Uncoated Woodfree Paper Market Size, Overview, and Growth Outlook (2025–2034)

Global Uncoated Woodfree Paper Market Expected to Double by 2034 as Sustainability and High-Quality Print Demand Drive Growth

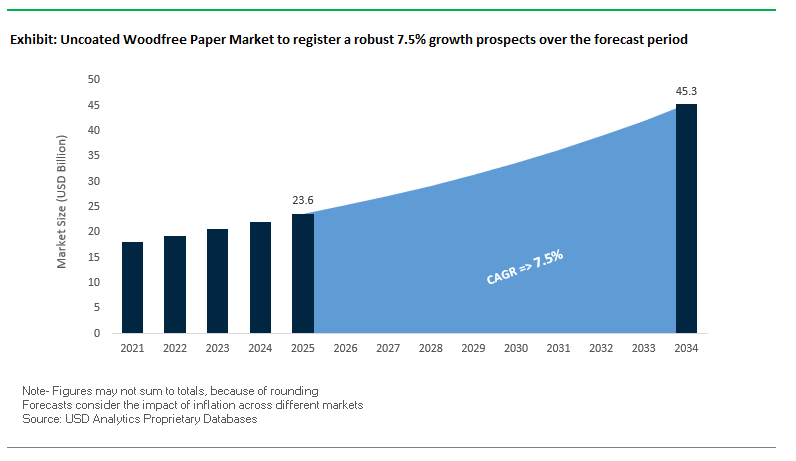

The global uncoated woodfree (UWF) paper market is projected to grow from $23.6 billion in 2025 to $45.2 billion by 2034, at a CAGR of 7.5%. This mature yet innovative market is critical for printing, publishing, and premium packaging applications. Uncoated woodfree paper, made from chemical pulp, offers durability, high brightness, and superior ink absorption, making it a preferred choice for books, magazines, promotional materials, and luxury packaging. Despite the shift toward digital media, the market continues to thrive by catering to specialty printing and retail applications.

Key Insights for industry professionals and buyers:

- Sustainability is a central focus, with manufacturers emphasizing responsibly sourced fibers and recycled content, including 100% EcoFiber pulp.

- High-quality printability ensures sharp text and vibrant images, crucial for premium publishing and marketing materials.

- Specialty packaging adoption enhances brand visibility and customer experience, particularly in luxury products.

- Digital printing compatibility enables UWF paper to meet evolving demands from inkjet and laser press technologies.

- Industry adaptation to eco-friendly and innovative materials positions companies as leaders in responsible production and circular economy initiatives.

Market Analysis: Strategic Transactions and Technological Advancements Shape the Uncoated Woodfree Paper Industry

The UWF paper industry is witnessing significant transformations driven by sustainability, market consolidation, and technological innovation. In August 2025, International Paper announced the sale of its Global Cellulose Fibers business for $1.5 billion, signaling a strategic focus on sustainable packaging solutions. The same month, Sappi Europe implemented price increases of $60–100/t for all Woodfree Coated grades for deliveries starting October 2025, highlighting market realignment and cost adjustments.

In July 2025, research highlighted a composite antimicrobial film made from carrageenan and polyoxometalate, showing bactericidal activity and biodegradability, reflecting innovation in eco-friendly and functional paper applications. The October 2024 merger of Smurfit Kappa and WestRock created a global packaging leader, expanding capabilities relevant to the UWF paper market. Similarly, September 2024 saw the acquisition of Eutecma, a modular sustainable packaging solutions firm, underscoring a focus on reusable and eco-friendly packaging technologies.

Earlier developments include March 2024, when TOPPAN Holdings launched GL-SP, a transparent BOPP barrier film, enhancing the recyclability of paper-based packaging solutions, and September 2023, when JBT Proseal introduced the CP4 case packing machine, supporting efficient packaging operations. These strategic moves highlight the market’s dynamism, combining sustainable production, high-performance materials, and industry consolidation to meet evolving professional and consumer needs.

