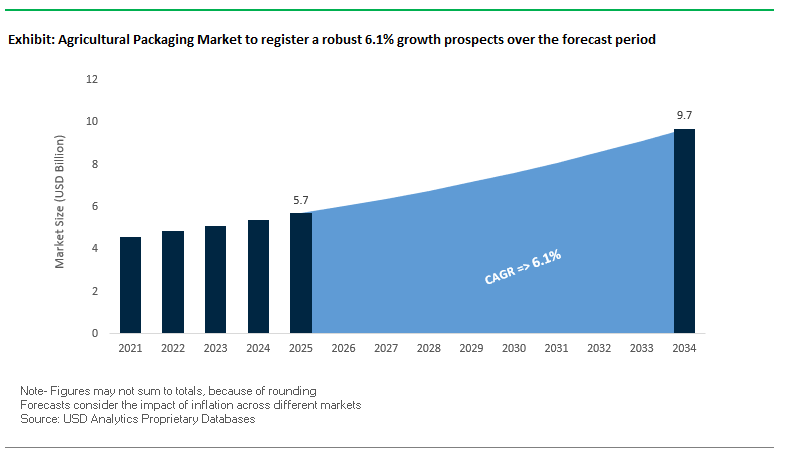

Market overview: shelf-life extension, bulk bags, and PCR plastics lift the market from $5.7B (2025) to $9.7B (2034) at 6.1% CAGR

Executive overview for procurement, operations, and sustainability leaders. The global agricultural packaging market underpins waste reduction from farm to fork by protecting quality during post-harvest handling, storage, and transport. Performance requirements diverge across bulk logistics (IBCs, FIBCs/bulk bags, drums) and consumer-ready formats for retail/SMB channels. Material selection is pragmatic plastics (especially HDPE) dominate for agrochemical containers, seed/fertilizer sacks, liners, while paper-based high-strength solutions expand share in fresh produce and dry goods. Strategy is shifting toward PCR content, recyclable mono-materials, and designs that balance barrier, venting, and moisture management to extend shelf life and lower total landed cost.

Key Insights for professionals

- Food waste reduction lever: Fit-for-purpose agri packaging diminishes losses during harvest, consolidation, and long-haul a direct P&L and ESG win.

- Plastics + bags dominate: HDPE and bulk bags (FIBC) remain first choice for grains, fertilizers, seeds due to durability, chemical resistance, and lightweight logistics.

- Sustainable pivot: Growth in paper-based high-strength sacks and PCR plastics for agrochem improves recyclability and compliance with evolving regulations.

- Format bifurcation: Bulk IBCs/large bags for upstream efficiency vs. consumer-friendly pack sizes for retail and smallholder markets.

- Design priorities: Venting (e.g., produce), moisture/UV barrier (seeds/fertilizer), tamper evidence (agrochem), and e-commerce readiness for direct-to-farm channels.

Market Analysis: 2021–2025 signals circular infrastructure, paper-based strength, and flexible upgrades for agri supply chains

Industry activity in 2025 reinforced capacity and circularity. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, extending high-reliability converting and quality systems that also serve food and agricultural applications in the region. The same month, Mauser Packaging Solutions opened a reconditioning and recycling facility at BASF’s Tarragona (Spain) site, scaling closed-loop IBC/drum programs critical for agrochemicals and liquid fertilizers. Also in July 2025, Greif agreed to sell its Containerboard Business for USD 1.8B to focus on its core industrial packaging platforms that service agricultural inputs and bulk logistics; Huhtamaki earned its fifth EcoVadis Gold (July 2025), echoing buyers’ preference for verified ESG credentials across agri value chains.

Concurrently, fiber and flexibles advanced sustainable options. DS Smith’s PackRight 2.0 (July 2024) introduced a collaborative route to optimize corrugated systems for produce and agri e-commerce, while Mondi + Saga Nutrition (June 2024) rolled out a recyclable solution in pet nutrition adjacent learnings for feed and specialty agri packaging. Earlier innovations set the trajectory: Mondi x Meade Farm Group (May 2021) delivered paper-based high-strength potato packaging, raising the ceiling on fiber’s load-bearing capability and print impact for produce; Polysack + Flessofab (June 2021) launched recyclable stand-up pouches, widening flexible-pack options for seeds, granules, and agri consumables.

