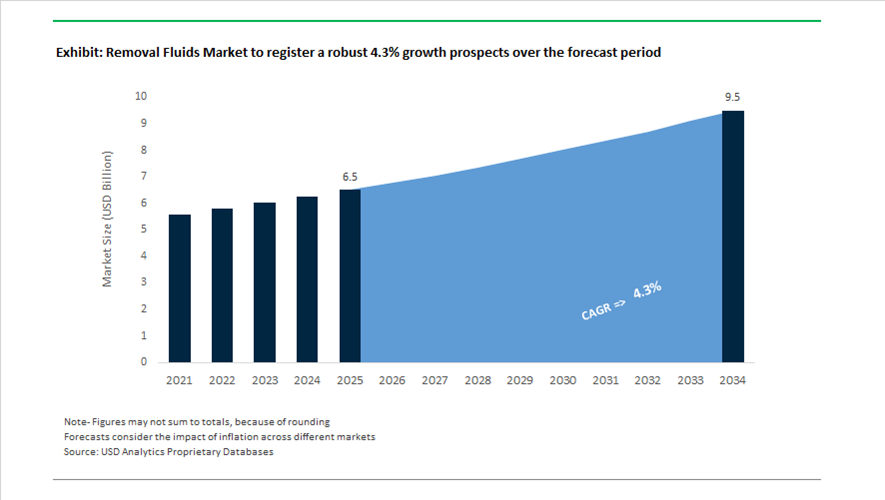

Removal Fluids Market Valued at $6.5 Billion in 2025, Projected to Reach $9.5 Billion by 2034 at 4.3% CAGR

The global removal fluids market is valued at $6.5 billion in 2025 and is projected to reach $9.5 billion by 2034, expanding at a CAGR of 4.3%. Demand is driven by increasing use of metal removal fluids, semi-synthetic coolants, high-speed CNC machining fluids, paint stripping chemicals, biodegradable solvent removers, aerospace-grade machining lubricants, and low-VOC industrial stripping solutions. Growth in aerospace alloys, EV battery manufacturing, infrastructure refurbishment, and precision machining is reinforcing the need for advanced cooling, lubrication, and environmentally compliant removal chemistries. Manufacturers are prioritizing thermal stability, corrosion resistance, extended sump life, and regulatory-safe formulations in response to tightening environmental standards.

Industrial innovation accelerated in 2024 and 2025. In June 2024, Master Fluid Solutions introduced TRIM SC417, a semi-synthetic coolant engineered for ferrous metal removal, delivering enhanced rust protection and low-foam performance in soft water environments. In February 2024, LANXESS expanded its distribution partnership with Palmer Holland to cover its full portfolio of metalworking removal fluids and industrial preservatives across North America, strengthening regional channel reach. Throughout 2024, SKF and Quaker Houghton advanced their circular oil collaboration, promoting regeneration and reuse of industrial removal fluids to align with net-zero manufacturing targets. In September 2025, ExxonMobil launched a new synthetic metalworking removal fluid range tailored for high-speed CNC machining of titanium and nickel alloys, addressing extreme thermal loads common in aerospace and defense applications. In late 2025, Quaker Houghton introduced a Digital Fluid Optimization Platform using real-time sensors and AI-driven analytics to monitor fluid concentration and health, significantly extending sump life and reducing chemical waste in large-scale manufacturing environments.

Sustainability and regulatory compliance are central to formulation strategy. In March 2025, Rust-Oleum launched a gel-based paint removal fluid designed for vertical surfaces, targeting residential and light-commercial users with no-drip, safety-focused formulations. In April 2025, 3M introduced a low-odor, biodegradable solvent-based paint remover engineered to comply with evolving global VOC regulations while maintaining industrial-grade stripping efficiency. In January 2025, AkzoNobel partnered with a major Asia-Pacific construction firm to test low-emission paint removal technologies for green building compliance. In February 2025, Henkel expanded its R&D center in Germany to accelerate development of non-toxic, non-CMR stripping technologies aligned with updated EU REACH directives.

