Stick Packaging Market Overview: Growth Driven by Portion Control and Sustainability

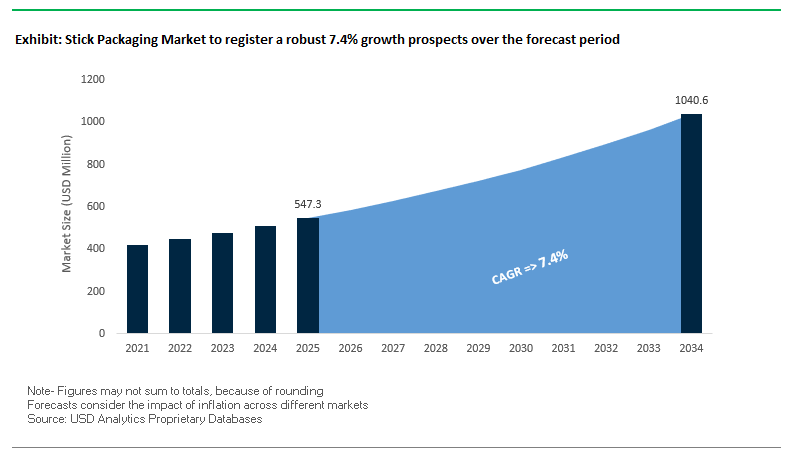

The Global Stick Packaging Market is projected to grow from $547.3 million in 2025 to $1,040.6 million by 2034, expanding at a CAGR of 7.4%. Stick packaging is rapidly gaining prominence as consumer preferences shift toward single-serve, portion-controlled, and on-the-go products. With strong adoption across the food, beverage, pharmaceutical, and nutraceutical industries, stick packs offer convenience, portability, and precision dosing, making them ideal for powdered drinks, instant coffee, supplements, and oral medicines.

Plastic continues to hold a dominant share in stick packaging, particularly biaxially oriented polypropylene (BOPP), which provides excellent strength, clarity, and barrier protection to extend product shelf life. However, the market is undergoing a significant sustainable transformation, with rising investments in paperboard and plant-based plastics that are biodegradable, compostable, and recyclable. The pharmaceutical sector is one of the most important growth drivers, leveraging stick packs to ensure accurate dosing, patient compliance, and product safety.

Key Insights for Industry Professionals

- Portability drives demand: Stick packs fit consumer needs for mobility and single-serve convenience.

- Plastic dominates: BOPP films provide essential moisture and barrier protection.

- Sustainability shift accelerating: Paperboard and bio-based plastics are reshaping the competitive landscape.

- Healthcare expansion: Nutraceuticals and pharmaceuticals are emerging as leading application segments.

Market Analysis: Recent Developments Reinforcing Innovation and Sustainability

The stick packaging industry is evolving through strategic mergers, eco-friendly material innovation, and global expansion initiatives. In August 2025, Smurfit WestRock formed from the Smurfit Kappa and WestRock merger reported strong Q2 results, showcasing enhanced capabilities to serve global markets, including flexible and stick packaging. Similarly, in February 2025, Mondi and Proquimia introduced a paper-based stand-up pouch for dishwashing tabs, advancing the shift toward recyclable and sustainable solutions for household products.

Collaborations and awards continue to highlight sustainability’s role. In March 2025, Constantia Flexibles and Aluflexpack AG partnered to strengthen their premium flexible packaging portfolio, while in January 2025, Constantia received two WorldStar Global Packaging Awards for its EcoPeelCover and EcoLamHighPlus solutions. On the innovation front, Mondi and Paulig’s recyclable mono-material coffee packaging launched in July 2024 emphasized the transition away from multi-layer plastics. Meanwhile, the Magical Mushroom Company secured $3 million in June 2024 to expand production capacity for mycelium-based, biodegradable packaging, signaling investor confidence in eco-materials.

Strategic restructuring also shaped the market. The Smurfit Kappa and WestRock merger in February 2025 created a new global leader in paper-based packaging with a strengthened focus on stick packaging applications. In addition, Mondi expanded EcoWicketBag production in February 2024 to meet demand from home and personal care segments.