Key Innovations and Strategic Opportunities Driving the Agricultural Packaging Market

Strategic Shift Towards Reusable and Returnable Transport Packaging (RTP) Systems

The agricultural packaging industry is witnessing a strong transition towards reusable and returnable transport packaging (RTP) systems. Major producers and distributors are investing in durable, tracked containers that move beyond single-use corrugated boxes or wooden pallets. RTPs reduce product damage, especially for delicate produce such as berries or grapes, by maintaining product integrity during transit. Standardized reusable containers, as offered by companies like Schoeller Allibert, enhance supply chain efficiency through compatibility with automated sorting, stacking, and washing systems, significantly reducing labor costs and accelerating operations. Additionally, reusable packaging reduces environmental impact by lowering carbon emissions and cutting down on single-use material waste, helping large agricultural corporations and retailers meet stringent Scope 3 emissions targets.

Integration of Smart Packaging Technologies for Traceability and Quality Monitoring

Smart agricultural packaging is rapidly evolving, driven by food safety regulations and consumer demand for transparency. Packaging now functions as an active data carrier, embedding QR codes, NFC tags, and sensor technologies to monitor freshness and provide full supply chain visibility. Real-time IoT-enabled condition monitoring alerts stakeholders when temperature deviations or spoilage risks occur during transit, protecting product quality. Enhanced smart packaging features also enable rapid source identification during recalls, improving food safety and regulatory compliance. Moreover, QR codes and other interactive features build consumer trust by offering detailed provenance information, including farm origin and transportation journey, fostering brand loyalty and transparency in the agricultural supply chain.

Development of High-Performance Bio-Based and Biodegradable Films

There is a significant growth opportunity in developing biodegradable and compostable films that replace conventional plastic mulch, silage wrap, and product bags. Agricultural plastic waste, especially from mulch films, accumulates in soils, contributing to microplastic pollution and impacting soil health. Biodegradable films made from materials such as polybutylene succinate (PBS) or polylactic acid (PLA) now match conventional polyethylene in weed control and moisture retention, as demonstrated by field trials in Spain. By allowing these films to break down directly in the soil, farmers can eliminate collection and disposal efforts, creating a sustainable, circular solution that addresses regulatory pressures and environmental concerns.

Standardization and Adoption of Blockchain-Enabled Traceability Systems

Blockchain-enabled traceability represents a major opportunity to move beyond proprietary smart packaging systems. By creating an immutable, transparent ledger, blockchain ensures end-to-end visibility from farm to fork, maximizing value for all supply chain participants. Decentralized blockchain solutions eliminate data silos, facilitating information sharing between farmers, distributors, and retailers. Real-world implementations by global tech companies allow consumers to scan QR codes and access verifiable product journeys, enhancing trust, preventing fraud, and ensuring compliance with food safety regulations. Adoption of standardized blockchain platforms can transform agricultural supply chains by integrating traceability, sustainability, and consumer engagement into a unified system.

Competitive Landscape: circular IBC fleets, fiber innovation, and high-barrier flexibles set the pace

A concentrated set of global players differentiates on life-cycle services (recondition/reuse), vertically integrated fiber systems, and high-barrier flexible technology. Scale, certification, and regional service density are the key moats.

Mauser Packaging Solutions Circular IBCs and reconditioning built for agrochem logistics

Mauser delivers rigid industrial packaging plastic/steel drums and IBCs for agrochemicals, fertilizers, and farm inputs. The Poly-MT IBC is a reusable, smart, heavy-duty platform that reduces carbon intensity and enables digital fleet visibility (location/fill/condition). A global reconditioning & recycling network underpins multi-cycle reuse, lowering total cost and waste. Strategically, Mauser covers the full life cycle (design → manufacture → recondition → recycle) from 170+ sites, acting as a one-stop partner for multinationals standardizing safe, compliant bulk movement of liquids and powders.

Smurfit WestRock Paper-based systems for produce, seeds, and moisture-managed transit

Formed by the Smurfit Kappa + WestRock merger (Dec 2024), Smurfit WestRock is a fiber powerhouse supplying corrugated bulk containers, trays, bags, and retail-ready formats to agriculture. Its offer includes EnduraGrip (paper grip packs for produce handling) and EverGrow (moisture-resistant packaging for fresh fruits/vegetables), balancing strength, print impact, and recyclability. With a vertically integrated fiber loop, the company aligns recycled content, right-weighting, and fit-to-product automation to cut damage, cube waste, and emissions across regional and export lanes.

