Triton X-100 Market Overview 2025–2034: $939.6 Million to $1,457.6 Million at 5% CAGR Under Regulatory Phase-Out Pressure and Biopharma Reformulation

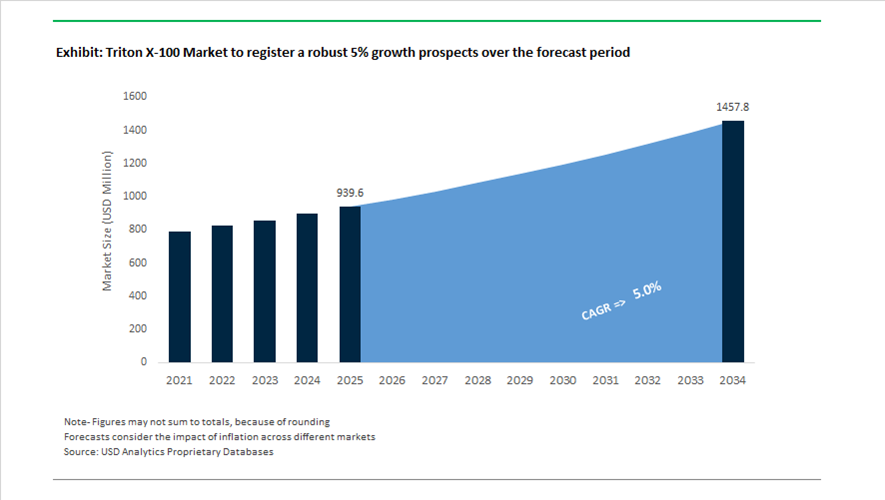

The global Triton X-100 market is valued at $939.6 million in 2025 and is projected to reach $1,457.6 million by 2034, expanding at a CAGR of 5%. Triton X-100, an octylphenol ethoxylate (OPE) nonionic surfactant with an HLB value of approximately 13.5, has historically been critical in biopharmaceutical viral inactivation, cell lysis, membrane solubilization, industrial cleaning, and specialty formulations. Market structure is undergoing structural realignment due to regulatory pressure under EU REACH Annex XIV, global expansion of SVHC-style restrictions, and accelerated substitution toward biodegradable and nitrosamine-free alternatives. Growth through 2034 is expected to be concentrated in research-grade and exempt bioprocessing applications, while legacy APE-based industrial uses continue to contract in regulated regions.

Regulatory dynamics intensified from 2024 onward. Throughout 2024, authorities in Asia and North America initiated alignment discussions with the European Chemicals Agency ban framework, triggering voluntary phase-out programs by global biopharma companies seeking long-term supply security. In late 2025, the European Commission postponed the broader REACH revision to 2026, extending the regulatory timeline but maintaining Triton X-100’s status on Annex XIV. As of December 18, 2025, all REACH registration and Classification & Labelling data for octylphenol ethoxylates were migrated to the new ECHA CHEM platform, improving traceability and compliance management for industrial users. This digital consolidation enables more granular tracking of authorization status, exposure scenarios, and safety documentation, reinforcing the compliance burden for formulators and contract manufacturers.

Substitution technologies and portfolio shifts accelerated between 2024 and 2026. In late 2024, Croda Pharma launched its Virodex™ TXR-1 and TXR-2 detergents as cGMP-manufactured replacements engineered to deliver equivalent viral inactivation and cell lysis performance without nitrosamine formation risk. In mid-2025, Merck expanded its Deviron® detergent portfolio, positioning these biodegradable surfactants as scalable alternatives tailored for downstream purification compatibility in bioprocessing. In late 2025, Dow reprioritized its ECOSURF™ and other next-generation surfactant lines, gradually de-emphasizing legacy APE-based Triton formulations in favor of 2026-compliant chemistries. During the same period, AI-driven surfactant discovery programs gained traction, with approximately 15% of R&D budgets at major chemical manufacturers allocated toward identifying drop-in replacements capable of replicating Triton X-100’s HLB profile and solubilization efficiency.

Despite industrial restrictions, niche resilience remains in high-purity laboratory applications. In May 2025, Promega reaffirmed the availability of molecular biology-grade Triton X-100 for research-exempt applications, including autoimmune and antiviral signaling studies. Corporate strategy adjustments reflect the broader transition. In February 2026, PerkinElmer announced an ESG-driven pivot prioritizing sustainable reagent distribution for industrial and biopharma clients. In September 2025, Triton Valves completed a subsidiary merger to streamline governance, while in early 2025 BlueTriton Brands finalized a major merger affecting industrial cleaning supply chains that rely on advanced surfactant systems.