Capacity expansion and strategic alignment continue into 2026. FUCHS completed a 40% capacity increase at its South African facility in late 2024, securing two major automotive OEM contracts in early 2025 to support regional manufacturing growth. In October 2025, Quaker Houghton announced executive appointments to advance its Enterprise Growth Strategy, emphasizing differentiated removal fluids for EV battery and aerospace sectors.

The removal fluids market is increasingly characterized by high-performance synthetic metalworking coolants, AI-optimized fluid management systems, biodegradable paint removers, low-VOC stripping agents, non-CMR compliant chemistries, circular oil regeneration models, and aerospace-grade machining lubricants. As advanced manufacturing and green infrastructure standards evolve, removal fluid innovation remains critical to productivity, regulatory compliance, and sustainable industrial operations.

Key Trends and Monetizable Opportunities in the Removal Fluids Market

Precision Machining Drives Adoption of High-Performance Synthetic Removal Fluids

The removal fluids market is being structurally reshaped by the increasing complexity of precision machining across aerospace, medical devices, and high-value industrial manufacturing. As machining tolerances tighten and cutting speeds increase, traditional mineral-based fluids are proving insufficient. Manufacturers are rapidly shifting toward low-viscosity, high-thermal-stability synthetic and semi-synthetic removal fluids engineered to manage extreme heat loads and prevent surface contamination during machining of difficult-to-cut alloys such as titanium (Ti-6Al-4V), Inconel, and cobalt-chrome.

Aerospace manufacturing has emerged as a critical demand driver. In 2024, major aircraft OEMs reinforced residue-free machining requirements to mitigate risks such as hydrogen embrittlement and surface micro-cracking in structural components. These mandates have accelerated the replacement of conventional emulsions with next-generation synthetic fluids that exhibit minimal misting, enhanced cooling efficiency, and superior chip evacuation. Industry performance data from 2024–2025 show that advanced synthetic formulations can extend tool life by double-digit percentages while simultaneously improving workplace air quality, a growing regulatory and ESG consideration.

In parallel, medical device manufacturing is amplifying demand for zero-residue removal fluids. Micromachining of surgical instruments, orthopedic implants, and minimally invasive devices now requires fluids that leave no ionic or organic residues, eliminating the need for secondary solvent cleaning. By 2025, industry benchmarks indicate that manufacturers adopting ultra-clean grinding and removal fluids have reduced post-processing time by approximately 12%, directly improving throughput and regulatory compliance under tightening FDA and EU MDR scrutiny.

Lifecycle Management and Fluid-as-a-Service Models Gain Industrial Traction

A second defining trend in the removal fluids market is the transition from transactional product sales to lifecycle-based service models. Rising disposal costs, stricter wastewater regulations, and sustainability targets are pushing manufacturers toward closed-loop fluid management systems that optimize usage, extend fluid life, and minimize environmental impact.

Leading suppliers are increasingly offering Fluid-as-a-Service platforms that integrate automated dosing, real-time condition monitoring, and on-site recycling. By 2024, multi-year service contracts covering global manufacturing footprints had become common in aerospace and automotive supply chains. These programs leverage AI-enabled analytics to maintain optimal fluid concentration, detect contamination early, and schedule regeneration before performance degradation occurs. Operational data from early adopters show that closed-loop systems can reduce total fluid waste by up to 40% while lowering unplanned downtime linked to fluid failure.

Regulatory pressure is reinforcing this shift. Updates to EU REACH and the Paints Directive in late 2024 have accelerated the phase-out of poorly biodegradable solvents, particularly in Europe. In response, suppliers are rapidly expanding portfolios of bio-based and readily biodegradable removal fluids that meet stringent ecological standards without sacrificing lubricity or thermal stability. This convergence of compliance, cost control, and sustainability is redefining removal fluids as managed assets rather than consumables.

Post-Processing Solutions for Metal Additive Manufacturing

Metal additive manufacturing is creating a structurally new demand segment for the removal fluids market. As 3D printing scales from prototyping to serial production, post-processing has emerged as a critical bottleneck. Complex lattice geometries, internal channels, and reactive metal powders require specialized removal fluids capable of penetrating confined spaces without inducing corrosion or dimensional distortion.