Amcor plc High-barrier flexibles and recyclable laminates for seeds, fertilizers, and farm consumables

Amcor supplies bags, pouches, and films for seeds, fertilizers, lawn & garden, and plant protection. Its AmLite Recyclable (metal-free, high-barrier) targets markets with polyolefin recycling streams, while Vento integrates venting into barrier laminates to manage respiration and freshness. GoSmart CanSealPro adds aluminum membrane sealing with strong barrier and tamper evidence for rigid ends. Strategy centers on recyclable/mono-material architectures and a 2025 goal for universal recyclability/reusability, giving buyers validated pathways to reduce scope-3 while maintaining shelf-life specs.

Mondi Group Functional Barrier Papers and performance sacks for feed, seed, and fertilizers

Mondi spans paper + flexible solutions with a material-neutral approach. Functional Barrier Paper provides fiber-based, recyclable alternatives with tailored grease/moisture/oxygen protection in European streams, while paper sacks and bags serve seeds, fertilizers, and animal feed with print-ready, high-strength structures. The Mondi–Meade Farm collaboration (potatoes, May 2021) showcased load-bearing fiber for produce, and Mondi’s vertical integration from forest management to converting tightens QA and traceability crucial for food safety and agrochem compliance.

Agricultural Packaging Market Share Insights

Flexible Intermediate Bulk Containers (FIBCs) Lead Market Share by Product Type in the Agricultural Packaging Industry

FIBCs dominate the agricultural packaging market with a projected 35% share, underscoring their role as the backbone of bulk logistics for fertilizers, animal feed, and dry agricultural inputs. Their cost-per-ton efficiency, collapsibility for return transport, and ease of disposal or recycling make them indispensable in global trade. Pouches and bags, holding 30%, remain the small-volume workhorse, critical for seeds, pesticides, and specialty fertilizers where barrier protection and portion control are essential. Intermediate Bulk Containers (IBCs) are rapidly gaining ground, particularly for liquid fertilizers and pesticides, where safety, reusability, and optimized cube utilization displace drums. Drums still serve a legacy role in hazardous chemical containment, particularly in markets with less developed bulk handling infrastructure. Bottles and cans, while the smallest segment, serve high-value applications like concentrated agrochemicals and plant growth regulators, where precision dosing and engineered closures are critical. Collectively, segmentation reflects a dual system where bulk packaging drives scale and smaller formats enable precision agriculture.

Agriculture Dominates Market Share by End-Use in the Agricultural Packaging Industry

Agriculture secures the largest end-use share at 55%, reflecting the industry’s reliance on packaging for fertilizers, pesticides, herbicides, and feed that directly impact farm productivity. This dominance is amplified by global agricultural output cycles and commodity price movements, which dictate input consumption. The chemicals sector holds a substantial share as the upstream formulator and supplier of active ingredients, demanding packaging formats like UN-certified drums and IBCs to ensure safe handling of hazardous products. Food and beverages, while a smaller share, represent the input supply chain through packaging for additives, feed supplements, and processing aids that ultimately enter the human food chain. Horticulture, the specialty niche, utilizes smaller bags and decorative packaging for nursery products, potting mixes, and ornamental seeds where branding at garden centers and moisture protection play a pivotal role. This segmentation highlights how regulatory compliance, logistics efficiency, and brand trust dictate packaging demand across agricultural value chains.

United States: Regulatory Pressure and Smart Packaging Driving Market Growth

The United States agricultural packaging market is undergoing a rapid transformation fueled by regulatory changes, corporate initiatives, and technological innovations. State-level Extended Producer Responsibility (EPR) laws are reshaping the industry by placing the cost of waste management on producers, which is pushing companies to adopt recyclable and sustainable materials. At the same time, technological innovation is central to U.S. packaging, with AI-powered recycling systems being deployed to sort and process agricultural packaging materials more efficiently than ever before. Leading players such as Greif, Inc. are developing reusable and eco-friendly drums from recycled inputs, underlining the strong focus on reducing carbon footprints across agricultural packaging supply chains.

The U.S. market also stands out as a global leader in smart packaging adoption. The integration of RFID tags, QR codes, and real-time sensors is gaining traction in agriculture, particularly in protecting perishable produce through continuous monitoring of temperature and humidity levels. Additionally, major infrastructure investments such as Schütz Container Systems’ $31 million expansion in Missouri signal growing demand for intermediate bulk containers (IBCs) tailored to agricultural chemicals, fertilizers, and pesticides. The strong demand for specialized chemical packaging solutions underscores the country’s dual focus on safety and sustainability while positioning the U.S. as a hub for high-value packaging innovation.

