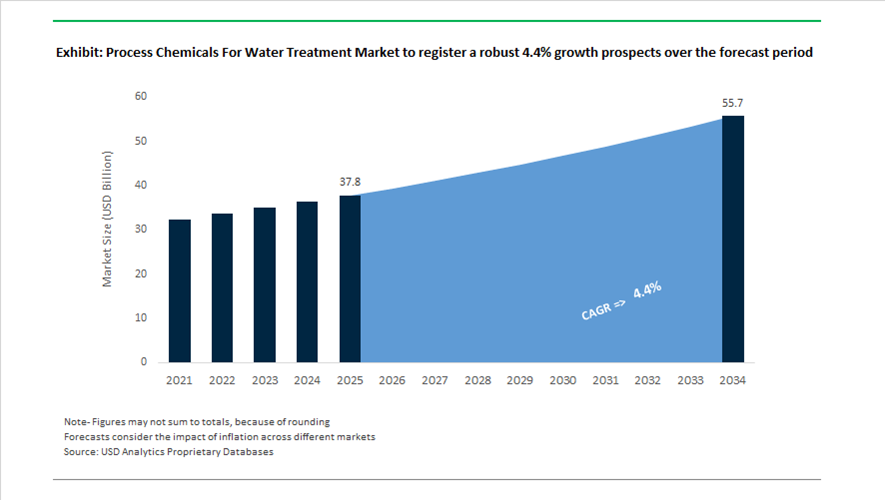

Process Chemicals for Water Treatment Market Valued at $37.8 Billion in 2025, Projected to Reach $55.7 Billion by 2034 at 4.4% CAGR

The global process chemicals for water treatment market is valued at $37.8 billion in 2025 and is projected to reach $55.7 billion by 2034, expanding at a CAGR of 4.4%. Growth is being driven by increasing demand for coagulants, flocculants, corrosion inhibitors, scale inhibitors, biocides, dispersants, membrane cleaning chemicals, ultrapure water treatment solutions, and desalination additives across energy, petrochemicals, semiconductors, pharmaceuticals, mining, and municipal infrastructure. Rapid industrialization in Asia, semiconductor fabrication expansion, AI-driven data center growth, and stricter water discharge regulations are intensifying the need for advanced water chemistry management and integrated treatment systems.

Strategic consolidation accelerated in 2024. In June 2024, Kurita Water Industries established Kurita AquaChemie India Private Limited to strengthen its presence in South Asia’s industrial water treatment chemicals market. In October 2024, Veolia Water Technologies opened a Life Science Centre of Excellence in Dublin, focused on high-purity water systems for biotech and pharmaceutical applications. In November 2024, Veolia launched Mobile Water Services in Europe, providing containerized chemical dosing and rapid-deployment treatment systems for life sciences and industrial facilities. In the same month, Ecolab acquired Barclay Water Management, enhancing its portfolio of Legionella risk mitigation chemicals and institutional water safety programs. Late 2024 also saw Solenis complete the acquisition of BASF’s mining flocculant business, expanding its offering in mineral processing and wastewater clarification.

Integration and digitalization defined 2025 developments. On April 1, 2025, Kurita formally merged Avista Technologies into Kurita America, consolidating expertise in membrane-specific antiscalants and cleaning chemicals for reverse osmosis systems. In March 2025, Honeywell acquired Sundyne for $2.16 billion, integrating high-pressure flow equipment with process chemical dosing systems for energy and petrochemical water treatment. In November 2025, Ecolab’s Nalco Water division launched an AI-powered 360-degree cooling program for data centers, automating the dosing of corrosion and scale inhibitors to manage the extreme water intensity of AI computing infrastructure. In late 2025, BASF introduced Sokalan DCS, a dispersant polymer optimized for membrane desalination plants, reducing scaling and lowering chemical cleaning frequency in high-output seawater reverse osmosis operations. In December 2025, Ecolab finalized the acquisition of Ovivo’s electronics ultrapure water division, strengthening its position in semiconductor-grade process chemicals and filtration systems.

Expansion into specialized chemical niches continued into 2026. In February 2026, Kemira acquired SIDRA Wasserchemie, reinforcing its coagulant portfolio in Central and Western Europe. Samyang Corporation’s 2024 Trilite RO and EDI launch signaled a shift toward integrated solutions combining ion exchange resins and membrane technologies for semiconductor ultrapure water systems, linking chemical treatment with hardware integration.

