Shrink Plastic Films Market Size, Overview, and Growth Outlook (2025–2034)

Global Shrink Plastic Films Market Expected to Reach $4.5 Billion by 2034 Amid Rising Demand for Food and E-Commerce Packaging

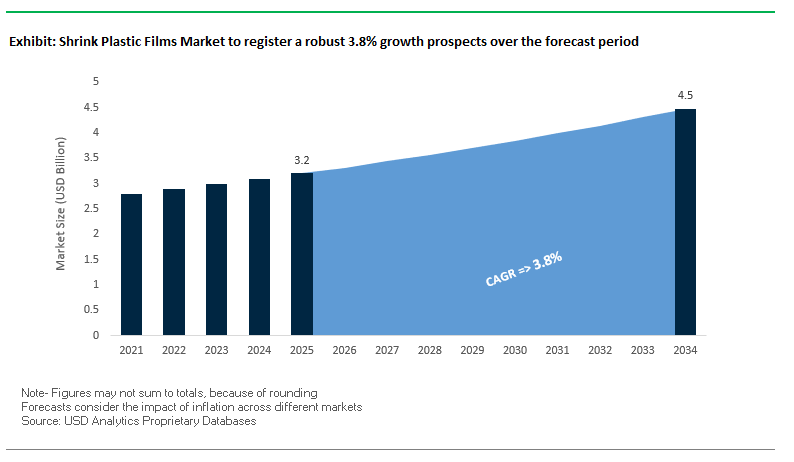

The global shrink plastic films market is projected to grow from $3.2 billion in 2025 to $4.5 billion by 2034, at a CAGR of 3.8%, driven primarily by food and beverage packaging, e-commerce logistics, and sustainability initiatives. Shrink films provide an effective solution for product protection, tamper-evidence, and brand visibility, making them indispensable across frozen foods, beverages, meat, and other perishable items. The surge in online retail has further intensified demand for films that can securely bundle products and protect goods during transit.

Key Insights for Industry Professionals:

- Food and Beverage Lead Consumption: Beverages, frozen foods, and meat products dominate shrink film use due to protection and shelf appeal requirements.

- E-Commerce Growth Drives Packaging Demand: Shrink films offer secure bundling, dust and moisture protection, and tamper-evident sealing for online logistics.

- Sustainability and Recycled Content Trends: Intertape Polymer Group reported 75% of its revenue from recyclable, reusable, or compostable packaging in 2024, highlighting the shift toward a circular economy.

- High Clarity and Graphic Potential: Innovations in printable, high-clarity shrink films combined with digital printing enhance branding and shelf impact.

- Focus on Operational Efficiency: Advanced films enable faster production runs, automated sealing, and reduced waste, increasing profitability.

The market combines product protection, visual appeal, and sustainability, positioning shrink films as a key enabler for modern packaging strategies across food, beverage, and logistics sectors.

Market Analysis: Recent Investments and Sustainable Innovations Are Shaping the Shrink Plastic Films Industry

The shrink plastic films market has witnessed several strategic investments, sustainability initiatives, and technological advancements. In August 2025, Berry Global expanded its Ohio production facility with a $25 million investment, addressing growing demand from the food packaging sector. In July 2025, Sealed Air launched a biodegradable shrink film line in the U.S., aimed at reducing environmental impact while maintaining strength, and Mitsubishi Chemical introduced a next-generation heat-shrink film for high-speed packaging lines in Japan, aligning with sustainable production goals.

Capacity expansions and automation are further enhancing market efficiency. In June 2025, UBE Industries invested $15 million to expand its Osaka facility, increasing industrial and food packaging output. Simultaneously, Mondi expanded its re/cycle MailerBAG capacity, addressing the surge in e-commerce packaging demand. In May 2025, Amcor unveiled an automated shrink film converting unit in Texas, improving supply capabilities for beverage and consumer goods packaging.

Sustainability remains a central theme. In April 2025, Toyo Seikan Kaisha introduced antimicrobial shrink films to enhance hygiene and shelf life for perishables in Japan. Coveris launched SleeveFlexR Stretch, a circular stretch sleeve solution using up to 75% recycled content, emphasizing the industry-wide move toward eco-friendly materials.

