Market Overview: Expanding Demand for Efficient and Sustainable Bulk Solutions

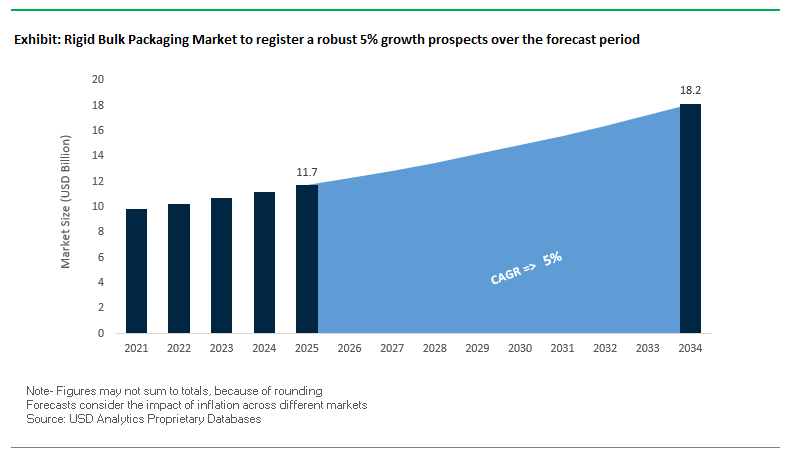

The global rigid bulk packaging market is projected to grow from USD 11.7 billion in 2025 to USD 18.2 billion by 2034, registering a steady CAGR of 5%. This growth is underpinned by rising demand from the food & beverage, chemical, and pharmaceutical sectors, where product safety, hygiene, and bulk handling efficiency are critical. Industry professionals and buyers are increasingly evaluating packaging solutions not just for durability but also for sustainability, lifecycle costs, and alignment with circular economy goals.

Rigid bulk packaging solutions like Intermediate Bulk Containers (IBCs), plastic drums, and heavy-duty corrugated boxes are seeing growing adoption due to their reusability, stackability, and compatibility with automated logistics systems. HDPE remains the most dominant material, primarily because of its lightweight properties and resilience against chemical exposure. The market is also evolving with rising investments in reconditioning and recycling services, as regulatory and corporate sustainability pressures accelerate the shift toward reusable packaging models.

Key Insights for Industry Professionals:

- Plastic leads the material mix: HDPE dominates due to durability and versatility.

- IBCs driving growth: Stackability and reusability fuel adoption across logistics.

- Food & beverage largest consumer: Over one-third market share due to bulk transport demand.

- Circular economy shaping strategies: Reconditioning and recycling are now core industry practices.

Market Analysis: Recent Industry Developments Reshaping Competition

The rigid bulk packaging market has seen a wave of consolidations, expansions, and sustainability-driven product launches that are redefining competition and global capacity.

In August 2025, SCHÜTZ expanded its U.S. footprint by opening a new plant in Kenosha, Wisconsin, strengthening IBC and drum production for Midwest customers. Similarly, January 2025 marked a major expansion by Mauser Packaging Solutions in Haiyan, China, reinforcing its strategic focus on the fast-growing Asian packaging market.

Acquisitions are reshaping global market leadership. In April 2025, Amcor completed its USD 8.4 billion acquisition of Berry Global, strengthening its plastic packaging capabilities, including rigid bulk solutions. In June 2025, International Paper finalized its acquisition of DS Smith, with the EU’s approval contingent on divesting select European plants, highlighting regulatory oversight in sector consolidation. Earlier, in March 2024, Greif acquired Ipackchem, expanding into specialty rigid packaging.

Sustainability remains at the core of product innovation. Berry Global’s Verdant tube with 25% PCR content (February 2024) and SCHÜTZ’s GREEN LAYER IBC technology reflect an industry-wide shift toward recycled content and closed-loop systems. Reports like Graphic Packaging Holding Company’s sustainability report (July 2025) also reinforce how sustainability disclosures are shaping procurement decisions across industries.

Trends and Opportunities Defining the Future of the Rigid Bulk Packaging Market

Strategic Shift Towards High-Performance, Reconditionable Composite IBCs

The rigid bulk packaging market is undergoing a structural transformation as industries transition from single-use containers to reconditionable composite Intermediate Bulk Containers (IBCs). This shift is fueled by logistics cost pressures, sustainability mandates, and regulatory safety requirements. Unlike corrugated or disposable alternatives, composite IBCs can be reused more than 50 times before degradation, offering a significantly lower total cost of ownership. While the upfront investment is higher, companies realize long-term savings through reduced container replacement costs and lower waste management expenses.