By late 2025, semi-automated post-processing systems such as dry-ice blasting and hybrid solvent-assisted cleaning were gaining traction as alternatives to labor-intensive manual methods. These technologies require highly specialized fluids that can safely interact with powder bed fusion components made from aluminum, titanium, and nickel alloys. At the same time, auxiliary energy-assisted cleaning approaches using thermal or acoustic fields are enhancing fluid penetration into internal structures. This has opened a premium opportunity for high-penetration, low-surface-tension chemistries tailored specifically for additive manufacturing workflows, where reliability and repeatability directly influence part certification.

Ultra-High-Purity Removal Fluids for Semiconductor Fabrication

The semiconductor industry represents the most technically demanding and highest-margin opportunity for removal fluids. Advanced node manufacturing requires ultra-high-purity chemicals for photoresist stripping, post-etch cleaning, and post-CMP processes, where even trace contamination can compromise yield.

In 2025, renewed global investment in semiconductor fabrication intensified demand for semiconductor-grade removal fluids with impurity levels measured in parts per trillion. High-purity acids and specialty cleaning chemistries are becoming strategic enablers of advanced AI, automotive, and communications chips. Capital investments in new fabrication facilities are increasingly paired with dedicated on-site chemical purification and water recycling infrastructure, reflecting the critical role of removal fluids in overall fab economics.

Water reuse has become inseparable from removal fluid strategy in microelectronics. Facilities commissioned in 2025 are designed to recycle thousands of cubic meters of ultrapure process water per day, integrating removal fluid management with wastewater treatment and reuse. For suppliers, this creates an opportunity to move beyond product supply into long-term partnerships centered on chemical purity assurance, water efficiency, and yield protection.

Removal Fluids Market Share and Segmentation Insights

Water-Based Removal Fluids Lead Market Adoption as Aqueous Cleaning Technologies Advance

Water-based fluids accounted for 48.60% of the removal fluids market in 2025, establishing them as the dominant product category across industrial maintenance and process cleaning operations. Their leadership is driven by strong environmental compliance, improved worker safety, and cost-effective large-scale deployment in sectors such as industrial cleaning, oil and gas displacement, and maintenance operations. Regulatory pressure to reduce hazardous solvent usage has accelerated the shift toward aqueous removal fluid formulations. A major 2025 innovation trend is the advancement of next-generation aqueous cleaning technologies, incorporating advanced surfactant systems, nano-emulsion chemistry, and optimized pH regulators. These improvements enable water-based formulations to remove heavy oils, cured coatings, and persistent industrial deposits, expanding their application range beyond traditional cleaning systems.

Oil & Gas Displacement Drives Large-Volume Consumption Across Pipeline Operations

Oil and gas displacement represents the largest application segment in the removal fluids market, accounting for 34.80% of total demand in 2025 due to the extensive scale of global pipeline infrastructure. Removal fluids are widely used during pipeline commissioning, hydrostatic testing, dewatering operations, and product displacement procedures across upstream and midstream energy systems. These operations require significant fluid volumes to ensure pipeline integrity and efficient transition between transported products. A key 2025 industry driver is the increasing requirement for environmentally acceptable removal fluids in pipeline operations located in environmentally sensitive regions. Operators increasingly specify biodegradable, non-toxic, and non-bioaccumulative fluid formulations that comply with regulatory frameworks such as OSPAR and EPA guidelines for discharge or incidental environmental exposure.

Removal Fluids Market Competitive Landscape

The 2026 removal fluids market is transitioning toward PFAS-free, low-VOC formulations, bio-based esters, and closed-loop cleaning systems. Growth is driven by regulatory enforcement, semiconductor and EV demand, and advanced aqueous and vapor degreasing technologies for high-precision industrial applications.

3M transitions to PFAS-free removal fluids with clean tech portfolio and electronic-grade innovation

3M Company is redefining the removal fluids market through a complete exit from PFAS-based chemistry, eliminating fluorinated solvents across its portfolio by the end of 2025. This shift impacts approximately $1.3 billion in annual sales while strengthening compliance with global environmental regulations. The company has reformulated nearly 7,000 products using advanced polymer systems that maintain stripping efficiency without fluorinated additives. Focus on electronic-grade cleaning fluids and thermal management liquids supports semiconductor and data center applications. 2026 guidance targets adjusted EPS of $8.50–$8.70 with 3% organic growth driven by next-generation materials. Emphasis on PTFE-free solutions aligns with demand for sustainable precision cleaning technologies.

