Smart Plastics for Flexible and Wearable Electronics Market Size, Overview, and Growth Outlook (2025–2034)

Smart Plastics for Flexible and Wearable Electronics Poised to Reach $8.6 Billion by 2034 as Demand for Conformable Devices Surges

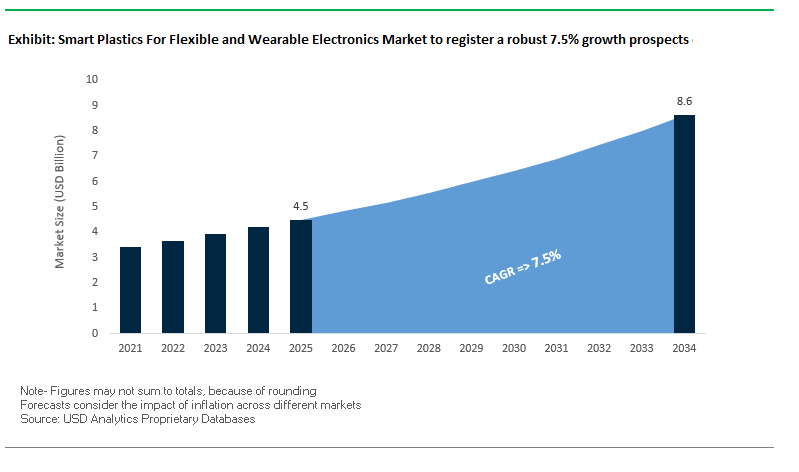

The global smart plastics for flexible and wearable electronics market is projected to grow from $4.5 billion in 2025 to $8.6 billion by 2034, at a CAGR of 7.5%. This market is centered on advanced polymers that enable electrical conductivity, environmental sensing, and self-healing, supporting the next generation of lightweight, pliable, and integrated electronic devices. These materials are crucial in healthcare, consumer electronics, and defense sectors, providing a powerful solution for high-performance, ergonomic, and aesthetically optimized devices.

Key Insights for Industry Professionals:

- Flexible and Conformable Designs: Smart plastics allow electronics to bend, stretch, and conform to human body or wearable applications without loss of functionality.

- Healthcare and Medical Wearables: Biocompatible materials enable continuous patient monitoring and implantable devices, improving healthcare outcomes.

- Enhanced User Experience and Aesthetics: Flexible displays and rollable electronics, such as LG’s OLED TVs, create immersive experiences with thin, lightweight, and visually appealing devices.

- Innovations in Material Science: Conductive polymers like PEDOT:PSS and composites infused with carbon nanotubes or graphene are expanding application potential in wearables and flexible electronics.

- Sustainability and Safety: Environmentally safer materials, removing harmful chemicals like poly(vinylidene fluoride), reflect growing regulatory and consumer expectations.

Market Analysis: Recent Technological Breakthroughs and Strategic Moves Reinforce the Growth of Smart Plastics in Wearables

The smart plastics market for flexible and wearable electronics is witnessing accelerated innovation and strategic activity. In August 2025, scientists at Brookhaven National Laboratory and Case Western Reserve University developed eco-friendly electronic plastics for wearable sensors without using harmful poly(vinylidene fluoride), marking a significant step toward safer, sustainable materials. That same month, LG Display launched its QNED 83 series smart TVs in India, underscoring continued expansion in consumer electronics.

In July 2025, HKC produced its first operating smartphone AMOLED panel sample, signaling its entry into OLED panel manufacturing. Meanwhile, DOW introduced a lightweight shrink sleeve film, designed to reduce plastic usage, showcasing cross-industry applicability of smart polymers in packaging. Flex, in June 2025, highlighted advanced plastics capabilities in wearable electronics and gaming devices, demonstrating the growing adoption of smart plastics across multiple consumer electronics categories.

The market has also been shaped by corporate consolidation and asset transfers. Royole Corporation’s assets, including OLED production equipment, went to auction in December 2024 and January 2025, while Constantia Flexibles acquired Aluflexpack in October 2024, and Stora Enso launched Trayforma BarrPeel in April 2024, expanding sustainable packaging solutions.