In addition to cost efficiency, compliance and safety are driving adoption, especially for hazardous materials. Agencies such as the U.S. Department of Transportation (DOT) mandate the use of certified containers for dangerous goods transport. Composite IBCs, often designed with steel cages for added structural integrity, meet these standards by withstanding the rigors of international shipping. Moreover, the environmental sustainability factor is accelerating uptake, as reusable IBCs reduce raw material consumption and the energy required for container production, aligning with global carbon reduction targets and corporate ESG goals.

Integration of Smart Technologies for Supply Chain Visibility and Condition Monitoring

A defining trend in the rigid bulk packaging industry is the integration of smart technologies that transform packaging into data-rich assets. IoT-enabled IBCs and rigid containers are equipped with embedded sensors that track real-time parameters such as location, shock, temperature, and humidity. This capability is proving critical for industries handling sensitive cargo like pharmaceuticals, chemicals, and food ingredients.

Companies like Hoover CS have pioneered fleets of IBCs with advanced tracking, combining GPS, cellular, and Wi-Fi connectivity. The data feeds into customer dashboards, providing visibility into tank locations, product movements, and performance metrics. These insights enable proactive management: if conditions deviate from set thresholds, real-time alerts can trigger immediate interventions to prevent spoilage or damage. Additionally, the traceability benefits are vital for compliance in highly regulated industries. With a full auditable trail of temperature, movement, and custody, IoT-enabled rigid bulk containers strengthen confidence in the supply chain and ensure compliance with FDA, WHO, and EU regulatory standards.

Development of Advanced Barrier Materials for Extended Shelf-Life of Food and Pharma Ingredients

As global supply chains expand, there is a growing opportunity to develop rigid bulk packaging solutions with superior barrier technologies. Sensitive food and pharmaceutical ingredients often require months of storage and long-distance shipping, making moisture and oxygen ingress control critical. This has fueled innovation in multilayer polymer blends such as PET with EVOH, which provide outstanding barrier performance to prevent oxidation, moisture penetration, and chemical degradation.

Beyond passive barriers, companies are exploring active packaging solutions that interact with the internal environment to further extend shelf life. Oxygen scavengers and moisture regulators embedded within rigid packaging can protect bulk ingredients like dairy powders, protein isolates, and pharmaceutical actives during long transit times. The need is particularly urgent in pharmaceuticals echoed by the World Health Organization (WHO) highlighting that more than 50% of vaccines are wasted globally due to cold chain failures. Rigid bulk packaging designed with advanced barrier coatings and controlled-atmosphere systems presents a strategic solution to reduce spoilage and protect high-value products across borders.

Standardization and Palletization Systems for Automated Logistics

The rise of warehouse automation and robotics is reshaping packaging requirements, creating opportunities for standardized, automation-ready rigid bulk containers. These containers are being designed with consistent footprints, stackability, and robotic-gripper-friendly structures, ensuring seamless integration into automated warehouses and robotic palletizing systems.

In automated environments, robotic palletizers can handle heavy drums and IBCs with greater efficiency and accuracy than manual labor. Standardized IBCs allow higher stacking heights, optimize warehouse space, and enable error-free robotic handling, improving throughput while reducing costs. Furthermore, automation-driven solutions directly contribute to labor reduction with studies showing palletizing automation can cut labor requirements by 75% or more, while also reducing workplace injuries caused by manual handling of heavy bulk containers.

For logistics-intensive industries such as chemicals, food, and pharmaceuticals, standardization ensures efficiency in handling and transport across multiple geographies. This trend aligns with the larger industry push toward Industry 4.0-enabled logistics, where smart automation and packaging design work hand-in-hand to streamline the supply chain.

Trends and Opportunities Reshaping the Rigid Bulk Packaging Market

Strategic Shift Towards High-Performance, Reconditionable Composite IBCs

The rigid bulk packaging market is experiencing a decisive move toward reconditionable composite Intermediate Bulk Containers (IBCs) as industries prioritize long-term cost efficiency, durability, and sustainability. Unlike single-use corrugated or fiber containers, composite IBCs can withstand over 50 reuse cycles before degradation, drastically lowering cost per trip. Although the upfront investment is higher, the total cost of ownership is significantly reduced due to fewer replacements and decreased waste management requirements.