Shrink Plastic Films Market: Transitioning Towards Recyclability and Circular Packaging Solutions

Accelerated Material Transition from PVC to PETG and Polyolefins

The shrink plastic films market is undergoing a fundamental transformation driven by the incompatibility of PVC with existing recycling streams. PVC’s high chlorine content and density make it particularly problematic for PET recycling, as it contaminates PET flakes during the sink/float process, significantly reducing the quality of recycled PET. With regulatory scrutiny tightening under the EU Packaging and Packaging Waste Regulation (PPWR) and similar frameworks, brand owners face increasing pressure to eliminate PVC from their packaging portfolios.Corporate commitments are amplifying this shift. A 2024 environmental report from a global CPG leader publicly pledged to phase out PVC as part of its global sustainability roadmap. This transition is not just regulatory compliance—it is also a risk mitigation strategy, enabling companies to avoid material bans and maintain access to major markets. As a result, PETG and polyolefin-based shrink films are rapidly emerging as preferred alternatives, combining printability and shelf appeal with recyclability compatibility.

Development and Adoption of Floatable Sleeve Materials

Another pivotal trend in the shrink films industry is the rise of floatable polyolefin-based shrink films designed specifically to solve recycling challenges. Unlike PVC, these films have a density below 1.0 g/cm³, allowing them to float during sink/float separation while PET bottle flakes sink. This ensures a clean separation process and preserves the value of recycled PET.

The industry’s confidence in this solution has been reinforced by third-party validations. The Association of Plastic Recyclers (APR) has recognized multiple floatable shrink film products as meeting recyclability guidelines, a stamp of credibility that allows brands to make strong sustainability claims. This validation is driving adoption across beverage, personal care, and household product categories, where full-body sleeves play a critical role in branding and shelf visibility but can no longer come at the expense of recyclability.

Advanced Bio-Based and Compostable Shrink Film Formulations

The global shift toward circular and compostable packaging presents a major innovation opportunity in shrink plastic films. Manufacturers are exploring bio-based alternatives such as polylactic acid (PLA), which can achieve industrial composting certification while delivering the necessary clarity, strength, and shrink properties for consumer packaging. Recent developments highlight PLA-based shrink films that offer up to 20% shrink rates, competitive transparency, and robust tensile strength, making them viable for food and beverage packaging applications.

A 2025 academic review on PLA shrink films underscores their biodegradability and environmental benefits but also points to ongoing challenges with barrier performance and heat resistance. Continuous R&D into enhanced barrier coatings and improved resin formulations is expanding the scope of compostable shrink films, particularly for sectors where sustainable branding and waste reduction are crucial. This positions bio-based shrink films as a high-growth niche in markets with strong consumer preference for eco-friendly packaging.

Integration of Digital Watermarking for Smart Packaging and Waste Sorting

Shrink plastic films also represent a prime canvas for digital watermarking technologies that enhance packaging intelligence and waste sorting. The HolyGrail 2.0 initiative, involving over 130 companies, demonstrated that invisible digital watermarks printed on shrink labels can be accurately detected by high-resolution sorting cameras with over 95% purity rates in recycling trials. This enables recyclers to differentiate between food and non-food plastics, streamlining the creation of high-quality recycled materials.

Beyond recycling, digital watermarking turns shrink films into smart packaging tools. These invisible codes can encode detailed information such as material composition, product type, and brand identity, effectively serving as a digital passport for each package. This technology not only enhances recycling efficiency but also supports brand authentication, supply chain traceability, and consumer engagement, giving shrink film packaging a dual role as both a branding and sustainability enabler.

Competitive Landscape: Leading Players Are Driving Innovation and Sustainability in Shrink Plastic Films

The global shrink plastic films market is shaped by key players leveraging material science expertise, production efficiency, and sustainability strategies to provide high-performance packaging solutions across food, beverage, and industrial applications.

