Packaging Foams Market Size, Growth Forecast, and Strategic Insights

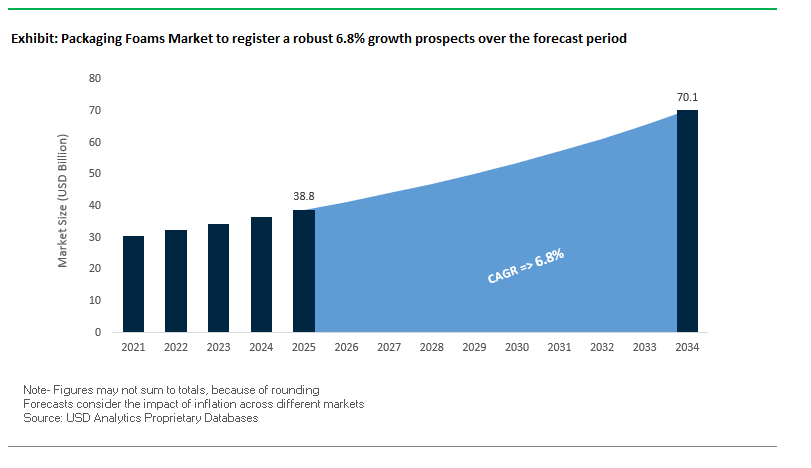

The Global Packaging Foams Market is projected to grow from $38.8 billion in 2025 to $70.1 billion by 2034, registering a CAGR of 6.8%. Packaging foams, including expanded polystyrene (EPS) and polyurethane (PU) foams, play a pivotal role in protective, insulating, and cushioning solutions for a wide array of industries. These materials ensure product integrity, reduce transit damages, and optimize supply chain efficiency, making them indispensable in modern logistics, especially in the booming e-commerce and cold chain sectors.

Key Insights for Industry Stakeholders

- E-Commerce Growth Driving Foam Demand: Fragile and high-value items require shock-absorbing and protective foam solutions to reduce returns and improve customer satisfaction.

- Sustainability and Recyclability Trends: There is a growing shift toward fiber-based, bio-based, and post-consumer recycled (PCR) foams, aligned with ESG goals and corporate sustainability targets.

- Cold Chain and Thermal Protection: Foams with enhanced insulation properties are increasingly used in pharmaceuticals, food, and beverages to maintain product efficacy during transport.

- Customization and Design Optimization: Advanced design software allows tailored foam solutions, minimizing material use, lowering shipping costs, and enhancing the unboxing experience.

- Technological Integration: Intelligent packaging solutions incorporating sensors and coatings are gaining traction, enabling real-time condition monitoring and improved supply chain security.

The market is poised for continued growth as technological innovation, sustainability, and logistics efficiency converge, driving the adoption of high-performance, recyclable, and customizable foam packaging solutions globally.

Recent Developments and Strategic Innovations Shaping Packaging Foams Market

The Global Packaging Foams Industry has witnessed dynamic developments in recent years, emphasizing sustainability, innovation, and market consolidation. In August 2025, industry reports highlighted the increasing adoption of intelligent packaging solutions, where coatings and sensors ensure optimal product conditions during storage and transit.

In May 2025, Mondi commissioned a €400 million paper machine at its Štětí mill, strengthening its leadership in sustainable packaging materials, including alternatives to traditional foam. February 2025 marked Stora Enso’s launch of Papira, a fully recyclable, biodegradable, bio-based foam packaging made from wood fiber. In December 2024, Woamy, in collaboration with Paptic and Secto Design, introduced a fully bio-based, recyclable bio-foam for plastic-free packaging.

March 2024 saw Seawise Innovative Packaging develop an EPS alternative to reduce plastic usage in supply chains. In February 2024, ExxonMobil and Pregis LLC partnered to develop a certified-circular polyethylene (PE) foam, advancing plastics circularity. January 2024 brought Tekni-Plex Consumer Products’ polypropylene foam trays for fresh food, offering lightweight and durable alternatives to traditional polystyrene. Furthermore, September 2024 reports emphasized the adoption of mono-material foam solutions, driving demand for compatible, highly recyclable manufacturing equipment.

