportation of powders, granules, and chemicals.

- Woven PP Sacks Remain Dominant: Their durability, moisture resistance, and versatility make them preferred in construction, agriculture, and industrial applications.

- Sustainable Alternatives Are Gaining Momentum: Biodegradable, recycled, and paper-plastic hybrid sacks are growing in popularity to meet ESG requirements.

- Product Protection Remains Core: Plastic sacks prevent spoilage, contamination, and physical damage during storage and transit.

- Innovation Focused on Circular Economy: Material advances, nanocoatings, and compostable options are emerging as key differentiators.

Market Analysis: Recent Developments Highlight a Strategic Shift Toward Sustainable and High-Performance Packaging Sacks

The plastic packaging sacks market is witnessing strategic innovations, sustainability initiatives, and capacity expansions. In August 2025, Mondi ramped up production of FunctionalBarrier Paper Ultimate, an ultra-high barrier paper solution providing a sustainable alternative to conventional plastic sacks. That same month, Sonoco invested $30 million to expand production in the adhesives and sealants market, reinforcing its leadership in industrial plastic sack solutions. In May 2025, Mondi further expanded its re/cycle MailerBAG capacity to serve e-commerce customers seeking sustainable and flexible packaging.

The industry is also embracing high-tech innovations to enhance performance and environmental compliance. In April 2025, Novolex received a national award for its reusable foodservice containers, while a Nano Letters study introduced ALD-based ultrathin film techniques, which could impact next-generation high-barrier sacks. March 2025 saw Novolex earn a Gold Award for Sustainability for its compostable butter wrap, signaling a strong industry shift toward eco-friendly solutions.

Collaborations and international expansions reflect market maturation. February 2025 featured Mondi and Proquimia launching paper-based stand-up pouches for dishwashing tabs, highlighting a move toward monomaterial and sustainable packaging. In August 2024, Amcor expanded its healthcare packaging network in Costa Rica, demonstrating the company’s strategic focus on global presence and supporting industrial demand for plastic packaging sacks.

Emerging Trends and Opportunities Reshaping the Plastic Packaging Sacks Market

Accelerated Integration of Post-Consumer Recycled (PCR) Content

The plastic packaging sacks market is witnessing a rapid transformation as regulatory frameworks and corporate sustainability goals converge to accelerate the adoption of post-consumer recycled (PCR) content. The European Union’s Packaging and Packaging Waste Regulation (PPWR), which came into force in early 2025, sets binding minimum recycled content requirements across all plastic packaging formats, including sacks. This regulation establishes a direct compliance pathway that compels manufacturers to integrate PCR content to maintain market access. On the corporate front, leading FMCG companies are intensifying commitments. PepsiCo, for instance, has pledged to achieve an average of 40% recycled content in plastic packaging by 2035, while Nestlé has committed to cutting virgin plastic use by 30% by 2025. Such ambitious targets cascade through the value chain, placing pressure on suppliers of industrial and consumer sacks to align with these benchmarks. To meet demand, the industry is strengthening its supply chain with large-scale investments. Plastics Europe has reported that chemical recycling investments are projected to triple from €2.6 billion in 2025 to €8 billion in 2030, ensuring a steady supply of food-grade and high-performance recycled polyolefins. Together, these regulatory and corporate dynamics are driving systemic change in how plastic sacks are produced and sourced.

Adoption of Performance-Enhanced Mono-Material Structures

Another defining trend in the plastic sacks market is the pivot toward mono-material structures, addressing one of the sector’s biggest recycling challenges. Traditional sacks made from multi-layer laminates often combine incompatible polymers, making them difficult to reprocess. To overcome this barrier, companies are engineering mono-material sacks designed for recyclability without sacrificing performance. Mondi’s innovations in mono-material pouches, which achieve a 100% recyclability rating and incorporate removable panels, provide a blueprint for sacks that can seamlessly re-enter the circular economy. Technological advances in co-extrusion and material science now enable the production of mono-material films with strong resistance to oxygen, moisture, and light. Academic research further confirms that polyolefin-based mono-material films can meet the stringent shelf-life and durability requirements for applications ranging from animal feed and fertilizers to construction materials. This shift to mono-material formats not only addresses regulatory recycling requirements but also positions sacks as a viable, circular solution in markets with high material recovery standards.

