Solketal Market Valuation 2025–2034: $90.1 Billion to $127.1 Billion at 3.9% CAGR Anchored in Bio-Based Solvents, Plasticizers, and Advanced Battery Intermediates

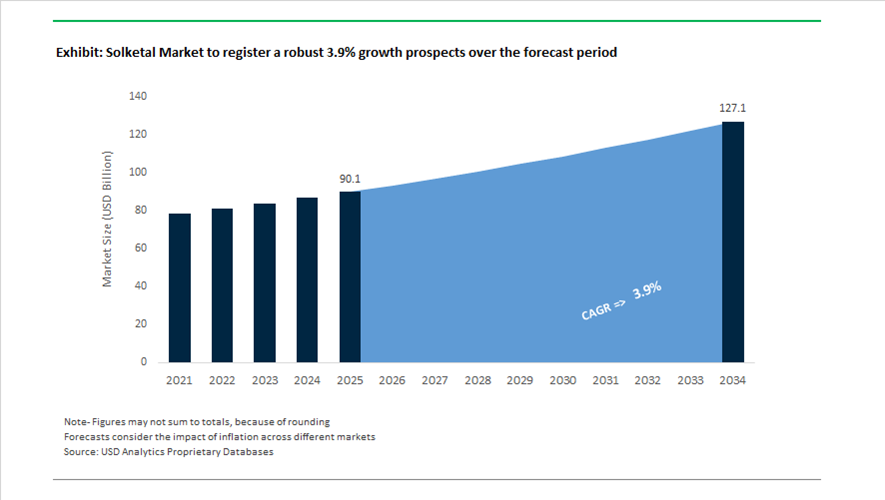

The global solketal market is valued at $90.1 billion in 2025 and is projected to reach $127.1 billion by 2034, expanding at a CAGR of 3.9%. Growth is supported by rising demand for bio-based solvents, fuel additives, pharmaceutical intermediates, cosmetic humectants, green plasticizers, and advanced electrolyte precursors. Solketal, derived from glycerol acetalization, has gained prominence as a renewable chemical building block offering low toxicity, biodegradability, high solvency, and compatibility with sustainable formulation standards. Expanding biodiesel production has structurally increased glycerol availability, driving downstream integration into value-added solketal production for coatings, personal care, flexible PVC, and next-generation energy storage materials.

In March 2024, manufacturers introduced high-purity solketal grades exceeding 99% purity for synthesis of chiral pharmaceutical intermediates, particularly targeting monoglyceride-based drug delivery systems. During 2024, major personal care brands incorporated solketal into clean-label skin care formulations as a biodegradable solvent and moisturizing agent, replacing petroleum-derived glycols. In 2024, specialty chemical producers expanded bio-based solvent capacity in Nanjing, China, focusing on regional demand for eco-friendly paints, coatings, and non-toxic cleaning agents. Following its acquisition of Momentive Performance Materials in 2024, KCC Corporation completed operational integration in early 2025, centralizing production of high-purity specialized solvents, including solketal-derived intermediates for pharmaceutical and electronics applications.

Innovation in process efficiency accelerated in 2025. In February 2025, researchers and industry collaborators demonstrated a microwave-assisted, catalyst-free method for converting solketal into solketal carbonate, achieving 90% yield within 30 minutes compared to 48 hours under conventional synthesis routes. This advancement targets liquid electrolyte development for emerging potassium battery technologies. By late 2025, extraction from biomass was identified as the fastest-growing manufacturing segment, enabled by improved glycerol fractionation technologies that reduce feedstock costs and enhance traceability. In late 2025, developers launched bio-plasticizer blends utilizing solketal as a core building block, offering improved thermal stability and lower volatility compared to traditional phthalate plasticizers in flexible PVC systems.