Stick Packaging Market: Key Trends and Emerging Opportunities

Material Transition to Mono-Material, Polyolefin-Based Films for Recyclability

The stick packaging market is undergoing a major material transformation as converters and brand owners migrate from multi-material laminates, such as PET/ALU/PE structures, to recyclable mono-material polypropylene (PP) and polyethylene (PE) films. This transition is heavily influenced by Extended Producer Responsibility (EPR) regulations in markets such as the UK, which impose financial and logistical responsibility on producers for end-of-life packaging. To meet these obligations and avoid higher compliance costs, brands are prioritizing materials that integrate seamlessly into existing store drop-off recycling streams. In parallel, global sustainability pledges from companies like Nestlé are accelerating the adoption of mono-material structures across confectionery and powdered beverage product lines. These commitments are reshaping material supply chains, pushing converters to rapidly develop recyclable alternatives. Technological advancements in film extrusion and coatings now enable mono-material packaging to achieve oxygen and moisture barrier properties that were once only possible with aluminum- or PET-based laminates. This innovation ensures sensitive contents like instant coffee, electrolytes, and probiotics remain protected while keeping the package fully recyclable. The shift not only reduces environmental impact but also enhances compliance readiness and consumer trust in sustainable packaging.

Proliferation of High-Speed, Digital-Printed Short Runs for Personalized Nutrition

The growing demand for personalized nutrition, functional supplements, and niche product launches is propelling the stick packaging market toward digital printing technologies that support agile, short-run production. Traditional plate-based printing methods are cost-prohibitive for limited runs, but digital printing eliminates this barrier by enabling brands to create packaging variations quickly and economically. This capability has unlocked new strategies for seasonal promotions, localized campaigns, and market testing without inflating costs or lead times. Brands can print multiple designs on a single roll of film within hours, a major advantage for companies addressing regional flavor preferences or limited-edition product drops. Beyond marketing flexibility, digital printing also helps optimize inventory management. By reducing reliance on bulk pre-printed stock, brands minimize the risk of packaging waste from discontinued or short-lived SKUs. Furthermore, on-demand customization aligns with the sustainability agenda by lowering material waste and streamlining supply chains. For consumers, the result is packaging that is not only functional but also visually engaging and highly relevant to their lifestyle or health goals.

Development of High-Barrier, Bio-Based and Compostable Films

One of the most compelling opportunities for innovation in stick packaging lies in the development of bio-based and compostable films that deliver the high barrier performance required for sensitive products such as probiotics, instant coffee, and electrolyte powders. Conventional multi-material structures excel in blocking oxygen and moisture but are difficult to recycle, leaving a significant market gap. Academic research highlights the potential of modified bacterial cellulose films and new bio-based polymers that demonstrate strong water vapor and oxygen resistance. This research is fueling commercial efforts by material developers to produce compostable films that meet both performance and sustainability criteria. Certifications from organizations such as the Biodegradable Products Institute (BPI) are critical in assuring consumers of a legitimate end-of-life pathway, fostering trust and adoption. Biopolymers like polyhydroxyalkanoates (PHAs), derived from renewable resources, are at the forefront of this innovation wave. These materials promise plastic-like functionality with lower carbon footprints and industrial compostability, offering brands a premium sustainable packaging solution that resonates with eco-conscious consumers.

Integration of Smart Features for Dose Verification and Consumer Engagement

The compact format of stick packs presents a unique opportunity for digital and interactive enhancements that extend value beyond the physical product. Smart features such as QR codes, NFC tags, and augmented reality triggers can be seamlessly integrated into stick pack surfaces, transforming them into platforms for consumer engagement. These technologies provide direct access to dosage instructions, preparation guides, authentication tools, and even personalized brand storytelling. For instance, a QR code on an electrolyte stick pack could guide users to a video demonstration, simplifying preparation and reinforcing brand credibility. Serialized QR or NFC-enabled packs also create powerful anti-counterfeiting safeguards, allowing real-time product verification and traceability. This is especially critical in the nutraceutical and pharmaceutical stick packaging segments where consumer safety is paramount. Additionally, interactive features enhance marketing by offering recipes, promotions, or loyalty programs, directly boosting brand-consumer relationships. By leveraging digital connectivity, brands can turn functional stick packaging into a consumer experience tool, differentiating their products in an increasingly competitive marketplace.

Competitive Landscape: Leading Companies Shaping the Stick Packaging Industry

The global stick packaging market is highly competitive, driven by innovation in barrier materials, sustainability initiatives, and product customization. Major players are leveraging both plastic and paper-based solutions to address evolving consumer and regulatory demands.

Mondi Group: Driving Growth with FunctionalBarrier Paper

Mondi is a leader in sustainable paper and flexible packaging solutions, with strong offerings for stick packaging. Its FunctionalBarrier Paper Ultimate is a recyclable, ultra-high-barrier alternative to traditional plastic laminates. Mondi’s strategy focuses on developing compostable and recyclable products, leveraging renewable resources. The company’s partnerships and product launches in recyclable stick packaging formats highlight its position as a pioneer in sustainable innovation.