Trends and Opportunities Reshaping the Packaging Foams Market

Legislative Bans and Plastic Taxes Driving the Phase-Out of Expanded Polystyrene (EPS)

The packaging foams market is undergoing a rapid structural shift as regulatory bans and plastic taxes accelerate the phase-out of Expanded Polystyrene (EPS). Across the United States, more than 125 cities and counties in California, along with states such as New York and Washington, have enacted strict bans on EPS foodservice and loose-fill packaging. These policies are non-negotiable compliance mandates that are forcing companies to abandon EPS-based packaging formats. In Europe, the EU Plastic Tax of €0.80 per kilogram on non-recycled plastic packaging waste has further increased the cost burden of using virgin EPS, triggering widespread corporate reassessment of material choices. Asian markets are also adopting strong measures. India’s Extended Producer Responsibility (EPR) guidelines, effective April 1, 2025, target the reduction of single-use plastics and mandate recycled content, creating additional pressure to eliminate EPS. In response, large retailers and e-commerce companies are investing in alternative protective packaging systems, phasing out EPS loose-fill entirely and transitioning to paper-based and fiber-based cushioning. This regulatory and financial environment positions EPS phase-out not as a corporate preference but as an unavoidable global market reality.

Rapid Adoption of Molded Fiber and Paper-Based Cushioning for E-Commerce

The rise of e-commerce and direct-to-consumer delivery models is driving rapid adoption of molded fiber and paper-based cushioning materials as sustainable substitutes for EPS. Amazon India, responding to plastic bans, has completely eliminated single-use plastics in its fulfillment centers, replacing air pillows and EPS with paper-based cushioning systems. Similarly, HP has transitioned to molded fiber cushions made from 100% recycled content for computing products, demonstrating that fiber-based solutions can deliver the strength and impact resistance required for fragile electronics. Investment momentum is equally strong on the supply side: DS Smith recently announced capacity expansions in paper mills and conversion facilities to meet soaring demand for paper-based packaging across e-commerce channels. Technological advancements are enhancing performance as well. Academic research into kirigami-based molded fiber designs has produced structures that provide superior cushioning and shock absorption, proving that fiber-based materials are not compromises but engineered, high-performance replacements for EPS. These trends highlight how e-commerce adoption, combined with regulatory pressure, is accelerating the mainstreaming of paper-based cushioning across multiple product categories.

Development of High-Performance Bio-Based Foams from Algae or Mycelium

One of the most compelling opportunities in the packaging foams market is the development of bio-based foams derived from algae and mycelium. Ecovative Design has commercialized mycelium foams grown on agricultural waste, delivering cushioning performance comparable to EPS while being 100% compostable. Similarly, researchers at the University of California, San Diego (UCSD) have developed algae-based polyurethane foams, which can be tailored to rigid insulation or flexible cushioning applications, marking a breakthrough in petroleum-free feedstocks. These innovations are particularly well-suited for niche, high-value applications such as cold chain packaging, premium electronics, and branded consumer goods, where sustainability and brand image are critical differentiators. Additionally, these foams capitalize on waste-to-value models, using feedstocks such as agricultural residues (corn husks, wood chips) and byproducts from algae oil extraction, thereby creating closed-loop material cycles. For manufacturers and brands, bio-based foams provide a dual advantage: reducing reliance on fossil-based polymers and building a strong sustainability narrative that resonates with eco-conscious consumers.

Advanced Foam Recycling and Chemical Repolymerization Technologies

Another major growth avenue is the advancement of chemical recycling and repolymerization technologies that enable closed-loop recovery of foams. Dow’s Renuva™ Mattress Recycling Program exemplifies this opportunity, using chemical depolymerization to convert end-of-life polyurethane foams into polyols for new foam production, achieving virgin-like quality. Similarly, the CIRCULAR FOAM project, involving Covestro and 22 industrial partners, is developing large-scale recycling solutions for rigid polyurethane insulation foams critical in construction and refrigeration. Polystyrene is also benefiting from this trend: INEOS Styrolution and Trinseo are building a commercial-scale depolymerization facility in France to recycle post-consumer polystyrene waste back into styrene monomer. Beyond recycling technology, strategic partnerships are key enablers. For example, Dow and Gruppo Fiori have pioneered recovery processes for polyurethane foams from end-of-life vehicles, making recycling economically viable. These initiatives are positioning chemical recycling as the cornerstone of circularity in the foam packaging market, transforming foams from environmentally problematic materials into recyclable, resource-efficient solutions.

