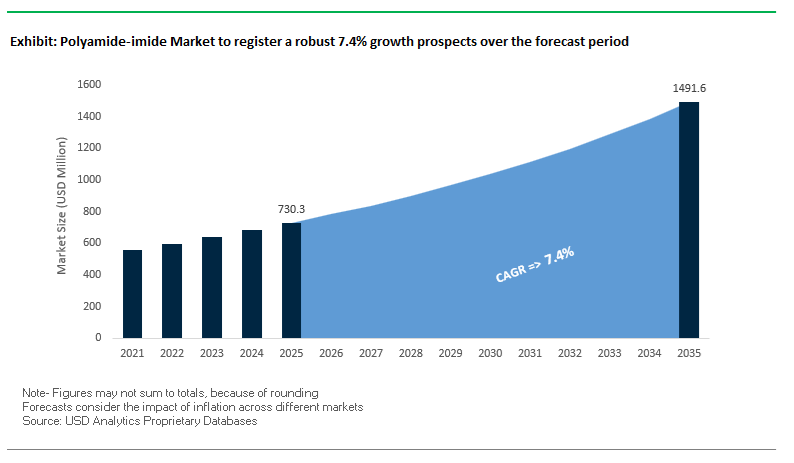

The Polyamide-imide (PAI) Market, valued at USD 730.3 million in 2025, is projected to reach USD 1,491.2 million by 2035, expanding at a strong CAGR of 7.4%. Market growth is driven by surging demand for ultra-high-temperature polymers, the miniaturization of electronics, semiconductor equipment expansion, and the shift toward metal replacement materials in aerospace, automotive, and oil–gas environments.

The Polyamide-imide Market is experiencing accelerated technology adoption, particularly in aerospace propulsion, semiconductor manufacturing, and e-mobility systems, where extreme thermal and mechanical loading create material performance gaps that PAI fills better than any competing polymer. In October 2025, Syensqo spotlighted the integration of Torlon® PAI into cryogenic propulsion systems for next-generation satellite launchers. The application leverages Torlon’s ultra-low-temperature ductility down to −200°C—capabilities extremely rare among high-temperature thermoplastics, expanding PAI’s relevance in aerospace engines and spaceflight seals.

In September 2025, Ensinger announced substantial extrusion capacity expansion for its TECAPAI product family in North America, targeting the semiconductor manufacturing equipment sector. As extreme ultraviolet (EUV) lithography and wafer transport systems demand ultra-pure polymers with low outgassing and plasma resistance, TECAPAI rods and plates are increasingly deployed in wafer handling tools, test sockets, and furnace components. Meanwhile, the global oil & gas sector updated specifications in June 2025, mandating PAI adoption in downhole sealing systems and high-pressure electrical connectors, citing its proven resistance to H₂S exposure, hydrocarbons, and thermal cycling—further solidifying PAI as a reliability-critical E&P material.

Regulatory shifts also shape product innovation. In April 2025, RTP Company launched a PFAS-free PAI wear-compound portfolio addressing emerging restrictions across Europe and North America. The positions RTP as a key supplier to industries seeking sustainable tribology solutions for high-temperature bearings and sliding components. Earlier in January 2025, Mitsui Chemicals advanced miniaturization trends with its AURUM® thin-wall injection molding grade, engineered for thermal management in 5G electronics and compact electromechanical components.

In November 2024, Syensqo introduced a high-flow PAI injection molding grade, reducing cure cycle times by up to 15%, addressing one of the largest processing bottlenecks for PAI and improving throughput in automotive and industrial part production. By August 2024, the North American EV sector had significantly ramped up PAI adoption in e-motor slot wedges, UL94 V-0 dielectric components, and battery thermal runaway barriers, reflecting PAI’s unparalleled combination of dielectric strength, heat resistance, and structural reliability. Additional momentum came from Saint-Gobain’s May 2024 expansion of its Meldin® 7000 PAI/PI hybrid series into hydrogen fuel cell systems, positioning PAI as a core material within the clean energy sector’s high-pressure sealing environment.

