Market Overview of Vanillic Acid Market – Purity Standards, Natural Bioconversion, and Functional Performance Driving Steady Demand

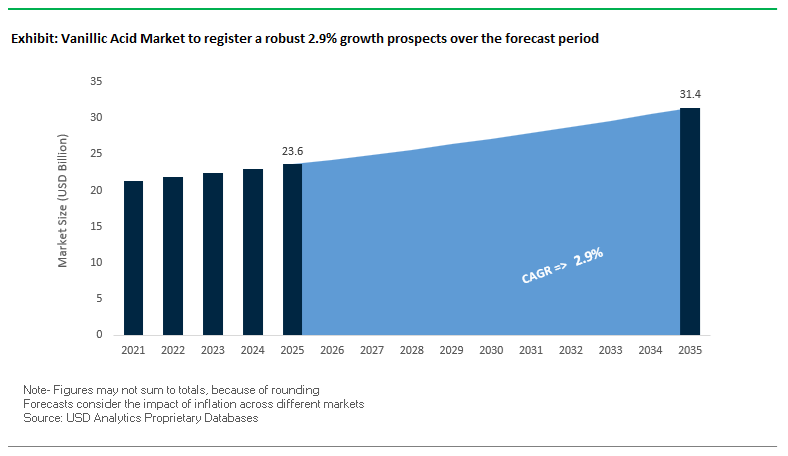

The Vanillic Acid Market, valued at USD 23.6 billion in 2025, is projected to reach USD 31.4 billion by 2035 at a moderate CAGR of 2.9%, driven by rising applications across the food & beverage, pharmaceutical intermediates, cosmetics, nutraceuticals, and agrochemical sectors. For manufacturers and vendors, the competitive landscape increasingly revolves around purity assurance (97–99%), bio-based sourcing, and high-performance functional benefits such as antioxidant efficacy and flavor intensity. As global demand shifts toward clean-label ingredients, sustainable synthesis pathways, and controlled fermentation, Vanillic Acid is becoming a cornerstone intermediate across multiple regulated industries.

A significant proportion of production is transitioning toward bioconversion of Ferulic Acid—a natural phenolic compound derived from rice bran, corn hulls, wheat bran, and agricultural residues. This transition positions Vanillic Acid as a strategic molecule in the bioeconomy, reducing dependence on petrochemical routes while enabling natural flavor development, sustainable intermediates for vanillin, and high-purity derivatives for cosmetics and pharmaceuticals. Its antioxidant properties further strengthen adoption in dermal formulations, nutraceutical blends, anti-aging solutions, and oxidative-stress-targeted products.

Advanced biocatalytic routes capable of delivering ~60% molar yields allow scalable production under mild conditions, enabling cost reduction and reducing environmental impact. These improvements, combined with the compound’s well-defined vanilla-like flavor profile, continue to enhance its value across consumer goods and specialty chemical markets.

Key Takeaways for Manufacturers and Formulators

- Purity standard (97–99% Vanillic Acid) ensures compliance for pharmaceutical and food-grade applications.

- Ferulic Acid bioconversion is emerging as the leading sustainable production route.

- Strong antioxidant activity expands use in skincare, nutraceuticals, and anti-aging formulations.

- Flavor-enhancement capability supports cost-effective vanilla profile expansion.

- Biocatalytic yields of ~60% signal strong scalability for natural and bio-based production ecosystems.

Market Analysis of Vanillic Acid Market – Biotech Expansion, Sustainable Precursors, and High-Purity Demand Reshaping Global Supply Chains

The global Vanillic Acid industry is experiencing progressive shifts driven by biotechnology investments, high-purity product innovation, and strengthened regulatory validation. In August 2025, a major European specialty chemicals group announced a USD 50 million R&D investment aimed at expanding biotechnological production capacity using lignin derivatives—a milestone that directly supports the long-term transition from petrochemical feedstocks to sustainable bio-based sources. This move underscores the industry's alignment with renewable phenolic platforms, strengthening raw material security for vanillin, Vanillic Acid, and aromatic intermediates.

