Market Overview: Meat Sector Dominance and Round-Bottom Bag Preference

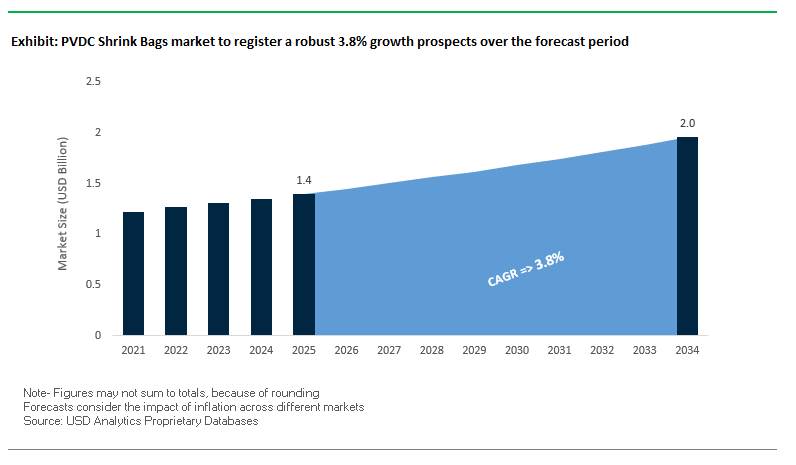

The global PVDC shrink bags market is projected to grow from USD 1.4 billion in 2025 to USD 2 billion by 2034, registering a CAGR of 3.8%. The demand for PVDC shrink bags is strongly driven by the meat, poultry, and seafood industries, where extended shelf life, food safety, and product appeal are critical. These bags are favored for their superior oxygen and moisture barrier properties, which help preserve freshness and reduce food waste in both retail and e-commerce channels.

Among product types, round-bottom PVDC shrink bags dominate the market, widely used for packaging hams, turkeys, and large cheese blocks. Their seamless design reduces puncture risk while offering a smooth, wrinkle-free appearance that improves visual merchandising. Additionally, PVDC shrink bags are valued for their optical clarity, gloss, and puncture resistance, features that enhance shelf presentation and durability during distribution. The rise of online grocery and direct-to-consumer models is also accelerating the use of high-barrier shrink packaging, as companies seek reliable formats that withstand transportation while maintaining food integrity.

Key Insights for Industry Professionals:

- Meat, poultry, and seafood account for the largest consumption share.

- Round-bottom shrink bags dominate due to puncture resistance and product aesthetics.

- High clarity and gloss boost product appeal in retail settings.

- E-commerce growth fuels demand for high-performance packaging solutions.

Market Analysis: Recent Industry Developments Shaping the Sector

The PVDC shrink bags market is undergoing rapid evolution through material innovation, acquisitions, and expansions aimed at sustainability and efficiency.

In August 2025, Syntegon introduced Amplified Heat Sealing (AHS) technology at PACK EXPO, enabling tighter seals compatible with sustainable mono-materials. While not directly PVDC-based, such innovations are influencing the entire barrier packaging ecosystem. Similarly, in July 2025, ProAmpac launched recyclable high-barrier fiber-based technology, reflecting the industry’s ongoing search for PVDC-free and recyclable alternatives.

Consolidation continues to play a key role. In May 2025, Amcor completed its USD 8.4 billion acquisition of Berry Global, expanding its reach in high-barrier films, including shrink bags. Meanwhile, Buergofol introduced 100% recyclable barrier films in November 2024, highlighting the growing shift toward non-PVDC solutions in meat and dairy packaging.

Product expansion remains strong. Amcor launched a 40µm PVDC-free PrimeSeal shrink bag in September 2024, designed to enhance recyclability while maintaining barrier strength. A month earlier, in July 2024, Amcor also expanded its UK production line for PrimeSeal, boosting capacity for Europe’s meat packaging industry. Other innovators include Asahi Kasei, which formed a strategic partnership in June 2024 to advance barrier packaging technology, and Adapa Group, which unveiled two new shrink bag product lines in May 2024 at its St. Helens plant, strengthening its commitment to high-performance food packaging.