Sealed Air Corporation (SEE): Leading Biodegradable and Tamper-Evident Shrink Film Solutions

Sealed Air Corporation (Cryovac® brand) specializes in shrink films for processed meats, poultry, and cheese. In July 2025, it launched a biodegradable shrink film line in the U.S. and partnered with Nextek for food-grade mechanical recycling. SEE’s Net Positive Circular Ecosystem strategy aims to ensure 100% of packaging is recyclable or reusable by 2025, offering tamper-evident solutions for perishable foods.

Amcor plc: Expanding Global Reach Through Automated and Sustainable Shrink Film Technologies

Amcor provides flexible and rigid shrink films for food, beverages, and personal care. Its July 2025 merger with Berry Global created a diversified global packaging leader. In May 2025, Amcor launched an automated shrink film converting unit in Texas, enhancing supply and efficiency. The company also emphasizes sustainability with recyclable films and AmFiber Performance Paper heat-seal sachets, designed for dry food and beverage applications.

Berry Global Group, Inc.: Driving Circular Economy Initiatives in High-Volume Shrink Film Manufacturing

Berry Global offers a broad portfolio of shrink plastic films for food, beverage, and healthcare. In August 2025, it expanded its Ohio production facility by $25 million. The company targets 30% circular plastics in FMCG packaging by 2030, focusing on sustainable, cost-effective, and innovative packaging solutions while maintaining strong manufacturing agility and extensive product range.

Coveris: Advancing Circular Packaging Through Recycled Content and Innovative Sleeve Solutions

Coveris manufactures flexible and rigid shrink films for food, beverage, industrial, and consumer goods. In April 2025, it launched SleeveFlexR Stretch, a circular stretch sleeve with up to 75% recycled content. Coveris emphasizes its No Waste vision, supporting fully recyclable solutions across plastic and paper formats, enhancing sustainability for its customers.

Intertape Polymer Group (IPG): Integrating Sustainable Shrink Films With Advanced Automation Systems

IPG produces shrink films, tapes, and packaging systems for logistics and e-commerce. In 2024, it achieved 75% revenue from recyclable, reusable, or compostable products, meeting sustainability goals a year early. In August 2025, its Chicago facility earned TRUE Gold Zero Waste Certification, and in October 2024, IPG launched iTRACK™ Data Collection System for automated packaging. Its integrated approach provides high-quality, tamper-evident shrink films combined with automation solutions.

Shrink Plastic Films Market Share Insights, 2025-2034

Center-Folded Film Dominates Market Share by Product Type in the Shrink Plastic Films Industry

Center-folded shrink film leads with 45% share of the shrink plastic films market, making it the most widely used format in high-volume packaging operations. Its dominance is rooted in its exceptional versatility and efficiency on automated wrapping lines, where the folded design enables seamless sealing and shrinking around multipacks of beverages, frozen foods, and consumer staples. The format is particularly valued by the food and beverage sector, where tamper evidence, product visibility, and stability during transit are critical. In addition, the ongoing transition from PVC to polyolefin (POF) and PETG enhances its sustainability profile while maintaining the mechanical strength and clarity required by retailers. Flat roll-stock and pre-formed bags hold important roles in specialized and semi-automated packaging, but center-folded film remains the industry standard for speed, cost-effectiveness, and broad application versatility.

Food & Beverages Lead Market Share by End-Use in the Shrink Plastic Films Industry

The food and beverages sector accounts for 50% of shrink plastic film demand, underscoring its role as the core growth driver of the market. Shrink films are indispensable for multi-packing bottled water, soft drinks, canned goods, frozen foods, and fresh produce, ensuring stability in transit, product protection, and enhanced shelf visibility. Modified packaging requirements for cold chain logistics and frozen storage further reinforce demand for films with superior tensile strength, oxygen barrier properties, and low-temperature performance. The increasing adoption of POF films in this sector reflects industry-wide commitments to sustainability, recyclability, and safety compliance, particularly as global regulations accelerate the phaseout of chlorine-based PVC films. While consumer goods, e-commerce logistics, and industrial goods are expanding applications, the food and beverage sector continues to dominate because of its sheer consumption volume and critical hygiene and preservation requirements.