Product diversification is accelerating as leading manufacturers introduce advanced formulations tailored to high-value applications. In May 2024, Solvay launched a high-purity natural Vanillic Acid grade engineered specifically for dermal patches and transdermal drug delivery systems, leveraging the compound’s intrinsic anti-inflammatory and antioxidant properties. This development reflects the growing integration of Vanillic Acid into pharmaceutical delivery technologies and functional cosmetics, where purity, assay consistency, and safety certifications are non-negotiable.

Strategic consolidations are reshaping the supply landscape. In October 2025, a Chinese fine chemical producer finalized its acquisition of a Ferulic Acid extraction facility in India, effectively securing a vertically integrated supply chain for natural Vanillic Acid and Bio-vanillin production. Concurrently, TCI’s expansion in February 2025 strengthened availability of high-purity Vanillic Acid for laboratory, analytical, and pharmaceutical research markets, addressing rising global demand for certified reference materials.

Research breakthroughs have been equally influential: in November 2024, academic scientists achieved ≈90% entrapment efficiency using Nanostructured Lipid Carriers (NLCs), significantly improving Vanillic Acid’s skin retention—positioning it as a next-generation active ingredient in premium anti-aging cosmetics.

Regulatory updates and government initiatives continue to reinforce market growth. The EFSA’s June 2024 reaffirmation of Vanillic Acid as a safe food additive strengthened its stability in European food manufacturing. Additionally, a March 2025 partnership between Brazilian and U.S. companies is exploring the use of Vanillic Acid derivatives as precursors for bio-based fungicides, expanding its relevance into the agrochemical domain. Meanwhile, USD 30 million in April 2024 was allocated to improve vanilla bean cultivation yields in Madagascar, indirectly influencing the economics of naturally derived Vanillic Acid across global markets.

Biobased Lignin Conversion, High-Temperature Polymer Precursors, Functional Antioxidant Derivatives, and Liquid Crystal Monomers Fuel Market Growth

Market Trend 1: Lignin-Derived Vanillic Acid Emerging as a High-Purity, Industrial-Scale Biobased Platform Chemical

A defining trend in the vanillic acid market is the rapid acceleration of lignin valorization technologies, which are reshaping the availability and quality of biobased aromatics. As global chemical manufacturing shifts toward renewable carbon, vanillic acid is increasingly produced through base-catalyzed depolymerization (BCD) of lignin—an abundant, underutilized pulp-and-paper byproduct. BCD processes have demonstrated conversion yields of 45–78% into low-molecular-weight intermediates, establishing lignin as a viable feedstock. The intermediate step—oxidative depolymerization—has already achieved vanillin yields of up to 10.9 wt%, setting a performance benchmark that directly influences vanillic acid production scalability.

Purification technologies are equally pivotal. Centrifugal Partition Chromatography (CPC) has emerged as the leading separation platform, capable of achieving up to 96% purity for isolated vanillic acid. This level of separation ensures compliance with quality standards for use in fine chemicals, food additives, pharmaceuticals, and advanced polymer synthesis. Collectively, advancements in lignin depolymerization efficiency, precursor yield maximization, and high-resolution separation systems are positioning vanillic acid as one of the most commercially attractive aromatic building blocks derived from biomass.

Market Trend 2: Vanillic Acid as a Precursor for High-Performance Bio-Based Polymers, Epoxies, and Flame-Resistant Resins

A second major trend reshaping demand is vanillic acid’s growing role as a platform molecule for bio-based, engineering-grade polymers. As industries seek petroleum-free alternatives with equivalent or superior thermal performance, derivatives of vanillin and vanillic acid are enabling high-performance epoxy systems with Glass Transition Temperatures (Tg) of 141–145°C, exceeding traditional DGEBA epoxies. The statistic heat resistance index (Ts) of ~193°C demonstrates robustness in thermomechanical environments, supporting applications in electronics, aerospace composites, and high-temperature adhesives.