Emerging Trends and Opportunities Reshaping the PVDC Shrink Bags Market

Strategic Retention in High-Value Protein Packaging Amidst Broader Material Substitution

While the broader packaging industry is steadily transitioning toward recyclable mono-material structures, PVDC shrink bags continue to hold strategic importance in high-value protein packaging applications. Their unmatched barrier properties against oxygen and moisture make them indispensable in segments such as premium cured meats and specialty cheeses, where maintaining flavor, aroma, and texture is critical. According to USDA data, rising poultry consumption and exports are further fueling demand for durable and high-performance packaging solutions. Unlike alternative substrates, PVDC shrink bags ensure extended shelf life, reducing food waste and safeguarding product quality across long and complex cold chains. This strategic retention underscores PVDC’s resilience, even as material substitution gains momentum in other packaging categories.

Increased Scrutiny and Investment in Closed-Loop Recycling and Chemical Recovery Technologies

The sustainability profile of PVDC shrink bags remains under scrutiny, driving major producers to invest in recycling and chemical recovery solutions. Instead of arguing for curbside recyclability, industry players are focusing on advanced recovery systems. Syensqo’s 2025 initiative proved that multi-layer PVDC structures could be mechanically recycled with polyethylene, reusing the material in non-food items. Meanwhile, Solvay’s proof-of-concept for PVDC chemical recycling shows potential to reintegrate polymers without losing high-barrier performance. Emerging technologies, such as Halocycle’s microwave-based chlorine plastic recycling, are pioneering circular economy pathways. Collectively, these developments signal a market shift from defensive positioning to proactive investment, ensuring PVDC can sustain its role in critical applications while aligning with global circularity goals.

Development of High-Barrier, Recyclable Alternative Coatings for PVDC Replacement

One of the most significant opportunities lies in the commercialization of recyclable high-barrier coatings that can rival PVDC’s performance while aligning with global recycling mandates. Bio-based innovations like Melodea’s MelOx Ngen provide recyclable barrier coatings for PE films, addressing food freshness and compliance with circular economy standards. Collaborative efforts from ExxonMobil, Kuraray, and Alico demonstrate how fully recyclable PE-based shrink bags can maintain barrier performance without relying on PVDC. Additionally, paper-based alternatives such as Sappi’s AvantGuard are proving that fiber substrates can integrate high-barrier performance with recyclability. These developments create a compelling pathway for brands under regulatory and consumer pressure to adopt next-generation PVDC alternatives that combine sustainability with product protection.

Expansion into High-Growth Emerging Markets for Protein Packaging

Emerging markets present a major growth vector for PVDC shrink bags in protein packaging. The rapid expansion of cold chain infrastructure, rising supermarket penetration, and changing dietary preferences toward processed protein products are driving packaging demand across Asia-Pacific, Latin America, and parts of Africa. In these regions, Western-style retail presentation and longer shelf-life packaging are becoming consumer expectations. PVDC shrink bags provide superior protection in meat, poultry, and cheese segments, ensuring products remain fresh throughout distribution. Moreover, with recycling infrastructure still under development in many of these economies, the performance benefits of PVDC outweigh recyclability concerns, offering suppliers a near-term advantage. This makes emerging markets a prime target for both global and regional packaging companies looking to expand their footprint in high-value protein segments.

Competitive Landscape: Leading Players in PVDC Shrink Bags Industry

The global PVDC shrink bags market is moderately consolidated, with leading packaging companies driving innovation in barrier performance, sustainability, and food safety.

Sealed Air Corporation: Strengthening Market Leadership with Cryovac Brand

Sealed Air dominates the PVDC shrink bag market through its Cryovac brand, widely used for meat, poultry, and cheese. The brand is recognized for its oxygen and moisture barrier performance, puncture resistance, and high-gloss finish. The company continuously invests in advanced printing technologies, allowing brands to leverage customized designs and superior visual appeal. Its expertise in food science and shelf-life extension remains a core differentiator, keeping Sealed Air at the forefront of food packaging innovation.