Regulatory Sunset, Process Revalidation, and Replacement Economics in the Triton X-100 Market

Regulatory Rescaling of Pharmaceutical Bioprocessing and Viral Inactivation

The Triton X-100 market in 2025 is defined less by incremental demand growth and more by regulatory inevitability. The classification of Octylphenol Ethoxylates as Substances of Very High Concern has turned Triton X-100 from a trusted industry standard into a compliance liability for biopharmaceutical manufacturers. Its historical role in viral inactivation for monoclonal antibodies, plasma-derived therapies, and vaccines is now under direct pressure from evolving global guidance that prioritizes biodegradability and environmental safety without compromising viral clearance performance.

The adoption of the revised ICH Q5A(R2) guideline has institutionalized this transition. By explicitly recognizing alternative detergents for viral safety, the guideline has forced pharmaceutical companies to embed non-NPE surfactants into Chemistry, Manufacturing, and Controls submissions across 2024 and 2025. This is not a discretionary optimization exercise. For products operating at low-temperature viral inactivation windows between 15°C and 28°C, failure to align with revised expectations introduces approval delays, post-approval change burdens, and long-term market access risk.

The economic stakes are substantial. Regulatory assessments in Europe estimate that unresolved authorization uncertainty for OPEs places billions of euros of biologics value at risk. As a result, leading biopharma firms are committing tens of millions of euros per molecule to revalidate entire manufacturing workflows using Triton X-100 alternatives. This spending is justified not by performance gaps but by the need to avoid abrupt authorization sunsets that could halt commercial production. Consequently, Triton X-100 demand in pharmaceutical bioprocessing is undergoing structural erosion rather than cyclical fluctuation.

Strategic Stockpiling and Inventory Overhang in Legacy Industrial Applications

Outside regulated life sciences, Triton X-100 is experiencing a very different but equally transitional demand pattern. Legacy industrial sectors such as textiles, oilfield chemicals, and architectural coatings are engaging in deliberate last-time-buy strategies to preserve validated formulations that cannot be rapidly reformulated without performance or certification risk. This behavior has created a temporary demand bulge that masks the underlying contraction of the addressable market.

Throughout 2025, manufacturers in North America and Europe have focused on supply chain de-risking rather than long-term procurement. By front-loading purchases ahead of regulatory tightening and tariff adjustments, these firms have built inventories sufficient to sustain production through multi-year depletion cycles. Trade data indicates that while apparent consumption showed short-term stability, underlying import and export volumes declined as companies pivoted away from ongoing dependence on Triton X-100 toward domestically sourced substitutes.

Tariff-driven front-loading in the United States has further amplified this effect. Elevated inventories are suppressing spot prices and delaying visible demand destruction, but this should not be interpreted as market resilience. Instead, it reflects a classic sunset pattern where consumption persists temporarily due to inventory drawdown rather than repeat purchasing. As these stocks are exhausted through 2026, replacement surfactants are expected to displace Triton X-100 permanently rather than coexist alongside it.

Commercialization of Bio-Based Drop-In Replacement Kits

The most immediate and commercially attractive opportunity emerging from Triton X-100’s decline lies in drop-in replacement systems designed to preserve validated protocols. Laboratories, contract research organizations, and diagnostic manufacturers are unwilling to redesign assays, buffers, and solubilization workflows simply to remove a surfactant. This has created strong demand for alternatives that replicate Triton X-100’s micellar behavior, protein compatibility, and temperature performance while offering improved environmental profiles.

Next-generation nonionic surfactants are being positioned explicitly as one-to-one substitutes, with critical micelle concentration, cloud point, and solubilization efficiency engineered to closely match Triton X-100. In 2025, these alternatives are no longer sold as generic green surfactants but as compliance-enabling tools that reduce regulatory exposure without altering experimental outcomes. This positioning is particularly powerful in the in vitro diagnostics segment, where assay reproducibility and regulatory stability are paramount.