Flame retardancy further differentiates these biobased materials. Vanillin-derived epoxies show substantially higher char yields at 500°C compared to DGEBA, reducing flammability and toxic smoke formation—two critical parameters in advanced materials engineering. Reinforcement with Lignin-Containing Cellulose Nanofibrils (LCNFs) has yielded 81% increases in tensile strength and 185% gains in toughness, proving that vanillic-acid-based polymers can deliver mechanical performance competitive with next-generation nanocomposites. This trend strengthens vanillic acid’s position as an indispensable intermediate for the rapidly expanding bio-based polymer economy.

Market Opportunity 1: Expansion into Antioxidant and Antimicrobial Systems for Food, Nutraceutical, and Pharmaceutical Applications

A significant commercial opportunity lies in vanillic acid’s biochemical versatility as a synergistic antioxidant and antimicrobial agent. Although pure vanillic acid exhibits a relatively high IC50 value (11,608.65 μM) in the DPPH assay, structural modifications—particularly Mannich base derivatives—deliver IC50 values as low as 26.55 μM, comparable to natural antioxidants used in functional foods and nutraceuticals. This performance enhancement directly broadens application potential in lipid-rich food matrices and oxidative stress–sensitive formulations.

Even more compelling is the behavior of vanillic acid esters, whose increased lipophilicity leads to superior antioxidant activity in ORAC and OxHLIA assays, outperforming Trolox in protecting biomembranes against oxidative damage. This positions vanillic acid derivatives as frontier compounds for plasma protection, anti-aging formulations, and functional foods. Biocompatibility studies confirm safe use across 1–50 μg/mL concentrations in human PBMCs and neutrophils, reinforcing the molecule’s suitability for pharmaceuticals, injectable formulations, and therapeutic antioxidant delivery. These properties align squarely with the trend toward clean-label, bio-derived functional additives.

Market Opportunity 2: Use of Vanillic Acid in High-Temperature, Anisotropic Liquid Crystal Monomers for Advanced Display Technologies

A second high-value opportunity is vanillic acid’s emerging role in liquid crystal (LC) monomer synthesis, supporting next-generation display technologies. LC copolyesters derived from vanillic acid exhibit extraordinarily broad nematic phase windows (183–390°C), enabling stable mesophase performance across a wide operational temperature range. Their thermal degradation onset at 436°C confirms suitability for high-temperature processing used in advanced LCD, OLED, and microdisplay manufacturing.

The chemical structure of vanillic acid—particularly its methoxy (electron-donating) and hydroxyl (hydrogen-bonding) substituents—creates intrinsic molecular anisotropy, a prerequisite for stable mesogenic alignment. These characteristics allow precision tuning of clearing points, viscosity, and molecular order, all essential for advanced optical modulators, flexible displays, and high-resolution imaging systems.

As demand intensifies for bio-based LC materials compatible with sustainability mandates and high-performance electronics, vanillic acid offers a unique, scalable aromatic precursor capable of bridging renewable chemistry and display-grade functionality.

Vanillic Acid Market Share Analysis

Market Share by Source: Synthetic Vanillic Acid Dominates Owing to Cost Efficiency and Industrial-Scale Production

Synthetic Vanillic Acid accounts for approximately 85% of the global market because it is the only economically viable and scalable production route capable of meeting the accelerating industrial demand from high-volume sectors such as flavors, fragrances, pharmaceuticals, and chemical intermediates. Synthetic production—typically achieved through controlled oxidation of vanillin or lignin-derived feedstocks—provides manufacturers with high-yield, high-purity output, ensuring consistent chemical quality that is essential for downstream applications with stringent regulatory requirements. The cost of sourcing vanillic acid from natural botanical sources is significantly higher due to limited raw material availability, labor-intensive extraction, and fluctuating crop yields, making natural vanillic acid a niche premium product rather than a mainstream commercial input. In contrast, synthetic processes align with global manufacturing needs for large-scale, reproducible, and price-stable supply, which is critical for companies producing tens of thousands of tons of aroma chemicals per year. Given this combination of affordability, production reliability, and suitability for high-purity end-use categories, synthetic vanillic acid retains a clear leadership position and is expected to remain the dominant material source for the foreseeable future.