Competitive Landscape: Leading Players Driving Innovation in Packaging Foams

The Global Packaging Foams Industry is shaped by prominent players leveraging materials science expertise, advanced manufacturing, and sustainability-focused solutions. These companies are redefining packaging standards with high-performance, durable, and eco-friendly foam offerings.

Sealed Air Corporation: Pioneering Customizable and Sustainable Foam Solutions

Sealed Air Corporation excels in foam-in-place protective solutions, focusing on efficiency and sustainability. Its Instapak® foam systems create custom-fit cushions for fragile and high-value products. The company emphasizes touchless automation for e-commerce, industrial, and food applications and continues to invest in sustainable and innovative foam technologies to optimize global supply chains.

Sonoco Products Company: Expanding Protective and Thermal Assurance Foam Packaging

Sonoco provides insulated shippers and temperature-controlled containers for sensitive products, incorporating foam inserts and liners for protection and thermal regulation. The company recently refined its business portfolio by divesting non-core thermoformed and flexible packaging, focusing on high-value, sustainable solutions for healthcare and industrial sectors.

Pregis LLC: Driving Circularity with Foam-in-Place and Sustainable Innovations

Pregis LLC offers EasyPack® foam-in-place systems and specialized foam inserts for cushioning and thermal protection. In February 2024, Pregis partnered with ExxonMobil to develop certified-circular PE foam, reinforcing its commitment to plastics circularity. Pregis emphasizes resource efficiency, waste reduction, and enhanced unboxing experiences through sustainable innovation.

Armacell International S.A.: Advancing Lightweight and Recycled Foam Solutions

Armacell specializes in high-performance flexible foams, including ArmaPET® made from recycled PET bottles. The company recently highlighted its sustainability progress and environmental impact tracking, while expanding manufacturing with a new aerogel insulation plant in India. Armacell focuses on energy-efficient, recyclable foam solutions for protective packaging and structural applications.

DS Smith Plc: Delivering Paper-Based Alternatives to Traditional Foam

DS Smith offers fiber-based inserts, molded pulp trays, and protective structures as sustainable alternatives to traditional foam. Following its $9.9 billion acquisition by International Paper in April 2025, the company surpassed its goal of replacing over one billion plastic packaging items with fiber-based solutions. DS Smith prioritizes circular economy initiatives and high-performance, recyclable protective packaging.

Packaging Foams Market Share Insights, 2025-2034

Flexible Foams Secure the Largest Market Share by Structure in the Packaging Foams Industry

Flexible foams dominate the packaging foams market with 62% of the share, reflecting their irreplaceable role as protective void-fill and cushioning materials in high-volume logistics and shipping operations. Polyethylene (PE) and polyurethane (PU) foams are widely adopted because of their lightweight, cost-effectiveness, and superior shock absorption, making them the go-to solution for protecting consumer goods in transit. Their flexibility allows them to be engineered into formats such as foam-in-bag, rolls, sheets, and loose fill, supporting scalability in diverse industries from e-commerce to industrial packaging. The growth of global online retail and parcel shipments has cemented flexible foams as the backbone of modern logistics, directly linking their market share to macroeconomic trends in digital commerce and global supply chain expansion. While rigid foams, particularly EPS and EPP, are crucial for thermal protection and reusable transit packaging, the dominance of flexible foams lies in their volume intensity and unmatched adaptability across packaging applications.

E-Commerce & Logistics Lead Market Share by End-Use Industry in the Packaging Foams Industry

E-commerce and logistics account for 35% of the packaging foams industry, making them the single largest and fastest-growing end-use segment. This leadership is underpinned by the exponential rise of online retail, direct-to-consumer shipping models, and global parcel volumes, which create immense demand for lightweight, impact-absorbing foam packaging to reduce in-transit damages. Air pillows, foam-in-place systems, and insulated shipping containers are widely deployed to ensure secure deliveries across categories ranging from consumer electronics to perishables. Importantly, the segment’s growth is reinforced by the rising consumer expectations for damage-free delivery, sustainable materials, and cost-efficient protection solutions. Beyond parcel packaging, logistics also integrates high-performance foams into pallet-level stabilization and temperature assurance for cold-chain distribution, especially in food and pharmaceuticals. While consumer electronics and automotive segments drive value with engineered foams tailored for anti-static and vibration protection, the scale, frequency, and growth momentum of global e-commerce firmly secure its role as the demand epicenter for packaging foams worldwide.