Huntsman strengthens amine-based removal fluids portfolio with cost optimization and semiconductor demand growth

Huntsman Corporation is expanding its presence in removal fluids through specialty amines and carbonate-based formulations targeting high-efficiency stripping and cleaning. The Performance Products segment reported $16 million EBITDA in Q4 2025 with improved cost structure following facility rationalization. Demand growth in semiconductor and fuels applications supports increased adoption of amine-based precision cleaning fluids. Ongoing cost-reduction initiatives, with 80% workforce adjustments completed, enhance competitiveness against low-cost producers. Q1 2026 EBITDA is projected between $20 million and $30 million, supported by recovery in coatings and adhesives demand. Focus on performance amines strengthens positioning in high-spec industrial cleaning markets.

BASF advances low-emission removal fluids through integrated Verbund production and green transformation strategy

BASF SE is strengthening its removal fluids portfolio through integrated production and sustainability-driven innovation within its Industrial Solutions segment. The Zhanjiang Verbund site supports localized manufacturing of intermediates used in next-generation low-VOC industrial cleaners. Reorganization of catalyst and refining operations enhances supply chain efficiency for high-performance process fluids. The company reported €6.6 billion EBITDA in 2025 and expects improved earnings in 2026 driven by specialty additives demand. Renewable energy integration supports reduction of CO2 emissions toward the 17.2–18.2 million metric ton target. Focus on label-friendly solvent systems aligns with regulatory requirements in Europe and Asia.

Eastman expands circular removal fluids with methanolysis technology and bio-based solvent innovation

Eastman Chemical Company is advancing sustainable removal fluids through molecular recycling and bio-based solvent development. Its Kingsport methanolysis facility exceeded targets by producing 2.5 times more recycled content in 2025, generating $60 million in incremental earnings. Cost-reduction initiatives targeting up to $250 million support margin stability in the Chemical Intermediates segment. Cellulose-based innovations such as Naia™ Lyte are being leveraged to develop eco-friendly removal fluids for textile and packaging industries. Strong operating cash flow of nearly $1 billion supports continued expansion of recycling platforms. Focus on circular feedstocks enhances sustainability and performance of industrial cleaning solutions.

Arkema drives advanced removal fluids for battery recycling and high-performance material processing

Arkema is expanding its role in removal fluids through specialty solutions supporting battery recycling and advanced material processing. New technologies enable safe disassembly of battery components without damaging adjacent cells, addressing EV recycling challenges. Integration with bio-based materials such as Rilsan® Polyamide 11 supports efficient stripping and recovery processes. Launch of Zenimid™ polyimides and expansion of Kynar® PVDF capacity drive demand for high-purity cleaning fluids in semiconductor and energy applications. Strategic focus on bond-breaking technologies supports repair and recycling of composite materials. Emphasis on sustainable processing fluids aligns with circular economy objectives.

Dow strengthens industrial removal fluids portfolio with AI-driven efficiency and carbon capture integration

Dow Inc. is enhancing its removal fluids portfolio through large-scale manufacturing integration and digital optimization under its Transform to Outperform initiative. The company reported $40 billion in 2025 sales and is targeting $2 billion EBITDA improvement through operational efficiencies. Development of CO2 removal fluids based on amine chemistry supports carbon capture and storage applications. Global manufacturing footprint across 29 countries enables cost-competitive supply of industrial cleaning solvents. Focus on MRO and lubrication markets aligns with tightening VOC regulations in North America and Europe. Integration of AI in production processes improves formulation efficiency and customer-specific solutions.

