Market Overview: High-Strain Recovery, Biocompatibility Standards & Thermal Actuation Precision

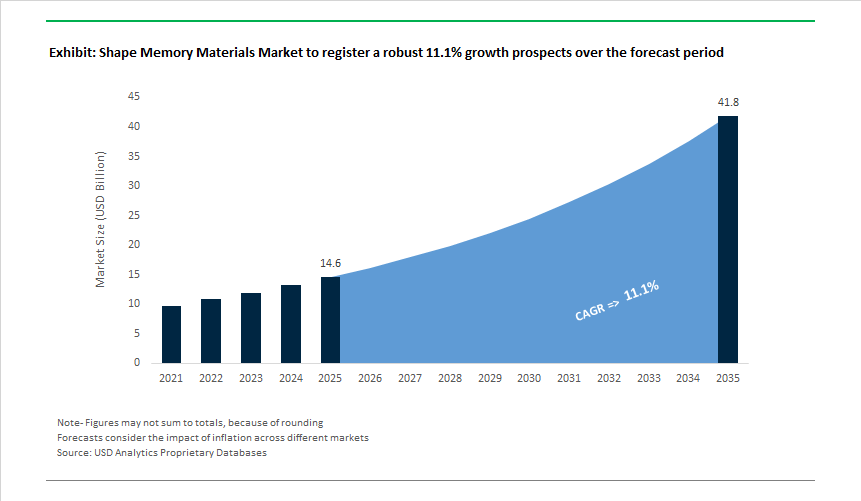

The Shape Memory Materials Market, valued at USD 14.6 billion in 2025, is projected to grow at an 11.1% CAGR to reach USD 41.8 billion by 2035, driven by accelerating adoption of Nitinol superelastic systems, high-temperature SMAs for aerospace, and medical-grade shape memory polymers for next-generation biomedical and soft-robotics applications.

The market is entering a transformative expansion phase as manufacturers increasingly prioritize recoverable strain performance (up to 8%), long-cycle superelastic fatigue life), and precision transformation-temperature engineering for actuation-critical components. Nitinol’s unique combination of superelasticity, corrosion resistance, and biocompatibility continues to anchor its dominance across cardiovascular stents, orthopedic devices, and surgical robotics, with more than 124 U.S. medical device OEMs relying on SMA components. On the other hand, the aerospace sector is accelerating adoption of high-temperature SMAs (HTSMAs) such as NiTiHf, capable of 400°C operation with stable cyclic performance, enabling morphing structures, adaptive inlets, and thermal-control hardware. In parallel, shape memory polymers (SMPs) and emerging 4D-printing routes are creating new pathways for programmable biomedical scaffolds, autonomous robotic systems, and tunable morphing structures. As OEMs shift toward engineered microstructures, alloying precision, and highly controlled thermal-response windows, the competitive advantage is increasingly defined by fatigue-optimized designs, ultra-clean melt processing, and validated biocompatibility frameworks that support clinical and aerospace certification requirements.

Market Analysis: Sma/Smp Innovation, Aerospace Validation & Biomedical Commercialization

The Shape Memory Materials Market is witnessing major performance breakthroughs and commercialization milestones, particularly in medical, aerospace, and smart-material manufacturing ecosystems. In December 2025, Dynalloy introduced an upgraded generation of Flexinol® SMA wires engineered for silent consumer-electronics actuators, addressing OEM demand for compact, low-power motion systems. The improved thermal-response characteristics and reduced electrical load position Flexinol® as a preferred solution for micro-actuators in IoT devices and compact automation. This followed a significant September 2025 investment round where Shape Memory Medical Inc. secured nearly USD 38 million, accelerating development of SMP foams for vascular interventions-highlighting the continued dominance of shape memory materials in structural heart and peripheral vascular therapy.

The market also strengthened its scientific foundation through transformative R&D milestones. In November 2025, an academic-industry consortium successfully demonstrated 4D-printed SMP bone scaffolds with 90% shape fixity and 84% recovery at physiological temperature (37°C). This represents a major step toward next-generation regenerative materials with built-in actuation and morphological adaptability. In May 2025, the U.S. DOE further advanced the field by funding magnetic-field-actuated shape memory materials (MSMMs) for ultra-efficient magnetocaloric cooling systems-expanding SMA application potential beyond medical and aerospace into energy efficiency and industrial sustainability.