European Union: PPWR and ESPR Regulations Driving Mono-Material Shrink Films

The European Union shrink plastic films market is undergoing a major transformation under the Packaging and Packaging Waste Regulation (PPWR), which became effective in February 2025. By January 2030, all plastic packaging, including shrink films, must contain minimum percentages of post-consumer recycled content, a requirement pushing innovation in circular packaging design. The Ecodesign for Sustainable Products Regulation (ESPR), effective mid-2024, introduces Digital Product Passports (DPPs), demanding transparency on material composition and recyclability, a move directly influencing shrink film producers to shift toward mono-material solutions.

The upcoming PFAS ban in food contact materials (August 2026) is accelerating the search for alternative barrier coatings. A significant trend is the adoption of perforated shrink films, allowing consumers to easily separate films from bottles or containers, improving recyclability rates. Companies such as Berry Global have already committed to sustainability, announcing in April 2024 that they would produce shrink films from post-consumer recycled (PCR) plastics, demonstrating the region’s strong regulatory push toward circularity.

United States: EPR Laws and Recycling Infrastructure Fueling Market Growth

The United States shrink plastic films market is being reshaped by state-level Extended Producer Responsibility (EPR) laws, now enacted in seven states, with Maryland mandating Producer Responsibility Organizations (PROs) to cover at least 90% of packaging waste management costs by 2030. This, coupled with the U.S. Environmental Protection Agency’s (EPA) national recycling goal of 50% by 2030, is driving packaging manufacturers to redesign shrink films for recyclability and sustainability.

A landmark development occurred in November 2022, when WM and Dow launched a collaboration to enable curbside recycling of hard-to-recycle plastic films, including shrink films, showcasing an industry-wide shift toward circular waste management. The Association of Plastic Recyclers (APR) is guiding best practices with recommendations such as washable inks and floatable films, which enhance PET bottle recyclability. At the same time, demand is surging in e-commerce, food & beverage, and logistics sectors, where high-performance shrink films are essential for supply chain durability and automation compatibility.

China: E-Commerce and Luxury Packaging Trends Accelerating Shrink Film Demand

The China shrink plastic films market is influenced heavily by regulatory reforms and consumer-driven trends. Effective June 1, 2025, new regulations require express delivery companies to adopt eco-friendly and reusable packaging, reinforcing the adoption of sustainable shrink films. Additionally, the 14th Five-Year Plan, under the leadership of the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE), prioritizes stricter controls on plastic pollution, boosting the development of recyclable flexible packaging formats.

Market demand is fueled by the rise of premium and luxury packaging, where advanced printing technologies such as 3D embossing, holographic finishes, and foil stamping are being used to create visually striking shrink films that serve branding as well as tamper-evidence functions. Simultaneously, the country’s booming e-commerce sector is driving demand for lightweight, durable shrink films that reduce logistics costs while protecting products during last-mile delivery.

India: EPR Rules and Barcode Traceability Strengthening Shrink Film Regulations

The India shrink plastic films market is regulated by the Plastic Waste Management (Amendment) Rules, 2024, which place a strong emphasis on Extended Producer Responsibility (EPR) for producers, importers, and brand owners. Effective July 1, 2025, all plastic packaging—including shrink films—must carry a barcode or QR code for traceability, ensuring accountability across the packaging supply chain. However, MSMEs are exempt from EPR obligations, shifting the compliance burden onto larger players and importers.

Demand is being driven by the e-commerce boom and rapid retail sector expansion, both of which rely on shrink plastic films for efficient bundling, protection, and branding of products. As sustainability pressures rise, local manufacturers are increasingly adopting PCR-based materials and recyclable shrink films to remain compliant with regulations while meeting growing consumer and brand-owner expectations for eco-friendly packaging.

Japan: Circular Economy Laws Shaping Sustainable Shrink Film Adoption

The Japan shrink plastic films market is advancing under the Plastic Resource Circulation Strategy, which mandates that all plastic packaging be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, also effective in 2025, enforces the reduction or redesign of 12 categories of single-use plastics, compelling manufacturers to rethink shrink film production in favor of compostable or recyclable solutions.