Development of Bio-Based and Biodegradable Polymers for Technical Applications

A key opportunity in the plastic sacks sector lies in the adoption of bio-based and biodegradable polymers, particularly for applications where recycling infrastructure is limited or collection is impractical. In agriculture and horticulture, for instance, sacks used for mulch, soil, or fertilizers often remain contaminated and difficult to recover. Here, certified compostable polymers such as BASF’s ecoflex® (PBAT) and ecovio® offer an alternative end-of-life pathway by breaking down under industrial composting conditions and contributing to soil enrichment. Beyond compostability, bio-based polyethylene derived from renewable sources like sugarcane provides a “drop-in” solution compatible with existing production lines. This reduces fossil fuel dependence while enabling manufacturers to market sacks with a lower carbon footprint. By integrating bio-based polymers, manufacturers not only address end-of-life challenges but also enhance brand positioning with eco-conscious consumers and industries increasingly measured by their environmental performance.

Digital Watermarking for Intelligent End-of-Life Sorting

The integration of digital watermarking presents a transformative opportunity for the end-of-life management of plastic packaging sacks. Flexible plastics, including sacks, are among the most challenging waste streams to recycle profitably due to contamination and sorting inefficiencies. The HolyGrail 2.0 initiative has demonstrated that digital watermarks embedded into packaging can provide unique information about composition and intended use, enabling high-speed optical sorters to achieve sorting purity levels above 93%. By creating clearly defined material streams, digital watermarking elevates the value of recycled plastics and makes flexible sack recycling economically viable. Importantly, this technology can differentiate food-grade from non-food-grade packaging, ensuring compliance with safety standards while producing higher-value recyclates. As Extended Producer Responsibility (EPR) fees increase globally, the economic incentive to adopt such solutions becomes even stronger. By embracing digital watermarking, sack manufacturers and recyclers can close the loop on flexible plastics, advancing both regulatory compliance and circular economy objectives.

Competitive Landscape: Leading Companies Are Driving Innovation, Sustainability, and Market Expansion in Plastic Packaging Sacks

The plastic packaging sacks industry is dominated by companies leveraging sustainability, material innovation, and global manufacturing capabilities to meet demand across industrial, agricultural, and e-commerce sectors.

Berry Global Group, Inc.: Delivering Heavy-Duty and Sustainable Industrial Sacks

Berry Global manufactures bags, liners, flexible films, and industrial sacks for food, beverage, retail, and industrial markets. The company’s strategy focuses on sustainable packaging solutions, targeting 100% of packaging to be reusable, recyclable, or compostable by 2025. Berry’s Right-Fit can liners and high-performance industrial sacks minimize plastic waste while offering superior durability. Its broad product portfolio and global footprint enable service to a diverse customer base.

Mondi Group: Pioneering High-Barrier and Sustainable Plastic Sack Alternatives

Mondi is a global leader in plastic and hybrid paper-plastic sacks, offering laminated and high-performance paper sacks. In August 2025, the company launched FunctionalBarrier Paper Ultimate, a sustainable solution against oxygen, moisture, and grease. Mondi’s strategy emphasizes circular economy principles, investing in technologies and acquisitions like Schumacher Packaging to enhance its sustainable and connected packaging capabilities.

Novolex: Advancing Eco-Friendly Packaging Solutions Across Multiple Sectors

Novolex provides plastic sacks, paper bags, and compostable solutions across foodservice, retail, and industrial applications. In March 2025, Novolex earned a Gold Award for Sustainability for its compostable butter wrap. Its operations include two HDPE recycling centers in the U.S., and the company is committed to reducing greenhouse gas emissions by 30% per ton of production by 2030. Novolex serves grocery, industrial, and specialty packaging sectors, highlighting versatility and sustainability.