Smart Plastics for Flexible and Wearable Electronics Market: Innovation in Stretchable Polymers and Bio-Derived Substrates

Development of Intrinsically Stretchable and Self-Healing Polymer Semiconductors

The smart plastics for flexible and wearable electronics market is being transformed by the emergence of intrinsically stretchable semiconductors capable of maintaining reliable performance under extreme mechanical stress. A research paper published in August 2025 demonstrated a breakthrough in polymer design, introducing a new semiconducting material that maintains high field-effect mobility even under 100% strain, with stable electronic performance across more than 1,000 stretching-relaxation cycles. This level of mechanical durability is crucial for the commercialization of wearable electronics, which require both flexibility and long-term stability.

Another frontier is self-healing functionality, a feature inspired by biological systems. A scientific article on “skin-inspired electronics” described how hydrogen bonding networks in polymer semiconductors enable self-repair after damage. These materials were shown to recover up to 95% of their original charge transport mobility after a tear, dramatically extending device lifespans. Such self-repairing smart plastics pave the way for resilient consumer wearables, medical sensors, and soft robotics, where longevity and reliability are as critical as performance.

Strategic Pivot to Bio-Derived and Biodegradable Substrates

The market is also witnessing a strong pivot toward bio-based and biodegradable plastics as substrates for electronics, driven by sustainability mandates and circular economy goals. An academic study from May 2025 reported that polyhydroxybutyrate (PHB), a biopolymer produced by microorganisms, has been successfully deployed as a flexible substrate for organic field-effect transistors. PHB combines mechanical stability, flexibility, and biodegradability, positioning it as a compelling alternative to petroleum-derived substrates.

Further innovation is occurring in functional biodegradability. A May 2025 review of biodegradable electronics highlighted that materials like silk fibroin, derived from silkworms, can be used in transient electronic devices that dissolve harmlessly after use. This innovation is particularly significant for medical implants and single-use environmental sensors, eliminating the need for surgical retrieval or contributing to e-waste. By reducing lifecycle waste and enabling transient device applications, bio-derived substrates are a critical enabler of sustainable electronics.

Enabling Next-Generation Medical Diagnostic Patches

One of the most promising applications for smart plastics in wearable electronics lies in medical diagnostics and patient monitoring. A February 2025 research publication showcased the development of flexible, wireless biosensor patches that can continuously measure vital parameters such as body temperature, heart rate, and ECG signals. Designed for long-term wear, these patches leverage skin-friendly smart polymers that conform seamlessly to the body, enabling clinical-grade continuous monitoring outside of hospital settings.

A case study from a specialty plastics manufacturer further demonstrated the potential of these innovations. Their collaboration with a biosensor company led to a hybrid patch system combining a disposable polyurethane film-based sensor patch with a reusable electronic hub. This design not only enhances patient comfort but also minimizes material waste. As healthcare increasingly adopts remote monitoring and telemedicine, smart polymer-enabled patches will play a central role in personalized medicine, early diagnostics, and chronic disease management.

Integration into Automotive Human-Machine Interfaces (HMI)

The automotive industry represents another high-growth opportunity for smart plastics, particularly in human-machine interfaces (HMIs). An October 2024 academic study highlighted how injected smart plastic polymers embedded with capacitive touch sensors are replacing traditional mechanical switches and buttons. This innovation enables the creation of seamless, single-part control panels that merge decorative and functional elements, reducing complexity while improving design flexibility.

In addition, smart plastics are advancing structural health monitoring in automotive applications. A September 2025 industry article reported on sensor-equipped plastic components capable of tracking real-time wear, strain, and fatigue in vehicle structures. By embedding sensing capabilities directly into plastic parts, automakers can implement predictive maintenance systems, reducing downtime and enhancing safety. This innovation not only supports the shift toward smart, connected vehicles but also aligns with the industry’s push for lightweight, multifunctional materials that enhance both performance and sustainability.

Competitive Landscape: Leading Global Companies Are Driving Smart Plastics Innovation in Flexible and Wearable Electronics

The smart plastics industry is dominated by companies leveraging materials science, engineering expertise, and technology integration to deliver high-performance, flexible, and sustainable solutions for consumer electronics, healthcare, and defense applications.