Industry professionals evaluating PAI prioritize properties including thermal endurance at 275°C, extreme dimensional stability, high mechanical strength, and exceptional tribological performance under dry lubrication conditions. For buyers, key questions center around long-term thermal reliability, processing difficulty, regulatory compliance (PFAS-free), and PAI’s ability to deliver metal-like precision in next-generation mechanical assemblies.

- Highest continuous-use temperature among thermoplastics (275°C): Ensures reliable performance in electric motor insulation, turbocharger components, and jet engine seals.

- Flexural Modulus 35% higher than unfilled PEEK: Offers superior stiffness for high-pressure valves, bushings, and structural precision components.

- Carbon-fiber-reinforced PAI matches metal CLTE: Enables tolerance-critical applications including labyrinth seals and semiconductor fixtures.

- Limiting PV > 14,000 psi-fpm: Makes PAI the leading choice for unlubricated compressor vanes, thrust washers, and high-speed bearing systems.

High-Temperature Electrification Demands, Advanced Aerospace FST Regulations, and New High-Performance Applications Reshape the Polyamide-Imide (PAI) Market

Trend 1 - PAI Becomes the Critical High-Temperature Insulation and Structural Material for 800V+ EV Traction Motors

Polyamide-imide is rapidly becoming a mission-critical high-performance polymer for next-generation high-speed EV traction motors, where extreme thermal, electrical, and mechanical demands disqualify most alternative engineering plastics. As OEMs transition toward 800V–1000V platforms to achieve higher efficiency and faster charging, PAI’s superior thermal endurance and stability make it the premier choice for insulation, seals, and load-bearing elements inside EV electric drive units.

PAI’s maximum continuous use temperature of 260°C-with a Heat Deflection Temperature approaching 280°C-provides a thermal margin unmatched by most high-performance polymers, including PEEK. With a Class 220°C thermal index, PAI enables magnet wire enamels, slot liners, and motor insulation components to operate safely under high-power density and high-frequency switching conditions that typically accelerate polymer breakdown.

The electrical-grade variants of PAI offer exceptionally high dielectric strength and volume resistivity, directly supporting the suppression of partial discharge phenomena in high-voltage motors. This enables thinner insulation designs without sacrificing long-term integrity, a key factor for increasing copper fill factor and motor power density.

Structurally, PAI retains a remarkably high percentage of its tensile strength even at 200°C, outperforming competing thermoplastics that soften under such loads. Its low creep behavior further ensures that precision-fit structural components-including thrust washers, rotor spacers, and bearing retainers-maintain dimensional stability across the full lifespan of the EV powertrain. As EV powertrains continue to push the boundaries of temperature and rotational speed, PAI's combination of mechanical, thermal, and electrical performance solidifies its role as the enabling polymer for high-efficiency electric propulsion.

Trend 2 - PAI Adoption Accelerates in Aerospace Wire & Cable to Meet Evolving FST, Radiation, and Weight Reduction Requirements

The Polyamide-imide Market is also receiving strong momentum from the aerospace sector, where OEMs and regulatory bodies are enforcing stricter requirements for flame resistance, smoke density, toxicity (FST), radiation endurance, and weight optimization. PAI-based insulation materials are being deployed across wiring harnesses, cabin systems, and mission-critical electronics due to their ability to exceed FAA and UL 94 V-0 fire performance criteria.

PAI's excellent radiation resistance is particularly valuable in advanced aircraft and spacecraft. Certified tests show that a 30% glass-reinforced PAI retained 95% of its mechanical properties after exposure to 10⁹ rads, a performance level few polymers can match. This makes PAI ideal for long-duration space missions and high-altitude unmanned systems where ionizing radiation rapidly degrades conventional insulations.

A key differentiator is PAI’s ability to achieve significant weight savings across wiring harnesses. Its high mechanical strength and dielectric stability allow for reduced insulation thickness without affecting performance or safety-translating into measurable reductions in aircraft mass and improved fuel efficiency. This aligns strongly with the aviation industry’s push toward lightweight materials across all subsystems.

Furthermore, PAI’s robust resistance to aviation fuels, hydraulic oils, and de-icing chemicals ensures insulation longevity even under harsh environmental conditions. These traits are driving rapid adoption of PAI in next-generation aircraft programs and accelerating its role as a foundational material in aerospace electrification and More-Electric Aircraft (MEA) architectures.