The government’s goal of doubling renewable material use by 2030 is driving companies to experiment with bio-based polymers and hybrid paper-film solutions. Japan’s emphasis on waste sorting at collection ensures that shrink films, which have historically been difficult to recycle, are being integrated into advanced material recovery systems. This positions Japan as a leader in innovative shrink film materials with reduced carbon footprints.

Brazil: PNRS and Reverse Logistics Strengthening Domestic Shrink Film Market

The Brazil shrink plastic films market is guided by the National Solid Waste Policy (PNRS), which emphasizes reuse, recycling, and responsible waste management. A pivotal reform came with Law No. 15,088 (January 2025), banning the import of solid waste—including plastics—to promote domestic recycling infrastructure and reduce reliance on foreign disposal.

The government is also strengthening reverse logistics systems, requiring producers to take responsibility for the post-consumer collection and disposal of shrink films. With Brazil’s growing food & beverage and retail industries, shrink films are seeing wider adoption for product protection and extended shelf life. Local converters are aligning with regulations by investing in film downgauging, water-based inks, and recyclable mono-material films, aligning market growth with sustainability priorities.

Shrink Plastic Films Market Report Scope

Shrink Plastic Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.2 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Material (PE, PP, POF, PVC, Bioplastics), By Product Type (Flat Roll-stock, Center-folded Film, Pre-formed Bags), By Application (Bundling & Multipacks, Individual Product Wrapping, Tamper-Evident Seals, Protective Coverings), By End-Use Industry (Food & Beverages, Consumer Goods, E-commerce & Logistics, Pharmaceuticals, Building & Construction, Industrial Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Amcor plc, Berry Global, Inc., Coveris Holdings S.A., Intertape Polymer Group Inc., Huhtamaki Oyj, Mondi Group, Dow Inc., Sonoco Products Company, Transcontinental Inc., Winpak Ltd., Klöckner Pentaplast, RKW Group, Novolex, Polyrafia

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Shrink Plastic Films Market Segmentation

By Material

- PE

- PP

- POF

- PVC

- Bioplastics

By Product Type

- Flat Roll-stock

- Center-folded Film

- Pre-formed Bags

By Application

- Bundling & Multipacks

- Individual Product Wrapping

- Tamper-Evident Seals

- Protective Coverings

By End-Use Industry

- Food & Beverages

- Consumer Goods

- E-commerce & Logistics

- Pharmaceuticals

- Building & Construction

- Industrial Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Shrink Plastic Films Market

- Sealed Air Corporation

- Amcor plc

- Berry Global, Inc.

- Coveris Holdings S.A.

- Intertape Polymer Group Inc.

- Huhtamaki Oyj

- Mondi Group

- Dow Inc.

- Sonoco Products Company

- Transcontinental Inc.

- Winpak Ltd.

- Klöckner Pentaplast

- RKW Group

- Novolex

- Polyrafia

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-step research methodology to provide authoritative insights into the global shrink plastic films market. Our approach integrates comprehensive secondary research from corporate disclosures, regulatory filings, patent databases, industry journals, sustainability reports, and market news, combined with primary research via interviews with packaging engineers, sustainability managers, supply chain specialists, and brand owners. Market sizing and forecasts are segmented by material type (PE, PP, POF, PVC, bioplastics), product type (flat roll-stock, center-folded film, pre-formed bags), application (bundling & multipacks, individual product wrapping, tamper-evident seals, protective coverings), and end-use industries (food & beverages, consumer goods, e-commerce & logistics, pharmaceuticals, building & construction, industrial goods). USDAnalytics evaluates growth drivers including e-commerce expansion, food & beverage demand, sustainability initiatives, regulatory mandates like PPWR, EPR, and Japan’s circular economy laws, and innovations in recyclable, compostable, and bio-based films. Competitive intelligence analyzes strategic investments, capacity expansions, automation, and digital printing technologies adopted by industry leaders such as Sealed Air, Amcor, Berry Global, Coveris, and Intertape Polymer Group, providing actionable insights for professionals seeking to optimize packaging performance, compliance, and sustainability in this evolving market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.