Amcor plc: Expanding with Sustainable Shrink Bag Solutions

Amcor has built a strong presence in the shrink bag segment, particularly with its PrimeSeal series, designed for meat packaging. In September 2024, the company launched a PVDC-free 40µm shrink bag, a step toward offering sustainable solutions without compromising quality. Its new Swansea production line (July 2024) expanded capacity to meet growing European demand. With its May 2025 acquisition of Berry Global, Amcor significantly broadened its flexible packaging portfolio, reinforcing its role as a leader in both PVDC and next-generation shrink bag innovations.

Winpak Ltd.: Focusing on North American Meat and Dairy Packaging

Winpak has established itself as a specialist in high-barrier flexible packaging, with a strong focus on shrink bags for mid-sized meat and cheese processors. Its strength lies in providing tailored, high-quality packaging solutions backed by technical expertise in the North American market. Recently, Winpak invested in fully recyclable shrink bags, responding to growing sustainability requirements from retail and foodservice clients. Its portfolio covers both processed and fresh protein sectors, ensuring reliable performance across demanding supply chains.

Schur Flexibles Holding GesmbH: Innovating with Patented PVDC Formulations

Schur Flexibles is a European leader in barrier packaging, with shrink bags forming a critical part of its portfolio. In recent years, it obtained a patent for improved PVDC formulations, strengthening its position in the premium meat and dairy segments. The company emphasizes sustainability and recyclability, working on next-gen shrink bags with lower environmental impact. Its extensive European footprint and customer-focused solutions allow it to provide specialized products across food, pharma, and personal care industries.

PREMIUMPACK GmbH: Niche Expertise in Meat and Cheese Packaging

PREMIUMPACK is a specialist manufacturer of high-barrier shrink bags, with a focus on meat and cheese packaging industries. Its products are valued for exceptional oxygen and moisture barrier protection, aroma retention, and optical clarity. Unlike diversified competitors, PREMIUMPACK follows a niche strategy, emphasizing consistent product quality and reliability for its clients. By concentrating on core strengths and maintaining a narrow but specialized portfolio, the company has built strong trust among food producers that prioritize durability and shelf-life performance.

PVDC Shrink Bags Market Share Insights

Straight Bottom Sealed Bags Dominate PVDC Shrink Bags Market Share by Bag Type

Straight bottom sealed shrink bags account for 45% of the PVDC shrink bags market, making them the dominant format due to their versatility, high-speed machine compatibility, and efficient material usage. Their flat base provides stable standing and consistent pack presentation, which is particularly important in automated packaging lines for cheese blocks, meat loaves, and large cuts of processed meat. Round bottom sealed bags follow as the premium solution for whole-muscle meat and poultry, enhancing retail display with wrinkle-free, second-skin aesthetics. Side-sealed bags, though smaller in share, support high-speed applications for portion-controlled items, while the “other” segment caters to custom designs for specialty products like seafood or artisan cheeses. The strong performance of straight bottom sealed bags highlights their dual role in delivering operational efficiency to processors and extending product shelf life through PVDC’s unmatched barrier properties.

Processed Meat Leads PVDC Shrink Bags Market Share by Application

Processed meat holds the largest share at 30% of PVDC shrink bag applications, underscoring the irreplaceable role of PVDC films in shelf-life extension and color preservation for sausages, salami, and cured meats. The material’s ability to prevent oxidation and moisture loss ensures consistent quality and consumer appeal, making it the standard across global meat processing industries. Fresh meat and poultry combined hold nearly half of the market, with PVDC enabling the critical control of oxygen transmission rates that maintain the bright red “bloom” consumers associate with freshness. Cheese follows as a high-value growth segment, where PVDC blocks mold growth and preserves texture, flavor, and appearance in retail-ready and specialty cheese products. Seafood remains a smaller yet high-stakes application, relying on PVDC to protect delicate proteins from oxidation and freezer burn. This segmentation clearly reflects PVDC shrink bags’ concentration in protein and dairy categories, where their unique barrier capabilities translate directly into extended shelf life, reduced waste, and higher retail margins.

