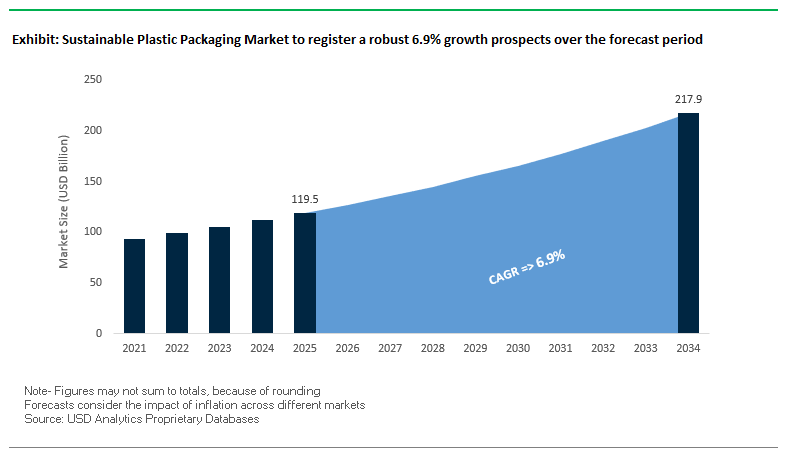

Sustainable Plastic Packaging Market Overview: Circular Designs, PCR Content and Mono-Material Films Drive Growth (MV USD 119.5 Bn, 2025 → USD 217.9 Bn, 2034; CAGR 6.9%)

Executive overview for buyers and strategy leaders. The global sustainable plastic packaging market is rapidly shifting from linear “take–make–dispose” models to circular economy systems built on mono-material design (PE/PP), post-consumer recycled (PCR) content, and design-for-recycling. Demand is strongest in FMCG, food & beverage, healthcare, and beauty, where brands must balance product protection, regulatory compliance, and decarbonization with shelf impact and line efficiency. Scale advantages now favor suppliers investing in recycling infrastructure upgrades, PCR quality control, and bio-based feedstocks to de-risk supply and meet Scope 3 targets.

Key insights at a glance

- Market vector: From USD 119.5 Bn (2025) to USD 217.9 Bn (2034) at 6.9% CAGR, powered by retailer mandates, EPR laws, and brand PCR targets.

- Recyclability first: Mono-material film/rigid formats replace multi-layer laminates, improving MRF sortability and end-market yield without compromising barrier in many SKUs.

- PCR supply security: Brand programs are lifting demand for food-grade rPET/rPE/rPP; proprietary cleaning and decontamination technologies are a differentiator.

- Bio-based runway: Early-stage bioplastics (e.g., plant-based PE, PLA blends) add decarbonization options where recycling streams are immature.

- System design: “Sustainable by design” now includes light-weighting, tethered closures, refill/reuse, and digital IDs for material tracking and sortation.

Market Analysis: Momentum Shifts to Mono-Material, PCR Scale-Up, and Recyclability Enhancements

Technology and policy tailwinds are accelerating investment and product launches. In August 2025, Amcor announced a UK recycling facility upgrade to boost high-quality PCR supply for its flexible portfolio, while Aptar Beauty (August 2025) launched TSP, an all-plastic, recyclable trigger sprayer for home/personal care streams—both moves aimed at improving true circularity at scale. A July 2025 academic review spotlighted advanced additives that enhance mechanical and antimicrobial properties in sustainable films, enabling down-gauging without sacrificing pack performance. On the conversion front, Mondi (June 2025) partnered with Saga Nutrition on recyclable mono-material dry-pet-food bags, and in April 2025 created a recyclable pre-made paper bag for chemical powders with Evonik, removing a plastic-coated layer to lower product carbon footprints.