Strategic partnerships and pilot-scale commercialization are shaping the 2025–2026 landscape. In October 2025, R3V Tech secured an Innovate UK grant to build a pilot demonstrator at a biodiesel facility, deploying an electrochemical process that converts crude glycerol directly into solketal at room temperature, reducing refining energy intensity and transportation requirements. In late 2025, a major global chemical producer partnered with a biotechnology organization to commercialize an improved catalytic route for solketal production, reporting higher yields and lower energy consumption in acetalization. These developments underscore how renewable feedstock valorization, decentralized on-site production, advanced battery chemistry integration, and phthalate replacement strategies are reinforcing solketal’s position as a strategic bio-based platform chemical through 2034.

Key Trends and Strategic Opportunities in the Global Solketal Market

Integration of Solketal as a High-Octane Gasoline Oxygenate for Refinery Optimization

The solketal market is gaining strategic relevance within refinery operations as fuel producers search for bio-components that meet tightening emission standards without compromising blend stability. In Europe and Asia Pacific, refiners are actively evaluating solketal as a drop-in oxygenate to comply with Euro 6 and EN 228 gasoline specifications. Unlike ethanol, solketal offers low Reid Vapor Pressure and strong resistance to water absorption, eliminating phase separation risks that complicate logistics and storage in humid climates.

Industrial trials conducted during late 2024 and 2025 demonstrate that solketal blending can raise gasoline octane numbers by up to 2.5 points while its approximately 36% oxygen content improves combustion efficiency. This translates into measurable reductions in particulate matter and gum formation in modern spark-ignition engines, aligning directly with urban air quality mandates. Policy dynamics are reinforcing this trend. Updates to National Biofuel Policy frameworks during 2023 and 2024 in several emerging economies raised biodiesel blending mandates to as high as 35%, generating a structural surplus of glycerol. This surplus has accelerated refinery-linked pilot projects that convert glycerol into solketal using solid acid catalysts. By 2025, transition metal-based systems such as SZZ catalysts achieved glycerol conversion rates above 99% and solketal yields approaching 98%, making refinery-scale integration economically viable and positioning solketal as a value-added outlet for biodiesel byproducts.

Strategic Pharmaceutical Adoption as a Chiral Building Block and Green Solvent

A second major trend is unfolding in pharmaceuticals, where regulatory pressure to eliminate hazardous solvents is reshaping process chemistry. Solketal’s 1,3-dioxolane structure allows it to function both as a polar aprotic solvent and as a chiral intermediate in active pharmaceutical ingredient synthesis. This dual functionality is driving its adoption as a replacement for solvents such as DMF and NMP in line with green chemistry mandates.

Specialty chemical suppliers have moved early to capture this demand. In September 2023, Arkema introduced a dedicated portfolio of solketal-based pharmaceutical intermediates, signaling a structural shift toward bio-derived processing routes. By May 2025, production of ultra-high-purity solketal exceeding 98% purity had scaled significantly and now accounts for more than 41% of total market volume. This growth is driven by pharmaceutical and cosmetic formulators that require low-toxicity, high-stability solvents with consistent chiral performance. Industry data from December 2025 further indicates that nearly 40% of chemical blending facilities have integrated solketal-based formulations. The adoption is supported by favorable process mass intensity and atom economy metrics frequently cited in studies published by the Royal Society of Chemistry, enabling pharmaceutical manufacturers to progress toward 2030 sustainability targets without sacrificing yield or throughput.

Bio-Based Plasticizers and Sustainable Surfactant Intermediates

A significant growth opportunity lies in solketal-derived esters as non-toxic plasticizers and sustainable surfactant intermediates. These derivatives are increasingly preferred over traditional phthalates in applications where regulatory scrutiny and human exposure risks are highest. In medical devices and food-contact packaging, solketal-based plasticizers offer low volatility, enhanced thermal stability, and full biodegradability, addressing the limitations of legacy DEHP-based systems.

In 2025, medical device manufacturers including B. Braun Medical accelerated transitions toward bio-based plasticizers for intravenous bags and catheter systems. Solketal-derived blends are capturing share within the rapidly expanding bio-plasticizer segment, which is moving away from regulated phthalates across a market valued at several billion dollars. Beyond plasticization, solketal’s compatibility with a wide range of polymer matrices is enabling multifunctional formulations. New resin and surfactant intermediates launched in mid-2025 demonstrated superior solubility for active ingredients, supporting the development of green coatings, inks, and personal care formulations that retain performance under chemically aggressive conditions.

