Silage Cover Market Size, Overview, and Growth Outlook (2025–2034)

Global Silage Cover Market Poised to Reach $3.9 Billion by 2034 Driven by Advanced Livestock Feeding and Sustainable Film Innovations

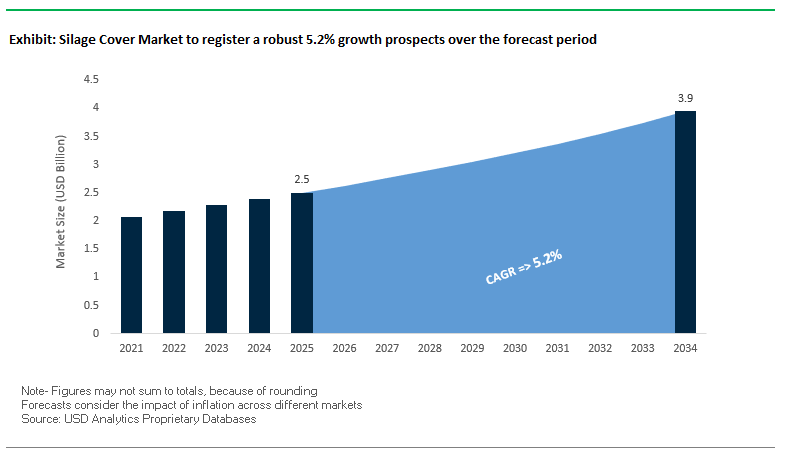

The global silage cover market is projected to grow from $2.5 billion in 2025 to $3.9 billion by 2034, at a CAGR of 5.2%, fueled by increasing adoption of silage films in livestock feeding, advances in multilayer film technology, and sustainability trends. Silage covers are critical for preserving forage quality, preventing spoilage, and enhancing farm productivity, particularly in dairy and beef cattle operations. Modern agricultural practices, including automated balers and film-wrapping attachments, are further driving market adoption.

Key Insights for Industry Professionals:

- Livestock Feeding Dominates Market Use: USDA data shows 63% of dairy farmers report higher feed preservation using silage films, underscoring the importance of protective covers.

- Multilayer Films Offer Superior Preservation: Over 75% of market volume comes from multilayer films providing strength, durability, and high oxygen barriers.

- Modern Farming Techniques Increase Efficiency: More than 55% of silage balers now include film-wrapping attachments, reflecting automation trends in forage preservation.

- Bio-Based Films Highlight Sustainability Focus: In 2024, bio-based silage films accounted for over 18% of new global launches, emphasizing eco-friendly innovation.

- Enhanced Product Protection and Operational Ease: Advanced films reduce labor, improve silage longevity, and ensure consistent forage quality across farms.

The market is positioned at the intersection of agricultural efficiency, product innovation, and sustainability, making it critical for farmers, distributors, and packaging professionals to monitor technological and regulatory trends.

Market Analysis: Strategic Mergers, Technological Advancements, and Sustainability Initiatives Are Transforming the Silage Cover Industry

The silage cover market has witnessed significant mergers, acquisitions, and product innovations, reflecting an industry focused on expansion and sustainability. In August 2025, Constantia Flexibles completed its acquisition of Aluflexpack, strengthening its footprint in high-value agricultural films. July 2025 saw a European player acquire a U.S.-based specialist in high-performance adhesives, expanding its North American market presence. In June 2025, Mondi launched sustainable sachet solutions for pet food, demonstrating expertise in functional, eco-friendly packaging.

Operational efficiency and portfolio expansion remain central to market dynamics. In May 2025, a merger between two European adhesive players created a leader in high-performance solutions, while April 2025 witnessed the launch of a new polyethylene surface protection film tape, catering to manufacturing and shipping protection needs. The market also emphasizes automation and data-driven efficiency, exemplified by IPG’s iTRACK™ Data Collection System in October 2024 and consecutive “Vendor of the Year” awards recognizing operational excellence.

Silage Cover Market: Driving Innovation in Barrier Films and Sustainable Alternatives

Adoption of High-Oxygen-Barrier Films with Enhanced Durability

The silage cover market is rapidly shifting toward multi-layer films with high oxygen barrier properties, particularly those incorporating ethylene vinyl alcohol (EVOH) layers. Studies have demonstrated that EVOH-based films achieve a much lower oxygen transmission rate (OTR) than conventional polyethylene (PE) films, directly reducing spoilage and dry matter losses. In a comparative trial, silage stored under EVOH films maintained superior forage integrity for 170 days, showcasing better fermentative stability and nutritional quality than traditional PE films.