Hardware and component innovation support functionality with less material. LINDAL Group (April 2025) introduced FlipStraw—a dual spray actuator with a foldable straw—to cut product waste and improve usability in aerosols. Berry Global (March 2025) detailed progress in its 2024 Sustainability Report, including portfolio recyclability and increased bioplastics purchasing—evidence that resin sourcing strategies now blend PCR and bio-based inputs. Ecosystem collaboration continues: UFlex (January 2025) partnered with the Indian Institute of Packaging to expand recycling and circularity via an innovation hub, signaling growing emphasis on infrastructure + design standards to convert pilot programs into mainstream, MRF-compatible packaging.

Trends and Opportunities in the Sustainable Plastic Packaging Market

Design for Recycling through Mono-Material Polyolefin Structures

One of the most influential trends in the sustainable plastic packaging market is the accelerated adoption of mono-material structures designed for recyclability. Traditionally, high-barrier requirements forced the use of multi-layer laminates, combining materials like PET, PE, and aluminum, which were incompatible with conventional recycling streams. However, innovation is breaking this trade-off. Mondi Group has developed a mono-material polypropylene (PP) stand-up pouch with ultra-high oxygen, moisture, and light barrier properties. Certified with an AAA recyclability rating (over 95%) by the German Institute Cyclos-HTP, this demonstrates that packaging can achieve both high performance and recyclability.

Commercial adoption is accelerating. Nestlé is piloting mono-material flexible packaging for its baby food products, while Unilever is deploying all-PE pouches across its personal care portfolio to meet its circular economy commitments. A critical enabler of this shift is the emergence of advanced mono-oriented polyethylene (MOPE) and similar films engineered to run seamlessly on existing high-speed packaging lines. This reduces capital barriers for brands, enabling the transition without costly infrastructure overhauls. As these innovations scale, mono-material packaging is expected to become the industry standard for high-barrier applications, particularly in food, beverages, and personal care.

Significant Investment in Advanced (Chemical) Recycling Capacity

Another major trend shaping the sustainable plastic packaging market is the large-scale expansion of advanced chemical recycling infrastructure. Mechanical recycling struggles to handle multi-layer plastics, colored packaging, and contaminated waste streams, creating a critical need for molecular-level recycling solutions. Substantial capital is being invested worldwide to meet this demand. In September 2025, Ester Industries and Loop Industries announced a $192 million chemical recycling facility in Gujarat, India, with a projected capacity of 70,000 metric tons annually, signaling strong growth in Asia’s circular economy landscape.

Similarly, in the United States, the Department of Energy allocated $375 million to fund new chemical recycling projects, while ExxonMobil expanded its pyrolysis capacity in Texas by 350 million pounds annually, with further projects in Europe. These moves highlight how governments and corporations are aligning to create scalable recycling infrastructure. By converting hard-to-recycle plastics into virgin-quality feedstocks, advanced recycling ensures a consistent supply of high-purity PCR resins that meet stringent packaging requirements, closing the loop for sustainable plastic packaging.

Development of Drop-in Bio-Based Polymers

A major growth opportunity lies in scaling bio-based plastics that function as drop-in replacements for fossil-derived polymers. Braskem’s bio-polyethylene (bio-PE), produced from sugarcane, captures 2.12 tons of CO₂ per ton produced, making it a carbon-negative material. This environmental advantage positions bio-PE as a key enabler for brands aiming to meet their net-zero and ESG targets.

The unique appeal of drop-in polymers is their chemical equivalence to conventional plastics. They can be processed on existing extrusion, molding, and lamination equipment without modification, offering cost-neutral scalability. Furthermore, they can be recycled in the same streams as conventional PE and PP, eliminating complexity at the end of life. This dual advantage of renewability and recyclability makes bio-based polymers one of the most promising long-term solutions for sustainable packaging across sectors like FMCG, food & beverage, and healthcare.