Aviation and Wind Energy Anti-Icing Fluids as Glycol Alternatives

Environmental constraints surrounding propylene glycol runoff are opening a high-value niche for solketal-based de-icing and anti-icing systems in aviation and renewable energy infrastructure. Solketal’s low freezing point, rapid biodegradability, and low aquatic toxicity profile make it an attractive candidate for replacing conventional glycols in Type I and Type II de-icing fluids.

In wind energy, research published in March 2025 on bio-derived phase-change material coatings demonstrated anti-icing efficiencies of more than 65% at temperatures down to minus 15 degrees Celsius. Solketal is being evaluated as a functional component in these passive anti-icing systems, where it extends the freezing delay of water droplets by nearly twofold, improving turbine availability in cold climates. In aviation, airports are under increasing pressure to comply with groundwater protection and runoff management regulations. This is driving investment in sustainable de-icing fluid programs and dispensing systems, creating direct demand for solketal-based formulations that deliver required holdover times while significantly reducing environmental burden compared with traditional glycol-based fluids.

Solketal Market Share and Segmentation Insights

High Purity Grade Solketal Leads Market Demand for Biofuel and Specialty Chemical Applications

High purity grade solketal accounted for 42.80% of the solketal market in 2025, reflecting strong demand from applications requiring consistent chemical quality and performance. High purity solketal is widely used in biofuel additive formulations, cosmetics ingredients, and specialty chemical synthesis, where controlled impurity levels and stable chemical composition are essential. Derived primarily from glycerol feedstocks obtained as a biodiesel production byproduct, solketal represents an important value-added chemical in bio-based chemical manufacturing. A key 2025 market development is the emergence of fuel additive specifications for solketal, where high purity grades must meet strict requirements related to water content, acidity, and impurity profiles to ensure compatibility with fuel systems and engine performance.

Biofuel Additives Drive Global Solketal Demand Through Glycerol Valorization

Biofuel additives represent the largest application segment in the solketal market, accounting for 38.60% of global demand in 2025 due to the increasing use of solketal as a fuel performance enhancer. Solketal improves octane rating, cold flow properties, and particulate emission performance when blended into gasoline and diesel fuels. The chemical also contributes to improved fuel combustion efficiency while supporting renewable fuel development. A major 2025 industry trend is the growing focus on glycerol valorization within integrated biodiesel production systems, where excess crude glycerol generated during biodiesel manufacturing is converted into higher-value chemicals such as solketal. This approach supports the circular economy in biofuel production, enabling biodiesel producers to transform low-value byproducts into commercially valuable fuel additives.

Solketal Market Competitive Landscape

The global solketal market in 2026 is driven by biodiesel-derived glycerol valorization, high-purity bio-solvent demand, and decentralized production technologies. Leading players are focusing on green oxygenates, pharmaceutical-grade solketal, and modular on-site conversion systems to enhance sustainability, reduce costs, and meet regulatory requirements.

Solvay Strengthens Bio-Based Oxygenate Leadership Through Integrated Glycerol Value Chains and Decarbonization Strategy

Solvay S.A. is reinforcing its leadership in the solketal market with €4.3 billion in 2025 net sales and a strong 20.7% EBITDA margin, supported by €101 million in cost savings. Its Coatis business unit in Latin America plays a central role in producing oxygenated solvents derived from glycerol, positioning solketal as a low-carbon alternative to petrochemical solvents. The company’s 29% reduction in Scope 1 and 2 emissions enhances the product carbon footprint profile of its solketal derivatives. Strategic investments are directed toward high-purity bio-solvents for pharmaceutical and fragrance applications. Solvay’s integrated value chain and sustainability-driven production strengthen its competitiveness in renewable chemical intermediates. Its 2026 outlook focuses on energy transition projects and specialty bio-based chemicals.