United States: High-Barrier PVDC Shrink Bags Driving Food Safety and Sustainability

The U.S. PVDC shrink bags market is being propelled by evolving consumer preferences for fresh and processed meat, poultry, seafood, and other perishable products requiring extended shelf life. PVDC bags are highly valued for their exceptional oxygen and moisture barrier properties, which preserve food quality and safety, making them a preferred choice for food manufacturers and distributors.

Technological advancements are central to market growth, with companies investing in high-speed, fully integrated automation systems that maximize throughput and ensure consistent product quality. Sustainability is also a strong growth driver, as manufacturers are introducing PVDC-free, recyclable, biodegradable, and compostable alternatives, exemplified by Amcor’s new sustainable shrink bag range. Regulatory frameworks from the FDA further reinforce the adoption of food-safe, high-barrier packaging solutions, while strategic acquisitions by Winpak and Sealed Air Corporation expand distribution networks and portfolio offerings for premium applications.

Germany: Circular Economy Leadership and PVDC-Free Innovations Accelerating Market Demand

Germany’s PVDC shrink bags market is shaped by a stringent regulatory environment, including the EU Packaging and Packaging Waste Regulation (PPWR) and a single-use plastics levy effective from 2024, incentivizing sustainable packaging adoption. The market emphasizes circular economy principles, encouraging the development of recyclable and high-recycled-content shrink bags that comply with national and EU sustainability targets.

Technological advancements are also prominent, with innovations such as the adapa Group’s VACUshrinkʳᵉ MEX 55, a fully recyclable shrink bag free from PVDC, aligning with EU regulations and evolving consumer preferences. These initiatives, combined with governmental mandates on waste reduction and improved recyclability, are accelerating the shift toward eco-friendly, high-performance shrink packaging solutions in Germany.

China: Industrial Growth and High-Efficiency Automation Fuel PVDC Shrink Bag Demand

China’s PVDC shrink bags market is heavily driven by rapid industrialization and expanding manufacturing activities in the food, e-commerce, and logistics sectors. The country is investing in automation and AI technologies, including robotics for packaging lines, to improve production efficiency and product consistency.

Sustainability initiatives are also shaping the market, driven by China’s dual carbon goals for carbon peak and neutrality. Regulations now require packaging companies to prioritize eco-friendly, reusable, and reduced-material solutions, creating opportunities for innovative shrink bag designs that combine high-barrier performance with environmental responsibility.

India: Food Safety Regulations and Evolving Sustainability Trends Boost Market Growth

In India, PVDC shrink bags are increasingly adopted due to governmental sustainability measures, including the Plastic Waste Management (Amendment) Rules, which encourage eco-friendly and reusable alternatives. The rapid growth of food processing, ready-to-eat products, and bakery sectors is a primary catalyst, as manufacturers seek hygienic, lightweight, and durable packaging for meat, poultry, and other perishable products.

Food safety regulations from the Food Safety and Standards Authority of India (FSSAI) are driving demand for high-barrier films, ensuring product quality and compliance with industry standards. Combined with sustainability-focused initiatives, these trends are positioning India as a fast-growing market for PVDC shrink bags and high-performance packaging solutions.

Brazil: Regulatory Push and Technological Innovation Enhancing Sustainable Packaging

Brazil’s PVDC shrink bags market is being shaped by stringent legislation restricting single-use plastics, including the National Solid Waste Policy, which promotes a circular economy. This is propelling a shift toward reusable, durable, and environmentally responsible shrink bags.

Technological advancements such as robotics and AI are improving production efficiency and quality control, enabling automated sorting, defect detection, and precise application of high-barrier films. Sustainability remains a core focus, as highlighted by WWF-Brazil’s research advocating a move from disposable plastics to materials like paper and recyclable polymers, positioning the country as a key adopter of innovative and eco-friendly shrink bag solutions.

Japan: Advanced Recycling and High-Performance Materials Driving Market Innovation

Japan’s PVDC shrink bags industry benefits from one of the world’s highest waste plastic and paper collection and utilization rates, supported by the Plastic Resource Circulation Act, fostering circular packaging practices. The market is increasingly adopting bio-based materials, including bio-polypropylene (bio-PP), for sustainable food and pharmaceutical packaging applications.