The opportunity extends beyond reagents into packaged substitution kits that bundle surfactants with validated protocols and transition guidance. By lowering switching friction, suppliers are capturing share not through price competition but through risk mitigation. As laboratories standardize on these replacements, repeat demand shifts structurally away from Triton X-100, accelerating volume decline while supporting premium pricing for validated alternatives.

Reactive Surfactants and Emulsion Polymerization Innovation

A second, more technically differentiated opportunity is emerging in polymer emulsions and coatings, where the exit of Triton X-100 is catalyzing innovation rather than direct substitution. In high-performance emulsions, especially those used in automotive coatings and construction materials, formulators are increasingly adopting reactive surfactants that become chemically bound within the polymer matrix.

These reactive systems address one of the fundamental weaknesses of Triton X-100, namely leaching during service life, which contributes to VOC emissions, surface defects, and durability loss. As electric vehicle production scales globally and coating specifications tighten around water resistance and environmental performance, non-leachable surfactants are becoming a design requirement rather than a differentiator.

In Asia-Pacific markets, regulatory momentum toward low-VOC architectural paints is reinforcing this shift. Biodegradable and polymerizable surfactants offer formulators a pathway to meet environmental standards while improving coating performance. Importantly, these innovations also simplify regulatory review, as bound surfactants reduce exposure concerns under chemical control frameworks. This positions reactive surfactants as long-term growth drivers in segments where Triton X-100 once played a foundational but now obsolete role.

Triton X-100 Market Share and Segmentation Insights

Product Grade Market Share: Technical Grade Leads Amid Regional Regulatory Divergence

Technical grade Triton X-100 holds a 52.80% share in 2025, driven by its continued use in industrial cleaners, paints and coatings, and textile processing in regions with fewer regulatory restrictions. Its cost-effectiveness and established performance sustain demand in Asia and Latin America, while laboratory, molecular biology, and diagnostic grades serve specialized high-purity applications. A key market dynamic is regulatory-driven divergence, where nonylphenol ethoxylate restrictions in Europe and North America have accelerated the shift toward alternative nonionic surfactants, creating a dual-market structure where technical grade persists in less regulated regions but declines in compliant markets.

Application Market Share: Bioprocessing and Life Sciences Segment Leads with Critical Biopharma Applications

Bioprocessing and life sciences account for 38.60% of the Triton X-100 market in 2025, supported by its essential role in protein extraction, virus inactivation, and cell lysis in biopharmaceutical manufacturing. Laboratory and diagnostic uses, legacy industrial applications, and alternative nonionic surfactants represent additional segments with evolving demand patterns. A key growth factor is the criticality of Triton X-100 in validated biopharma processes, where replacing the surfactant requires extensive process revalidation and regulatory approval. This has sustained demand in life sciences even as industrial applications increasingly transition to compliant surfactant alternatives.

Triton X-100 Market Competitive Landscape

The Triton X-100 market in 2026 is defined by bio-interfacial substitution, with leading manufacturers prioritizing biodegradable, REACH-compliant surfactants that replicate HLB 13.5 performance, micelle aggregation behavior, and cloud point characteristics required for viral inactivation, protein solubilization, and biopharmaceutical processing.

Dow Inc. Leads Triton Replacement Strategy with ECOSURF™ and TERGITOL™ Portfolios

Dow Inc. is spearheading the transition in the Triton X-100 market through a managed phase-out strategy supported by its ECOSURF™ and TERGITOL™ surfactant platforms. Products such as ECOSURF™ EH-9 and TERGITOL™ 15-S-9 are engineered as ready-to-use replacements, delivering equivalent wetting, detergency, and HLB alignment without APEO-associated ecotoxicity. The ECOSURF™ SA-9 series, derived from seed oils, offers 100% biodegradability under OECD 301F, targeting life sciences and bioprocessing applications. Dow’s TERGITOL™ TMN-100X provides low surface tension and rapid dissolution, making it suitable for industrial cleaning and coatings. Through its APE transition program, the company provides detailed comparative data on CMC and performance equivalence. This data-driven substitution strategy strengthens its leadership in sustainable nonionic surfactants.