Trends and Opportunities in the Uncoated Woodfree Paper Market

Corporate Pivot to Digital-Last Communication Driving Declining Demand

The uncoated woodfree paper market is being reshaped by the rapid adoption of digital-first communication strategies across industries. Over 90% of organizations globally are actively implementing digital transformation initiatives, with 87% of senior executives classifying it as a top priority. This structural shift directly impacts the demand for uncoated office paper, as workflows such as invoices, purchase orders, and reporting systems are increasingly digitized.

Case studies highlight this transformation in practice. An HVAC distributor, Faulkner Hayes, eliminated paper-based processes by adopting an automated enterprise software platform, reducing manual order entries and paper invoices. This demonstrates how efficiency gains from automation accelerate the decline of traditional paper use in business environments.

The ripple effect is visible at scale. In its 2023 sustainability report, Amazon revealed that it had eliminated 1,180 metric tons of packaging from Amazon Fresh and 1,300 metric tons from Whole Foods Market through digital-first and optimized packaging solutions. Such high-profile initiatives reinforce the decline in demand for uncoated woodfree paper, particularly in traditional office, publishing, and retail applications.

Rising Demand for Specific, High-Performance Recycled Content Grades

Despite the overall decline in consumption, demand for recycled-content uncoated paper grades is on the rise, driven by corporate ESG mandates and sustainability-driven procurement policies. Organizations aligned with the Environmental Paper Network (EPN) are actively prioritizing paper with high post-consumer recycled content, reducing their reliance on virgin fiber.

To meet this demand, manufacturers are innovating with dual-layer fiber designs. These structures feature a virgin fiber outer layer that delivers superior print quality while integrating a high proportion of recycled fiber in the base layer for environmental performance. This hybrid model balances sustainability with functionality, ensuring recycled papers meet the stringent requirements of commercial printing, publishing, and packaging.

This trend underscores a strategic pivot: while general-purpose communication paper consumption declines, specialized recycled uncoated woodfree grades are gaining market traction, particularly in sectors with strong sustainability commitments.

Serving the Growing Market for Sustainable Packaging and Cartons

The growth of e-commerce and sustainable packaging mandates presents a major opportunity for uncoated woodfree paper to expand beyond traditional applications. Increasingly, it is being repurposed for cartons, rigid boxes, and recyclable mailers, providing an alternative to mixed-material and plastic-based formats.

A notable example is Amazon’s replacement of 99.7% of its mixed-material padded mailers with recyclable paper mailers in 2024, which reflects the scalability of paper-based solutions in global logistics. Similarly, brands in food and beverages are turning to uncoated paper-based cups and rigid packaging. Nissin Foods USA’s Cup Noodles, for instance, introduced a paper-based cup made with 40% recycled fiber, highlighting uncoated paper’s premium, natural aesthetic in consumer packaging.

This repositioning toward luxury and premium packaging is particularly compelling. Uncoated woodfree paper conveys a sense of authenticity and sustainability, making it ideal for high-end retail boxes, specialty food packaging, and branded gift items where both performance and image matter.

Development of Functional and Specialty Uncoated Papers

A second major opportunity lies in functional and specialty paper innovation, where uncoated grades are being engineered for high-value applications beyond traditional printing. Security features such as micro-text, watermarks, and embedded fibers are transforming uncoated woodfree paper into a robust medium for legal, financial, and government documentation where forgery protection is paramount.

The integration of IoT technologies into paper packaging further expands its utility. Papers embedded with RFID tags or printed electronics enable smart packaging applications that track products, verify authenticity, or provide interactive consumer engagement. In May 2025, Amazon’s rollout of automated packaging machines across Europe—capable of producing custom cardboard boxes and paper bags demonstrates the future role of technology-enabled paper packaging in supply chain optimization.

By combining sustainability with advanced functionality, uncoated woodfree paper producers can transition from declining commodity applications into growth markets such as premium packaging, security printing, and smart logistics solutions.

Competitive Landscape: Leading Companies Drive Innovation and Sustainability in the Global Uncoated Woodfree Paper Market

The uncoated woodfree paper market is dominated by global players leveraging materials expertise, sustainable practices, and operational excellence to offer high-quality, durable paper solutions across printing, publishing, and packaging sectors.