GLACONCHEMIE Advances High-Purity Solketal Production and Catalytic Efficiency for Biofuel and Coatings Applications

GLACONCHEMIE GmbH is a specialized leader in glycerol valorization, focusing on high-purity solketal production through advanced acetalization processes. Its 99% purity grades are tailored for pharmaceutical intermediates and high-performance solvent applications. Innovations in heterogeneous acid catalysis reduce reliance on harsh mineral acids, improving yield and aligning with EU Green Deal sustainability targets. The company is actively promoting solketal as a biodiesel stabilizer, enhancing cold-flow properties and preventing gelation in low-temperature environments. Continuous-flow reactor optimization supports increased demand from VOC-compliant paints and coatings markets. Its strong European manufacturing base enhances supply reliability for bio-based solvent demand. GLACONCHEMIE’s focus on purity and process efficiency differentiates it in the specialty chemicals segment.

Evonik Industries Enhances Solketal Purification and Custom Solutions Through Advanced Membrane Technologies

Evonik Industries AG is leveraging its Advanced Technologies segment to scale high-performance solketal derivatives, supported by a 2025 EBITDA of €1.87 billion and strong 2026 outlook. Its “Evonik Tailor Made” strategy accelerates commercialization of customized solketal applications across personal care and agrifood industries. The integration of SEPURAN® membrane technology enables ultra-high purity solketal production while reducing energy consumption by up to 20% compared to conventional distillation. Evonik’s global presence across more than 100 countries ensures localized supply of bio-based intermediates. Its focus on high-ROCE projects drives investment into sustainable chemical processes. The company’s expertise in separation technologies strengthens its role in advanced bio-solvent manufacturing.

Merck KGaA Expands Reagent-Grade Solketal Supply and Green Chemistry Integration for Life Sciences

Merck KGaA is a key supplier of reagent-grade solketal, supporting pharmaceutical R&D and industrial synthesis with ultra-high purity enantiomers. With €21.1 billion in 2025 net sales, its Life Science division drives demand for (S)-(+)- and (R)-(-)-solketal used in asymmetric synthesis and drug development. The company’s DOZN™ green chemistry framework positions solketal as a preferred sustainable solvent alternative. AI-driven digital supply chain capabilities enable just-in-time delivery, reducing waste and inventory costs for biotech and pharmaceutical clients. Merck’s integrated offering includes catalysts, analytical tools, and process solutions, enabling end-to-end support for glycerol-derived chemical innovation. Its focus on precision chemistry and sustainability reinforces its leadership in specialty reagents.

R3V Tech Pioneers Modular Electrochemical Solketal Production for On-Site Glycerol Valorization

R3V Tech is emerging as a disruptive innovator in the solketal market, focusing on decentralized production through electrochemical synthesis. Its proprietary process converts crude glycerol into solketal under ambient conditions, eliminating the need for energy-intensive distillation and conventional catalysts. Backed by an Innovate UK grant, the company is scaling its pilot system to kilogram-per-hour production by 2026. Its modular plug-in units enable biodiesel producers to perform on-site valorization, transforming waste glycerol into high-value bio-solvents while reducing logistics costs. The process integrates captured CO2 and renewable electricity, aligning with net-zero manufacturing goals. R3V Tech’s approach redefines supply chain efficiency and sustainability in glycerol-based chemical production.

United States Solketal Market Accelerated by Fuel Mandates and Onshored Green Chemistry

The United States solketal industry is being structurally reshaped by renewable fuel policy, supply chain localization, and regulatory-driven solvent substitution. Following the increase in national biofuel blending mandates in late 2024, targeting a minimum of 36 billion gallons of renewable fuels, solketal adoption has accelerated as a preferred oxygenate additive in biodiesel formulations. Its ability to improve cold-flow properties and oxidative stability has positioned solketal as a functional additive aligned with low-temperature operability requirements in northern states. Trade policy has reinforced domestic capacity expansion. After the 2025 tariff updates on imported chemical intermediates, U.S. producers moved aggressively to install on-site glycerol-to-solketal conversion units, reducing dependence on petrochemical solvent imports and improving margin resilience through feedstock integration.