United States Packaging Foams Market Shaped by State Bans and Rise of Bio-Based Alternatives

The United States packaging foams market is undergoing significant transformation as state-level bans on polystyrene foam containers take effect in Delaware, New Jersey, and Oregon between 2025 and 2026. These restrictions are accelerating the transition to sustainable packaging foams and alternative materials such as recyclable paper foams and bio-based substitutes. Compliance with these rules is becoming a top priority for manufacturers serving the food service industry, while pressure from regulators and consumers is driving innovation across other sectors.

The U.S. market is also a hub for technological advancements in sustainable foams. Companies like Seawise Innovative Packaging (March 2024) and Woamy, in collaboration with Paptic and Secto Design, have introduced biodegradable, plastic-free foam alternatives that can replace EPS packaging. Strategic corporate investments are reshaping the industry, as seen in Tekni-Plex’s launch of polypropylene foam trays for fresh food in 2022, which offer durability and heat resistance while reducing reliance on traditional PS foams. Key applications extend to consumer electronics, automotive, and e-commerce logistics, with foams critical for vibration dampening, lightweighting, and sound insulation—particularly in electric vehicle packaging.

Germany Packaging Foams Market Supported by EU PPWR and Advanced Polypropylene Solutions

Germany’s packaging foams market is governed by the European Union’s Packaging and Packaging Waste Regulation (PPWR) and the updated German Packaging Act, which mandate ambitious recycling and circular economy targets. These frameworks are pushing manufacturers toward mono-material foams and recyclable polypropylene solutions. Germany’s leadership in materials science is evident in ongoing R&D investments, which are aligning the market with both EU climate goals and industry sustainability commitments.

In June 2025, Borealis invested in its Burghausen site to expand polypropylene foam production, a move designed to deliver lightweight, recyclable, and performance-driven materials for packaging. Germany also benefits from a robust recycling ecosystem that supports the reprocessing of post-consumer foams into new feedstock, strengthening the country’s circular economy model. Demand is particularly strong in automotive, electronics, and construction packaging, where foams ensure safe transportation, insulation, and vibration protection for high-value components.

China Packaging Foams Market Accelerated by Express Delivery Regulations and Smart Manufacturing

The packaging foams market in China is expanding under government policies targeting sustainability and eco-friendly logistics packaging. Starting June 2025, new express delivery regulations mandate the adoption of degradable and reusable materials across the supply chain, boosting demand for next-generation packaging foams. These policies reflect broader national strategies to strengthen environmental compliance and reduce over-reliance on single-use plastics.

China’s Made in China 2025 plan is a major growth driver, with the government targeting 70% domestic content in advanced materials by 2025. This includes packaging foams, where heavy investment is being funneled into automation and smart manufacturing systems to increase efficiency and meet global standards. The largest demand comes from consumer electronics and e-commerce, with China’s massive parcel volumes requiring protective foams for everything from smartphones to household appliances. The scale of growth ensures packaging foams remain indispensable in both domestic and export-driven sectors.

India Packaging Foams Market Strengthened by EPR Guidelines and E-Commerce Growth

India’s packaging foams market is gaining momentum through government-backed initiatives such as Make in India and the Production Linked Incentive (PLI) scheme, which incentivize domestic manufacturing and technological advancement. Regulatory shifts, particularly the implementation of Extended Producer Responsibility (EPR) guidelines, are accelerating the adoption of recyclable foams and driving the packaging industry toward a circular economy model.

The rise of e-commerce and organized retail is fueling strong demand for protective foams to ensure safe transit of products across long distances and diverse climates. Corporate investments are reinforcing this growth; for example, the Huhtamaki Foundation’s CloseTheLoop project (₹10 crore/US$1.18 million) is establishing recycling infrastructure that will directly support foam recovery and reprocessing. Key demand sectors include electronics, automotive, and pharmaceuticals, where foams are critical for safe packaging, lightweighting, and damage prevention.

Japan Packaging Foams Market Driven by Positive List Regulations and Bio-Based Foam Innovation

Japan’s packaging foams market is adapting to new food container regulations that came into effect in June 2025. The introduction of a “positive list” for approved synthetic substances in food-contact applications is encouraging innovation in bio-based and recyclable foams. This aligns with Japan’s national goal of cutting greenhouse gas emissions by 46% by 2030 and achieving net zero by 2050.