The process chemicals for water treatment market is increasingly characterized by AI-driven dosing optimization, membrane-specific antiscalants, mining flocculant integration, desalination dispersant innovation, ultrapure water chemicals for semiconductor fabs, Legionella risk management solutions, and containerized mobile treatment services. Cross-industry consolidation, digital water management platforms, and regional expansion into high-growth Asia-Pacific markets are reshaping competitive positioning across industrial, municipal, and high-purity water treatment segments.

Strategic Trends and High-Impact Opportunities in the Process Chemicals for Water Treatment Market

Performance-Based Shift Toward Blended and Digitally Optimized Chemical Programs

The process chemicals for water treatment market is undergoing a structural transition as industrial effluent streams become more variable, concentrated, and regulation-sensitive. Traditional single-ingredient coagulants and flocculants such as ferric chloride and alum are increasingly inadequate for complex wastewater profiles, particularly in food and beverage processing, pulp and paper, and petrochemical operations. In response, operators are pivoting toward performance-based blended formulations that combine coagulants, polymers, and functional additives into customized treatment programs designed to reduce total operational expenditure rather than minimize unit chemical cost.

This shift is evident in large-scale industrial expansions. In September 2024, Veolia completed delivery of industrial water infrastructure for Suzano’s Cerrado project in Brazil, the world’s largest single-line eucalyptus pulp mill, backed by an investment of approximately USD 4 billion. The facility relies on advanced process chemical programs engineered to handle wide swings in organic load and color, significantly lowering chemical waste generation and sludge volumes compared with conventional treatment lines. Such projects underscore how blended formulations are becoming integral to industrial water design rather than a downstream add-on.

Operational efficiency gains are further reinforced by digitalization. Strategic data disclosed by Ecolab through its Nalco Water division shows that replacing commodity chemicals with digitally managed blending systems can cut water consumption by up to 15% in high-impact industries. Platforms such as 3D TRASAR™ continuously adjust dosing in real time based on influent quality, helping protect membranes and heat exchangers from fouling while stabilizing treatment performance under fluctuating operating conditions. This marks a decisive move from static dosing to adaptive, data-driven chemical management.

Mainstreaming of Non-Oxidizing and Microbiome-Compatible Biocides

Global tightening of regulations on disinfection by-products is accelerating the shift away from oxidizing biocides such as chlorine and bromine. Compounds linked to trihalomethanes and other regulated by-products are increasingly incompatible with water reuse objectives and stricter discharge limits. As a result, non-oxidizing and microbiome-compatible biocides, including isothiazolinones, quaternary ammonium compounds, mixed peracids, and enzymatic systems, are moving into the mainstream of industrial water treatment.

Regulatory momentum is particularly visible in emerging markets. In January 2025, India’s Ministry of Environment, Forest and Climate Change implemented the Control of Water Pollution Guidelines 2025, tightening discharge norms for high-pollution industries. These rules effectively favor non-oxidizing biocides that enable compliance without residual chlorine odors or secondary carcinogenic by-products, especially where treated water is reused within the plant. Similar regulatory pressures are shaping adoption in aviation, commercial buildings, and large cooling systems.

Commercial-scale deployment is accelerating in cold sanitation and cooling tower applications. Aviation and large commercial facilities are increasingly adopting mixed-peracid and enzymatic biocides that provide effective microbial control while remaining fully biodegradable. These solutions align with evolving EPA Maximum Disinfectant and Disinfection By-Product Rules, which are under review for stricter Total Organic Carbon removal requirements. The result is a clear market signal toward biocides that manage biofilm architecture without compromising environmental or occupational safety standards.

Enabling Water Reuse and Zero Liquid Discharge in Water-Stressed Regions

Water scarcity is transforming zero liquid discharge from a sustainability aspiration into a regulatory mandate across multiple geographies. Regions such as the U.S. Southwest, India, and Northern China now require near-total recycling of industrial process water, creating sustained demand for specialty antiscalants, dispersants, and high-recovery reverse osmosis chemicals that can operate reliably under extreme salinity and concentration conditions.

In India, the Liquid Waste Management Rules 2025 issued by the Central Pollution Control Board have pushed industries in water-stressed states including Gujarat and Maharashtra toward ZLD compliance. This has triggered rapid growth in demand for advanced evaporative chemicals and next-generation antiscalants capable of controlling calcium carbonate and silica scaling in high-brine environments. These chemistries are making modular ZLD systems economically viable even for small and medium enterprises, expanding the addressable market beyond large industrial complexes.