Beyond fuels, pharmaceutical and specialty chemical demand is strengthening. Midwest-based facilities expanded high-purity solketal production above 98% to meet rising requirements for chiral intermediates used in cardiovascular and neurological therapies. Process innovation is also emerging as a competitive lever. In 2025, a leading North American producer reported successful piloting of an AI-optimized catalytic pathway that improved solketal yield by 12% while cutting energy consumption by 18%, enhancing both economics and sustainability metrics. Regulatory pressure is further widening the addressable market. Under the EPA’s final TSCA risk management rules restricting dichloromethane, U.S. manufacturers are pivoting toward solketal-based cleaning and processing agents as low-VOC, non-halogenated alternatives.

Germany Solketal Market Anchored by Circular Feedstocks and EU Regulatory Leadership

Germany represents a high-value solketal market where regulatory alignment, backward integration, and derivative innovation converge. In mid-2025, German specialty chemical firms led the development of bio-methanol-derived solketal, achieving a near carbon-neutral profile designed to meet the EU REACH 2026 benchmarks. This shift reflects Germany’s broader emphasis on standardized bio-based inputs across specialty chemicals. Industrial synergies are also strengthening. Regional producers such as Glaconchemie GmbH have optimized backward integration models by sourcing crude glycerol directly from nearby biodiesel refineries, converting it into technical-grade solketal for European coatings and resin applications.

Downstream diversification is accelerating. Following updates to the EU Cosmetics Regulation in 2025, German personal care brands have replaced synthetic humectants with pharmaceutical-grade solketal due to its superior skin compatibility, solvency profile, and biodegradability. Research-driven expansion into energy storage is also notable. Berlin-based research institutes demonstrated a microwave-assisted, catalyst-free synthesis of solketal carbonate in late 2024, with the derivative now under evaluation as a stable electrolyte for potassium-based batteries within the hydrogen economy ecosystem. At an infrastructure level, German chemical parks have established bio-foundry clusters focused on refining solketal derivatives for high-performance bio-lubricants used in wind turbine gearboxes, reinforcing circular industrial design.

India Solketal Market Scaled by BioE3 Policy and Export-Oriented Manufacturing

India’s solketal industry is expanding rapidly on the back of policy stimulus, MSME participation, and export competitiveness. The BioE3 policy approved in August 2024 has prioritized commercialization of bio-based chemicals, with dedicated funding for bio-foundries producing solketal from renewable glycerol streams. Complementing this, the Vigyan Dhara scheme launched in 2025 has enabled MSMEs to access capital subsidies of up to 30% for decentralized solketal units located in rural hubs, allowing valorization of agricultural-waste-derived glycerol and strengthening local value chains.

Industrial scale-up has translated into export momentum. With new large-scale facilities commissioned in Gujarat and Maharashtra during 2025, India has emerged as a top-three global exporter of 96% purity solketal. Domestic consumption is also rising, particularly in pharmaceuticals. Indian drug manufacturers reported a 25% year-on-year increase in solketal usage as a green substitute for petroleum-based intermediates in API synthesis. Product innovation is extending into food applications, where Indian producers introduced solketal-based flavor carriers in early 2025 to serve the global natural-identical additives market, leveraging solketal’s stability and regulatory acceptance.

China Solketal Market Driven by Mandatory Standards and Electronic-Grade Purification

China’s solketal market is being propelled by regulatory mandates, glycerol valorization policy, and high-purity downstream applications. In late 2025, the National Health Commission introduced stringent limits on volatile substances in food-contact materials, accelerating the shift toward solketal-derived plasticizers as compliant, low-volatility alternatives. Industrial policy support is reinforcing supply. Under the 2025 guidelines issued by the Ministry of Industry and Information Technology, biodiesel byproduct conversion has been prioritized, with tax rebates incentivizing investment in solketal refineries that upgrade crude glycerol into high-value chemical inputs.

Technological capability is advancing rapidly. Chinese producers have achieved mass production of electronic-grade solketal through improved purification systems, enabling its use in semiconductor cleaning and lithography processes where ultra-low impurity thresholds are critical. Sustainability-driven product launches are also shaping the market. In September 2025, a major domestic chemical conglomerate introduced solketal-based water-borne resins aligned with the country’s Blue Sky air quality initiatives, embedding solketal into compliant coatings and construction materials supply chains.