Safety and compliance further strengthen this shift. Regulatory agencies like the U.S. Department of Transportation (DOT) mandate certified containers for hazardous materials, and composite IBCs, often reinforced with steel cages, are engineered to meet these stringent standards. Beyond safety, environmental benefits are driving adoption. By reducing virgin raw material usage and energy demand for new container manufacturing, reconditionable IBCs align with corporate ESG goals and global carbon-reduction mandates. As chemical, pharmaceutical, and food industries move toward circular models, composite IBCs are becoming the gold standard.

Integration of Smart Technologies for Supply Chain Visibility and Condition Monitoring

The digitalization of packaging has reached rigid bulk containers, where IoT-enabled IBCs are transforming logistics into a connected, data-driven ecosystem. With embedded sensors, GPS, and wireless transmitters, these containers monitor location, temperature, humidity, and handling conditions in real time critical for pharmaceuticals, chemicals, and food-grade ingredients.

Companies like Hoover CS are pioneering smart container fleets, feeding live data into customer dashboards for end-to-end supply chain visibility. IoT also delivers proactive management, enabling real-time alerts when temperature or handling thresholds are breached, allowing immediate corrective actions to prevent spoilage or damage. Enhanced traceability is another benefit, as IoT-equipped containers create auditable custody records to meet FDA, EU, and WHO standards. This integration of smart technology elevates rigid bulk packaging from a simple transport medium to a strategic compliance and risk management tool.

Development of Advanced Barrier Materials for Extended Shelf-Life of Food and Pharma Ingredients

Global supply chains for sensitive products such as dairy powders, nutritional supplements, and active pharmaceutical ingredients are creating demand for rigid bulk containers with advanced barrier technologies. New multilayer structures that combine PET with EVOH offer exceptional protection against oxygen and moisture, extending shelf life while reducing waste.

Beyond passive materials, active packaging technologies are being explored. Oxygen scavengers and moisture regulators embedded in rigid bulk containers help maintain product integrity during extended storage or long-distance shipping. For pharmaceuticals, where WHO estimates that over 50% of vaccines are wasted due to cold chain breaks, barrier-enhanced rigid bulk systems provide a safeguard against product loss. These innovations position packaging not only as a container but also as a performance-enhancing technology for global supply chains.

Standardization and Palletization Systems for Automated Logistics

The rise of warehouse automation, robotics, and Industry 4.0 logistics is generating opportunities for rigid bulk containers designed with standardized footprints, stackability, and robotic compatibility. Standardization ensures seamless integration into automated palletizers, robotic arms, and conveyor systems, significantly reducing manual intervention.

Robotic palletizers capable of handling drums and IBCs enable precise stacking, optimize warehouse space, and improve stability in transport. These systems cut labor requirements by up to 75%, while also reducing the risk of worker injuries from heavy lifting. Standardized rigid containers also enhance global supply chain efficiency, as consistent sizing improves transport compatibility across regions. With the accelerating adoption of automation in e-commerce, chemicals, and food industries, rigid bulk packaging optimized for robotics represents one of the most promising growth vectors in this sector.

Competitive Landscape: Leading Companies in Rigid Bulk Packaging

The global rigid bulk packaging market is highly competitive, characterized by regional expansions, product innovation, and sustainability-driven initiatives. Companies are increasingly differentiating through integrated lifecycle services, recycling infrastructure, and global distribution networks.

Mauser Packaging Solutions: Expanding Global IBC and Recycling Capabilities

Mauser Packaging Solutions remains a leader in rigid bulk packaging, offering plastic drums, IBCs, fiber, and metal packaging. Its Twinshot recyclable pails and Poly-MT IBC highlight its sustainability-driven innovation. With expansions in Mexico (September 2023) and China (January 2025), the company is strengthening global capacity. Its end-to-end lifecycle solutions, including reconditioning and recycling, make it a frontrunner in supporting circular economy goals.