Aerospace applications recorded meaningful progress as well. In March 2025, NASA validated a NiTiHf-based, high-temperature SMA morphing system for variable-geometry inlets, demonstrating stable operation at 400°C-a crucial threshold for high-speed propulsion platforms. This builds upon prior developments from July 2025, when Johnson Matthey commercialized a next-generation NiTi alloy with enhanced durability for orthodontic and surgical instruments. On the other hand, SMP innovation accelerated with the June 2024 launch of DEGRES INX by BIO INX, enabling biodegradable shape-changing structures for 3D bioprinting and tissue engineering.

The increasing diversification-from medical implants to energy systems, robotics, 4D-printed scaffolds, and aerospace morphing components-shows that the market’s trajectory through 2035 will be defined by material engineering precision, actuation fatigue reliability, and the ability to scale advanced SMA/SMP formulations for high-tech industries.

Shape Memory Materials Market: Trends and Opportunities

High-Cycle Fatigue–Optimized NiTi Alloys Redefine Reliability in Class III Medical Implants

The medical device industry is recalibrating its material specifications for shape memory alloys as implantable devices move toward longer service lives and higher physiological loading. The strategic pivot is toward ultra-clean Nitinol (NiTi) with tightly controlled inclusion populations and precipitate morphology, shifting fatigue behavior from flaw-driven failure to intrinsic microstructural stability. A decisive milestone was reported in July 2025, when a peer-reviewed study demonstrated that VAR/EBR-processed NiTi tubing sustained 100 million physiological cycles without fracture by limiting non-metallic inclusions to <10 μm—a threshold that effectively suppresses crack initiation under cyclic loading.

Regulatory and application benchmarks are reinforcing this direction. In endovascular devices, 2025 engineering standards now require components to tolerate ≥400 million arterial pressure cycles, particularly for heart valve frames and stents subjected to continuous pulsatile strain. Advanced thermomechanical processing routes have shown stable martensitic transformation under mean strains up to 7%, a critical requirement for maintaining superelastic response over multi-decade implant lifetimes. Surface engineering is compounding these gains: Atomic Layer Deposition (ALD) of alumina (Al₂O₃) on cold-drawn NiTi wires has been shown to increase fatigue life from ~7,500 cycles to >293,000 cycles, creating a credible pathway for long-duration implantable actuators and neuromodulation devices. Collectively, these advances reposition NiTi from a high-performance material with known fatigue constraints to a predictable, regulator-ready platform for next-generation cardiovascular and orthopedic implants.

Shape Memory Polymer Composites Replace Mechanical Complexity in Aerospace Deployment Systems

Aerospace OEMs are increasingly adopting shape memory polymer composites (SMPCs) to eliminate the mass, complexity, and failure modes associated with motors, gears, and hinges in deployable structures. Unlike metallic SMAs, SMPs offer up to four times the recoverable strain, enabling compact stowage and reliable deployment of large antennas, booms, and solar arrays. This shift is particularly pronounced in satellites and UAVs, where payload mass directly impacts mission economics.

Program-level validation has accelerated confidence. The NASA Langley Research Center has flight-tested LaRC-SMPC architectures in adaptive airframe components, using carbon-nanotube fillers to enable rapid, electrically triggered shape recovery. These smart structures reconfigure during different flight phases, delivering functional benefits such as airframe noise reduction without mechanical actuation. In 2025, collaborative testing aboard the International Space Station confirmed that SMPCs retain shape memory behavior after repeated thermo-mechanical cycling under vacuum and UV exposure—a critical proof point for orbital durability. From a systems perspective, industry assessments in late 2024 showed 40–60% weight reductions versus electromechanical deployment systems, making SMPCs a cornerstone technology for the “New Space” ecosystem where reliability must be achieved with minimal redundancy.