LG Display Co., Ltd.: Pioneering Flexible OLED Technology for Consumer Electronics

LG Display specializes in flexible and rollable OLED displays, with applications spanning TVs, mobile devices, and automotive screens. In August 2025, the company launched its 2024 OLED TV lineup with the α (Alpha) 11 AI processor, offering 70% improved graphics performance and 30% faster processing. LG’s brand recognition and vertically integrated operations strengthen its position as a global leader in flexible display technologies.

Samsung Electronics Co., Ltd.: Transforming Wearable Devices and Foldable Displays with Super AMOLED Technology

Samsung Electronics is a leading provider of flexible displays, foldable smartphones, and wearable devices. Notable innovations include the Galaxy Fold series, introduced in 2019, creating a new mobile category. Samsung continues to invest in system semiconductors and personalized appliances, maintaining its global brand presence and vertical integration across multiple electronics sectors.

Universal Display Corporation (UDC): Advancing OLED Efficiency with Phosphorescent Materials

UDC is a leader in OLED material development, notably through UniversalPHOLED® technology, which achieves up to four times higher efficiency than traditional fluorescent OLEDs. The company focuses on continuous innovation and expanding core competencies to support next-generation flexible electronics.

Corning Incorporated: Enhancing Flexible Electronics with Advanced Glass Solutions

Corning is a global leader in materials science, providing solutions for consumer electronics, optical communications, and life sciences. Its Gorilla Glass is widely used in flexible displays. Corning emphasizes innovation, sustainability, and R&D expansion, reinforcing its leadership in advanced glass and flexible electronics applications.

Asahi Glass Co., Ltd. (AGC): Supporting Flexible and Wearable Electronics with Specialized Glass Products

AGC produces glass and chemical products tailored for flexible and wearable electronics. Innovations in architectural and automotive glass demonstrate its capability in high-performance, sustainable production. AGC’s vertically integrated operations enable it to serve diverse markets globally.

Smart Plastics For Flexible and Wearable Electronics Market Share Insights, 2025-2034

Conductive Polymers Drive Market Share by Polymer Type in Smart Plastics for Flexible & Wearable Electronics

Conductive polymers capture 38% of the smart plastics market for flexible and wearable electronics, positioning themselves as the essential enabler of the sector. Their ability to conduct electricity while maintaining flexibility makes them indispensable for printed circuits, biosensors, and electrodes embedded directly into wearable devices. Applications range from fitness trackers to biomedical monitoring patches, where reliability and comfort are paramount. This segment is growing rapidly as demand for next-generation AR/VR headsets, flexible displays, and diagnostic wearables surges. By combining light weight, mechanical flexibility, and high conductivity, conductive polymers outperform many traditional materials. Although advanced materials like self-healing polymers are on the horizon, conductive polymers remain the industry standard, providing the structural foundation for mass production and scalability of smart, connected electronics.

Consumer Electronics Command Market Share by End-Use in Smart Plastics for Flexible Electronics

Consumer electronics account for 45% of end-use demand in smart plastics for flexible and wearable electronics, making it the undisputed volume driver of this sector. The rapid adoption of smartwatches, fitness trackers, foldable smartphones, AR/VR headsets, and wireless hearables ensures that electronics brands consume the majority of advanced smart materials. Consumer expectations for lightweight, flexible, and durable devices fuel demand for thermoplastic elastomers for housings, conductive polymers for circuitry, and fluoropolymers for insulation. The sector also benefits from scale—global brands push production volumes that dwarf those of other industries, enabling lower costs and faster commercialization of new material technologies. At the same time, integration of health monitoring features into consumer devices blurs the line between lifestyle electronics and medical diagnostics, ensuring consumer electronics will remain the primary growth engine in smart plastics demand through the forecast period.

United States: Defense Investments and Eco-Friendly Polymer Innovation

The United States smart plastics market for flexible and wearable electronics is strongly driven by government-backed initiatives in defense, healthcare, and sustainability. The U.S. Department of Defense (DoD) has allocated substantial funding through the NextFlex Manufacturing Innovation Institute to advance flexible hybrid electronics (FHE) for military applications such as wearable sensors, lightweight communication devices, and field-deployable monitoring systems. Parallel to this, the National Science Foundation (NSF) is supporting breakthrough academic research, such as Case Western Reserve University’s development of ferroelectric polymers free from PFAS chemicals, a milestone in sustainable and biocompatible smart plastics.