The adoption of these advanced films is being accelerated by livestock producers who require reliable preservation solutions to optimize feed efficiency and animal health. High-barrier silage covers also reduce the risk of mycotoxin formation and nutrient degradation, ensuring higher milk yields and livestock productivity. With margins in the dairy and livestock sector under pressure, the shift toward high-barrier EVOH silage films is becoming a critical investment for long-term operational efficiency.

Integration of Additives for UV Protection and Strength

Manufacturers are increasingly enhancing silage films with UV stabilizers and strength-enhancing additives to improve performance in demanding agricultural environments. UV degradation is a major issue for silage covers exposed to prolonged sunlight, often leading to chalking, brittleness, and tears. Technical specifications from agricultural film producers highlight the integration of specialized UV stabilizer masterbatches that extend film longevity, ensuring consistent performance over multiple seasons.

In addition to UV protection, additives such as anti-slip agents are being incorporated to improve bale stability and handling efficiency. These enhancements minimize the risk of stacked bales sliding during transport and storage, preserving the critical anaerobic conditions needed for silage conservation. The result is a new generation of durable, user-friendly silage films that combine protective performance with improved operational practicality.

Development of Truly Biodegradable or Biodegradable-in-Soil Films

One of the most pressing challenges in the silage cover market is end-of-life disposal. Traditional PE-based films are rarely recycled due to contamination with silage residues, leading to environmentally damaging practices such as open burning or burying. This issue is driving significant demand for biodegradable alternatives that can decompose safely in soil without leaving behind microplastics.

A feasibility study at Hof University of Applied Sciences demonstrated the potential of biodegradable films like Mater-Bi®, which successfully covered silage for up to 110 days while maintaining forage quality comparable to conventional PE films. These early trials highlight the commercial viability of bio-based silage covers that align with circular economy goals. For farmers, biodegradable silage films could reduce waste management costs and improve compliance with tightening agricultural sustainability regulations, particularly in the EU and North America.

Incorporation of Oxygen-Scavenging Technology

Beyond passive barrier solutions, the future of silage covers lies in active oxygen management. Oxygen-scavenging technology, already established in food and pharmaceutical packaging, is now being explored for agricultural use. Films embedded with oxygen scavengers can reduce internal oxygen concentrations to below 0.1%, a level significantly lower than standard barriers can achieve.

Applied to silage, this technology could extend preservation periods, reduce lipid oxidation, and inhibit microbial activity, even in cases of imperfect sealing or micro-perforations. By actively preventing spoilage, oxygen-scavenging silage films would help farmers minimize dry matter loss, improve forage quality, and ultimately enhance feed efficiency. As adoption of precision agriculture practices grows, oxygen-scavenging silage covers are poised to become a premium solution in high-value livestock operations where feed quality directly impacts profitability.

Competitive Landscape: Leading Silage Cover Manufacturers Are Driving Innovation, Sustainability, and Operational Efficiency

The global silage cover market is shaped by specialized film manufacturers leveraging oxygen barrier technology, sustainable materials, and advanced production capabilities to deliver high-quality silage protection solutions.

Silostop Agri: Pioneering High Oxygen Barrier Films to Minimize Dry Matter Losses

Silostop Agri specializes in High Oxygen Barrier (HOB) silage films and covers, engineered with industry-leading Oxygen Transmission Rates (OTR). In July 2023, the company launched Silostop Complete, a UV-stable, one-step cover that eliminates the need for nets. Its HOB technology can reduce dry matter losses in the top three feet of a bunker by over 40%, offering fully recyclable solutions that simplify application and save labor for farmers.

Trioworld: Advancing Sustainable and Bio-Based Silage Films for Efficient Forage Preservation

Trioworld produces silage wrap and stretch films known for durability and oxygen/moisture protection. The company emphasizes sustainable, high-performance films, actively developing bio-based films with high elongation, reducing tearing and material usage. Its innovations align with the circular economy and ensure consistent forage quality and UV protection, reinforcing its market leadership.

RKW Group: Delivering Functional and Technologically Advanced Silage Films for Global Agriculture

RKW Group manufactures a wide range of silage sheets, stretch films, and agricultural films. Its strategy focuses on portfolio optimization and new growth areas, with investments in R&D for innovative and sustainable solutions. RKW’s products provide thermal management, oxygen barriers, and UV resistance, supporting applications from general packaging to specialized agricultural needs.

Berry Global Group, Inc.: Expanding Sustainable Shrink Film Capacity to Meet Global Agricultural Demands

Berry Global produces silage films for agriculture, food, and beverage industries. In August 2025, it expanded its Ohio facility with a $25 million investment, increasing production to meet growing demand. The company emphasizes 30% circular plastics usage in FMCG packaging by 2030, combining innovative, cost-effective, and sustainable solutions with strong manufacturing agility.