Sonoco Products Company: Expanding Industrial Sack Production to Meet Growing Market Needs

Sonoco offers plastic sacks and bags for industrial and agricultural applications, emphasizing strength and moisture protection. In July 2025, Sonoco invested $30 million to expand production, adding 100 million units annually. The company’s strategy focuses on value-added packaging solutions and sustainability, combining flexible and rigid formats to meet diverse client requirements.

Amcor plc: Providing High-Performance and Eco-Conscious Plastic Sacks Globally

Amcor delivers high-performance sacks and rollstock for building, industrial, and consumer products. Leveraging the Catalyst™ program, Amcor collaborates with brands to design tailored sustainable packaging. Its sacks feature barrier properties, reinforced handles, and recycled content, supporting durability, brand visibility, and sustainability objectives. The company aims for 100% recyclable or reusable packaging by 2025, positioning it as a leader in eco-conscious solutions.

Plastic Packaging Sacks Market Share Insights, 2025-2034

Trash Bags and Liners Lead Market Share by Product Type in the Plastic Packaging Sacks Industry

Trash bags and liners hold the largest share at 28% of the plastic packaging sacks market, reflecting their indispensable role in households, institutions, and municipal waste management. Their demand is non-discretionary and resilient, directly tied to rising urbanization and waste generation, making them a volume leader even as regulations target single-use plastics. Woven sacks form the industrial backbone, with polypropylene-based solutions dominating agriculture, fertilizers, animal feed, and construction due to their high tensile strength, reusability, and cost-efficiency. Laminated sacks play a pivotal role in barrier-sensitive applications such as chemicals, premium fertilizers, and food staples, where product integrity drives value. Film sacks cater to lighter consumer goods and retail packaging, prized for printability and branding but less durable than woven formats. Gusseted sacks continue to grow in bulk food and industrial retail, offering superior palletization and shelf stability. Rubble sacks remain entrenched in construction waste applications, while specialty sacks (anti-static, breathable, custom designs) cater to low-volume, high-value industrial niches. This segmentation highlights how trash bags dominate everyday volume, while woven and laminated sacks are central to global agriculture, construction, and chemical supply chains.

Waste Management Represents the Largest Market Share by Application in Plastic Packaging Sacks

Waste management leads with 30% of the global plastic packaging sacks application share, sustained by its role as the core application for trash bags and liners across residential, commercial, and municipal sanitation systems. This segment is the most heavily regulated, facing mandates for recycled content, compostable alternatives, and reductions in single-use plastics, yet its demand remains stable due to the absence of viable large-scale substitutes. Agriculture and fertilizers, holding 22%, represent the next major application, where woven and laminated sacks are indispensable for transporting seeds, fertilizers, and animal feed, with demand closely tied to agricultural output cycles and government subsidies. Construction follows as a cyclical but high-volume sector, where woven sacks package cement and sand while rubble sacks manage demolition waste, making the segment a direct indicator of infrastructure growth. Industrial goods and chemicals, though smaller in volume, demand high-performance sacks with barrier protection and chemical resistance, prioritizing safety and reliability over cost. Food and beverages rely on laminated and gusseted sacks for flour, sugar, salt, and grains, with innovation focused on barrier-critical mono-material recyclability. Retail and consumer goods add value through branding and shelf presence in categories like pet food and potting soil. Together, these applications highlight how waste management drives stable volume, agriculture ensures scale, and food & chemicals demand high-performance innovation, shaping the industry’s dual challenge of meeting mass demand while transitioning toward circularity.

European Union: Regulatory Pressure Driving Circular Economy Packaging

The European Union plastic packaging sacks market is being heavily reshaped by the Packaging and Packaging Waste Regulation (PPWR), which officially entered into force in February 2025. This regulation sets mandatory recyclability standards and reuse targets, compelling manufacturers to innovate around mono-material structures and higher recycled content. The EU Single-Use Plastics Directive further restricts consumption, setting a target of reducing lightweight plastic carrier bags to 40 bags per citizen by the end of 2025. National-level measures amplify these effects—Italy’s plastics tax introduced in 2023 continues to discourage disposable packaging use. Demand is shifting toward durable plastic bags usable for at least 125 cycles, which aligns with EU circular economy principles. Producers are investing in designs that meet recyclability requirements while reducing virgin plastic use, ensuring compliance and competitiveness in an increasingly sustainability-driven market.