China: Dual Carbon Goals and Industrial Internet Reshape Agricultural Packaging

China’s agricultural packaging industry is experiencing a pivotal shift as the government pushes forward its “dual carbon” agenda aimed at achieving peak carbon emissions and carbon neutrality. New regulations effective June 2025 are set to transform packaging standards by requiring recycled content and reusable systems to minimize delivery waste. Alongside regulatory momentum, Chinese manufacturers are embracing the integration of “5G plus industrial internet” and artificial intelligence to optimize production processes, streamline supply chains, and increase the flexibility of packaging production for agricultural applications.

The move away from non-degradable plastics is driving demand for paper-based and biodegradable packaging, while industry consolidation is strengthening the role of larger, more efficient players. Companies such as Jingxing Packaging Materials Co. are adopting closed-loop recycling systems where corrugated packaging production heavily relies on recycled inputs. This combination of sustainability mandates, high-tech manufacturing, and recycled-content adoption is not only reducing environmental impact but also positioning China as a global leader in next-generation agricultural packaging solutions.

Germany: Stringent EU Rules Accelerating Circular Economy in Agricultural Packaging

Germany is at the forefront of the agricultural packaging market in Europe, underpinned by one of the most stringent regulatory frameworks globally. The EU Packaging and Packaging Waste Regulation (PPWR), introduced in 2025, mandates that all packaging must be recyclable or reusable by 2030, with strict minimum targets for recycled content. This regulation is compelling companies to redesign products, pushing innovation in substrates such as grass paper and high-strength recycled fibers. The German Packaging Act (VerpackG) further enforces producer responsibility across the entire packaging lifecycle, strengthening the country’s leadership in the circular economy.

Germany’s highly developed recycling infrastructure provides a competitive edge in achieving EU mandates, but it also accelerates innovation. Companies are investing heavily in developing sustainable alternatives that meet both regulatory requirements and growing consumer demand for environmentally responsible packaging. For the agricultural sector, these mandates are shaping packaging strategies for fertilizers, pesticides, and bulk storage solutions, where durability, recyclability, and compliance are key. As a result, Germany remains a benchmark market for sustainable agricultural packaging in Europe.

India: Government Incentives and Biodegradable Innovations Fuel Market Expansion

India’s agricultural packaging market is being reshaped by a combination of governmental initiatives, corporate expansions, and sustainable technology development. The National Strategy for Additive Manufacturing is creating opportunities for startups and innovations in materials that directly apply to packaging, while the Production Linked Incentive (PLI) Scheme for food processing is encouraging high-quality, standardized packaging adoption. Regulatory shifts, including the Plastic Waste Management (Amendment) Rules, are pushing the market away from single-use plastics, creating strong demand for biodegradable and recyclable alternatives.

Technological innovation is also playing a key role, with IIT Madras developing agricultural waste-based packaging foams as a sustainable substitute for conventional plastics. Global companies are reinforcing their presence in India, with Mauser Packaging Solutions expanding production facilities to cater to rising demand in chemicals and pharmaceuticals. Additionally, local innovators are experimenting with 3D printing for packaging, exemplified by WOL3D’s launch of India’s first 3D-printed consumer goods requiring unique packaging formats. With growing emphasis on biodegradable and compostable materials, India is rapidly emerging as one of the most dynamic and future-ready agricultural packaging markets in Asia.

Brazil: Sustainability Mandates and Investment Surge Transform Packaging Industry

Brazil’s agricultural packaging market is undergoing a strong sustainability-driven transformation under the National Solid Waste Policy, which prioritizes a circular economy and reusable alternatives. New regulations, including the 2025 ban on importing solid plastic waste, are reinforcing domestic recycling and sustainable packaging practices. At the same time, Brazil’s packaging sector is rapidly adopting robotics and AI to improve efficiency, automate quality control, and enhance defect detection in production lines ensuring consistency in packaging for agricultural goods.