Croda International Captures Biopharma Shift with Virodex™ Triton Alternatives

Croda International Plc is emerging as a disruptive force in the Triton X-100 market by addressing the regulatory-driven demand for validated biopharmaceutical surfactant replacements. Its Virodex™ TXR-1 and TXR-2 are designed for viral inactivation and cell lysis, offering 100% biodegradability and compendial-grade compliance under cGMP EXCiPACT standards. Integration of Solus Biotech and expansion of Avanti Polar Lipids has enabled a sovereign supply chain for high-purity bioprocessing materials. Croda’s development of PPB-level analytical detection ensures complete removal validation of surfactants from final drug products, overcoming key regulatory barriers. Collaboration with U.S. authorities to scale domestic vaccine component production enhances strategic positioning. Its transition to a pure-play life sciences model reinforces focus on high-margin, sustainable ingredients.

Merck KGaA Advances EcoDesign Detergents for Triton-Free Bioprocessing

Merck KGaA is accelerating Triton replacement in laboratory and clinical workflows through its EcoDesign-driven Deviron® detergent portfolio. These surfactants are optimized for downstream protein purification and demonstrate superior removal efficiency, a critical parameter in biologics manufacturing. The company is integrating Raman spectroscopy for real-time monitoring of detergent concentration in CHO cell cultivation, enabling precise dosing of Triton alternatives. By early 2026, Merck transitioned over 80% of its diagnostic kit production to Triton-free formulations, validating large-scale feasibility. Its SMC™ scoring framework provides transparent environmental metrics, including biodegradability and aquatic toxicity, guiding regulatory-compliant surfactant selection. This combination of process innovation and sustainability benchmarking strengthens its role in next-generation life science materials.

Thermo Fisher Scientific Expands Dual-Track Supply and Pre-Formulated Triton-Free Systems

Thermo Fisher Scientific Inc. is positioning itself as a transition enabler in the Triton X-100 market through dual-track supply and application-integrated surfactant systems. While maintaining limited availability of Triton X-100 for legacy use, the company promotes Surfact-Amps™ solutions, offering pre-diluted, high-purity detergents that reduce handling risks. Its integration of Triton alternatives such as polysorbates and Nonidet P-40 substitutes into RIPA buffers supports advanced proteomics and immunopeptidomics workflows. The company’s 2026 catalog update highlights over 500 green surfactant SKUs with REACH-compliant labeling, facilitating procurement decisions. Investment in single-use bioprocessing systems with pre-loaded Triton-free detergents enhances containment and reduces environmental exposure. This application-centric approach strengthens Thermo Fisher’s relevance across research and biomanufacturing ecosystems.

Shell Chemicals Enables Bio-Based Feedstock Supply for Next-Generation Surfactants

Shell Chemicals is a critical upstream player in the Triton X-100 market, supplying high-purity alcohols required for alcohol ethoxylate-based alternatives. Its NEODOL™ range serves as a foundational feedstock for biodegradable nonionic surfactants replacing octylphenol ethoxylates in industrial and home care applications. Shell is scaling bio-based NEODOL production using renewable feedstocks to support downstream manufacturers in achieving Scope 3 emission reductions. Its Geismar facility, the world’s largest alpha olefins plant, provides vertically integrated production of high-purity ethoxylates, ensuring supply chain stability. The company is advancing circular chemical initiatives, including the use of chemically recycled plastic waste to produce surfactant intermediates. This upstream integration positions Shell as a key enabler of sustainable surfactant innovation.

United States Triton X-100 Market Dynamics Driven by Regulatory Harmonization and Industrial End-Use Persistence

The United States Triton X-100 market is in a controlled transition phase, shaped by regulatory alignment in life sciences and sustained demand in industrial applications. In mid-2025, leading domestic chemical suppliers, including Dow Inc., accelerated strategic portfolio rationalization programs aimed at reducing exposure to octylphenol ethoxylates. While Triton X-100 continues to serve as a historical performance benchmark for non-ionic surfactants, Tier-1 biopharma customers are increasingly being guided toward alternatives such as the Tergitol 15-S Series. These substitutes offer comparable hydrophilic–lipophilic balance and cloud point behavior without generating endocrine-disrupting degradation metabolites, aligning more closely with evolving sustainability and compliance expectations.