Active Vibration Damping Opens a New Role for SMAs in EV Architectures

Electrification has shifted vehicle NVH profiles, exposing high-frequency motor harmonics and road-induced vibrations that were previously masked by combustion noise. This has created a focused opportunity for shape memory alloys as tunable, lightweight vibration dampers within EV powertrains and battery systems. Unlike passive elastomers, SMAs provide temperature- and load-responsive damping, absorbing kinetic energy through stress-induced phase transformation.

Policy support is catalyzing adoption. In April 2025, India’s Department of Science and Technology launched the EVolutionS Program to accelerate indigenous EV materials, explicitly supporting SMA integration for battery protection and power electronics longevity. Engineering trials indicate that embedding SMA wires into mounts and subframes can reduce low-frequency vibration transmission by up to 12 dB, a meaningful improvement for perceived cabin quality. SMAs are also being integrated into active grille shutters and battery cooling architectures, where transformation temperatures (Af) enable passive-active thermal control—reducing parasitic energy draw from fans and pumps. This convergence of NVH mitigation and thermal management positions SMAs as multi-functional enablers rather than single-use components in EV design.

Shape Memory Materials Enable Human-Centric Soft Robotics and Wearables

The fastest-growing opportunity frontier for shape memory materials lies in soft robotics and wearable assistive devices, where compliance, safety, and force-to-weight efficiency are paramount. Shape memory materials excel in these environments by delivering muscle-like actuation without rigid transmissions. At RoboSoft 2025, the Soft Wrist Assist (SWA) prototype demonstrated this advantage using SMA coil springs to generate 10 N of force with a 40% contraction ratio, all within a 151 g wearable—a practical alternative to bulky pneumatic systems for rehabilitation.

Hybrid actuation strategies are extending functionality. 2025 disclosures showed compact soft robots (≈40×45 mm) combining dielectric elastomer actuators with SMA springs to achieve 91 mm/s locomotion speeds and 80 mm jump heights, underscoring applicability in search-and-rescue and minimally invasive diagnostics. Beyond discrete devices, the market is progressing toward SMA-integrated smart fabrics, embedding thin-film shape memory elements into textiles that dynamically adjust porosity or insulation in response to body heat. This trend aligns with growing demand in sports medicine and rehabilitation, where adaptive garments can provide continuous, low-profile assistance—positioning shape memory materials as foundational technologies in the shift toward human-centric, intelligent systems.

Shape Memory Materials Market Share Analysis

Market Share by Product Form: Shape Memory Wires and Strips Power High-Response Actuation

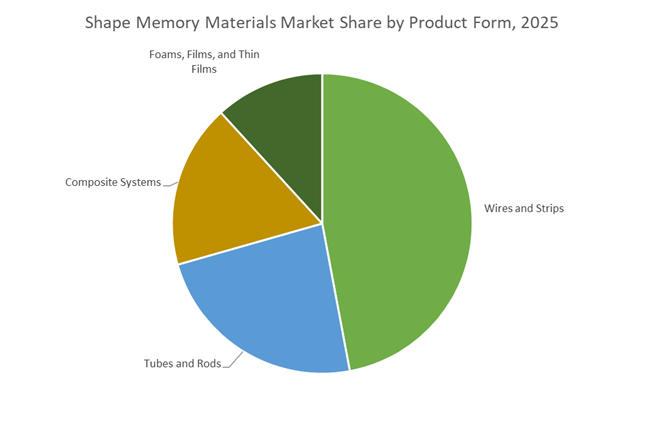

Wires and strips account for approximately 40% of the global Shape Memory Materials Market, reflecting their role as the most efficient and commercially scalable form factor for shape memory actuation. This segment dominates because thin-profile geometries offer the highest surface-area-to-volume ratio, enabling rapid thermal response and precise, repeatable motion—critical performance requirements across medical devices, robotics, and aerospace systems. Shape memory alloy wires, particularly Nitinol, deliver muscle-like contraction behavior, allowing engineers to replace bulky electromechanical components with ultra-compact, lightweight actuators that dramatically simplify system design. Market share is further reinforced by exceptional fatigue resistance, as high-quality wires are engineered to perform tens of thousands of actuation cycles without losing shape memory functionality, making them suitable for continuous-use applications. Superelastic recovery characteristics also differentiate this segment, enabling wires and strips to endure large elastic strains without permanent deformation—an attribute that underpins adoption in kink-resistant medical guidewires and flexible mechanical linkages. From a value perspective, the force-to-weight advantage of shape memory wires allows significant mechanical output from minimal material mass, a decisive benefit in weight-sensitive platforms such as minimally invasive surgical tools and aerospace subsystems. Collectively, these response-speed, durability, and miniaturization advantages explain why wires and strips remain the structural backbone of the shape memory materials market.