Digital Watermarks for Precision Sorting and Circularity

A second transformative opportunity is the integration of digital watermarking technologies into packaging to enable high-precision sorting. The HolyGrail 2.0 initiative, involving over 88 global companies, has successfully conducted large-scale industrial trials with remarkable results—99% detection accuracy, 95% ejection rates, and 95% purity levels. By embedding imperceptible digital codes directly into packaging, waste management systems equipped with high-resolution cameras can differentiate packaging at the SKU level, such as separating food-grade PET from non-food PET.

This technology addresses one of the recycling industry’s biggest barriers: ensuring food-contact-safe PCR supply. By enabling granular separation, digital watermarks make high-value recycling economically viable and scalable. If adopted globally, this solution could redefine plastic circularity, drastically reducing downcycling and unlocking closed-loop systems for packaging manufacturers and brand owners.

Competitive Landscape: Leaders Scaling Recycle-Ready Formats, PCR, and Circular Infrastructure

A concentrated set of packaging majors are redefining sustainable plastic packaging via materials science, in-line manufacturability, and end-of-life pathways. Below, each player’s proposition in sustainability, performance and scale.

Amcor: Scaling AmPrima™ recycle-ready and PCR integration for global brands

Amcor’s portfolio spans flexible and rigid formats with AmPrima™ recycle-ready pouches and PCR-rich bottles/jars. In August 2025, it upgraded a UK recycling facility to secure high-quality PCR for flexibles and recently launched a 50% recycled-content paint container with Flügger—a signal of rigid PCR readiness. Its strengths are a global converting footprint, deep materials science, and a vertically integrated model that accelerates design-for-recycling transitions without sacrificing seal integrity, OTR/MVTR, or machinability. Strategic focus: circular economy leadership through R&D and customer co-development to meet retailer and EPR scorecards.

Berry Global: Circularity at scale with CleanStream® and Impact 2025 roadmap

Berry’s breadth across rigids, closures, and films enables rapid roll-outs of light-weighted, PCR-content solutions. In March 2025, Berry’s 2024 Sustainability Report cited that 93% of FMCG packaging is recyclable or has a validated recyclable alternative, and bioplastics purchases rose 130% YoY—evidence of multi-path decarbonization. Core leverage: CleanStream® high-quality recycled resins, global tooling, and line-ready specs for food-contact and personal care. Strategy centers on its Impact 2025 framework to scale PCR, bio-based inputs, and design-for-recycling while preserving brand aesthetics and barrier performance.

AptarGroup: Recyclable dispensing systems and active packaging enhance circularity

Aptar brings dispensing, drug-delivery, and active material science into sustainable plastic packaging via recyclable closures, pumps, and triggers (e.g., SimpliCycle™). In August 2025, Aptar Beauty launched the all-plastic TSP trigger, enabling mono-material recovery within existing streams. Differentiators include active closures (desiccants/oxygen control) that maintain product stability even as structures are light-weighted or mono-materialized. Strategy: lead circular dispensing with components designed for recyclability, reusability, or certified recycled content, supporting full-pack sustainability claims.

Mondi: Mono-material flexibles and paper-plastic hybrids via EcoSolutions

Mondi’s EcoSolutions approach delivers recycle-ready plastic films, mono-material PE/PP laminates, and paper-based alternatives where feasible. In June 2025, it introduced recyclable mono-material bags with Saga Nutrition; in April 2025, it co-developed a recyclable paper bag for chemical powders with Evonik; and it has advanced paper-based secondary alternatives (e.g., Hug&Hold). Mondi’s strength is its dual competence in paper and plastics, allowing fit-for-purpose selections that meet performance, MRF compatibility, and brand carbon targets.

DS Smith: Fiber systems replacing problem plastics and enabling circular logistics

DS Smith focuses on fiber-based packaging, retail-ready and transit formats, and plastic replacement initiatives. It has replaced >1 billion plastic items ahead of its 2025 pledge and, in January 2025, combined with International Paper, expanding reach into healthcare and pharmaceutical packaging adjacencies. The company’s Circular Design Principles and closed-loop model help customers raise recycled content, improve recyclability, and cut supply-chain waste—often pairing with sustainable plastic solutions where barrier or hygiene is essential.