Opportunity 1 - PAI as a High-Purity, High-Temperature Metal Replacement in Semiconductor Process Chamber Equipment

A major growth opportunity lies in expanding PAI’s role as a metal replacement in semiconductor fabrication equipment, especially in high-temperature, plasma-rich environments where purity and dimensional stability are indispensable. PAI’s ultra-low outgassing performance supports cleanroom-driven manufacturing requirements, making it ideal for wafer handling arms, wear components, alignment parts, and chamber internals.

The polymer’s extremely low Coefficient of Linear Thermal Expansion (CLTE)-approximately 1.7×10⁻⁵ in/in/°F for unfilled grades-ensures precision and repeatability across rapid thermal cycling events ranging from ambient temperatures to 260°C. This dimensional stability is essential for tools that must maintain micron-level tolerances to prevent wafer misalignment or yield loss.

Wear-optimized bearing grades of PAI integrate PTFE, graphite, or carbon fibers, significantly outperforming metals and ceramics in frictional environments. Their low wear rates also reduce particle contamination, a critical factor for ultra-thin nodes below 7 nm. PAI’s broad chemical and plasma resistance widens its applicability across etching, deposition, cleaning, and dry processing chambers.

As semiconductor manufacturers shift toward higher-temperature, higher-vacuum, and lower-contamination process environments, PAI’s value proposition expands substantially-unlocking new revenue streams in advanced fabrication equipment, wafer transfer systems, and precision robotic handling.

Opportunity 2 - Development of Laser-Sinterable PAI Powders for Additive Manufacturing (AM) of High-Performance End-Use Components

Additive Manufacturing represents one of the highest-potential growth avenues for the PAI Market, particularly through the development of laser-sinterable PAI powders for Selective Laser Sintering (SLS). While SLS is currently dominated by PA12, the inability of traditional polymers to withstand temperatures above 150°C creates an industry-wide gap for ultra-high-performance AM materials-a gap PAI is uniquely positioned to fill.

Engineering PAI for SLS applications addresses several unmet needs:

- Thermal capability: AM components made from PAI could operate continuously at up to 260°C, enabling their use in aerospace ducts, oil & gas seals, high-temperature brackets, and engine-bay automotive parts.

- Mechanical strength: Fiber-filled PAI formulations can achieve tensile strengths of 150–220 MPa, approaching the performance of injection-molded grades and positioning AM as a viable alternative to machined metal in specific applications.

- Design freedom: The ability to print complex structures-conformal cooling channels, lightweight lattice structures, integrated hinges-would allow manufacturers to consolidate components, reduce assembly costs, and optimize system weight.

Developing stable, laser-processable PAI powders will accelerate the adoption of the polymer across high-value industrial applications where conventional plastics cannot perform, positioning PAI as a transformative material in the metal-replacement AM landscape.

Polyamide-Imide Market Share Analysis

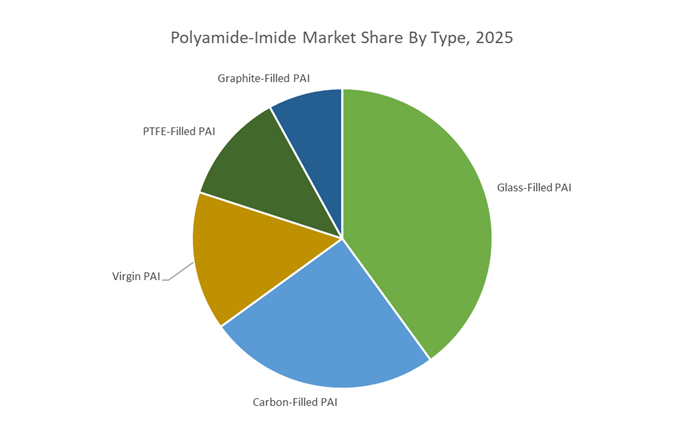

Market Share by Type/Grade: Glass-Filled PAI Leads Through High-Temperature Dimensional Stability and Metal-Like Mechanical Performance

Glass-Filled Polyamide-Imide (PAI) holds the dominant 40% share in the PAI market because it delivers the precise combination of thermal stability, stiffness, and dimensional accuracy required for high-performance structural applications that operate under extreme heat and mechanical stress. PAI is already recognized as one of the highest-performing thermoplastics on the market, but the incorporation of glass fibers significantly amplifies its capability by enabling the material to maintain exceptional rigidity at continuous operating temperatures ranging from 250°C to 275°C (500°F–530°F)—a range where most engineering polymers lose structural integrity. This elevated performance allows glass-filled PAI to compete directly with metals for demanding applications.