Barbier Group: Innovating Mono-Material and UV-Resistant Silage Films for Environmental and Operational Efficiency

Barbier Group focuses on silage, stretch, and greenhouse films, emphasizing sustainability, high UV protection, and durability. Its research centers on innovative mono-material solutions that are recyclable within existing infrastructures, enhancing both environmental sustainability and silage preservation, making it a key European market player.

Silage Cover Market Share Insights, 2025-2034

Silage Bunker Film Leads Market Share by Film Type in the Silage Cover Industry

Silage bunker film holds 40% of the silage cover market, making it the single largest segment within this specialized agricultural packaging sector. Its dominance stems from its indispensable role in covering bunker silos and drive-over piles, which remain the most widely adopted and cost-efficient feed storage systems for large-scale livestock producers. These heavy-duty, multi-layer films must combine superior tensile strength, advanced oxygen barrier properties, and UV resistance to preserve forage quality over long storage periods while withstanding harsh environmental conditions. The growing adoption of co-extruded EVOH barrier layers and UV-stabilized polyethylene blends ensures that silage bunker films remain essential for modern intensive dairy and beef operations. While silage wrap, bag, and tube films serve critical niches, bunker films dominate because of their scale efficiency and ability to protect massive feed volumes at the lowest cost per ton stored.

Bunker Silos Dominate Market Share by Application in the Silage Cover Industry

Bunker silos account for 45% of application share in the silage cover industry, highlighting their unmatched role in large-scale, cost-efficient feed storage. Favored by commercial dairy and beef operations, bunker silos allow farmers to store thousands of tons of silage at once, requiring the use of extensive, highly durable films that provide airtight seals, weather resistance, and UV stability. The application typically combines bunker films with protective weights and sealing layers, ensuring minimized oxygen ingress and feed spoilage. Their widespread adoption is directly linked to economies of scale in industrial livestock production, where feed preservation efficiency directly impacts profitability. Although baled silage and drive-over piles are increasingly used by medium and smaller farms, bunker silos remain the backbone of intensive livestock feed management, securing their leading position in global silage cover demand.

United States: Recycling Goals and Smart Silage Covers Reshaping the Market

The United States silage cover market is heavily influenced by sustainability regulations and technological advancements. The U.S. Environmental Protection Agency (EPA) has set a national target to raise the recycling rate to 50% by 2030, which is directly impacting investment in recycling infrastructure for agricultural films. Additionally, seven states have implemented Extended Producer Responsibility (EPR) laws, with Maryland mandating that Producer Responsibility Organizations (PROs) fund at least 90% of packaging waste management by 2030. These policies are pushing manufacturers toward recyclable silage covers.

Market trends also highlight rising demand for high-performance silage covers tailored for large-scale bunkers, individual bales, and advanced feed storage solutions. Farmers are increasingly adopting smart silage covers equipped with sensors to monitor temperature and moisture, enabling better control of the ensiling process and reducing feed spoilage. Investments supported by the Infrastructure Investment and Jobs Act are driving local production and recycling facilities, ensuring that innovation and compliance align with sustainability objectives.

European Union: PPWR and ESPR Driving Circular Economy in Silage Covers

The European Union silage cover market is being transformed by the Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which sets ambitious reuse and recycled content targets for all packaging, including agricultural films. This is accelerating the development of mono-material silage covers and paper-based solutions that can be more easily recycled. Similarly, the Ecodesign for Sustainable Products Regulation (ESPR), effective mid-2024, requires a Digital Product Passport (DPP) to enhance traceability and compliance across the supply chain.

The upcoming PFAS ban in food contact packaging (August 2026) is fueling innovation in alternative barrier technologies for silage covers. Manufacturers such as Rani Plast are leading the shift by producing silage films made from recyclable raw materials. Combined with EU-wide efforts to boost circular agriculture and sustainable farming, these developments are making the region a hub for eco-friendly silage cover innovation.

China: Advanced Agricultural Technologies and Green Policies Boost Demand

The China silage cover market is shaped by both regulatory reforms and rising agricultural modernization. Under the 14th Five-Year Plan, the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are tightening policies on plastic pollution control. Effective June 1, 2025, express delivery companies must prioritize eco-friendly and reusable packaging, indirectly boosting demand for recyclable agricultural films.

China is experiencing rising demand for premium agricultural products, which has led to the adoption of sophisticated silage covers featuring enhanced oxygen barriers and UV stabilization to protect feed quality. Additionally, tax incentives for remanufacturing and green technology adoption are encouraging domestic producers to scale up sustainable silage cover production, making the market increasingly competitive and innovation-driven.