Greif, Inc.: Strengthening Premium Specialty Packaging Portfolio

Greif has a strong presence in steel, fiber, and plastic drums as well as IBCs, serving industries such as chemicals, food & beverage, and oil & gas. Its USD 100 million cost reduction program enhances competitiveness, while the Ipackchem acquisition (March 2024) reinforced its position in premium rigid packaging. With a strong global network and UN-rated durable drums, Greif maintains leadership in packaging hazardous and sensitive materials.

SCHÜTZ GmbH & Co. KGaA: Driving Innovation in Sustainable IBCs

SCHÜTZ is widely recognized for its ECOBULK and RECOBULK IBCs. Its GREEN LAYER technology integrates recycled materials, while the SC1 jerrycan series diversifies its product base. The new Wisconsin plant (August 2025) strengthens its U.S. presence, adding to its 55+ global production sites. SCHÜTZ’s RECONTAINER service, which manages global collection and reconditioning, positions the company as a circular economy leader.

DS Smith Plc: Expanding Heavy-Duty Corrugated Bulk Packaging

Though primarily a paper-based packaging leader, DS Smith plays a vital role in corrugated rigid bulk packaging with solutions like triple-wall boxes and bulk liquid containers. Its acquisition by International Paper (June 2025) is reshaping the global fiber-based packaging sector. DS Smith’s core strength lies in cost-effective, recyclable heavy-duty solutions that optimize shipping efficiency.

Brambles Ltd. (CHEP): Driving Reuse-Based Packaging Logistics

Operating under the CHEP brand, Brambles leads in pallets, crates, and containers pooling services. Its Zero Waste World (ZWW) program helps reduce inefficiencies, while BXB Digital technology enhances supply chain visibility. With a fleet of 348 million+ pallets and containers and 750+ service centers worldwide (as of June 2025), Brambles remains a dominant force in reuse-based logistics packaging solutions.

Rigid Bulk Packaging Market Share Insights

Intermediate Bulk Containers Lead Rigid Bulk Packaging Market Share by Product Type

Intermediate Bulk Containers (IBCs) account for 38% of the rigid bulk packaging market in 2025, establishing themselves as the most efficient logistics solution for bulk liquid and semi-liquid transport. Their cubic design maximizes container space, reduces freight costs, and streamlines handling compared to multiple drums, making them indispensable for chemicals, food ingredients, and industrial applications. Reusable cage IBCs and growing adoption of composite and plastic variants further strengthen their dominance. Drums, with a 32% share, remain the industrial workhorse due to standardization, universal regulatory acceptance, and their balance of durability and cost-effectiveness for hazardous and non-hazardous goods alike. Pails, bulk boxes, and other rigid formats cater to medium-batch, dry goods, and niche applications, reinforcing the market’s adaptability. The product segmentation clearly shows how IBCs dominate through efficiency, while drums continue as the backbone of industrial transport across regulated supply chains.

Chemicals Dominate Rigid Bulk Packaging Market Share by Application

The chemical sector commands 45% of the rigid bulk packaging market in 2025, underscoring its role as the largest and most critical end-user. From industrial chemicals and solvents to specialty resins and hazardous substances, the industry relies heavily on UN-rated IBCs and drums that meet stringent safety and compliance standards. Industrial applications follow with 25%, reflecting demand from paints, coatings, lubricants, and construction materials, where packaging strength and reusability are non-negotiable. Food and beverages represent a fast-growing application, leveraging IBCs for liquid ingredients such as oils and syrups, and bulk boxes for grains and powdered products. Pharmaceuticals and healthcare, while smaller in share, represent a premium segment, requiring stainless steel and specialized containers for sterile raw materials. Together, these insights highlight how chemicals anchor rigid bulk packaging demand, while food, beverages, and pharma create new value-driven opportunities for precision and compliance.

United States: E-Commerce Growth and Sustainability Redefining Rigid Bulk Packaging

The U.S. rigid bulk packaging market is witnessing accelerated demand, primarily fueled by the rapid expansion of the e-commerce industry. The need for durable, stackable containers such as intermediate bulk containers (IBCs) and bulk boxes has intensified, ensuring product safety and efficiency during transit. At the same time, a strong focus on sustainability is reshaping packaging strategies, with companies emphasizing reusability in closed-loop supply chains. For instance, Greif, Inc. has strengthened its leadership by increasing its ownership stake in Centurion Container LLC, a pioneer in IBC reconditioning, to expand its eco-friendly packaging portfolio. Growth in the country’s chemical and pharmaceutical industries further drives demand, as industrial drums and barrels remain indispensable for transporting refined petroleum products and pharmaceuticals. Additionally, automation and robotics are being increasingly adopted to streamline production and mitigate labor shortages. However, the patchwork of state-level regulations, including Extended Producer Responsibility (EPR) laws and PFAS-free mandates, is pushing innovation toward more sustainable and compliant solutions across nationwide supply chains.