From a bioprocessing standpoint, Triton X-100 remains relevant in legacy pharmaceutical formulations. Industry data from 2025 indicates that roughly 20% of U.S. pharmaceutical solutions still rely on non-ionic surfactants to achieve formulation stability and solubilization efficiency. However, this reliance is being offset by a measurable redirection of capital. Research and development expenditure on eco-conscious detergent replacements has increased by approximately 15%, reflecting a shift toward biodegradable polysorbates and next-generation surfactants. Regulatory pressure is a key catalyst. The U.S. Food and Drug Administration is increasingly harmonizing review frameworks with International Council for Harmonisation ICH Q5A (R2), which prioritizes excipient safety documentation and environmental profiles. This has resulted in a 25% rise in polysorbate and biodegradable non-ionic surfactant inclusion within new drug filings.

Despite the tightening life sciences landscape, Triton X-100 demand remains structurally supported by non-regulated industrial segments. Public construction spending in the United States reached an annualized rate of $511.6 billion by mid-2025, according to the U.S. Census Bureau. This spending has indirectly sustained consumption of Triton X-100 in heavy-duty industrial coatings, wood adhesives, and construction chemicals, where regulatory sunset timelines are less immediate. As a result, the U.S. market exhibits a bifurcated structure, with accelerated substitution in pharmaceuticals and diagnostics, alongside steady utilization in infrastructure-linked industrial applications.

European Union Triton X-100 Landscape Defined by REACH Enforcement and Green Chemistry Substitution

The European Union Triton X-100 market has largely transitioned from commercial usage to tightly controlled authorized or exempted applications, driven by stringent regulatory enforcement. Following the REACH Annex XIV sunset date, Triton X-100 use is now primarily confined to approved research activities and narrowly defined industrial exemptions. This shift was reinforced in June 2025 with the introduction of Commission Regulation (EU) 2025/1090, which expanded restrictions under Annex XVII and directly impacted imported articles containing phenol-based ethoxylates. For manufacturers and distributors, compliance has moved from a competitive differentiator to a market entry prerequisite.

Germany continues to play a pivotal role in shaping the post-Triton X-100 ecosystem through green chemistry innovation. The country remains a central hub for drop-in replacements that replicate Triton-class performance without regulatory liabilities. In late 2024, Croda Pharma introduced Virodex TXR-1 and TXR-2, fully REACH-compliant alternatives optimized for CHO-K1 and HEK293T cell lysis workflows. These products have gained traction across European bioprocessing facilities seeking regulatory continuity without compromising process efficiency. The Netherlands, meanwhile, functions as a strategic logistics and formulation center, facilitating the redistribution of compliant surfactants across EU and export markets.

On the supply side, asset rationalization is reshaping regional capacity. In July 2025, Dow announced the planned shutdown of three upstream European assets beginning mid-2026. This decision reflects broader efforts to remove energy-intensive operations that conflict with the EU Green Deal’s structural decarbonization targets. Collectively, these dynamics have effectively repositioned Triton X-100 in Europe from a mainstream surfactant to a legacy reference material, while accelerating demand for compliant substitutes across pharmaceutical, diagnostics, and specialty chemical applications.

China Triton X-100 Market Anchored in High-Purity Production and Semiconductor Integration

China’s Triton X-100 market remains structurally resilient, underpinned by high-purity production scaling and diversified end-use adoption. Chemical manufacturing clusters in Nanjing and Suzhou have significantly expanded output of 99%+ purity Triton X-100 to serve domestic in vitro diagnostic requirements. This focus on purity is particularly relevant for diagnostic reagent consistency and membrane permeabilization efficiency. In 2025, WuXi Biologics published internal studies defining minimum effective concentrations for Triton-class membrane-active agents, signaling a dual-track strategy. While legacy Triton X-100 supply is maintained for domestic use, parallel development of globally acceptable substitutes is underway to support export-oriented biopharmaceutical clients.

Beyond life sciences, Triton-type surfactants are gaining renewed relevance in China’s electronics and semiconductor sectors. High-purity non-ionic detergents are being incorporated into the Ministry of Industry and Information Technology’s 2026 blueprint for electronic-grade chemicals. These surfactants are utilized in precision wafer cleaning, photoresist formulation, and contamination control processes, where surface tension modulation and residue minimization are critical. This cross-sector integration provides China with a unique demand profile that partially insulates Triton X-100 consumption from pharmaceutical regulatory headwinds observed in Western markets.

Pricing dynamics further enhance China’s competitive position. As of the third quarter of 2025, technical-grade Triton X-100 pricing in China remains the global floor at approximately $710 per metric ton. This cost advantage supports large-scale industrial textile processing, agrochemical formulation, and downstream supply chains across Southeast Asia. Consequently, China functions both as a consumption hub and a pricing benchmark for Triton X-100 in industrial applications.