United States: State-Level Bans and EPR Laws Redefining the Market

In the United States, the plastic packaging sacks industry is influenced by a patchwork of state-level regulations. California’s 2024 law banning single-use plastic carryout bags will take effect in January 2026, permitting only recycled paper or certified reusable plastic bags. Similarly, Washington’s ESHB 1293 law, effective January 2026, increases charges on plastic film carryout bags to 12 cents, creating economic disincentives for single-use plastics. At the federal level, the FDA and USDA impose stringent rules on food-grade plastic sacks, prioritizing safety and contamination prevention. The growing adoption of Extended Producer Responsibility (EPR) laws, such as Maryland’s 2025 packaging waste legislation, is pushing brands toward post-consumer recycled (PCR) content. Companies are focusing on developing PCR-based sacks that align with both sustainability goals and regulatory requirements, making the U.S. market a hotspot for compliance-driven innovation.

China: Strong Bans and Push Toward Biodegradable Plastics

China’s government is leading a strict campaign against plastic pollution, beginning with the “plastic limit order” that bans bags under 0.025 mm thickness. A new June 2025 regulation focuses on curbing e-commerce delivery waste by mandating recyclable and reusable systems, significantly influencing the demand for packaging sacks. The NDRC and MEE have strengthened enforcement of bans on environmentally harmful plastics while encouraging investment in biodegradable and oxo-degradable plastic alternatives. Recycling remains a critical area, with China’s recycling rate already surpassing 30% by 2021 and expected to rise. The 2025 positive list for food-contact materials and new adhesive standards are redefining how food-grade plastic sacks are produced. This dual push—towards biodegradable materials and circular economy practices—positions China as a leader in both regulation and large-scale adoption of sustainable sack solutions.

India: Extended Producer Responsibility Accelerating Local Innovation

India’s plastic packaging sacks market is evolving under the Plastic Waste Management Rules (2016, amended in 2022), which mandate strict Extended Producer Responsibility (EPR) compliance. Manufacturers and brand owners must take accountability for plastic waste collection and recycling, intensifying the shift toward eco-friendly alternatives. National programs such as Swachh Bharat Abhiyan complement these measures by promoting waste segregation and door-to-door collection. India is witnessing a surge in bioplastics innovation, including the recent patent of ghee residue–based bioplastic, which highlights local approaches to circularity. Venture funding, such as the investment secured by Dharaksha Ecosolutions for packaging made from agricultural waste, demonstrates rising domestic investment in sustainable packaging. Meanwhile, FSSAI’s consultations on sustainable packaging are steering food businesses toward biodegradable and recyclable sack solutions. India’s market trajectory combines grassroots innovation with regulatory enforcement, making it a rapidly growing hub for sustainable sack manufacturing.

United Kingdom: Plastic Packaging Tax Shaping Material Selection

The UK’s Plastic Packaging Tax (PPT), introduced in April 2022, has become a defining force in the plastic packaging sacks market. This tax applies to packaging with less than 30% recycled content, effectively incentivizing recyclability. HMRC data shows that by 2024–2025, 51% of UK plastic packaging met the 30% recycled threshold, a significant achievement in material circularity. The market is increasingly focused on single-material recyclable packaging, aiming to eliminate the complexities of multi-material sack recycling. In addition, the government is preparing a deposit return scheme for plastic bottles, which will indirectly influence sack designs used for collection and logistics. The UK’s proactive fiscal measures and growing industry compliance rates are reinforcing its position as a leader in recycled-content packaging sacks across Europe.