International Paper Company: Focusing on Sustainable Packaging Solutions and Market Leadership

International Paper provides a wide portfolio of paper and paperboard products, tailored to UWF applications. In August 2025, the company sold its Global Cellulose Fibers business to concentrate on sustainable packaging solutions, following its 2025 acquisition of DS Smith. Its vertically integrated model ensures consistent quality and global distribution, while its strategic focus emphasizes innovation, sustainability, and compliance across markets.

Domtar Corporation: Driving Circular Economy Initiatives in Paper Manufacturing

Domtar specializes in UWF paper products for printing and publishing. The company’s Better Planet 2050 strategy emphasizes reducing environmental footprint and investing in sustainable materials. Domtar leverages global expertise in pulp and paper production to serve diverse regions and industries while prioritizing eco-friendly innovations and high-quality output.

Sappi Limited: Maintaining Competitive Edge through Strategic Pricing and Sustainable Production

Sappi offers a broad range of high-quality UWF paper products, catering to stringent publishing standards. In August 2025, Sappi Europe increased prices for all WFC paper grades, effective October 2025. Its Sappi Way strategy focuses on sustainability, circular economy adoption, and advanced material development, reinforcing its global leadership in paper and pulp.

UPM-Kymmene Corporation: Integrating Bio-Based Innovation into Paper Production

UPM delivers UWF paper and other bio-industry products with a strong sustainability focus. Its UPM Way strategy prioritizes eco-conscious production, material innovation, and global distribution, positioning the company as a leader in both the forest industry and premium paper applications.

Oji Holdings Corporation: Advancing Eco-Friendly Paper Solutions with Global Expertise

Oji Holdings provides high-quality UWF paper, emphasizing sustainability and circular economy initiatives through its Oji Way strategy. The company continues to invest in innovative materials, maintaining a strong global presence and vertically integrated operations to serve diverse industrial and publishing clients.

Siam Cement Group (SCG): Strengthening Market Position with Sustainable Paper Products

SCG offers a comprehensive range of UWF paper and packaging solutions, guided by the SCG Way strategy. The company invests in sustainable materials and innovative technologies, ensuring eco-friendly, high-performance paper products that meet the evolving needs of printing, publishing, and specialty packaging markets.

Uncoated Woodfree Paper Market Share Insights, 2025-2034

Reels Command Market Share by Product Type in the Uncoated Woodfree Paper Industry

Reels represent the largest share of the uncoated woodfree (UWF) paper market at about 45%, highlighting their critical role in large-scale commercial printing. Supplied in massive rolls, reels are indispensable for high-volume web offset and digital presses, which produce books, brochures, magazines, direct mail, and office documents at industrial scale. Their efficiency, cost-effectiveness, and ability to run continuously on high-speed machines make them the preferred input for commercial print houses that demand consistency and throughput. Additionally, reels offer significant economies of scale in logistics and handling, reducing waste and production downtime compared to smaller sheet formats. As global demand for high-quality printed marketing collateral and corporate communications continues, reels remain the backbone of professional printing, particularly in markets where physical media still complements digital channels.

Commercial Printing Holds Largest Market Share by End-Use in the Uncoated Woodfree Paper Industry

The commercial sector dominates the uncoated woodfree paper market with a commanding 65% share, reflecting the sustained reliance of businesses on physical documentation and professional print media. Despite digital transformation, commercial enterprises continue to generate high demand for marketing materials, annual reports, legal documents, and office communications that require durability, brightness, and print quality offered by UWF paper. The sector also benefits from the global print services industry, which relies heavily on reels and sheets of UWF paper for bulk printing projects. Regulatory requirements for maintaining physical records, coupled with the need for premium-quality paper in corporate identity materials, further anchor this segment’s dominance. While digitization has reduced paper volumes in certain administrative functions, the commercial sector’s demand for reliable, professional-grade paper ensures its continued leadership in driving market revenues for uncoated woodfree paper.