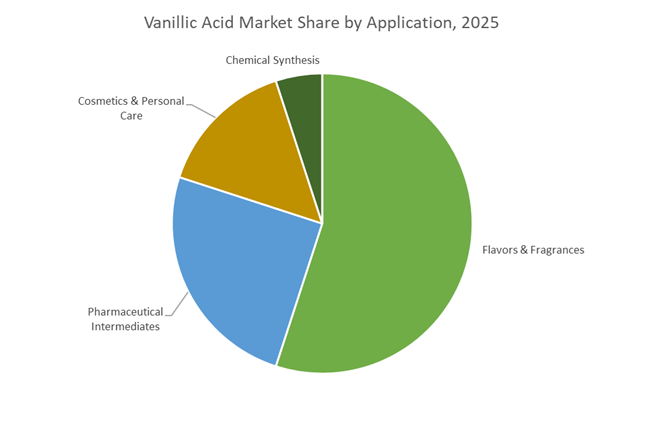

Market Share by Application: Flavors & Fragrances Lead Due to High-Volume Use in Aroma Chemicals and Vanilla-Based Formulations

The Flavors & Fragrances segment holds the largest market share—around 55%—because vanillic acid plays an essential functional role as both a direct aromatic ingredient and a precursor molecule in the synthesis of key flavor compounds, particularly vanillin. Given that vanillin is one of the most widely used flavoring agents worldwide—present in packaged foods, beverages, confectionery, bakery products, fragrances, and personal care formulations—the demand for vanillic acid is strongly tied to the global growth in food processing, consumer packaged goods, and perfumery manufacturing. Vanillic acid contributes to stability and depth of aroma profiles, enhancing sweet, creamy, and warm notes that dominate premium fragrance blends and mass-market food applications. Its role as a chemical intermediate also makes it indispensable in producing derivative aromatic aldehydes and esters used across the fragrance and flavor industries. With the increasing shift toward natural-identical and sustainable aroma chemicals, as well as surging demand from emerging markets for processed foods and cosmetics, the flavors and fragrances industry continues to represent the highest-volume consumer. This entrenched integration into global flavor chemistry, combined with constant demand across multiple high-growth FMCG categories, firmly secures its leading market position in vanillic acid consumption.

Country Analysis: Global Vanillic Acid Market Hotspots and Bio-Based Production Strategies

China: Synthetic Vanillic Acid Leadership and Ferulic Acid Bioconversion Advancements

China remains the world’s largest producer of synthetic vanillic acid, supported by expansive chemical manufacturing infrastructure and a robust supply chain for vanillin oxidation, ensuring cost-efficient large-scale production. Vanillic acid is widely consumed by China’s food and beverage sector as a flavor enhancer and antimicrobial preservative, enabling manufacturers to extend shelf life while maintaining clean sensory profiles across packaged products. This demand is reinforced by China’s dominant role in supplying vanillic acid intermediates to downstream fragrance, pharmaceutical, and industrial chemical markets.

Parallel to synthetic capacity, China is rapidly expanding its biotechnology footprint in vanillic acid production. Research funded by the Natural Science Foundation of China (NSFC) has delivered significant progress in whole-cell catalytic systems using engineered E. coli, enabling efficient transformation of ferulic acid into vanillin, which serves as a key precursor to vanillic acid. These advancements reflect a strategic push toward environmentally friendly, bio-based production pathways that can reduce process emissions, improve feedstock flexibility, and leverage agricultural waste streams. As China scales this bioconversion pathway, its competitive advantage in supplying high-volume, cost-effective vanillic acid is expected to strengthen even further.

United States: Natural Flavor Demand and Expanding Pharmaceutical/Nutraceutical Applications

The United States is emerging as a global hub for natural and clean-label vanillic acid demand, driven by a strong consumer shift toward minimally processed ingredients in food, beverages, and functional nutrition products. The ingredient’s classification by the U.S. FDA as GRAS ensures seamless regulatory acceptance, enabling formulators to incorporate vanillic acid into flavorings, plant-based beverages, dietary supplements, and health-forward packaged foods without additional regulatory burden. This regulatory clarity positions vanillic acid as a preferred natural flavor substitute amid rising scrutiny of artificial additives.