France Solketal Market Strengthened by Luxury, Pharma Innovation, and Zero-Waste Models

France has emerged as one of Europe’s most influential solketal markets, supported by luxury personal care demand, pharmaceutical innovation, and integrated biorefinery models. Under the national Natural Beauty initiative, solketal adoption has surged in high-end fragrances and cosmetics as a biodegradable solvent that aligns with clean formulation narratives without compromising performance. This has positioned France as the second-largest solketal consumer in Europe, particularly within premium personal care segments.

Pharmaceutical innovation is reinforcing this leadership. French drug manufacturers have pioneered the use of solketal as a chiral intermediate in targeted drug delivery systems, supported by research grants from Inserm in 2024. At the infrastructure level, France is deploying integrated biorefinery configurations where solketal synthesis is co-located with biogas generation from residual waste streams. These zero-waste refinery models enhance energy efficiency and improve lifecycle sustainability metrics, strengthening France’s role as a reference market for circular solketal production.

Comparative Snapshot: Country-Level Solketal Industry Dynamics

Solketal Market County Level Snapshot

|

Country

|

Primary Demand Drivers

|

Strategic Focus Areas

|

Structural Impact

|

|

United States

|

Biofuels, pharmaceuticals, green solvents

|

Onshoring, AI-optimized catalysis, DCM substitution

|

Supply security and regulatory-driven demand

|

|

Germany

|

Cosmetics, coatings, energy storage

|

Backward integration, bio-methanol solketal

|

REACH-aligned circular production

|

|

India

|

APIs, exports, flavors

|

MSME scale-up, BioE3 bio-foundries

|

Cost-competitive global supply

|

|

China

|

Food-contact materials, semiconductors

|

Glycerol valorization, electronic-grade purity

|

Policy-backed capacity expansion

|

|

France

|

Luxury personal care, pharma R&D

|

Chiral intermediates, zero-waste biorefineries

|

High-value downstream differentiation

|

Solketal Market Report Scope

Solketal Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$90.1 Billion

|

|

Market Size (2034)

|

$127.1 Billion

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Purity Grade (Pharmaceutical Grade, High Purity Grade, Technical Grade, Low Purity Grade), By Application (Biofuel Additives, Pharmaceutical Intermediates, Industrial Solvents, Cosmetics & Personal Care, Food & Beverage, Agrochemicals), By Synthesis Process (Catalytic Synthesis, Enzymatic Production, Microwave-Assisted Synthesis)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Solvay SA, Merck KGaA, Thermo Fisher Scientific Inc., Glaconchemie GmbH, Suzhou Jinghua Chemical Co. Ltd., Alfa Chemistry, Yancheng Jinghua Chemical Co. Ltd., Tokyo Chemical Industry Co. Ltd., Loba Feinchemie GmbH, Sasol Limited, BASF SE, Alteqo BV, CPS Performance Materials Corp., Glentham Life Sciences Ltd., Impag AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Solketal Market Segmentation

By Purity Grade

- Pharmaceutical Grade

- High Purity Grade

- Technical Grade

- Low Purity Grade

By Application

- Biofuel Additives

- Pharmaceutical Intermediates

- Industrial Solvents

- Cosmetics & Personal Care

- Food & Beverage

- Agrochemicals

By Synthesis Process

- Catalytic Synthesis

- Enzymatic Production

- Microwave-Assisted Synthesis

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Solketal Industry

- Solvay SA

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Glaconchemie GmbH

- Suzhou Jinghua Chemical Co. Ltd.

- Alfa Chemistry

- Yancheng Jinghua Chemical Co. Ltd.

- Tokyo Chemical Industry Co. Ltd.

- Loba Feinchemie GmbH

- Sasol Limited

- BASF SE

- Alteqo BV

- CPS Performance Materials Corp.

- Glentham Life Sciences Ltd.

- Impag AG

*- List not Exhaustive