Amcor plc: Expanding with Recycle-Ready Stick Packaging Solutions

Amcor offers a wide range of films, foils, and pouches for stick packaging, serving food, nutraceutical, and personal care industries. Its AmPrima™ Recycle Ready Solutions and AmFiber™ Performance Paper combine high-barrier performance with recyclability. Amcor’s sustainability roadmap includes making all packaging recyclable or reusable by 2025. Its stick packaging is particularly valued for portion control and on-the-go applications, cementing its leadership in both conventional and eco-friendly formats.

Constantia Flexibles: Award-Winning Sustainable Stick Packaging

Constantia Flexibles is recognized for its premium flexible packaging solutions, with a strong presence in food, beverage, and pharmaceuticals. The company’s EcoPeelCover and EcoLamHighPlus products won WorldStar Global Packaging Awards in January 2025, underscoring its leadership in sustainable innovation. Constantia’s offerings include laminates and foils with high-barrier properties, ensuring freshness while reducing environmental impact. Its focus on digital packaging features, such as AR integration and anti-counterfeit designs, strengthens brand engagement.

Sonoco Products Company: Expanding Sustainable Paperboard Solutions

Sonoco’s stick packaging portfolio emphasizes paper-based canisters and pouches for food and pharma. In April 2025, the company divested non-core flexible packaging businesses to focus on its sustainability-driven core operations. Its EnviroSense™ line is a cornerstone of this strategy, offering recyclable paper containers as an alternative to plastics. Sonoco’s focus on circular economy packaging positions it as a trusted partner for brands seeking greener solutions without compromising functionality.

Huhtamaki Oyj: Flexible Stick Packs for Food and Snacks

Huhtamaki delivers flexible packaging solutions, including laminates and stick pack formats for snacks, powders, and dry foods. In mid-2025, the company launched a recyclable and compostable ice cream cup, reinforcing its sustainability leadership. For stick packaging, Huhtamaki provides customizable portion-control packs and easy-pour laminates, meeting the needs of convenience-driven consumers. Its global presence and focus on reducing plastic content make it a strong player in eco-friendly and food-safe packaging innovations.

Stick Packaging Market Share Insights

Powder Filling Leads Market Share by Filler Type in Stick Packaging

Powder filling dominates the stick packaging industry with a commanding 65% share, reflecting its perfect alignment with free-flowing applications like instant coffee, protein powders, electrolytes, condiments, and nutritional supplements. This leadership is reinforced by the boom in personalized nutrition, single-serve beverages, and precision dosing in medical nutrition. The stick pack format minimizes product waste while ensuring portability, creating a natural fit for powders where convenience and dosing accuracy are paramount. High-speed filling lines and material compatibility with moisture-barrier laminates further consolidate powder’s position, making it not just the current leader but also the foundation for scaling new stick packaging applications in foodservice and healthcare.

Food & Beverages Dominate Market Share by Application in Stick Packaging

Food and beverages account for 50% of stick packaging applications, making them the largest and most innovation-driven end-use sector. The segment’s dominance stems from the immense global demand for portion-controlled, on-the-go products such as instant coffee, tea, drink mixes, spices, and sweeteners. For FMCG brands, stick packs are not merely a packaging format but a marketing tool, enabling variety packs, sampling campaigns, and travel-friendly product lines that drive customer acquisition and brand engagement. Sustainability pressures are beginning to reshape this space, with efforts to develop recyclable or mono-material laminates that preserve barrier performance while reducing environmental impact. The segment’s scale and alignment with consumer convenience trends ensure that food and beverages will remain the strategic engine of growth in the stick packaging industry.

United States: Convenience and Sustainability Driving Stick Packaging Adoption

The U.S. stick packaging market is experiencing strong growth due to rising consumer demand for convenience and on-the-go formats, particularly in the food, beverage, and nutraceutical sectors. Single-serve stick packs for coffee, drink mixes, and dietary supplements are increasingly popular, providing pre-measured doses and portability. Technological advancements, including high-speed, multi-lane packaging machinery, have enabled manufacturers to produce stick packs at scale, making the format cost-effective for high-volume consumer goods.

Sustainability is a key focus area. The industry is increasingly adopting paper-based, mono-material, and fully recyclable solutions, catering to both brand and consumer preferences for eco-friendly packaging. Corporate initiatives further support market expansion; for example, Berry Global launched compact sizes for its Stick and Refill line in February 2025, targeting cosmetics and personal care while enhancing sustainability and travel-friendliness. Stick packaging is also gaining traction in OTC medications and nutritional supplements, where pre-measured powdered or granular forms provide discretion, convenience, and health-conscious dosing.

Germany: Regulatory Mandates and Circular Economy Strengthen Stick Packaging Market

Germany’s stick packaging industry is shaped by stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), which mandates fully recyclable packaging by 2030 and sets ambitious reuse and refill targets. These regulations have heightened demand for eco-friendly and recyclable stick packaging solutions, supporting the country’s leadership in the circular economy. Manufacturers are increasingly focusing on mono-material films made from polyethylene (PE) and polypropylene (PP) to improve recyclability while maintaining packaging performance.