Market Share by Application: Medical and Healthcare Applications Anchor Premium Demand

The medical and healthcare segment represents approximately 45% of total demand in the Shape Memory Materials Market, making it the largest and highest-value application area. This dominance is driven by the clinical shift toward minimally invasive procedures, where shape memory materials enable compact devices to be delivered through small incisions and then expand precisely inside the body. Self-expanding Nitinol stents exemplify this value proposition, offering crush-recoverable performance that maintains vessel patency even under external compression—an outcome that conventional metallic implants cannot reliably achieve. Market share is further reinforced by the biocompatibility and MRI compatibility of medical-grade shape memory alloys, which are non-magnetic and safe for long-term implantation, meeting stringent regulatory and clinical requirements. The ability to fine-tune transformation temperatures to human body temperature adds another layer of clinical control, ensuring devices deploy exactly when and where intended. Miniaturization is a final, decisive driver, as ultra-thin shape memory wires enable advanced neurovascular and cardiovascular interventions that demand extreme precision. Together, these functional and clinical advantages position medical and healthcare applications as the primary demand center for shape memory materials, sustaining their leading share in the global market.

Competitive Landscape: Leading SMA/SMP Producers and High-Precision Alloy Manufacturers

The competitive landscape of the Shape Memory Materials Market is driven by companies specializing in Nitinol metallurgy, high-temperature SMA design, precision medical-grade processing, and emerging SMP technologies. Market leaders differentiate through mastery of transformation-temperature control, fatigue-resistant thermomechanical processing, biocompatibility engineering, and integrated manufacturing-from alloy melting to final device fabrication. Their innovations are shaping next-generation applications in minimally invasive surgery, aerospace morphing, robotics, and biomedical scaffolds.

Fort Wayne Metals - Precision Medical-Grade Nitinol For Implants and Minimally Invasive Surgery

Fort Wayne Metals is a global leader in medical-grade Nitinol wire and precision tubing, serving high-criticality applications such as vascular stents, guidewires, and catheter components. The company’s core competitive strength lies in tight control of transformation temperature tuning, ensuring precise actuation at ~37°C for minimally invasive surgery. Its product portfolio includes proprietary alloys such as FWM® L605 and 35N LT®, complementing its Nitinol offerings for broader biomedical applications. By integrating specialized surface finishing, laser cutting, and electropolishing, the company ensures corrosion resistance, fatigue strength, and biocompatibility that meet stringent implantable-device standards.

SAES Getters - Miniaturized SMA Actuators and Biomedical Alloy Innovation

SAES Getters combines advanced SMA technology with its expertise in getters, dispensers, and thermal-management systems to create high-reliability actuation solutions. The company supplies miniaturized, noiseless SMA actuators widely used in robotics, medical devices, and consumer electronics such as autofocus and stabilization systems. In September 2024, SAES launched new medical-grade SMA formulations to support next-generation self-expanding devices, highlighting its strategy of expanding into high-value biomedical components. Its high-purity metallurgy enables thin SMA wires and springs with stable superelasticity across thousands of cycles, reinforcing SAES’s reputation in precision actuation materials.

Confluent Medical Technologies - Integrated Nitinol Manufacturing For Complex Implantable Devices

Confluent Medical Technologies operates as a specialized Nitinol contract manufacturer, supporting medical OEMs with complete vertical integration-from raw material melting to component assembly. The company produces custom Nitinol structures used in structural heart devices, neurovascular implants, and peripheral vascular stents, where geometric precision and phase-transformation consistency are essential. Confluent employs laser cutting, proprietary etching, and electropolishing to create sub-millimeter features with high fatigue resistance. Its engineering support accelerates OEM time-to-market by assisting in material selection, prototype development, and performance optimization.