Germany: Circular Economy and Regulations Driving Innovation in Rigid Bulk Packaging

Germany’s rigid bulk packaging market is anchored in strict compliance with the EU Packaging and Packaging Waste Regulation (PPWR), which is compelling manufacturers to prioritize eco-friendly and highly recyclable solutions. The country’s leadership in circular economy initiatives has fostered close collaboration between manufacturers and end-users, driving the adoption of packaging with higher recycled content to meet EU-wide targets. Innovation is another hallmark of the German market, with companies such as Schütz GmbH & Co. developing IBCs featuring advanced ventilation systems to optimize performance. With Germany’s strong industrial and pharmaceutical base, rigid bulk packaging finds robust demand for applications in storage, transportation, and blending. The dual influence of sustainability regulations and industrial strength positions Germany as one of the most advanced hubs for packaging innovation in Europe.

China: Industrialization, Sustainability, and Export Growth Fuel Rigid Bulk Packaging Demand

China’s rigid bulk packaging market is experiencing rapid growth, driven by its vast industrial base, booming e-commerce sector, and expanding logistics networks. Secure and efficient packaging solutions such as IBCs and industrial drums are vital for protecting goods during large-scale transportation and handling. The government’s “dual carbon” goals of carbon peak and carbon neutrality are accelerating the shift toward eco-friendly, reduced, and reusable packaging formats across logistics and manufacturing. Technological innovation also plays a central role, with Chinese producers adopting automation, AI, and robotics to boost production efficiency and adapt to automated logistics systems. Furthermore, China’s status as the world’s second-largest exporter amplifies its reliance on rigid bulk packaging for international trade, reinforcing the country’s global significance in this market.

India: Government Initiatives and Expanding Manufacturing Base Strengthening Rigid Bulk Packaging Industry

India’s rigid bulk packaging market is gaining momentum through strong governmental and industrial initiatives. Programs such as the Integrated Cold Chain and Value Addition Infrastructure are boosting demand for insulated bulk containers, particularly for pharmaceuticals and perishable foods. Meanwhile, the implementation of the Plastic Waste Management (Amendment) Rules is pushing industries toward reusable, eco-friendly rigid bulk alternatives, aligning with the country’s sustainability goals. On the manufacturing front, companies like Pyramid Technoplast are investing heavily in polymer drum and IBC production, while partnerships such as Manjushree Technopack’s collaboration with the Indian Institute of Science highlight efforts in developing recyclable elastomeric materials. Rising investments and regulatory pressures are collectively reshaping India’s packaging industry into a more advanced and environmentally conscious sector.

Brazil: Cold Chain Logistics and Circular Economy Shaping Rigid Bulk Packaging Growth

Brazil’s rigid bulk packaging market is undergoing a transformation driven by regulatory action and industrial demand. The National Solid Waste Policy, aimed at restricting single-use plastics, is fueling the adoption of durable and reusable bulk containers. At the same time, governmental investments in infrastructure, particularly for vaccine sovereignty, are spurring demand for ultra-low-temperature storage and high-performance rigid packaging solutions in pharmaceutical supply chains. The Brazilian market is also embracing circular economy principles, with companies adopting closed-loop systems to recycle post-consumer plastics into new packaging. Furthermore, the growing cold chain logistics sector is boosting demand for temperature-controlled bulk packaging to ensure the safe storage and transportation of perishable foods and medicines. These developments position Brazil as a rapidly evolving market with strong sustainability and healthcare-driven applications.