A parallel opportunity is emerging from the global data center expansion. By mid-2025, the AI-driven surge in hyperscale data centers had significantly intensified industrial water demand. In response, Ecolab launched a dedicated 360-degree program for data center cooling that integrates liquid cooling chemistries with water-saving technologies. The initiative positions data centers to operate with dramatically lower water intensity, addressing forecasts of a 56% global water deficit by 2030 while opening a new, high-value end market for advanced process chemicals.

Ultra-High-Purity Chemicals for Semiconductor Fabs and Battery Gigafactories

The rapid build-out of semiconductor fabrication plants and lithium-ion battery gigafactories is creating a specialized, high-margin niche within the process chemicals for water treatment market. These facilities require ultra-high-purity chemicals, often at parts-per-trillion contamination thresholds, to maintain yield and performance in sub-3-nanometer semiconductor nodes and high-energy-density battery chemistries.

In May 2025, Veolia reported securing more than USD 750 million in new flagship contracts, many tied to semiconductor and energy projects. Advanced fabs now specify metal and boron concentrations below 1 to 10 ng/L, necessitating electronic-grade chemicals with purities of 99.999% or higher. Supplying these grades demands tightly controlled manufacturing, packaging, and logistics, elevating barriers to entry and reinforcing the strategic value of established suppliers.

Battery manufacturing is driving a parallel demand stream. The expansion of lithium-ion production in Europe and North America by players such as Tesla, CATL, and Northvolt is accelerating consumption of battery-grade sulfuric acid with purities exceeding 99.9%. While electronic-grade volumes remain dominant, battery-grade demand is rising rapidly as manufacturers seek tighter control over ion exchange and degradation pathways in next-generation cells. This positions ultra-high-purity water treatment and process chemicals as a critical enabler of both digitalization and electrification megatrends.

Process Chemicals for Water Treatment Market Share and Segmentation Insights

Coagulants and Flocculants Lead Water Treatment Chemical Demand for Suspended Solid Removal

Coagulants and flocculants accounted for 32.80% of the Process Chemicals for Water Treatment Market by chemical type in 2025, reflecting their essential role in removing suspended solids, turbidity, and organic contaminants during water clarification processes. These chemicals are widely used in municipal drinking water treatment plants and industrial wastewater treatment facilities to aggregate fine particles into larger flocs that can be removed through sedimentation or filtration. Aluminum salts, iron salts, and polymer-based flocculants remain the primary chemistries used in large-scale water treatment operations. In 2025, advanced coagulation technologies are being optimized to address emerging contaminants, including microplastics, PFAS compounds, and pharmaceutical residues present in drinking water and wastewater streams.

Municipal Water Treatment Sector Drives Demand for Water Treatment Process Chemicals

Municipal water treatment represented 42.80% of the Process Chemicals for Water Treatment Market by end-use industry in 2025, reflecting the essential role of water purification and wastewater treatment infrastructure in urban population centers worldwide. Municipal facilities use a wide range of treatment chemicals including coagulants, disinfectants, corrosion inhibitors, and pH control agents to meet drinking water standards and environmental discharge regulations. Population growth, urbanization, and rising regulatory requirements continue to drive investment in municipal water infrastructure globally. In 2025, aging water infrastructure modernization and treatment plant expansion are increasing demand for advanced water treatment chemicals, particularly specialty formulations used in membrane filtration systems, advanced oxidation processes, and tertiary wastewater treatment technologies.

Process Chemicals for Water Treatment Market Competitive Landscape

The global process chemicals for water treatment market in 2026 is defined by digital-chemical integration, PFAS-free formulations, and decentralized treatment models. Industry leaders are leveraging AI, circular chemistry, and mobile water services to address water scarcity, regulatory compliance, and high-purity demands from AI data centers and industrial sectors.

Kemira Accelerates PFAS-Free Water Treatment Innovation Through AI Integration and Performic Acid Solutions

Kemira is strengthening its leadership in sustainable water treatment chemicals through AI-driven innovation and PFAS-free chemistries. The company reported €2.8 billion in 2025 revenue with a strong 19.1% EBITDA margin, driven by its Water Solutions segment. Its partnership with CuspAI is transforming chemical discovery, particularly for PFAS removal, significantly reducing development timelines. Kemira’s investment in an activated carbon reactivation plant in Sweden enhances its micropollutant removal capabilities. The EPA registration of KemConnect™ DEX, a performic acid-based digital solution, positions it at the forefront of real-time wastewater treatment. This integration of digital intelligence and green chemistry reinforces Kemira’s role in next-generation water purification.