Sustainable Plastic Packaging Market Share Insights, 2025-2034

Rigid Packaging Leads Market Share by Packaging Format in Sustainable Plastic Packaging Industry

Rigid packaging holds the majority share of the sustainable plastic packaging industry, accounting for 55% of the market, primarily because of its established recycling infrastructure and technical maturity. PET and HDPE rigid formats—bottles, tubs, jars, and clamshells—are already supported by robust collection and recycling systems in most developed economies, giving them a structural advantage over flexible alternatives. Brands have rapidly increased the integration of high percentages of post-consumer recycled (PCR) content into rigid formats without compromising performance, making this category the backbone of the industry’s transition to circularity. The scalability of rPET water and beverage bottles, PCR-HDPE detergent bottles, and lightweight thermoformed containers also reinforces rigid packaging’s lead, especially as regulatory frameworks such as the EU’s PPWR and U.S. state-level PCR mandates prioritize rigid formats for compliance. While flexible packaging is catching up with mono-material innovation, rigid packaging remains the dominant segment because it combines cost efficiency, consumer familiarity, and proven recyclability.

Food & Beverages Command the Largest Share by Application in Sustainable Plastic Packaging Industry

Food and beverages account for 60% of the sustainable plastic packaging market, making this segment the undisputed growth engine. The dominance of this sector is driven by its scale and regulatory scrutiny, as it encompasses fresh produce, snacks, dairy, frozen foods, and ready-to-eat meals—categories that generate some of the highest volumes of single-use plastics. Within this sector, fresh produce alone represents 40% of the sub-segment share, with retailers shifting rapidly to rPET trays, rPP clamshells, and compostable films to comply with global plastic reduction targets. Snacks and confectionery account for another 30%, serving as the epicenter of flexible packaging innovation, where mono-material PP and PE structures are being developed to balance recyclability with high-barrier performance. Dairy and frozen foods rely on PCR-based rigid tubs and bottles, while ready-to-eat meals are increasingly packaged in recycled-content CPET trays with recyclable lidding films. The sector’s sheer size, consumer visibility, and strong regulatory drivers ensure that food and beverages remain the leading application for sustainable plastic packaging.

United States: EPR Laws and Mono-Material Packaging Innovations

The United States sustainable plastic packaging market is being reshaped by progressive state-level regulations and federal sustainability initiatives. California’s SB 54 Extended Producer Responsibility (EPR) law, which mandates producers to take financial and physical responsibility for packaging end-of-life management, is setting the pace, with Washington and Maryland adopting similar frameworks in 2025. Adding further momentum, California increased its plastic beverage bottle recycled content mandate to 25% in October 2025, pushing brand owners toward circular packaging strategies. On the federal side, the U.S. Environmental Protection Agency (EPA) is advancing its national goal of a 50% recycling rate by 2030, which is encouraging major investments in recycling infrastructure and the adoption of recyclable mono-material solutions.

Industry leaders are responding to these pressures with product innovation. Ball Corporation launched its ReAl® aluminum aerosol can, reducing the carbon footprint by 50% compared to conventional formats, while companies are increasingly commercializing PVC-free and aluminum-free blister systems that align with recycling mandates. The e-commerce sector further fuels demand for durable, lightweight, and space-efficient packaging, making sustainability a competitive necessity. Together, these dynamics are pushing U.S. companies to integrate bio-based resins, post-consumer recycled (PCR) plastics, and circular business models into their packaging portfolios.

European Union: PPWR, ESPR, and Digital Product Passport Driving Change

The European Union sustainable plastic packaging market is undergoing a regulatory transformation with the enforcement of the Packaging and Packaging Waste Regulation (PPWR) in February 2025. This landmark legislation requires all plastic packaging placed on the EU market to contain minimum percentages of post-consumer recycled content by 2030, making recyclability a non-negotiable standard. The Ecodesign for Sustainable Products Regulation (ESPR) complements these efforts by requiring packaging products to be durable, reusable, and repairable, accelerating the development of refillable systems and reusable components.