India Triton X-100 Market Supported by Diagnostics Growth and Healthcare Infrastructure Expansion

India’s Triton X-100 market is closely aligned with the rapid expansion of diagnostics manufacturing and healthcare infrastructure. In 2025, domestic suppliers, including HiMedia Laboratories, expanded their MB Chemicals portfolios to address rising demand for lateral flow immunoassays. Triton X-100 remains critical in these applications due to its proven effectiveness in membrane permeabilization, antigen release, and flow consistency. The growing domestic production of rapid diagnostic kits has reinforced demand for reliable, performance-validated non-ionic surfactants.

Infrastructure investment has further strengthened market fundamentals. The Indian government’s ₹25,000 crore healthcare infrastructure initiative announced in late 2025 has accelerated procurement of hospital-grade detergents, disinfectants, and antiseptic formulations. Many of these products continue to incorporate octylphenol ethoxylates due to their superior oil-in-water emulsification and cleaning efficiency. Unlike export-oriented pharmaceutical manufacturing, domestic healthcare and sanitation segments face comparatively moderate regulatory pressure, allowing Triton X-100 to retain relevance in formulation portfolios.

Collectively, India represents a demand-driven market where functional performance and cost efficiency currently outweigh regulatory substitution pressures. While global compliance trends are influencing long-term product development strategies, Triton X-100 remains embedded in India’s diagnostics and healthcare supply chains, particularly in applications where reformulation risks and validation costs remain prohibitive.

Summary of Country-Level Triton X-100 Market Characteristics

Triton X-100 Market County Level Snapshot

|

Country / Region

|

Regulatory Environment

|

Primary Demand Drivers

|

Strategic Market Position

|

|

United States

|

Increasing FDA and ICH alignment favoring safer surfactants

|

Legacy pharma formulations and public construction-linked industrial uses

|

Transitional market with dual life sciences substitution and industrial persistence

|

|

European Union

|

Strict REACH Annex XIV and XVII enforcement

|

Green chemistry replacements in bioprocessing

|

Post-sunset market focused on compliant substitutes

|

|

China

|

Balanced domestic regulation with industrial policy support

|

IVD manufacturing and semiconductor chemicals

|

High-purity production hub and global pricing benchmark

|

|

India

|

Moderate regulatory pressure in domestic applications

|

Diagnostics manufacturing and healthcare infrastructure

|

Performance-driven demand with sustained formulation usage

|

Triton X-100 Market Report Scope

Triton X-100 Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$939.6 Million

|

|

Market Size (2034)

|

$1457.6 Million

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Product Grade (Technical Grade, Laboratory Grade, Molecular Biology Grade, Diagnostic Grade), By Application (Bioprocessing and Life Sciences, Industrial and Household Cleaners, Paints and Coatings, Agrochemicals, Oilfield and Mining, Textile and Leather), By Substitution State (Legacy Triton X-100 Usage, Alternative Nonionic Surfactants)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Merck KGaA, Thermo Fisher Scientific Inc., Croda International Plc, BASF SE, Huntsman Corporation, Solis BioDyne, HiMedia Laboratories Private Limited, AppliChem GmbH, Loba Chemie Private Limited, Sino Lion USA Ltd., Promega Corporation, Bio-Rad Laboratories Inc., Nanjing Leopard Chemical Co. Ltd., Takara Bio Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Triton X-100 Market Segmentation

By Product Grade

- Technical Grade

- Laboratory Grade

- Molecular Biology Grade

- Diagnostic Grade

By Application

- Bioprocessing and Life Sciences

- Industrial and Household Cleaners

- Paints and Coatings

- Agrochemicals

- Oilfield and Mining

- Textile and Leather

By Substitution State

- Legacy Triton X-100 Usage

- Alternative Nonionic Surfactants

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Triton X-100 Market

- Dow Inc.

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Croda International Plc

- BASF SE

- Huntsman Corporation

- Solis BioDyne

- HiMedia Laboratories Private Limited

- AppliChem GmbH

- Loba Chemie Private Limited

- Sino Lion USA Ltd.

- Promega Corporation

- Bio-Rad Laboratories Inc.

- Nanjing Leopard Chemical Co. Ltd.

- Takara Bio Inc.

*- List not Exhaustive