In advanced applications, U.S. pharmaceutical and biomedical researchers—supported by NIH-backed programs (2025)—are exploring vanillic acid’s therapeutic potential. Cutting-edge studies demonstrate its compatibility with nanoparticle carriers, hydrogels, and controlled-release formulations, significantly enhancing its bioavailability. This is especially relevant for its anti-inflammatory, neuroprotective, and wound-healing properties, which are being tested across dermatology, neurology, and regenerative medicine. As U.S. pharma and nutraceutical innovators intensify their use of polyphenolic compounds, vanillic acid is transitioning from a traditional flavoring agent to a strategic active ingredient in next-generation therapeutic and functional formulations.

Japan: Breakthrough Enzymatic Biosynthesis and Precision Chemical Manufacturing

Japan continues to lead global innovation in sustainable and enzymatic vanillic acid production pathways, supported by its longstanding expertise in biocatalysis and high-purity specialty chemicals. A groundbreaking development by the Tokyo University of Science (May 2024) introduced a modified Ado oxidase enzyme enabling one-step conversion of agricultural-waste-derived ferulic acid into vanillin at room temperature. This innovation significantly reduces energy consumption, eliminates hazardous reagents, and positions Japan at the forefront of scalable, green vanillic acid production technologies.

Commercial momentum is reinforced by manufacturers such as Tokyo Chemical Industry (TCI), which announced expanded production capacities in 2024 to meet global demand for high-purity vanillic acid used in pharmaceuticals, analytical chemistry, and premium food formulations. Japanese producers maintain strict quality benchmarks across purity, stability, and traceability—attributes critical for medical, nutraceutical, and biotech sectors. These advances highlight Japan's strategic direction toward sustainable, technology-led growth in the vanillic acid market, with biosynthesis becoming a cornerstone of future supply.

India: Rising Flavors & Fragrances Manufacturing and Increasing Nutraceutical Use

India’s expanding Flavors & Fragrances (F&F), cosmetics, and pharmaceutical sectors are rapidly accelerating domestic demand for vanillic acid. Driven by rising disposable incomes, urbanization, and higher consumption of premium beauty and personal care products, Indian manufacturers are increasingly investing in high-purity vanillic acid for use as an aromatic agent, antioxidant, and preservative. Domestic chemical and API manufacturers are also scaling production to reduce import dependency, strengthening India’s position as a competitive supplier within the Asia-Pacific value chain.

Parallel growth in functional foods and nutraceuticals is amplifying the market opportunity. As Indian consumers shift toward wellness products with botanical or plant-derived actives, vanillic acid is gaining traction due to its anti-inflammatory, digestive health, and antioxidant benefits. This demand is reinforced by the expansion of India’s natural ingredients industry, supported by government incentives to enhance manufacturing self-reliance. Coupled with rising exports of processed foods and personal care products, India is evolving into a significant regional hotspot for both production and consumption of vanillic acid.

European Union: Clean-Label Regulations Driving Bio-Based Vanillic Acid Preference

The European Union remains one of the most stringent regulatory environments for food additives and aroma chemicals, creating strong momentum for bio-based and naturally sourced vanillic acid. EU clean-label standards, reinforced by consumer preference for transparency and sustainability, are pushing manufacturers to transition away from synthetic variants toward ferulic-acid-derived or enzymatically synthesized alternatives. This shift supports broader EU sustainability objectives, including circular economy policies and environmentally safe production practices.

European flavor houses, nutraceutical producers, and clean-beauty brands increasingly specify vanillic acid as a multifunctional ingredient that meets regulatory, environmental, and performance expectations. As the EU amplifies its restrictions on chemical residues, carbon emissions, and fossil-derived intermediates, the market for natural vanillic acid—particularly that produced via biotechnological pathways—is expected to accelerate rapidly. This regulatory-driven adoption makes the EU a powerful demand center for high-purity, traceable, and sustainable vanillic acid solutions.