United States: AI-Driven Fluid Intelligence and Energy Transition Use Cases

The United States removal fluids industry is moving decisively toward data-driven formulation control and energy-transition applications. In October 2025, a strategic collaboration between Savant Fluid Management and NPTLabs resulted in the launch of the first Predictive AI Fluid Management Platform in the sector. This system enables real-time optimization of removal fluid chemistries across complex shale extraction environments, directly improving fluid efficiency under highly variable downhole conditions. Parallel to upstream optimization, thermal management has emerged as a structurally new demand pocket. In June 2025, Shell launched DLC Fluid S3 in Houston, a propylene-glycol-based direct liquid cooling fluid engineered for AI and high-performance computing infrastructure, offering corrosion protection lifecycles exceeding six years and displacing legacy inorganic acid technology fluids.

Asset consolidation in gas-rich basins has further reinforced demand for high-performance removal fluids. Strategic shale acquisitions in the Haynesville, including the 2025 transaction by JERA Americas, have increased production intensity beyond 500 MMcf/d, requiring synthetic-based fluids capable of sustained contaminant removal under extreme flow regimes. Beyond hydrocarbons, the U.S. policy environment is catalyzing new fluid chemistries. The 2025 federal $35 million Carbon Dioxide Removal purchase pilot has accelerated the development of removal fluids for Direct Air Capture systems, while methane pyrolysis programs jointly advanced by ExxonMobil and BASF are scaling hydrogen production pathways that rely on specialized catalytic removal fluids. Concurrently, post-2024 Eco-mark compliance rules have pushed manufacturers toward VOC-free and biodegradable solvents, driving a documented 22% rise in adoption across industrial cleaning and surface preparation segments.

India: Infrastructure-Led Demand and Diversification into Specialty Fluids

India’s removal fluids market is being reshaped by mega-scale petrochemical investments and policy-backed industrial expansion. In April 2025, Indian Oil Corporation signed a ₹61,077-crore memorandum with the Government of Odisha for the Paradip petrochemical complex, incorporating dedicated production lines for specialty industrial removal and cleaning fluids. Refining innovation is also influencing downstream demand. The Panipat Refinery’s achievement of India’s first ISCC CORSIA certification for Sustainable Aviation Fuel in 2025 has intensified the use of advanced hydrometallurgical and displacement fluids critical to SAF processing workflows.

Industrial policy alignment further reinforces demand fundamentals. Under the Karnataka Industrial Policy 2025–2030, ₹7,50,000 crore has been earmarked for advanced manufacturing, increasing consumption of precision metal removal fluids in machining, tooling, and electronics assembly. Alongside heavy industry, India is witnessing diversification into non-traditional applications. Domestic firms such as Zed Black and IBCO India are developing wellness-oriented removal and diffuser fluid systems that integrate botanical oils for hospitality and commercial interiors. In parallel, IOCL’s 10,000-tonne-per-annum green hydrogen project at Panipat, finalized in May 2025, is creating new demand for ultra-high-purity electrolytic and removal fluids across hydrogen generation and handling infrastructure.

China: Regulatory-Driven Reformulation and Advanced Materials Integration

China’s removal fluids industry is being reshaped by regulatory modernization and export controls on critical processing agents. The Ministry of Industry and Information Technology’s 2025 Work Plan mandates large-scale equipment renewal across petrochemical hubs, accelerating the transition toward low-emission catalytic removal systems aligned with refining-to-chemicals pathways. These mandates are forcing domestic producers to redesign fluid formulations that meet both energy-efficiency and emissions benchmarks.

Export controls introduced in late 2025 on antimony-based catalysts and selected processing reagents have had global ramifications, prompting a rapid shift toward titanium-based and organic removal fluid alternatives. At the same time, innovation is emerging in aerospace and high-technology surface preparation. Startups such as Henan Holywell are producing hollow glass microspheres for use in lightweight aerospace paint removal and surface conditioning fluids, highlighting China’s growing role in specialty, high-value removal fluid components rather than bulk commodity formulations.

Japan: Semiconductor Purity and Closed-Loop Fluid Systems

Japan continues to lead in ultra-high-purity removal fluids tailored for semiconductor and electronics manufacturing. Domestic chemical developers are advancing nanotechnology-enhanced fluids designed to prevent DNA and microbial contamination in cleanroom environments, supporting increasingly stringent yield and defect-reduction requirements in advanced chip fabrication. These formulations emphasize trace-metal control, low ionic residue, and compatibility with next-generation lithography processes.