Canada: Federal Ban on Single-Use Plastics Accelerating Market Transition

Canada’s plastic packaging sacks market is primarily driven by the Single-Use Plastics Prohibition Regulations (SUPPR), which prohibit the manufacture, import, and sale of checkout bags and other problematic plastics. This legislation is part of Canada’s Zero Plastic Waste by 2030 goal and is expected to eliminate over 1.3 million tonnes of difficult-to-recycle plastic waste while preventing 22,000 tonnes of annual plastic pollution. To accelerate industry transition, the government provides guidance on PLA-based and compostable alternatives, supporting companies adopting non-conventional solutions. In addition, joint federal and provincial funding of $2.9 million for Exxel Polymers reflects the government’s commitment to scaling 100% recycled plastic production. The Canadian market is rapidly shifting toward bioplastics and recycled-content sacks, with federal and provincial incentives ensuring compliance and fostering innovation in sustainable alternatives.

Plastic Packaging Sacks Market Report Scope

Plastic Packaging Sacks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$2 Billion

|

|

Market Growth Rate

|

2.5%

|

|

Segments

|

By Material (PE, PP, Bio-Degradable Materials, Recycled Content Plastics, Others), By Product Type (Woven Sacks, Laminated Sacks, Film Sacks, Gusseted Sacks, Trash Bags & Liners, Rubble Sacks, Others), By Application (Industrial Goods & Chemicals, Agriculture & Fertilizers, Food & Beverages, Waste Management, Construction, Retail & Consumer Goods, Others), By Closure Type (Sewn/Stitched, Heat Sealed, Adhesive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Novolex Holdings, LLC, Berry Global, Inc., Mondi Group, Interplast Group, Uflex Ltd., Sonoco Products Company, Winpak Ltd., Coveris S.A., Rondo-Pak, LLC, International Plastics, Inc., Advance Polybag, Inc., Superbag, Ltd., Unistar Plastics Co., Cardia Bioplastics Ltd., Polybags Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Packaging Sacks Market Segmentation

By Material

- PE

- PP

- Bio-Degradable Materials

- Recycled Content Plastics

- Others

By Product Type

- Woven Sacks

- Laminated Sacks

- Film Sacks

- Gusseted Sacks

- Trash Bags & Liners

- Rubble Sacks

- Others

By Application

- Industrial Goods & Chemicals

- Agriculture & Fertilizers

- Food & Beverages

- Waste Management

- Construction

- Retail & Consumer Goods

- Others

By Closure Type

- Sewn/Stitched

- Heat Sealed

- Adhesive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Packaging Sacks Market

- Novolex Holdings, LLC

- Berry Global, Inc.

- Mondi Group

- Interplast Group

- Uflex Ltd.

- Sonoco Products Company

- Winpak Ltd.

- Coveris S.A.

- Rondo-Pak, LLC

- International Plastics, Inc.

- Advance Polybag, Inc.

- Superbag, Ltd.

- Unistar Plastics Co.

- Cardia Bioplastics Ltd.

- Polybags Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and systematic research methodology to deliver an authoritative and comprehensive analysis of the Plastic Packaging Sacks Market. Our approach combines both primary and secondary research, encompassing interviews with industry experts, executives, and key stakeholders across global markets, alongside detailed evaluation of company reports, press releases, regulatory updates, and financial filings. USDAnalytics incorporates quantitative modeling to forecast market size, growth trajectories, and segmental trends, integrating factors such as material adoption (PE, PP, biodegradable, recycled content), product types (woven, laminated, film, gusseted, trash bags), and end-use applications (industrial, agriculture, food, waste management). We also analyze technological advancements, sustainability initiatives, and government regulations across major regions, including the U.S., EU, China, India, UK, Canada, and Brazil, to assess their impact on demand, production, and supply chain dynamics. Our methodology emphasizes transparency, accuracy, and actionable insights for industry professionals, highlighting opportunities in recycled content adoption, bio-based polymers, mono-material innovations, and digital watermarking for intelligent sorting. By synthesizing market intelligence, competitive benchmarking, and regulatory landscapes, USDAnalytics delivers forward-looking insights that enable manufacturers, distributors, and investors to make informed strategic decisions in the evolving Plastic Packaging Sacks Market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.