In addition, the introduction of a Digital Product Passport (DPP) by the EU mandates transparency on packaging material origin, recyclability, and compliance, further encouraging traceability across supply chains. Financial support through Horizon Europe programs is funding R&D into bio-based polymers, starch blends, and cellulose films, supporting the next generation of sustainable materials. Industry players such as Mondi are innovating with flexible paper laminates and fiber-based solutions that meet both regulatory and consumer demands for sustainability. Collectively, these measures position Europe as a global leader in circular economy-driven packaging innovation.

China: Advanced Packaging with High-End Security Features

The China sustainable plastic packaging market is evolving under the directives of the “14th Five-Year Plan”, which emphasizes plastic pollution control and eco-friendly packaging mandates effective June 2025. These regulations compel express delivery companies and e-commerce giants to adopt reduced, reusable, and recyclable packaging, directly influencing demand for sustainable films, containers, and protective formats. The government is also promoting the remanufacturing industry, offering tax incentives to companies investing in green technologies.

A notable trend in China is the growing demand for high-end packaging with enhanced barrier properties and anti-counterfeiting features, driven by both consumer safety concerns and regulatory pressures. The Ellen MacArthur Foundation’s joint report with Tsinghua University has underscored the urgent need to expand China’s plastic recycling infrastructure and foster a market for high-quality recycled plastics. With consumer preference shifting toward premium, eco-friendly packaging solutions, companies are investing in bio-based plastics, security-enabled smart labels, and multilayer recyclable structures to align with both compliance and consumer expectations.

India: EPR Mandates and Traceable Packaging Regulations

The India sustainable plastic packaging market is advancing rapidly due to strong policy interventions and growing consumer awareness. The Plastic Waste Management (Amendment) Rules, 2024, effective April 2025, place Extended Producer Responsibility (EPR) obligations on producers, importers, and brand owners, mandating accountability for post-consumer recycling. Further strengthening transparency, the July 2025 mandate requires all plastic packaging to carry barcodes or QR codes, ensuring material traceability and environmental accountability.

While MSMEs are exempt from EPR compliance, the burden falls on larger manufacturers and raw material suppliers, driving innovation in eco-friendly resins, compostable formats, and recyclable mono-material solutions. The Indian government is also investing in reverse logistics systems, obligating producers to manage post-consumer collection and recycling. With the country’s e-commerce and retail sectors booming, demand for durable, lightweight, and traceable packaging formats is rising. These measures make India one of the fastest-growing markets for sustainable packaging solutions in Asia, particularly for consumer goods, food delivery, and healthcare applications.

Japan: Plastic Resource Circulation Strategy and Industry Collaborations

The Japan sustainable plastic packaging market is shaped by the government’s Plastic Resource Circulation Strategy, which requires that all plastic packaging be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, effective the same year, mandates the redesign of 12 categories of single-use plastic products, fueling adoption of reusable, compostable, and bio-based alternatives. Regulatory oversight is further strengthened by the Ministry of Health, Labor and Welfare (MHLW), which introduced a positive list system for synthetic food containers and packaging effective June 2025, ensuring material safety in contact applications.

Beyond regulation, industry collaboration is a cornerstone of Japan’s approach. Companies such as Toppan, Mitsubishi Chemical Group, and Kyoei Chemical are working on recycling technologies for separating, delaminating, and de-inking composite plastics, with implementation targeted by 2027. These innovations aim to create closed-loop recycling systems that drastically improve material recovery rates. Japan’s dual focus on bio-based material adoption and advanced recycling infrastructure is accelerating its transition toward a circular packaging economy, particularly in food, pharmaceuticals, and consumer goods.