European Union: EUDR and PPWR Driving Sustainable Paper Production

The European Union uncoated woodfree paper market is undergoing regulatory-driven transformation, with the EU Deforestation Regulation (EUDR) taking full effect by end of 2025. This landmark regulation requires companies to prove that their raw materials are deforestation-free, making supply chain traceability and due diligence critical for the paper sector. Alongside this, the Packaging and Packaging Waste Regulation (PPWR), effective February 2025, is pushing the industry toward circular economy practices, increasing the use of recycled fibers and alternative bio-based inputs in uncoated woodfree paper production.

The European Commission’s Horizon Europe program is further accelerating R&D into bio-based and compostable alternatives, reducing reliance on virgin wood pulp. Companies such as Mondi are setting benchmarks by ensuring certifications like FSC™ and EU Ecolabel, signaling compliance with stringent environmental standards. While graphic paper demand continues to decline, with some mills closing, manufacturers are strategically shifting production toward specialty and packaging grades, aligning with EU sustainability priorities and consumer demand for eco-friendly products.

United States: Premium Quality and Digital Printing Adoption

The United States uncoated woodfree paper market is shaped by strong sustainability initiatives and innovation. The EPA’s recycling goals are prompting investments in infrastructure that support recycled fiber integration and more sustainable production processes. A key market trend is the development of high-quality uncoated woodfree paper with superior printability, tactile feel, and brightness, targeting luxury packaging, branded collateral, and high-end publishing.

With the rise of digital printing technologies, demand for advanced uncoated substrates compatible with inkjet and laser systems is growing. These papers must deliver exceptional ink absorption and print fidelity, making them critical for modern publishing and on-demand printing. Companies are also focusing on certified sustainable forestry practices and innovations in energy-efficient machinery and water management systems to lower their environmental footprint. This dual emphasis on performance and sustainability positions the U.S. as a strong market for premium-grade uncoated woodfree paper.

China: Import Reliance and Demand for High-End Packaging

In China, the uncoated woodfree paper market is evolving under the government’s “14th Five-Year” plan, which emphasizes green technology adoption and remanufacturing incentives. While domestic regulations, such as logging bans and harvesting restrictions, have been introduced to preserve forest resources, they have simultaneously increased dependence on imported wood pulp. This reliance highlights China’s vulnerability in raw material supply but also underscores opportunities for international pulp exporters.

A key market driver is the increasing demand for high-end packaging solutions, particularly for luxury goods and pharmaceuticals. With consumer preferences shifting toward premium and secure packaging with enhanced barrier properties, uncoated woodfree paper is being engineered to meet both aesthetic and functional needs. The State Tobacco Monopoly Administration (STMA) is also influencing the paper sector through stricter supply chain control, encouraging the integration of advanced anti-counterfeiting features in packaging.

Brazil: Global Leader in BEKP and Sustainable Pulp Expansion

Brazil is a cornerstone of the global uncoated woodfree paper supply chain, with its dominance in bleached eucalyptus kraft pulp (BEKP) production. Companies such as Suzano S.A. are expanding aggressively, with the inauguration of a 2.55 million metric ton pulp mill in December 2024, cementing Brazil’s role as a leading exporter. Extensive planted eucalyptus forests provide low-cost, high-yield raw materials, giving Brazil a major competitive advantage in the global pulp market.

The sector is undergoing significant modernization, with investments in timber plantation expansion and advanced pulp mills aimed at improving efficiency while reducing environmental impacts. Supported by the National Solid Waste Policy (PNRS), Brazil’s pulp and paper industry is embracing sustainability by enhancing recycling initiatives and integrating renewable energy in operations. This synergy between resource abundance, policy support, and investment scale makes Brazil a pivotal supplier of uncoated woodfree paper inputs worldwide.

Japan: Recycling Leadership and Low-Carbon Paper Solutions

The Japan uncoated woodfree paper market is heavily shaped by sustainability mandates. The Plastic Resource Circulation Strategy (2025) and the Plastic Resource Circulation Promotion Law (2025) are accelerating the substitution of plastics with paper-based alternatives, boosting demand for woodfree grades in packaging and specialty applications.