Solenis Expands Global Dominance Through Strategic Acquisitions and Integrated Water Service Platforms

Solenis is rapidly scaling its presence in the water treatment chemicals market through aggressive acquisitions and service integration. The acquisition of NCH Corporation in 2025 expanded its operations to over 160 countries with a workforce of 23,000 employees. Building on its merger with Sigura Water, Solenis now operates 78 manufacturing facilities globally, enhancing its reach across industrial and commercial water segments. Its Solenis 360 platform integrates digital monitoring with chemical solutions, enabling optimized water treatment performance. The company’s diversification into "light water" markets provides resilience against industrial demand fluctuations. This scale and integration strategy positions Solenis as a dominant player in circular water chemistry.

Nalco Water Drives AI Data Center and Lithium Extraction Solutions with Advanced Digital Platforms

Nalco Water is aligning its strategy with the growth of AI infrastructure and the lithium economy, delivering high-purity water treatment solutions. Its ECOLAB3D™ IIoT platform enables predictive maintenance and real-time monitoring for cooling systems in data centers. The acquisition of Ovivo’s ultrapure water business strengthens its presence in semiconductor and pharmaceutical markets. Nalco is also advancing Direct Lithium Extraction technologies, providing critical chemicals for EV battery production. Through its Watermark™ initiative, the company supports Zero Liquid Discharge systems and water reuse strategies. This combination of digital tools and advanced chemistries positions Nalco as a leader in high-tech water treatment solutions.

Kurita Expands Global Footprint and Pioneers Advanced Water Treatment for Industrial and Emerging Applications

Kurita is expanding its global footprint while advancing innovative water treatment solutions under its PSV-27 strategy. The launch of its Mexico subsidiary enhances its ability to deliver localized chemical solutions in water-stressed industrial regions. Its partnership with ispace to develop lunar water treatment systems highlights its commitment to cutting-edge innovation. Kurita’s CSV model integrates chemical supply with digital monitoring to optimize resource efficiency and reduce emissions. The company’s Gemba-driven approach ensures tailored solutions for complex industrial applications. This combination of regional expansion and technological advancement strengthens Kurita’s competitive positioning.

Veolia Leads Circular Water Economy with Mobile Treatment Fleets and PFAS Remediation Technologies

Veolia is reinforcing its leadership in circular water management through its GreenUp strategy and advanced treatment technologies. The establishment of a major service hub in Brazil supports the largest mobile water treatment fleet in Latin America. Its BeyondPFAS platform provides comprehensive solutions for detecting and removing micropollutants using advanced membrane and separation technologies. Veolia is also advancing resource recovery, achieving over 90% capacity at its lithium extraction facility. With over 4,400 patents, the company maintains the largest water technology portfolio globally. Its focus on water reuse and Net Zero Water initiatives positions it as a key player in sustainable water infrastructure.

SNF Strengthens Polymer Leadership with Capacity Expansion and Sustainable Flocculant Innovation

SNF continues to dominate the water-soluble polymer market, focusing on high-performance flocculants and sustainable water treatment solutions. The acquisition of Syensqo’s Oil & Gas division strengthens its presence in energy-related water treatment applications. Its 80% capacity expansion for ADAM monomer enhances production of critical cationic polymers used in flocculation and sludge dewatering. SNF’s EcoVadis Platinum rating highlights its leadership in sustainability and environmental performance. The launch of NATURSOL™ and FLOCARE™ product lines demonstrates innovation in bio-based and high-efficiency formulations. This focus on scale, sustainability, and advanced polymer chemistry reinforces SNF’s global leadership.

United States: PFAS Finality, Semiconductor Purity, and Service-Led Consolidation

The United States market for process chemicals in water treatment is undergoing a decisive structural shift driven by regulatory finality on PFAS, high-purity industrial demand, and consolidation toward outcome-based service models. In September 2025, the U.S. Environmental Protection Agency confirmed the CERCLA hazardous substance designation for PFOA and PFOS, crystallizing compliance obligations across municipal and industrial water systems. This action has accelerated adoption of specialized ion-exchange resins, selective adsorbents, and next-generation flocculants capable of achieving the 4 ppt drinking water threshold by the 2026 spring deadline. Parallel regulatory tightening followed in November 2025, when updated NPDES permitting rules mandated PFAS monitoring for plastics and chemical facilities, increasing demand for polishing-grade treatment chemistries and analytical-support chemicals.