Technological innovation is also a key driver. Companies are exploring collaborations to integrate stick packaging into efficient supply chains and develop cost-effective production methods for high-quality, sustainable packaging. The combination of regulatory compliance, sustainability initiatives, and advanced production technology positions Germany as a leader in eco-conscious stick packaging for the European market, particularly for food, nutraceutical, and personal care products.

China: Government Initiatives and Urbanization Fuel Demand for Stick Packaging

China’s stick packaging market is being propelled by the government’s dual carbon policies, which aim for carbon peak and carbon neutrality, and promote eco-friendly, reusable, and recyclable materials. Chinese manufacturers are investing heavily in automation, AI, and “5G plus industrial internet” technologies, optimizing production efficiency and enabling flexible manufacturing of stick packs.

Rapid urbanization and rising disposable incomes are boosting consumer demand for convenient, ready-to-use products, including instant coffee, spices, and nutraceutical powders. The expansion of domestic e-commerce platforms has further fueled the market, creating demand for secure, tamper-evident, and recyclable packaging. Combined with supportive government policies, these factors make China a key growth market for sustainable and technologically advanced stick packaging solutions.

India: Rising Convenience Culture and Sustainable Packaging Drive Market Growth

India’s stick packaging market is being shaped by the government’s Make in India and Zero Effect Zero Defect missions, which promote domestic manufacturing and industrial infrastructure investment. Rising disposable incomes and urbanization are shifting consumer preferences toward single-serve and convenient products, particularly instant coffee, spices, and nutraceutical powders, driving stick packaging adoption.

The market is also benefiting from technology investments, as high-speed, modern stick packaging lines become essential for efficiency and quality. With the Indian paper and packaging industry growing at 22–25% annually, manufacturers are scaling up operations to meet increasing demand. Sustainability remains central, with the Plastic Waste Management (Amendment) Rules creating a surge in demand for eco-friendly and recyclable packaging alternatives, making India an emerging hub for sustainable stick packaging solutions.

Stick Packaging Market Report Scope

Stick Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$547.3 Million

|

|

Market Size (2034)

|

$1040.6 Million

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Material (Polyester, BOPP, Paper, Aluminum, Metallized Polyester, Polyethylene, Polypropylene, Other Materials), By Filler Type (Powder, Liquid, Tablet), By Application (Food & Beverages, Pharmaceuticals, Cosmetics & Personal Care, Industrial, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Constantia Flexibles Group GmbH, Catalent, Inc., Winpak Ltd., Glenroy, Inc., Sonoco Products Company, Huhtamaki Oyj, ProAmpac, Mondi Group, DS Smith plc, WestRock Company, AR Packaging, UFlex Ltd., Unither Pharmaceuticals SAS, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Stick Packaging Market Segmentation

By Material

- Polyester

- BOPP

- Paper

- Aluminum

- Metallized Polyester

- Polyethylene

- Polypropylene

- Other Materials

By Filler Type

By Application

- Food & Beverages

- Pharmaceuticals

- Cosmetics & Personal Care

- Industrial

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Stick Packaging Market

- Amcor plc

- Constantia Flexibles Group GmbH

- Catalent, Inc.

- Winpak Ltd.

- Glenroy, Inc.

- Sonoco Products Company

- Huhtamaki Oyj

- ProAmpac

- Mondi Group

- DS Smith plc

- WestRock Company

- AR Packaging

- UFlex Ltd.

- Unither Pharmaceuticals SAS

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive research methodology to deliver actionable insights into the global Stick Packaging Market. Our approach combined primary research, including interviews with packaging manufacturers, brand owners in food, beverage, pharmaceutical, and nutraceutical sectors, and sustainability officers, with extensive secondary research from company reports, press releases, industry journals, and regulatory frameworks such as EPR mandates and EU Packaging Waste Regulations. Market sizing and growth projections were developed using historical trends, material adoption patterns (BOPP, mono-material films, bio-based plastics), and technological innovations in high-speed filling, digital printing, and barrier solutions. Segmentation analysis included material types, filler types, applications, and end-use industries, while qualitative insights focused on mergers and acquisitions, sustainability initiatives, and smart packaging integration. Competitive benchmarking highlighted leaders such as Amcor, Constantia Flexibles, Mondi, Sonoco, and Huhtamaki, emphasizing their contributions to eco-friendly, portion-controlled, and digitally enabled stick packaging solutions. This methodology ensures that USDAnalytics provides industry professionals with precise, forward-looking intelligence to guide strategic planning, investment decisions, and sustainable packaging initiatives.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.