Japan: Bio-Based Innovation and Recycling Systems Driving Rigid Bulk Packaging Evolution

Japan’s rigid bulk packaging market is increasingly defined by innovation in bio-based materials and advanced recycling systems. A key example is the collaboration between LyondellBasell, Shiseido, Futamura Chemical, and Iwatani to incorporate bio-polypropylene (bio-PP) into cosmetic packaging, supporting the country’s environmental goals for 2030 and 2050. Japan’s advanced recycling infrastructure among the world’s most efficient provides a robust foundation for producing recycled-content rigid packaging at scale. The government’s commitment to reducing greenhouse gas emissions by 46% by 2030 and achieving net-zero by 2050 underlines a clear sustainability-driven trajectory for the sector. Simultaneously, Japanese manufacturers are leading in material science innovations, creating more hygienic, durable, and functional rigid bulk packaging solutions that meet the needs of high-performance industries. This combination of eco-innovation, recycling, and technological advancements makes Japan a global leader in the evolution of sustainable rigid packaging.

Rigid Bulk Packaging Market Report Scope

Rigid Bulk Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.7 Billion

|

|

Market Size (2034)

|

$18.2 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Product Type (Intermediate Bulk Containers, Drums, Pails, Bulk Boxes, Other Bulk Containers), By Material Type (Plastic, Metal, Wood, Fiberboard, Other Materials), By Application (Chemicals, Food & Beverages, Pharmaceuticals & Healthcare, Industrial, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Greif, Inc., Mauser Packaging Solutions, SCHÜTZ GmbH & Co. KGaA, Amcor plc, DS Smith Plc, BWAY Corp. (a subsidiary of Mauser Packaging Solutions), Nefab Group, Sonoco Products Company, Rieke Packaging Systems, Oji Holdings Corporation, Mondi Group, IPL Plastics, RPC Group, Bulk Handling Australia, E3 Sustainable Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rigid Bulk Packaging Market Segmentation

By Product Type

- Intermediate Bulk Containers

- Drums

- Pails

- Bulk Boxes

- Other Bulk Containers

By Material Type

- Plastic

- Metal

- Wood

- Fiberboard

- Other Materials

By Application

- Chemicals

- Food & Beverages

- Pharmaceuticals & Healthcare

- Industrial

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Rigid Bulk Packaging Market

- Greif, Inc.

- Mauser Packaging Solutions

- SCHÜTZ GmbH & Co. KGaA

- Amcor plc

- DS Smith Plc

- BWAY Corp. (a subsidiary of Mauser Packaging Solutions)

- Nefab Group

- Sonoco Products Company

- Rieke Packaging Systems

- Oji Holdings Corporation

- Mondi Group

- IPL Plastics

- RPC Group

- Bulk Handling Australia

- E3 Sustainable Solutions

*List not Exhaustive

Research Coverage

This report investigates the global rigid bulk packaging market with a detailed focus on technological breakthroughs, regulatory shifts, and sustainability-driven strategies reshaping the industry. USDAnalytics delivers an in-depth analysis review that highlights the evolving dynamics across product types, materials, and end-use applications. The study offers critical insights into competitive strategies, regional developments, and innovations such as reconditionable composite IBCs, IoT-enabled containers, and advanced barrier technologies. By covering key industry highlights and assessing how mergers, acquisitions, and sustainability initiatives influence the competitive landscape, this report is an essential resource for manufacturers, suppliers, investors, and policymakers seeking to understand the future of bulk packaging solutions.

Scope Highlights

- Segmentation: By Product Type (Intermediate Bulk Containers, Drums, Pails, Bulk Boxes, Other Bulk Containers), By Material Type (Plastic, Metal, Wood, Fiberboard, Other Materials), By Application (Chemicals, Food & Beverages, Pharmaceuticals & Healthcare, Industrial, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Company Insights: Profiles and strategic analysis of 15+ leading players including Greif, Mauser Packaging Solutions, SCHÜTZ GmbH & Co. KGaA, Amcor, and DS Smith.

Methodology

The research methodology integrates primary and secondary approaches to ensure accuracy and reliability. Primary research includes structured interviews with industry executives, packaging engineers, sustainability officers, and supply chain managers across multiple regions. Secondary research incorporates company filings, investor presentations, government regulations, trade association publications, and reliable databases to capture market trends and innovation pathways. A data triangulation model validates forecasts, combining demand-side analysis with supply-side capacity mapping and macroeconomic indicators. Forecasting from 2025–2034 applies both top-down and bottom-up models, ensuring consistency across product categories, material types, and regional demand patterns.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.