Japan also maintains one of the highest paper recovery rates globally, with the Japan Paper Association setting a target of achieving net-zero CO2 emissions by 2050. The country is investing in biomass energy and closed-loop resource systems, ensuring that recovered paper is efficiently reused in high-quality applications. The MHLW’s positive list system (June 2025) for food-contact safety is particularly important, as it ensures that uncoated woodfree papers used in packaging meet stringent health standards. Japan’s model of combining recycling efficiency with carbon-neutral targets is positioning it as a global leader in low-carbon uncoated woodfree paper solutions.

Indonesia: Expansion of Timber Plantations and Pulp Industry Modernization

Indonesia is positioning itself as a growing player in the global uncoated woodfree paper market, supported by government-backed reforms. The “Industrial Timber Plantation and Pulp Industry Development” plan is expanding timber plantations and pulp production capacity, ensuring a stronger and more reliable supply chain for paper manufacturers.

The country is also modernizing its pulp and paper sector with significant investments aimed at reducing environmental impacts, such as water pollution and carbon emissions. These efforts are enhancing Indonesia’s role as a competitive supplier of pulp and raw materials for uncoated woodfree paper production. With strategic alignment between government policy, corporate investment, and global demand growth, Indonesia is emerging as a key sourcing hub in the Asia-Pacific uncoated paper industry.

Uncoated Woodfree Paper Market Report Scope

Uncoated Woodfree Paper Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$23.6 Billion

|

|

Market Size (2034)

|

$45.2 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Product Type (Reels, Sheets, Offset Paper, Bond Paper), By Application (Printing, Publishing, Stationery, Packaging, Other Applications), By End-Use Industry (Commercial, Educational, Personal, Industrial), By Distribution Channel (Direct Sales, Distributors, Online Retail, Other Channels)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, Stora Enso Oyj, UPM-Kymmene Corporation, Nippon Paper Industries Co., Ltd., Sappi Limited, Nine Dragons Paper (Holdings) Limited, Mondi Group, Smurfit Kappa Group, Domtar Corporation, Resolute Forest Products Inc., WestRock Company (now Smurfit Westrock), Suzano S.A., Oji Holdings Corporation, Daio Paper Corporation, JK Paper Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Uncoated Woodfree Paper Market Segmentation

By Product Type

- Reels

- Sheets

- Offset Paper

- Bond Paper

By Application

- Printing

- Publishing

- Stationery

- Packaging

- Other Applications

By End-Use Industry

- Commercial

- Educational

- Personal

- Industrial

By Distribution Channel

- Direct Sales

- Distributors

- Online Retail

- Other Channels

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Uncoated Woodfree Paper Market

- International Paper Company

- Stora Enso Oyj

- UPM-Kymmene Corporation

- Nippon Paper Industries Co., Ltd.

- Sappi Limited

- Nine Dragons Paper (Holdings) Limited

- Mondi Group

- Smurfit Kappa Group

- Domtar Corporation

- Resolute Forest Products Inc.

- WestRock Company (now Smurfit Westrock)

- Suzano S.A.

- Oji Holdings Corporation

- Daio Paper Corporation

- JK Paper Limited

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-dimensional research methodology to analyze the global uncoated woodfree (UWF) paper market, combining primary interviews with key stakeholders such as manufacturers, pulp suppliers, publishers, and packaging companies, alongside secondary research from company reports, academic publications, and regulatory documents. Our approach assesses market drivers, including sustainability initiatives, recycled-content adoption, digital printing compatibility, premium packaging demand, and technological innovations like functional and smart papers. USDAnalytics integrates market sizing, CAGR projections, and segmentation across product types, applications, end-use industries, and distribution channels, while evaluating regional trends across North America, Europe, Asia-Pacific, China, India, Japan, Brazil, and Indonesia. We also incorporate regulatory frameworks, corporate ESG strategies, and competitive benchmarking, providing actionable insights for industry professionals seeking to navigate shifts from traditional printing to specialty, sustainable, and high-performance UWF paper applications.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.