South Korea: Cosmetics Export Expansion Driving High-Purity Vanillic Acid Demand

South Korea’s fast-growing cosmetics and personal care export industry is a major driver of vanillic acid demand, particularly in formulations emphasizing antioxidant, anti-aging, and skin-rejuvenating properties. As K-beauty brands continue to expand globally, vanillic acid is gaining relevance as a multifunctional active supporting product differentiation in premium skincare, serums, essences, and functional cosmetics. Its natural origin aligns with clean-beauty trends dominating Korean and global markets.

In parallel, South Korea’s domestic innovation ecosystem—comprising chemical manufacturers, biotech startups, and university research labs—is exploring expanded use of vanillic acid in dermal delivery systems, microencapsulation, and antioxidant stabilization. With South Korea reinforcing its leadership in high-performance and lightweight personal care formulations, vanillic acid is well-positioned to see growing adoption across the country’s cosmetics, pharmaceuticals, and wellness product categories.

Competitive Landscape of Vanillic Acid Market – Biorefineries, High-Purity Specialists, and Vertically Integrated Aroma Chemical Leaders

The competitive landscape of the Vanillic Acid industry is shaped by companies with deep expertise in aroma chemistry, bio-refining, high-purity intermediates, analytical reference materials, and vertically integrated synthesis routes. Strategic strengths increasingly lie in sustainable phenolic production, high-purity chemical synthesis, and the ability to support regulated markets such as pharmaceuticals, food additives, and cosmetics. Companies that can guarantee consistent assay values, traceability, and global regulatory compliance hold a decisive advantage.

Solvay S.A. Strengthens Global Leadership in Bio-Based Aroma Chemicals

Solvay maintains its leadership through extensive integration in aroma performance chemistry, leveraging its Rhovanil® Natural CW portfolio and advanced phenolic intermediates. The company plays a central role in global vanillin and Vanillic Acid supply chains due to its vertically integrated operations across guaiacol/catechol chemistry and biotechnological fermentation pathways. Solvay’s strategic investments in bio-based ingredient development, including its joint ventures such as Cipan, reflect its commitment to meeting surging demand for natural, clean-label, and sustainable aroma chemicals. The company’s ability to serve both high-volume flavor manufacturers and high-purity applications in pharmaceuticals gives it a diversified and defensible market position.

Borregaard ASA Advances Lignin-Based Vanillic Acid Precursors Through Bio-Refinery Expertise

Borregaard maintains a unique competitive advantage by producing vanillin and related phenolics from sustainable Norway spruce lignin, positioning it as the only major global producer operating a full-scale biorefinery model. This approach results in a 90% reduction in CO₂ emissions compared to petrochemical synthesis, making Borregaard a preferred supplier for environmentally focused brands. Its EuroVanillin® portfolio includes technical-grade phenolics used for agrochemicals and polymer intermediates, enabling cross-industry adoption. With sustainability mandates tightening globally, Borregaard’s lignin-based value chain positions it at the forefront of bio-based Vanillic Acid precursor supply.

Tokyo Chemical Industry Co. Ltd. (TCI) Expands High-Purity Vanillic Acid Access for Global Research Markets

TCI is a major supplier of reagent-grade Vanillic Acid (>97%), providing the precision, traceability, and controlled synthesis necessary for research, pharmaceutical development, and analytical chemistry. Its global distribution network serves laboratories and specialty manufacturers requiring certified purity and reproducibility. TCI’s strategic expansions announced in February 2025 reflect its commitment to meeting growing demand for reference standards and regulated high-purity compounds, especially as Vanillic Acid gains traction as a functional ingredient in drug delivery and biomedical research.

Merck KGaA (Sigma-Aldrich) Enhances Quality Control with Reference-Grade Vanillic Acid Materials

Merck, through its Sigma-Aldrich brand, remains the dominant supplier of Vanillic Acid Certified Reference Materials (CRMs), supporting regulatory submissions worldwide. Its TraceCERT® range offers purity levels up to 99%+, fully traceable to NIST/NMIJ standards, which is critical for pharmaceutical, cosmetic, and food additive compliance testing. Merck’s wide portfolio and global logistics capabilities enable it to support both high-volume manufacturers and specialized analytical laboratories. Its leadership is reinforced by its focus on purity validation, global regulatory alignment, and analytical quality control.