Industrial demand is being reshaped by digital infrastructure and advanced manufacturing. In March 2025, Ecolab through Nalco Water partnered with Digital Realty to deploy AI-driven water conservation systems across 35 U.S. data centers, relying on smart-dosed corrosion inhibitors and biocides to manage extreme thermal loads from AI servers. Consolidation is reinforcing integrated delivery. Solenis completed its acquisition of NCH Corporation in November 2025, expanding Chemicals-as-a-Service offerings for mid-market industrial users. Similarly, Kemira acquired Water Engineering for $150 million in September 2025 to scale boiler and cooling tower formulations. Semiconductor fabs supported by the CHIPS Act began validating sub-10 nm ultrapure water standards in late 2025, sharply increasing demand for TOC reduction chemicals and ultra-clean conditioning agents.

China: Water Reuse Scale-Up and Industrial ZLD Enforcement

China’s process chemicals market is being propelled by water reuse expansion, petrochemical efficiency upgrades, and stricter zero liquid discharge enforcement. In September 2025, the Ministry of Industry and Information Technology released a Work Plan to stabilize the chemical sector, prioritizing energy- and water-saving retrofits for paraxylene and ethylene complexes. These upgrades are directly lifting demand for antiscalants, corrosion inhibitors, and high-performance flocculants optimized for continuous high-load operations. Under the 14th Five-Year Plan, China is on track to add 15 million cubic meters per day of reclaimed water capacity by January 2026, positioning large-scale reverse osmosis systems as a central demand driver for membrane cleaners and biofouling control chemistries.

Environmental compliance is tightening at the industrial park level. Provinces such as Shandong and Jiangsu enforced stricter ZLD mandates in early 2025, requiring advanced sludge conditioners that reduce secondary pollution while improving dewatering efficiency. At the same time, China is constructing 100 low-carbon wastewater treatment plants scheduled for completion during 2025–2026, integrating chemical phosphorus removal with carbon control technologies. Niche demand is also emerging. The 2025–2026 Work Plan accelerates industrial-scale potassium extraction from seawater, creating a specialized market for highly selective precipitation and separation chemicals that operate under high salinity conditions.

India: Decentralized Potable Systems and Long-Term STP Contracting

India’s process chemicals for water treatment market is expanding through a combination of decentralized potable water initiatives and large-scale sewage treatment infrastructure. The Jal Shakti Abhiyan “Catch the Rain” campaign launched in March 2025 targets 148 priority districts, driving demand for coagulants and flocculants suited to modular, rural drinking water treatment units. These systems favor robust chemistries capable of handling variable raw water quality with limited operational oversight. At the same time, urban and river-basin investments are anchoring long-term supply contracts. In August 2025, the Ministry of Jal Shakti completed 15 sewage treatment projects in the Ganga basin valued at ₹3,184 crore under DBOT models, structurally favoring suppliers that can guarantee consistent chemical performance over multi-year operating horizons.

Advanced treatment is becoming standardized. Under Clean Ganga Mission Phase II, Asia’s largest sewage treatment plant in Delhi using A2O technology achieved full chemical optimization by mid-2025, driving sustained demand for nutrient removal chemicals and process stabilizers. Industrial water quality requirements are also tightening. New 2025 audits under FSSAI and the Indian Pharmacopoeia have compelled pharmaceutical manufacturers to adopt higher-purity biocides and pH conditioners to eliminate biofilms in processing lines, elevating specifications for process chemicals used in pharma-grade water systems.

Germany and European Union: Quaternary Treatment and Advanced Oxidation Mandates

Germany and the wider European Union are moving decisively toward advanced water treatment architectures that structurally favor high-value process chemicals. In June 2025, the European Commission launched the European Water Resilience Strategy, mandating removal of microplastics and pharmaceutical residues through advanced oxidation processes. This policy direction is accelerating adoption of ozone-compatible catalysts, peroxide activators, and specialty adsorbents across municipal and industrial facilities. Supply-side investments are responding. In July 2025, Kemira announced a €20 million expansion of Aluminium Chloro Hydrate production in Tarragona, Spain, to meet rising European demand for high-efficiency coagulants.