A key driver of its market leadership is its dramatically reduced Coefficient of Linear Thermal Expansion (CLTE). With glass reinforcement, PAI’s CLTE approaches values comparable to aircraft-grade aluminum, ensuring minimal dimensional drift during transitions from ambient to hot operating environments—an essential requirement for precision components such as fasteners, seals, compressor components, and gear systems. Glass-filled PAI also demonstrates superior creep resistance, enabling parts to withstand prolonged mechanical loading without deformation, even in high-temperature environments. This reliability, combined with its compatibility with high-precision machining and molding, ensures glass-filled PAI remains the preferred grade for OEMs across aerospace, industrial machinery, semiconductor equipment, and high-end automotive systems.

Market Share by End-Use Industry: Aerospace & Defense Dominates Owing to Lightweighting, High-Temperature Reliability, and Regulatory Compliance

Aerospace & Defense leads the Polyamide-Imide market with a 35% share, driven by the sector’s stringent requirements for lightweight materials that can outperform metals under extreme thermal and mechanical conditions. PAI is one of the very few thermoplastics capable of sustaining structural functionality in environments approaching 280°C (537°F)—its glass transition temperature—making it uniquely suited for jet engine components, high-friction control systems, precision bearings, seal rings, and high-temperature electrical insulation. By replacing metal parts with PAI, aerospace manufacturers achieve significant weight reductions—up to two-thirds compared to aluminum—directly improving fuel efficiency, extending flight range, and optimizing payload capacity, all of which are critical for commercial and military aviation platforms.

Beyond lightweighting, PAI’s dominance in aerospace stems from its ability to satisfy stringent flammability, smoke, and toxicity (FST) requirements, including the FAR 25.853 standard, making it one of the safest materials for cabin interiors, structural interfaces, and components that interact with high-energy or high-heat zones. Its outstanding dimensional stability and creep resistance ensure long-term reliability, reducing maintenance cycles and guaranteeing performance across multi-decade aircraft lifespans. As aerospace OEMs and defense contractors increasingly transition toward advanced materials to meet efficiency, sustainability, and safety targets, PAI’s exceptional thermal and mechanical profile solidifies its leadership and ensures continued high adoption across next-generation aircraft and defense systems.

Country Analysis: Global Polyamide-imide (PAI) Development Hubs

United States: Aerospace-Grade Polyamide-imide Advancing High-Wear, High-Temperature Engineering Applications

The United States remains the most influential development hub for Polyamide-imide (PAI) due to its reliance on high-performance polymers across aerospace, defense, oil & gas, and heavy industrial engineering. The country’s market is anchored by continuous product innovation from leading suppliers like Solvay, whose Torlon® PAI portfolio continues to evolve with new grades designed for high-wear, low-friction, unlubricated environments. Recent formulations—including graphite-filled and PTFE-enhanced PAI compounds—are engineered for critical rotating components such as compressor vanes, seal rings, and thrust washers, where PAI’s inherent creep resistance, dimensional stability, and tribological superiority outperform most engineering polymers.

The defense sector further elevates U.S. demand for PAI. The U.S. Department of Defense specifies the polymer for components requiring continuous service temperatures up to 260°C, particularly in aircraft engine parts, missile housings, and high-load structural elements. Its exceptional thermal stability and resistance to aviation fuels, lubricants, and aggressive chemicals make PAI indispensable for these mission-critical systems. Additionally, the oil & gas industry depends heavily on PAI for HPHT (High-Pressure/High-Temperature) applications. Downhole tools, sealing elements, and pump components rely on PAI to withstand extreme thermal loads, chemical exposure, and mechanical stress, enabling extended life cycles in harsh exploration environments.