Anthea Group Strengthens Its Aroma Chemicals Portfolio Through Vertical Integration

Anthea Group is rapidly growing as a key supplier in the Asian aroma chemicals market, leveraging its joint venture with Solvay—CATàSYNTH Specialty Chemicals—to build a fully integrated vanillin and aroma intermediates supply chain. This vertical integration ensures supply stability, lowers costs, and supports expanding Asian demand for Vanillic Acid and related aromatic compounds. With strong manufacturing capacity in India and increasing participation in global flavor and fragrance markets, Anthea is becoming a significant competitor in cost-efficient, high-quality Vanillic Acid precursor production.

Vanillic Acid Market Report Scope

Vanillic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$23.6 Billion

|

|

Market Size (2035)

|

$31.4 Billion

|

|

Market Growth Rate

|

2.9%

|

|

Segments

|

By Source (Synthetic Vanillic Acid, Natural Vanillic Acid), By Purity Grade (99%, 98%, Other Research Grades), By Application (Flavors & Fragrances, Pharmaceutical Intermediates, Cosmetics & Personal Care, Chemical Synthesis)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Solvay, TCI, Sigma-Aldrich/MilliporeSigma, Alfa Aesar, Acros Organics, Simson Pharma, CDH Fine Chemical, ABCR, Avanscure Lifesciences, Parchem, Santa Cruz Biotechnology, Guangzhou Sanyuan Chemical, OTTO KEMI

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Vanillic Acid Market Segmentation

By Source

- Synthetic Vanillic Acid

- Natural Vanillic Acid

By Purity Grade

- 99%

- 98%

- Other Research Grades

By Application

- Flavors & Fragrances

- Pharmaceutical Intermediates

- Cosmetics & Personal Care

- Chemical Synthesis

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Vanillic Acid Market

- Solvay

- TCI

- Sigma-Aldrich / MilliporeSigma

- Alfa Aesar

- Acros Organics

- Simson Pharma

- CDH Fine Chemical

- ABCR

- Avanscure Lifesciences

- Parchem

- Santa Cruz Biotechnology

- Guangzhou Sanyuan Chemical

- OTTO KEMI

*- List not Exhaustive

Research Coverage: Vanillic Acid Market

The latest Vanillic Acid Market study from USDAnalytics offers a deep-dive strategic intelligence platform for decision-makers as this report investigates demand drivers, technology pathways, and regulatory shifts across flavors & fragrances, pharmaceutical intermediates, cosmetics, nutraceuticals, and specialty chemicals. It tracks how bio-based bioconversion of ferulic acid, lignin valorization, and advanced biocatalytic routes are reshaping cost curves and purity benchmarks, while documenting breakthroughs in high-purity grades for dermal delivery, nano-formulations, and bio-based polymer precursors. The study further delivers analysis reviews of synthetic versus natural sourcing economics, downstream integration into vanillin and performance additives, and the evolving competitive landscape shaped by aroma chemical leaders, biorefineries, and high-purity reference material suppliers. It highlights how clean-label positioning, antioxidant and antimicrobial functionality, and circular feedstock strategies are redefining procurement and formulation strategies in regulated end-use industries. With quantitative coverage of market size, pricing structures, trade flows, and company positioning across key regions, this report is an essential resource for product managers, sourcing leaders, R&D chemists, and investors seeking granular visibility into how vanillic acid is transitioning from a traditional flavor intermediate to a versatile bio-based platform chemical in the global specialty ingredients economy.

Scope Highlights

- Segmentation:

By Source – Synthetic Vanillic Acid, Natural Vanillic Acid

By Purity Grade – 99%, 98%, Other Research Grades

By Application – Flavors & Fragrances, Pharmaceutical Intermediates, Cosmetics & Personal Care, Chemical Synthesis

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ companies across aroma chemicals, biorefineries, fine chemicals, and high-purity reagent suppliers.