Dynalloy Inc. - Flexinol® SMA Wires For Low-Cost, High-Utility Actuation

Dynalloy is the primary global supplier of Flexinol® SMA wires, delivering cost-effective and easy-to-integrate actuation solutions for non-medical and lightweight industrial applications. Its SMA wires can be activated through simple Joule heating, making them ideal for micro-valves, robotic grippers, latches, and motion control systems. The company provides pre-trained SMA wires with defined transition temperatures and recovery stresses, enabling rapid implementation by system designers. Continuous improvements in response time and cyclical stability support the growing adoption of Flexinol® in automation and consumer robotics.

The United States remains the global anchor market for high-temperature shape memory alloys (HTSMAs) and medical-grade Nitinol, with demand structurally linked to aerospace innovation, defense modernization, and reshoring policies. Reinforced tariff measures on imported nickel–titanium alloys in 2025 have materially altered procurement dynamics, accelerating domestic melting and processing of SMA ingots. This has directly benefited vertically integrated producers such as ATI and Fort Wayne Metals, strengthening the local supply chain for aerospace actuators and cardiovascular devices. Federal R&D funding from the Department of Energy and NASA has further shifted the U.S. market toward next-generation NiTiHf systems capable of operating at elevated temperatures, a requirement for hypersonic vehicles and space-based thermal control. In parallel, the Department of Defense’s prioritization of 4D printing-combining shape memory polymers with conductive architectures-signals a long-term expansion of SMM use in adaptive military hardware, positioning the U.S. as a technology leader rather than a cost-driven producer.

China: Industrial-Scale SMM Manufacturing Under the 14th Five-Year Plan

China’s shape memory materials market is defined by scale, state coordination, and rapid industrialization. Under the 14th Five-Year Plan, the government has treated SMMs as “new materials” critical to technological self-sufficiency, leading to the establishment of specialized R&D clusters and accelerated commercialization. Research institutions have translated laboratory advances in shape memory polyimides and aerogels into aerospace thermal protection and smart vehicle components. China has also become the largest consumer of SMMs in the automotive sector, where self-healing and adaptive components are increasingly embedded into EV crash systems and sensor housings. On the biomedical front, domestic manufacturers are closing the gap with Western suppliers in Nitinol-based stents, supported by state-backed quality and certification programs. This combination of volume, application diversity, and policy support positions China as the dominant manufacturing base for mid- to high-grade shape memory materials.

South Korea: Government-Funded MedTech Actuation Platforms

South Korea is strategically leveraging shape memory materials to move up the medical device value chain. The government’s multi-year investment program targeting “game-changing” medical technologies has elevated SMAs and SMP-based actuators as core enablers for surgical robots, minimally invasive tools, and next-generation implants. Localization targets for critical components are reducing reliance on imported Nitinol devices, while simultaneously creating export-ready platforms for Asia-Pacific healthcare markets. South Korea’s approach is highly focused: rather than broad industrial use, the market prioritizes high-margin, regulation-intensive medical applications where reliability and miniaturization favor advanced shape memory actuation systems.

India: PLI-Backed Specialty Alloy Ecosystem for Healthcare and Aerospace

India’s shape memory materials market is transitioning from import dependence toward indigenous capability, driven by the Production Linked Incentive (PLI 1.2) scheme for specialty steel and superalloys. Incentives covering titanium-based and superelastic alloys have catalyzed domestic production of Nitinol for medical and aerospace use. Government-backed entities such as MIDHANI are playing a central role, developing indigenous stents and space-grade actuators in collaboration with national aerospace laboratories. The emergence of specialty alloy clusters and sustained investment commitments are positioning India as a competitive supplier for cost-sensitive global markets, particularly in cardiovascular devices and defense-grade actuation systems.

Germany: Digital Twins, Circular Materials, and Industry 4.0 Integration

Germany leads Europe in the integration of shape memory materials into Industry 4.0 and sustainable manufacturing frameworks. National and EU-level funding under Horizon Europe has accelerated research into SMA-based fastening, joining, and actuation systems for aerospace and advanced manufacturing. Programs led by institutions such as Helmholtz Association are combining digital twins with fatigue modeling to improve the reliability of SMA actuators in industrial robotics. Simultaneously, German manufacturers are pioneering nickel-free and copper-based SMAs to address biocompatibility and regulatory pressures, reinforcing Germany’s role as a premium, regulation-compliant innovation hub rather than a volume producer.