The sector is attracting massive investments, with the plastics industry projecting R$10.5 billion (around $1.8 billion) annually in recycling technology, factory expansions, and reverse logistics. The food and beverage sector, a cornerstone of Brazil’s agricultural economy, remains the largest consumer of bulk packaging such as bags, totes, and containers. Corporate players like Yara are advancing sustainable packaging by trialing 100% recycled PET big bags for fertilizers in Brazil. These strategic moves underscore Brazil’s transition toward eco-friendly agricultural packaging while ensuring resilience and innovation across its value chain.

Japan: Bio-Based Materials and Functional Packaging Redefine Market Landscape

Japan’s agricultural packaging market is defined by its advanced recycling systems and cutting-edge innovation in sustainable materials. The Containers and Packaging Recycling Law has established one of the most efficient recycling structures globally, assigning responsibility for collection and recycling to businesses. Recent regulatory updates from the Ministry of Health, Labour and Welfare (MHLW) in 2025 also strengthen standards for food-contact packaging, ensuring safety alongside sustainability in agricultural and bulk packaging applications.

Japan is making a decisive shift toward bio-based packaging materials, with global chemical companies such as LyondellBasell supplying bio-based polypropylene for use in packaging by leading brands like Shiseido. Innovation in packaging functionality is also gaining traction, with producers developing high-performance materials that deliver stability and resistance to deformation critical for agricultural and industrial bulk packaging. These advancements reflect Japan’s dual strategy of promoting eco-friendly materials while enhancing packaging performance, positioning the country as a global trendsetter in sustainable agricultural packaging technologies.

Agricultural Packaging Market Report Scope

Agricultural Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.7 Billion

|

|

Market Size (2034)

|

$9.7 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Product Type (FIBCs, IBCs, Drums, Pouches & Bags, Bottles & Cans), By Material (Plastic, Paper & Paperboard, Metal, Composites, Wood), By Application (Pesticides, Fertilizers, Seeds & Grains, Fruits & Vegetables, Silage), By End-Use Industry (Food & Beverages, Chemicals, Agriculture, Horticulture)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Greif, Inc., International Paper, Smurfit Kappa Group, Mauser Packaging Solutions, Schoeller Allibert, RPC Group, Sonoco Products Company, NNZ Group, LC Packaging International B.V., DS Smith Plc, Uflex Ltd., Novolex, Berry Global Group, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Agricultural Packaging Market Segmentation

By Product Type

- FIBCs

- IBCs

- Drums

- Pouches & Bags

- Bottles & Cans

By Material

- Plastic

- Paper & Paperboard

- Metal

- Composites

- Wood

By Application

- Pesticides

- Fertilizers

- Seeds & Grains

- Fruits & Vegetables

- Silage

By End-Use Industry

- Food & Beverages

- Chemicals

- Agriculture

- Horticulture

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Agricultural Packaging Market

- Amcor plc

- Mondi Group

- Greif, Inc.

- International Paper

- Smurfit Kappa Group

- Mauser Packaging Solutions

- Schoeller Allibert

- RPC Group

- Sonoco Products Company

- NNZ Group

- LC Packaging International B.V.

- DS Smith Plc

- Uflex Ltd.

- Novolex

- Berry Global Group, Inc.

* List Not Exhaustive

Methodology

USDAnalytics leverages a comprehensive and multi-layered methodology to deliver actionable insights into the global Agricultural Packaging Market. Our research integrates primary interviews with packaging engineers, supply chain managers, agricultural producers, and regulatory experts, alongside secondary sources including corporate disclosures, sustainability reports, trade publications, and government databases. Market sizing rising from USD 5.7 billion in 2025 to USD 9.7 billion by 2034 at a CAGR of 6.1% is derived through both bottom-up and top-down approaches, analyzing product types (FIBCs, IBCs, drums, pouches/bags, bottles/cans), materials (plastic, paper, metal, composites, wood), applications (pesticides, fertilizers, seeds, produce, silage), and end-use industries (agriculture, chemicals, food & beverages, horticulture). USDAnalytics further evaluates key trends, including reusable and returnable transport packaging (RTP), bio-based and biodegradable films, smart packaging with IoT/QR integration, and blockchain-enabled traceability, alongside regional insights covering the U.S., China, Germany, India, Brazil, and Japan. Competitive benchmarking examines leaders such as Mauser Packaging Solutions, Amcor, Mondi Group, and Smurfit WestRock, focusing on circularity, fiber and flexible innovations, and regulatory compliance. This integrated methodology ensures industry professionals receive precise, forward-looking intelligence for operational efficiency, sustainability strategy, and packaging performance optimization.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.