Innovation is central, with companies like Toray Industries leading in high-performance films and packaging equipment. Academic research is also advancing the market, exemplified by Yamagata University’s development of printable, UV-densified barrier films with glass-like performance, enhancing product protection and shelf life. These developments position Japan as a global leader in functional, eco-friendly, and technologically advanced PVDC shrink bag solutions.

PVDC Shrink Bags Market Report Scope

PVDC Shrink Bags market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$2 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Bag Type (Round Bottom Sealed Shrink Bags, Straight Bottom Sealed Shrink Bags, Side Sealed Shrink Bags, Other Bag Types), By Application (Fresh Meat, Processed Meat, Poultry, Seafood, Cheese, Other Applications), By Barrier Type (High Barrier, Medium Barrier, Low Barrier)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Amcor plc, Bemban S.A., Winpak Ltd., Schur Flexibles Group, The Dow Chemical Company, Kureha Corporation, Krehalon B.V., Sevac S.R.O., Adapa Group, PACCOR, Flexi-Pack Ltd., Viscofan S.A., Sealed Air Corporation, VC999 Packaging Systems

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PVDC Shrink Bags Market Segmentation

By Bag Type

- Round Bottom Sealed Shrink Bags

- Straight Bottom Sealed Shrink Bags

- Side Sealed Shrink Bags

- Other Bag Types

By Application

- Fresh Meat

- Processed Meat

- Poultry

- Seafood

- Cheese

- Other Applications

By Barrier Type

- High Barrier

- Medium Barrier

- Low Barrier

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in PVDC Shrink Bags Market

- Sealed Air Corporation

- Amcor plc

- Bemban S.A.

- Winpak Ltd.

- Schur Flexibles Group

- The Dow Chemical Company

- Kureha Corporation

- Krehalon B.V.

- Sevac S.R.O.

- Adapa Group

- PACCOR

- Flexi-Pack Ltd.

- Viscofan S.A.

- Sealed Air Corporation

- VC999 Packaging Systems

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global PVDC shrink bags market, providing an in-depth examination of market breakthroughs, technological innovations, and evolving consumer and regulatory demands across the food packaging sector. The analysis reviews the critical role of PVDC shrink bags in preserving freshness, extending shelf life, and enhancing visual appeal in meat, poultry, seafood, and cheese applications, while also highlighting recent advances in high-barrier, recyclable alternatives. This report emphasizes sustainability trends, including chemical and mechanical recycling solutions, and explores the rise of PVDC-free coatings and mono-material substitutes designed to meet circular economy goals. Additionally, competitive developments such as acquisitions, capacity expansions, and strategic partnerships are assessed to provide a holistic view of market dynamics. This report is an essential resource for industry professionals seeking actionable insights on product development, regulatory compliance, and growth strategies in high-performance protein packaging.

Scope Highlights:

- Segmentation: By Bag Type (Round Bottom Sealed Shrink Bags, Straight Bottom Sealed Shrink Bags, Side Sealed Shrink Bags, Other Bag Types), By Application (Fresh Meat, Processed Meat, Poultry, Seafood, Cheese, Other Applications), By Barrier Type (High Barrier, Medium Barrier, Low Barrier)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ leading companies, including Sealed Air Corporation, Amcor plc, Winpak Ltd., Schur Flexibles, The Dow Chemical Company, Kureha Corporation, and PACCOR

Methodology

USDAnalytics employed a comprehensive research methodology combining primary and secondary sources to provide accurate market insights. Primary research included structured interviews and discussions with packaging manufacturers, meat processors, distributors, and end-users to understand product performance, operational challenges, and adoption trends. Secondary research drew on corporate reports, patent filings, trade publications, regulatory guidelines, and sustainability initiatives to validate historical data and forecast market growth. Quantitative models estimated market size, share, and growth across bag types, applications, and barrier levels, while qualitative assessment examined competitive strategies, material innovations, and regional dynamics. This approach ensures reliable insights into the evolving PVDC shrink bags market, guiding strategic decisions for packaging, manufacturing, and investment stakeholders.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.