Corporate and international partnerships are driving bio-based foam innovation in the Japanese market. Stora Enso has extended its packaging portfolio with wood-based foams suitable for thermal packaging and delicate product protection. These solutions are in high demand across electronics, automotive, and food and beverage applications, where Japanese manufacturers prioritize design, functionality, and environmental safety. By integrating sustainability with high-performance standards, Japan is setting benchmarks for lightweight and durable packaging foams in premium industries.

Mexico Packaging Foams Market Growing with Expanded PE Foam and Strategic Partnerships

The Mexican packaging foams market is witnessing strong growth through the increasing use of expanded polyethylene (PE) foams in industrial and logistics packaging. Known for their lightweight properties and superior shock absorption, PE foams are widely adopted for protecting fragile electronics, automotive components, and industrial goods during transport. Their insulating properties also make them an attractive solution for multi-sector load protection.

Strategic partnerships are shaping Mexico’s packaging foams industry. Worldwide Foam’s distribution of Sealed Air products, including ETHAFOAM® and STRATOCELL®, highlights the importance of reliable supply chains and high-quality materials in meeting customer needs. With automotive and industrial manufacturing expanding in Mexico, demand for protective and recyclable foams is accelerating. The country is emerging as a key regional hub where industrial packaging and logistics drive sustained demand for innovative foam solutions.

Packaging Foams Market Report Scope

Packaging Foams Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$38.8 Billion

|

|

Market Size (2034)

|

$70.1 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Material Type (PU, PS, PE, PP, Others), By Structure Type (Flexible Foams, Rigid Foams), By Service Type (Food Service Packaging, Protective Packaging, Thermal Packaging, Cushioning & Void Fill), By End-Use Industry (Automotive, Consumer Electronics, Food & Beverage, Medical & Pharmaceutical, E-commerce & Logistics, Other Industrial Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, JSP Corporation, BASF SE, Zotefoams plc, Armacell International S.A., The Dow Chemical Company, Rogers Corporation, Kaneka Corporation, Recticel N.V., SINOYAFOAM Industrial Co., Ltd., Sonoco Products Company, Pregis LLC, Foam Packaging, Inc., E-Z Pak Inc., Woodbridge Foam Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Foams Market Segmentation

By Material Type

By Structure Type

- Flexible Foams

- Rigid Foams

By Service Type

- Food Service Packaging

- Protective Packaging

- Thermal Packaging

- Cushioning & Void Fill

By End-Use Industry

- Automotive

- Consumer Electronics

- Food & Beverage

- Medical & Pharmaceutical

- E-commerce & Logistics

- Other Industrial Applications

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Foams Market

- Sealed Air Corporation

- JSP Corporation

- BASF SE

- Zotefoams plc

- Armacell International S.A.

- The Dow Chemical Company

- Rogers Corporation

- Kaneka Corporation

- Recticel N.V.

- SINOYAFOAM Industrial Co., Ltd.

- Sonoco Products Company

- Pregis LLC

- Foam Packaging, Inc.

- E-Z Pak Inc.

- Woodbridge Foam Corporation

* List Not Exhaustive

Methodology

The research methodology for the Global Packaging Foams Market combines both primary and secondary research approaches to ensure accuracy, reliability, and actionable insights for industry professionals. Primary research involved structured interviews with key industry stakeholders, including packaging engineers, sustainability experts, supply chain managers, and executives from leading foam manufacturers such as Sealed Air, Pregis LLC, Armacell, and DS Smith across North America, Europe, and Asia-Pacific. Secondary research comprised a comprehensive review of company annual reports, patent filings, regulatory frameworks, trade associations, sustainability disclosures, and verified industry journals. Advanced data triangulation was applied to validate market sizing, segment shares, and growth projections, incorporating macroeconomic indicators, raw material pricing trends, technological adoption models, and sustainability-driven shifts toward bio-based and recyclable foams. Forecasting employed both top-down and bottom-up approaches, while regional insights were contextualized against government regulations, EPR and PPWR frameworks, consumer trends, and global trade flows. This multi-layered methodology ensures that USDAnalytics provides fact-based, high-confidence insights into the market dynamics, emerging opportunities, and competitive landscape of the packaging foams industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.