India: Dairy Sector Expansion and EPR Driving Market Adoption

The India silage cover market is undergoing rapid transformation, fueled by regulatory reforms and agricultural modernization. The Plastic Waste Management (Amendment) Rules, 2024, effective April 2025, place strong emphasis on Extended Producer Responsibility (EPR), requiring silage cover manufacturers to account for recycling and safe disposal. From July 1, 2025, all plastic packaging must include barcode or QR code traceability, enhancing accountability across the agricultural packaging value chain.

The Punjab Agro Industries Corporation Limited (PAIC) has invested Rs. 8.02 Cr. in a silage-making project with advanced imported machinery, underscoring the government’s efforts to modernize silage adoption in agriculture. Rising silage usage is also linked to India’s dairy sector productivity goals, as the government promotes feed efficiency and storage quality. The market is additionally shaped by exemptions for MSMEs, shifting responsibility to large manufacturers and importers, while boosting the adoption of modern silage cover technologies.

Japan: Plastic Circulation Laws Driving Paper-Based Agricultural Alternatives

The Japan silage cover market is influenced by the Plastic Resource Circulation Strategy, which requires all plastic packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law (2025) further enforces the reduction or redesign of 12 single-use plastic categories, pushing companies to explore biodegradable and paper-based silage covers.

Japan’s goal to double renewable material usage by 2030 and strict waste sorting at collection points provide a strong foundation for sustainable agricultural packaging adoption. With its advanced R&D ecosystem, Japan is expected to lead in innovative silage cover solutions that balance durability, recyclability, and environmental compliance.

Brazil: Reverse Logistics and PNRS Strengthening Domestic Market Regulations

The Brazil silage cover market is driven by the National Solid Waste Policy (PNRS), which emphasizes reuse, recycling, and sustainable waste management. The introduction of Law No. 15,088 in January 2025, banning the import of solid waste including plastics, reinforces domestic recycling and sustainability practices.

The Brazilian government is also investing in reverse logistics systems, requiring producers to manage the post-consumer collection and recycling of silage covers. With the country’s growing focus on livestock and feed preservation, silage covers are becoming critical in minimizing agricultural losses. Local manufacturers are aligning with government initiatives by developing eco-friendly silage films, ensuring compliance while supporting the agricultural sector’s demand for durable and recyclable solutions.

Silage Cover Market Report Scope

Silage Cover Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.5 Billion

|

|

Market Size (2034)

|

$3.9 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Film Type (Silage Wrap Film, Silage Bunker Film, Silage Tube Film, Silage Bag Film), By Material (PE, EVA, EVOH, PA, PP), By Application (Bunker Silos, Silage Bales, Silage Piles), By Color (Black, White, Green, Black & White, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Armando Alvarez Group, Silotite, Karatzis S.A., Berry Global, Inc., RKW Group, Ab Rani Plast Oy, Trioplast Industrier AB, Tama Plastic Industry, Zill GmbH & Co. KG, Sotrafa, S.A., Ginegar Plastic Inc., Coveris Holdings S.A., RKW Agri GmbH & Co. KG, RPC Group Plc, Barbier Groupe

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silage Cover Market Segmentation

By Film Type

- Silage Wrap Film

- Silage Bunker Film

- Silage Tube Film

- Silage Bag Film

By Material

By Application

- Bunker Silos

- Silage Bales

- Silage Piles

By Color

- Black

- White

- Green

- Black & White

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Silage Cover Market

- Armando Alvarez Group

- Silotite

- Karatzis S.A.

- Berry Global, Inc.

- RKW Group

- Ab Rani Plast Oy

- Trioplast Industrier AB

- Tama Plastic Industry

- Zill GmbH & Co. KG

- Sotrafa, S.A.

- Ginegar Plastic Inc.

- Coveris Holdings S.A.

- RKW Agri GmbH & Co. KG

- RPC Group Plc

- Barbier Groupe

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver precise insights into the global silage cover market. Our approach combines extensive secondary research from company disclosures, sustainability and regulatory reports, patent databases, industry journals, and agricultural market publications, with primary research conducted through interviews with farmers, agronomists, packaging engineers, and supply chain managers. Market sizing and forecasts are segmented by film type (silage wrap, bunker, tube, and bag films), material (PE, EVA, EVOH, PA, PP), application (bunker silos, silage bales, silage piles), and color (black, white, green, black & white, others), while also evaluating adoption trends in major regions including the United States, EU, China, India, Japan, and Brazil. USDAnalytics examines growth drivers such as livestock feeding efficiency, multilayer and high oxygen barrier technologies, automation in silage wrapping, and sustainability innovations including bio-based and biodegradable films. Competitive intelligence covers strategic mergers, capacity expansions, and technological advancements by leading players such as Silostop Agri, Trioworld, RKW Group, Berry Global, and Barbier Group, offering actionable insights on operational efficiency, regulatory compliance, and sustainable packaging adoption across the agricultural sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.