The U.S. market is also witnessing surging demand for wearable health monitoring devices. Innovations include dual strain-temperature sensors, flexible glucose monitors, and self-healing polymers that extend device durability and performance. Startups and established companies alike are investing in lightweight, steel-strength polymers that enable thinner, stronger wearable devices. With the EPA’s emphasis on reducing plastic waste and regulating hazardous chemicals, the industry is moving toward eco-friendly, recyclable smart plastics that align with both consumer safety and environmental goals.

European Union: ESPR, PPWR, and Roll-to-Roll Flexible Electronics Leadership

The European Union smart plastics market is being reshaped by two cornerstone regulations— the Ecodesign for Sustainable Products Regulation (ESPR) and the Packaging and Packaging Waste Regulation (PPWR). Together, they mandate Digital Product Passports to provide transparency on material origins and recyclability, while requiring all plastics to include minimum recycled content by 2030. These policies are compelling manufacturers of flexible substrates and encapsulants to adopt mono-material, recyclable solutions.

Restrictions on PFAS from August 2026 are accelerating innovation in alternative barrier coatings for consumer and medical electronics. The VTT Technical Research Centre of Finland is pioneering roll-to-roll production systems for wearable sensors, a move that significantly lowers costs and enables mass manufacturing of flexible devices. As sustainability regulations tighten, European companies are leveraging smart plastics in wearable medical sensors, IoT devices, and e-textiles, positioning the EU as a leader in circular economy-driven electronics manufacturing.

China: Regulatory Controls and Graphene-Based Smart Textiles

The China smart plastics market is driven by dual pressures—regulatory enforcement and consumer demand for advanced technologies. Under the “14th Five-Year Plan”, the government has strengthened its control over plastic pollution, requiring express delivery companies from June 2025 to use eco-friendly, reusable packaging. This indirectly stimulates adoption of sustainable smart plastics across e-commerce and logistics.

China’s academic collaborations are yielding cutting-edge solutions. Researchers at Jiangnan University and the University of Cambridge have successfully developed graphene-ink conductive cotton fabrics, paving the way for environmentally friendly wearable electronics. The country’s growing appetite for luxury consumer electronics and premium healthcare devices is driving demand for sophisticated smart plastics with integrated sensors, flexible circuits, and durability-enhancing properties. Combined with government tax incentives for green technology and remanufacturing, China is becoming a major hub for next-generation flexible electronics powered by smart polymers.

India: Policy Support and NCFlexE-Driven Innovation

The India smart plastics for flexible and wearable electronics market is supported by strong national policies such as the National Policy on Electronics (NPE) 2019, which seeks to make India a global hub for Electronics System Design and Manufacturing (ESDM). Major government-backed schemes like the Production Linked Incentive (PLI) Scheme and the Semicon India Programme (SIP) are encouraging investment in semiconductors, display modules, and core component design.

At the research forefront, the National Centre for Flexible Electronics (NCFlexE) at IIT Kanpur plays a central role in developing printable conductive inks, flexible solar modules, and wearable healthcare devices. India’s regulatory framework also mandates that from July 1, 2025, all plastic packaging must be traceable via barcodes or QR codes, reinforcing the integration of smart labels and embedded traceability sensors. Combined with the Digital India initiative and a thriving startup ecosystem, India is rapidly emerging as a growth hotspot for low-cost, scalable smart plastics solutions in both consumer electronics and healthcare wearables.

Japan: Biocompatible Sensors and Anti-Counterfeiting Smart Packaging

The Japan smart plastics market is undergoing a rapid transition under the Plastic Resource Circulation Strategy, which requires all packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, effective the same year, mandates the redesign of 12 categories of single-use plastics, creating momentum for compostable and biocompatible smart polymers.