Brazil: Reverse Logistics and Waste Import Ban Supporting Circularity

The Brazil sustainable plastic packaging market is progressing under robust policy support. The National Solid Waste Policy (PNRS) establishes the framework for responsible waste disposal, recycling, and reduction, while Law No. 15,088, effective January 2025, bans the import of plastic waste and rejects. This move compels businesses to depend on domestic recycling systems and renewable raw materials.

Brazil is also investing heavily in reverse logistics systems that make producers responsible for collecting and recycling post-consumer packaging, aligning with circular economy principles. These frameworks encourage companies to explore sugarcane bagasse-based plastics, biodegradable resins, and PCR-integrated packaging formats. With sustainability becoming a defining feature of Brazil’s packaging ecosystem, businesses across consumer goods, healthcare, and retail are prioritizing compostable and recyclable solutions to comply with regulations and meet consumer expectations.

Sustainable Plastic Packaging Market Report Scope

Sustainable Plastic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$119.5 Billion

|

|

Market Size (2034)

|

$217.9 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Material (Recycled Plastics, Bio-based Plastics, Biodegradable & Compostable Plastics, Recycled Paper & Paperboard, Composites & Laminates), By Packaging Format (Rigid Packaging, Flexible Packaging), By Application (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, E-commerce & Retail, Industrial), By End-Use Industry (Food & Beverage, Consumer Goods, E-commerce & Logistics, Healthcare, Home & Personal Care)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Huhtamaki Oyj, Mondi Group, Smurfit Kappa Group, Sealed Air Corporation, Sonoco Products Company, DS Smith plc, Constantia Flexibles Group GmbH, WestRock Company, Pactiv Evergreen Inc., Alpla, PlastiPak Holdings, Inc., Novamont S.p.A., NatureWorks LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sustainable Plastic Packaging Market Segmentation

By Material

- Recycled Plastics

- Bio-based Plastics

- Biodegradable & Compostable Plastics

- Recycled Paper & Paperboard

- Composites & Laminates

By Packaging Format

- Rigid Packaging

- Flexible Packaging

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- E-commerce & Retail

- Industrial

By End-Use Industry

- Food & Beverage

- Consumer Goods

- E-commerce & Logistics

- Healthcare

- Home & Personal Care

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sustainable Plastic Packaging Market

- Amcor plc

- Berry Global, Inc.

- Huhtamaki Oyj

- Mondi Group

- Smurfit Kappa Group

- Sealed Air Corporation

- Sonoco Products Company

- DS Smith plc

- Constantia Flexibles Group GmbH

- WestRock Company

- Pactiv Evergreen Inc.

- Alpla

- PlastiPak Holdings, Inc.

- Novamont S.p.A.

- NatureWorks LLC

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-layered research methodology to analyze the sustainable plastic packaging market, integrating both primary and secondary research techniques to ensure the accuracy and reliability of insights. Our process begins with the collection of macroeconomic, industry, and regulatory data from verified sources, including government publications, company filings, investor presentations, trade associations, and peer-reviewed journals. USDAnalytics then conducts extensive primary interviews with key stakeholders, including packaging manufacturers, brand owners, material suppliers, recyclers, and policy experts, to validate market trends, adoption drivers, and challenges. Advanced analytical frameworks, such as market sizing models, CAGR calculations, and scenario forecasting, are applied to project revenue, product adoption, and regional growth patterns from 2025 to 2034. We further segment the market by material, packaging format, application, and end-use industry, providing actionable insights into mono-material adoption, PCR integration, bio-based polymer development, and digital sorting technologies. Regional regulatory impacts, such as EPR mandates, PPWR compliance, and traceability requirements, are carefully analyzed to assess influence on market dynamics. Competitive landscape assessments examine leading players’ strategies, innovation pipelines, and scale-up initiatives to identify opportunities for collaboration, differentiation, and investment. USDAnalytics ensures that the final output reflects a precise balance of current industry realities, emerging trends, and strategic foresight, equipping decision-makers with actionable intelligence for sustainable growth and circular economy alignment.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.