Energy diversification strategies are reinforcing international technology transfer. Through overseas investments such as North American shale assets held by JERA Americas, Japanese firms are exporting closed-loop fluid recycling systems and waste minimization technologies. These systems integrate removal fluids with advanced filtration and reuse protocols, reducing lifecycle chemical consumption while maintaining performance in high-intensity extraction and processing environments.

Saudi Arabia (GCC): Localization and Crude-to-Chemicals Fluid Demand

In Saudi Arabia, the removal fluids market is closely tied to downstream localization under Vision 2030. The April 2025 expansion of Axens Catalyst Arabia enabled domestic production of tail gas treatment fluids achieving sulfur recovery rates of 99.9%, reducing reliance on imports and strengthening in-kingdom value chains. These developments directly support refinery emissions compliance and gas processing efficiency across the GCC.

Crude-to-chemicals integration is emerging as a structural demand driver. Government incentives are accelerating the localized manufacture of heavy-duty FCC removal agents designed to bypass conventional fuel pathways and maximize olefin output from crude. This transition is increasing demand for high-temperature, catalyst-compatible removal fluids capable of operating under severe processing conditions while meeting increasingly strict environmental performance standards.

Removal Fluids Industry: Country-Level Strategic Snapshot

Removal Fluids Market County Level Snapshot

|

Country / Region

|

Core Demand Driver

|

Structural Impact on Removal Fluids

|

|

United States

|

AI optimization, HPC cooling, carbon removal

|

Shift toward predictive, VOC-free, and catalytic fluids

|

|

India

|

Petrochemical megaprojects, industrial policy

|

Scale-up of specialty and precision removal fluids

|

|

China

|

Regulatory reform, export controls

|

Rapid reformulation toward titanium and organic systems

|

|

Japan

|

Semiconductor purity, closed-loop recycling

|

Ultra-high-purity and reusable fluid technologies

|

|

Saudi Arabia (GCC)

|

Vision 2030, C2C integration

|

Localization of high-severity refinery removal fluids

|

Removal Fluids Market Report Scope

Removal Fluids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.5 Billion

|

|

Market Size (2034)

|

$9.5 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Product Type (Water-Based Fluids, Oil-Based Fluids, Synthetic-Based Fluids, Bio-Based & Organic Fluids), By Chemical Formulation (Surfactants & Emulsifiers, Solvents & Degreasers, Chelating Agents, pH Regulators & Buffers), By Application (Oil & Gas Displacement, Industrial Cleaning & Degreasing, Paint & Coating Removal, Electronic & Data Infrastructure Cleaning, Renewable Energy Equipment Cleaning)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shell PLC, ExxonMobil Corporation, SLB, Halliburton Company, Baker Hughes, BASF SE, TotalEnergies SE, Indian Oil Corporation Limited, Chevron Phillips Chemical Company, Evonik Industries AG, Quaker Houghton, Fuchs Petrolub SE, Sinopec Group, Arkema SA, Clariant AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Removal Fluids Market Segmentation

By Product Type

- Water-Based Fluids

- Oil-Based Fluids

- Synthetic-Based Fluids

- Bio-Based & Organic Fluids

By Chemical Formulation

- Surfactants & Emulsifiers

- Solvents & Degreasers

- Chelating Agents

- pH Regulators & Buffers

By Application

- Oil & Gas Displacement

- Industrial Cleaning & Degreasing

- Paint & Coating Removal

- Electronic & Data Infrastructure Cleaning

- Renewable Energy Equipment Cleaning

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Removal Fluids Industry

- Shell PLC

- ExxonMobil Corporation

- SLB

- Halliburton Company

- Baker Hughes

- BASF SE

- TotalEnergies SE

- Indian Oil Corporation Limited

- Chevron Phillips Chemical Company

- Evonik Industries AG

- Quaker Houghton

- Fuchs Petrolub SE

- Sinopec Group

- Arkema SA

- Clariant AG

*- List not Exhaustive