Japanese academic institutions are global leaders in innovation. The University of Tokyo recently developed a breathable wearable sensor capable of continuous use for a week, demonstrating advances in comfort and biocompatibility of smart plastics. Japanese companies are also integrating NFC-enabled packaging, blockchain, and intelligent tracking solutions in sectors such as beauty, healthcare, and e-commerce to fight counterfeiting and improve consumer trust. With its blend of regulatory push and research-driven progress, Japan is positioning itself as a pioneer in human-centered, sustainable wearable electronics.

Brazil: PNRS Framework and Medical Application Expansion

The Brazil smart plastics market is being shaped by the National Solid Waste Policy (PNRS), which mandates responsible reuse, recycling, and reduction of plastics. The enactment of Law No. 15,088 in January 2025, banning the import of plastic waste, is compelling domestic industries to innovate with sustainable smart polymers.

In the healthcare sector, Anvisa (Brazil’s Health Regulatory Agency) has revised food contact and medical-grade regulations, directly influencing the types of smart plastics approved for wearable healthcare applications. As Brazil’s medical device and consumer electronics industries expand, demand is rising for flexible, recyclable, and sensor-integrated polymers. Supported by reverse logistics systems and government incentives, Brazil is aligning its smart plastics industry with both sustainability imperatives and high-performance requirements.

Smart Plastics for Flexible and Wearable Electronics Market Report Scope

Smart Plastics For Flexible and Wearable Electronics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.5 Billion

|

|

Market Size (2034)

|

$8.6 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Polymer Type (Conductive Polymers, Thermoplastic Elastomers, Self-healing Polymers, Shape-memory Polymers, Fluoropolymers), By Application (Flexible Electronics, Wearable Electronics), By End-Use Industry (Healthcare & Medical, Consumer Electronics, Automotive, Aerospace & Defense, Logistics & Transportation)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., BASF SE, 3M Company, Covestro AG, Sabic, LG Chem, Asahi Kasei Corporation, Mitsubishi Chemical Corporation, Sumitomo Chemical Co., Ltd., Heraeus Holding GmbH, Solvay S.A., Nitto Denko Corporation, Dow Inc., Novares Group, Exothermix LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Smart Plastics For Flexible and Wearable Electronics Market Segmentation

By Polymer Type

- Conductive Polymers

- Thermoplastic Elastomers

- Self-healing Polymers

- Shape-memory Polymers

- Fluoropolymers

By Application

- Flexible Electronics

- Wearable Electronics

By End-Use Industry

- Healthcare & Medical

- Consumer Electronics

- Automotive

- Aerospace & Defense

- Logistics & Transportation

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Smart Plastics For Flexible and Wearable Electronics Market

- DuPont de Nemours, Inc.

- BASF SE

- 3M Company

- Covestro AG

- Sabic

- LG Chem

- Asahi Kasei Corporation

- Mitsubishi Chemical Corporation

- Sumitomo Chemical Co., Ltd.

- Heraeus Holding GmbH

- Solvay S.A.

- Nitto Denko Corporation

- Dow Inc.

- Novares Group

- Exothermix LLC

* List Not Exhaustive

Methodology

The research methodology for the Smart Plastics for Flexible and Wearable Electronics Market combines rigorous primary and secondary research to deliver accurate, actionable, and industry-relevant insights. USDAnalytics conducted in-depth primary research through interviews with polymer scientists, materials engineers, wearable device developers, healthcare technology experts, and supply chain professionals across North America, Europe, Asia-Pacific, India, Japan, and Brazil. Secondary research involved analysis of corporate annual reports, patent filings, regulatory databases, academic journals, sustainability disclosures, and verified industry publications. Data triangulation was applied to validate market sizing, growth projections, and adoption trends, integrating factors such as conductive polymer deployment, self-healing material innovations, bio-derived substrates, and flexible electronics commercialization. Forecasts were developed using top-down and bottom-up approaches, while regional insights were contextualized against policy frameworks, Extended Producer Responsibility (EPR) mandates, sustainability regulations, and consumer demand for ergonomic, durable, and technologically advanced devices. This comprehensive methodology ensures that the report provides fact-based, real-world intelligence on smart plastics innovation, flexible and wearable electronics applications, and market expansion for industry professionals and strategic decision-makers.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.