Regulatory depth is increasing. The late-2025 revision of the Urban Wastewater Treatment Directive requires large plants to implement quaternary treatment stages, structurally expanding the market for polishing chemicals and advanced adsorbents. Preparation for the Marine Strategy Framework targets beginning in 2027 has already influenced chemical selection in industrial runoff management, with stricter limits on persistent pollutants shaping dispersant and conditioner formulations. Germany’s market role is therefore defined by regulatory-driven sophistication rather than volume growth.

Japan: AI-Dosed Industrial Systems and Semiconductor Ultrapurity

Japan’s process chemicals market is increasingly anchored in digital dosing and semiconductor-grade water purity. In December 2025, Kurita Water Industries announced the scale-up of its S.sensing IoT platform, enabling AI-driven chemical dosing across a majority of industrial accounts by fiscal year 2027. This transition is shifting value toward precision formulations that perform reliably under autonomous control, reducing chemical waste while maintaining system stability.

Semiconductor manufacturing is reinforcing demand for ultra-high-purity chemicals. In late 2025, Kurita was shortlisted to supply multiple advanced fabs in Japan with UHP chemical consumables for ultrapure water generation, resist residue control, and advanced packaging processes. These applications require extremely low ionic contamination and consistent TOC suppression, positioning Japan as a premium market where chemical performance tolerance is exceptionally narrow.

Comparative Overview of Country-Level Dynamics in Process Chemicals for Water Treatment

Process Chemicals For Water Treatment Market County Level Snapshot

|

Region

|

Primary 2025–2026 Drivers

|

Structural Impact on Process Chemicals

|

|

United States

|

PFAS finality, CHIPS Act fabs, consolidation

|

Shift to high-selectivity and service-led chemistries

|

|

China

|

Water reuse expansion, ZLD enforcement

|

Scale-driven demand for RO and sludge-conditioning chemicals

|

|

India

|

Rural potable systems, DBOT STPs

|

Long-term contracts for robust coagulants and nutrients

|

|

Germany / EU

|

AOP mandates, quaternary treatment

|

Growth in advanced oxidation and polishing chemicals

|

|

Japan

|

AI dosing, semiconductor UPW

|

Premium demand for ultra-high-purity formulations

|

Process Chemicals For Water Treatment Market Report Scope

Process Chemicals For Water Treatment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.8 Billion

|

|

Market Size (2034)

|

$55.7 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Chemical Type (Coagulants & Flocculants, Corrosion & Scale Inhibitors, Biocides & Disinfectants, pH Conditioners & Softeners, Antifoaming Agents, Specific Pollutant Removers), By Application Process (Raw Water Pre-Treatment, Boiler & Cooling Water Treatment, Wastewater & Sewage Treatment, Desalination & Membrane Care, Ultrapure Water Production), By End-Use Industry (Municipal Water Treatment, Power Generation, Semiconductor & Electronics, Oil & Gas & Mining, Food & Beverage, Chemical & Pharmaceutical Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab, Solenis, Kemira Oyj, Kurita Water Industries Ltd., Veolia Water Technologies, Suez SA, BASF SE, Dow Inc., SNF Group, Akzo Nobel NV, Buckman Laboratories International, Thermax Limited, Feralco AB, Avista Technologies, Shandong Taihe Water Treatment

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Process Chemicals for Water Treatment Market Segmentation

By Chemical Type

- Coagulants & Flocculants

- Corrosion & Scale Inhibitors

- Biocides & Disinfectants

- pH Conditioners & Softeners

- Antifoaming Agents

- Specific Pollutant Removers

By Application Process

- Raw Water Pre-Treatment

- Boiler & Cooling Water Treatment

- Wastewater & Sewage Treatment

- Desalination & Membrane Care

- Ultrapure Water Production

By End-Use Industry

- Municipal Water Treatment

- Power Generation

- Semiconductor & Electronics

- Oil & Gas & Mining

- Food & Beverage

- Chemical & Pharmaceutical Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Process Chemicals for Water Treatment Industry

- Ecolab

- Solenis

- Kemira Oyj

- Kurita Water Industries Ltd.

- Veolia Water Technologies

- Suez SA

- BASF SE

- Dow Inc.

- SNF Group

- Akzo Nobel NV

- Buckman Laboratories International

- Thermax Limited

- Feralco AB

- Avista Technologies

- Shandong Taihe Water Treatment

*- List not Exhaustive