Academic and industrial research partnerships in the U.S. continue to push PAI performance boundaries. Universities funded by aerospace, electronics, and materials firms are developing nanocomposite PAI structures with enhanced dielectric properties, stiffness, and reliability for next-generation insulation systems, electrical connectors, and miniaturized power electronics. These ongoing innovations ensure that the U.S. remains the leading global center for PAI engineering solutions tailored to the most demanding high-temperature and high-wear applications.

Europe (Germany / Belgium): PAI Demand Driven by EV High-Voltage Electrification and Advanced Industrial Coatings

Europe’s Polyamide-imide market is increasingly shaped by the acceleration of electric vehicle (EV) manufacturing, stringent electrical insulation standards, and the region’s advanced industrial machinery sector. European automakers are significantly increasing their use of PAI-based wire enamels for high-voltage traction motors, where components must withstand temperatures exceeding 220°C, rapid thermal cycling caused by fast charging, and long-term chemical exposure. These requirements make PAI a preferred insulation material for motor windings, slot liners, and high-temperature varnishes, directly linking PAI consumption to EV platform proliferation.

PAI resin supply in Europe also benefits from the presence of Solvay’s dedicated PAI production capacity in Belgium, ensuring secure access to high-performance materials for aerospace, automotive, and industrial customers throughout the region. European coatings and adhesives manufacturers rely heavily on PAI resins for non-stick coatings, chemically resistant barriers, and thermal-protective films, particularly in cookware, industrial turbines, and heavy-duty machinery exposed to corrosive environments.

Germany’s precision engineering sector is another major contributor to regional PAI adoption. Glass-filled PAI materials are widely used for precision gears, compressor components, and piston parts in industrial pumps and automation systems, offering superior mechanical stability, metal replacement capability, and reduced lubrication requirements. Europe’s continued focus on electrification, energy efficiency, and high-reliability industrial components ensures a sustained and technologically advanced PAI market.

Japan: Ultra-High-Purity PAI Solutions Supporting Electronics Miniaturization and Flexible Circuitry

Japan remains a global leader in high-purity polymer science, making it a critical innovation hub for Polyamide-imide and related polyimide derivatives used in advanced electronics, semiconductor packaging, and automotive sensing technologies. Japanese chemical manufacturers are pioneers in producing ultra-thin Polyimide/PAI-based films, often reaching thicknesses of just ~5 μm, supporting the increasing miniaturization of flexible printed circuit boards (FPCBs), foldable displays, and high-frequency semiconductor devices.

Japan’s electronics industry requires extremely pure PAI varnishes for wire enameling, micro-motor insulation, connectors, and miniature sensors, where even trace impurities can compromise dielectric strength, heat resistance, and long-term reliability. As a result, Japanese manufacturers invest heavily in purification, resin refinement, and batch-to-batch consistency to meet stringent quality expectations from global semiconductor and electronics OEMs.

In the automotive sector, Japanese suppliers integrate PAI into oxygen sensors, exhaust gas sensors, solenoids, and under-hood electronic components, where chemical resistance, thermal endurance, and mechanical stability are essential for long service life. Japan’s unmatched expertise in producing high-precision polymer intermediates, aramid fibers, and advanced coatings reinforces its pivotal role in the global PAI supply chain.

Competitive Landscape: Global Leaders in Polyamide-imide Resins, Stock Shapes & High-Temperature Tribology Solutions

The Polyamide-imide industry is dominated by resin originators and specialized compounders possessing deep process expertise in thermal curing, tribological optimization, and high-precision machining. Competitive advantage relies heavily on resin purity, ability to produce large-format stock shapes, and engineering support for critical part geometries.

Syensqo remains the backbone of the global PAI market, holding the original Torlon® PAI patents and maintaining full-scale polymer production capability. Its flagship Torlon® 7130 (30% carbon fiber) grade delivers one of the lowest CLTE values among all thermoplastics, enabling precision metal replacement in jet engine components, aircraft seals, and high-load mechanical parts. The company operates a worldwide technical support network specializing in thermal curing profile optimization—critical for ensuring dimensional stability in complex molded parts. Strategically, Syensqo is directing R&D toward HTS electrical components, defense-grade connectors, and e-mobility systems, reinforcing Torlon’s position as the highest-performing thermoplastic in severe environments.