Japan: Materials DX and Precision Micro-Actuation Leadership

Japan’s shape memory materials market is anchored in precision engineering and digital transformation. The Materials Research DX Platform funded by MEXT is enabling AI-driven simulation of crystal growth and superelastic behavior, shortening development cycles for next-generation SMAs and SMPs. Japanese manufacturers are expanding capacity for ultra-fine Nitinol wires used in consumer electronics, particularly 5G smartphone camera modules requiring fast, reliable autofocus and optical image stabilization. Companies such as Furukawa Electric and Nippon Seisen are reinforcing Japan’s dominance in micro-actuation applications. Parallel research into copper–aluminum–nickel SMAs for hydrogen infrastructure highlights Japan’s cross-industry approach, linking SMM innovation to its broader energy transition strategy.

National Strategic Development Matrix: Shape Memory Materials Market (2025)

Shape Memory Materials Market Development Matrix by Country

|

Country

|

Primary Strategic Driver

|

2025 Focus Area

|

Core Shape Memory Applications

|

|

United States

|

Defense & aerospace reshoring

|

HTSMA and 4D printing

|

Hypersonic actuators, medical Nitinol

|

|

China

|

14th Five-Year Plan self-sufficiency

|

Industrial-scale SMM production

|

EV components, vascular stents

|

|

South Korea

|

MedTech localization

|

SMA-driven surgical systems

|

Medical robots, implants

|

|

India

|

PLI-led specialty alloys

|

Indigenous Nitinol production

|

Stents, aerospace actuators

|

|

Germany

|

Industry 4.0 & circular economy

|

Digital twins for SMA systems

|

Aerospace joining, robotics

|

|

Japan

|

Materials DX & precision

|

Micro-scale SMA manufacturing

|

Electronics actuators, hydrogen valves

|

Shape Memory Materials Market Report Scope

Shape Memory Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.6 Billion

|

|

Market Size (2035)

|

$41.8 Billion

|

|

Market Growth Rate

|

11.1%

|

|

Segments

|

By Material Type (Shape Memory Alloys, Shape Memory Polymers, Shape Memory Ceramics), By Actuation Stimulus (Thermal, Electrical, Light, Magnetic, Chemical), By Product Form (Wires & Strips, Tubes & Rods, Foams & Films, Thin Films, Composite Systems), By Application (Medical & Healthcare, Aerospace & Defense, Automotive, Consumer Electronics & Robotics, Construction & Civil Engineering)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Chemours Company, SAES Getters S.p.A., Confluent Medical Technologies Inc., Fort Wayne Metals Research Products Corp., ATI Inc., Memry Corporation, Furukawa Electric Co., Ltd., Admedes GmbH, BASF SE, Covestro AG, Dynalloy Inc., Nippon Seisen Co., Ltd., MedShape Inc., Composite Technology Development Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Shape Memory Materials Market Segmentation

By Material Type

- Shape Memory Alloys

- Shape Memory Polymers

- Shape Memory Ceramics

By Actuation Stimulus

- Thermal

- Electrical

- Light

- Magnetic

- Chemical

By Product Form

- Wires and Strips

- Tubes and Rods

- Foams and Films

- Thin Films

- Composite Systems

By Application

- Medical and Healthcare

- Aerospace and Defense

- Automotive

- Consumer Electronics and Robotics

- Construction and Civil Engineering

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Shape Memory Materials Market

- The Chemours Company

- SAES Getters S.p.A.

- Confluent Medical Technologies, Inc.

- Fort Wayne Metals Research Products Corp.

- ATI Inc.

- Memry Corporation

- Furukawa Electric Co., Ltd.

- Admedes GmbH

- BASF SE

- Covestro AG

- Dynalloy, Inc.

- Nippon Seisen Co., Ltd.

- MedShape, Inc.

- Composite Technology Development, Inc.

*- List not Exhaustive