Ensinger is a leading processor of PAI into rods, plates, tubes, and near-net shapes using advanced extrusion and compression molding technologies. Its TECAPAI portfolio serves semiconductor manufacturers requiring plasma resistance, low outgassing, and high dimensional stability for wafer handling equipment and test systems. The company also offers tribologically enhanced grades including TECAPAI CM XP440, combining PTFE and graphite for superior high-temperature bearing performance. Ensinger’s ability to supply large-format PAI plates and precision tubes positions it as a critical partner for OEMs machining specialized, ultra-tight–tolerance components.

RTP Company specializes in custom compounding, modifying PAI with fillers including glass fiber, carbon fiber, minerals, and conductive agents. In 2025, it advanced regulatory compliance leadership by launching PFAS-free wear compounds, replacing PTFE in high-performance applications while maintaining excellent friction and wear characteristics. RTP’s material portfolio also includes static-dissipative and electrically conductive PAI compounds engineered for electronics and ESD-sensitive equipment. Its in-house CAE (Computer-Aided Engineering) capability enables OEMs to optimize PAI injection-molded designs for thermal, structural, and tribological performance.

Mitsui Chemicals is the only fully integrated Asian producer of polyamide-imide resin under the AURUM® brand. Its key strength lies in Direct Forming Technology, enabling near-net-shape sintered PAI parts that drastically reduce machining waste. AURUM® high-flow grades are strategically targeted at mass-produced automotive components requiring miniaturization, thermal resistance, and tight tolerance—including engine sensors, transmission components, and high-frequency electronics. Mitsui also produces soluble PAI resins for flexible, heat-resistant PCB coatings, supporting the advancement of next-generation electronic architecture.

Saint-Gobain’s Omniseal business delivers Meldin® 7000 PAI/PI hybrid materials, combining the mechanical performance of PAI with the extreme thermal endurance of polyimide. These materials excel in aerospace seals, hydrogen fuel cell valves, high-pressure compressors, and defense systems where low permeability, creep resistance, and reliability are paramount. The company’s precision machining expertise and stringent AS9100-compliant quality control make it a trusted supplier for mission-critical components in aviation and energy transition markets.

Polyamide-imide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$730.3 Million

|

|

Market Size (2035)

|

$1491.2 Million

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Type/Grade (Glass-Filled PAI, Carbon-Filled PAI, Graphite-Filled PAI, Unfilled/Virgin PAI, PTFE-Filled PAI), By Form (Molding Resins, Wire Enamels/Varnishes, Coatings/Adhesives, Fibers), By Manufacturing Process (Compression Molding, Extrusion, Injection Molding), By End-Use Industry (Aerospace & Defense, Automotive, Electrical & Electronics, Industrial Machinery, Oil & Gas), By Thermal Class (Class 200, Class 220, CST ≥250°C)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Solvay S.A., Toyobo Co. Ltd., Mitsubishi Gas Chemical Company Inc., Axalta Coating Systems Ltd., Elantas GmbH (Altana Group), Ensinger GmbH, Drake Plastics Ltd. Co., Kermel S.A., UBE Corporation, Resonac, Victrex plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polyamide-Imide (PAI) Market Segmentation

By Type/Grade

- Glass-Filled PAI

- Carbon-Filled PAI

- Graphite-Filled PAI

- Unfilled/Virgin PAI

- PTFE-Filled PAI

By Form

- Molding Resins

- Wire Enamels / Varnishes

- Coatings / Adhesives

- Fibers

By Manufacturing Process

- Compression Molding

- Extrusion

- Injection Molding

By End-Use Industry

- Aerospace & Defense

- Automotive

- Electrical & Electronics

- Industrial Machinery

- Oil & Gas

By Thermal Class

- Class 200

- Class 220

- CST ≥ 250°C

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Polyamide-Imide Manufacturers

- Solvay S.A.

- Toyobo Co., Ltd.

- Mitsubishi Gas Chemical Company, Inc.

- Axalta Coating Systems Ltd.

- Elantas GmbH (Altana Group)

- Ensinger GmbH

- Drake Plastics Ltd. Co.

- Kermel S.A.

- UBE Corporation

- Showa Denko Materials Co. Ltd. (Resonac)

- Victrex plc

*- List not Exhaustive