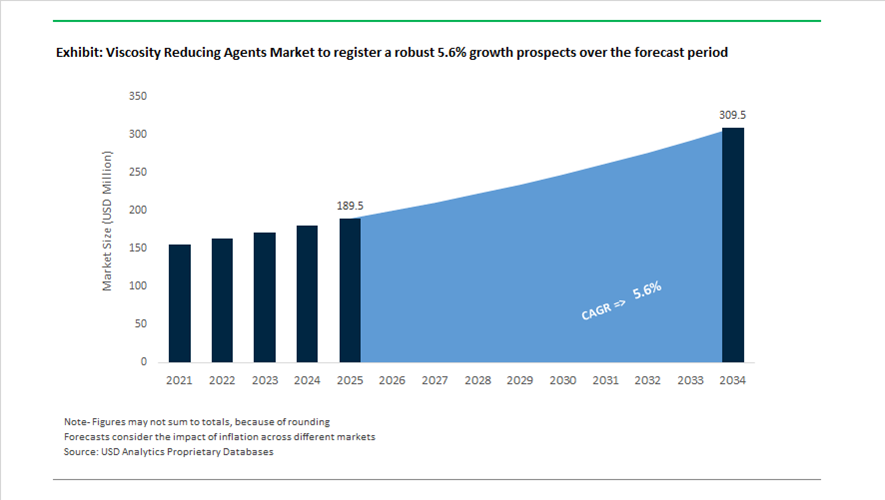

Viscosity Reducing Agents Market Overview 2025–2034: $189.5 Million to $309.4 Million at 5.6% CAGR Anchored in Flow Assurance, DRA Expansion, and Sustainable Additive Chemistry

The global Viscosity Reducing Agents market is valued at $189.5 million in 2025 and is projected to reach $309.4 million by 2034, expanding at a CAGR of 5.6%. Market expansion is being driven by rising demand for drag reducing agents (DRAs), friction reducers for pipelines, heavy oil viscosity modifiers, subsea flow assurance chemicals, liquid polybutadiene additives, and bio-based rheology modifiers across oil & gas, adhesives, plastics, and industrial processing sectors. Increasing pipeline throughput optimization, deepwater production complexity, and sustainability-driven reformulation in home care and industrial cleaning are reshaping additive design. Operators are prioritizing high-efficiency polymer-based friction reducers that improve laminar flow, reduce pumping energy requirements, and maintain performance in high-TDS and extreme pressure environments.

Strategic consolidation and capacity scaling accelerated between 2024 and 2026. In May 2024, FUCHS Group completed the acquisition and integration of LUBCON, strengthening its portfolio of advanced lubricants and viscosity management additives for high-load and vacuum environments. In 2024, Innospec introduced AquaBourne™, a patent-pending water-based friction reducer formulated without oil or surfactants, fully miscible in high total dissolved solids produced water, addressing environmental compliance and operational efficiency in unconventional shale plays. In early 2025, Halliburton and Coterra Energy launched the Octiv® Auto Frac system, automating real-time dosing of friction reducers and viscosity modifiers during hydraulic fracturing to reduce chemical waste and optimize well completions. In March 2025, Innospec introduced the LaZuli™ line certified for subsea production, engineered for viscosity control and flow assurance in deepwater offshore conditions. In July 2025, SLB finalized its acquisition of ChampionX, integrating heavy oil viscosity reduction technologies and midstream pipeline additives into its Production Systems division. In November 2025, Clariant Oil Services received recognition from Petrobras for chemical performance in Brazilian offshore fields, including viscosity management in naphthenate-stabilized emulsions. In February 2026, Innospec confirmed revenue growth tied to the successful scale-up of DRA manufacturing capacity expansion targeting North American pipeline optimization demand.

Sustainability and material science innovation are broadening application scope beyond oilfield chemicals. In October 2024, Evonik reorganized its portfolio to focus on liquid polybutadienes, critical viscosity-reducing components in high-performance adhesives and tire formulations, improving processing without compromising mechanical strength. In May 2025, Nouryon disclosed that 74% of its R&D pipeline is focused on sustainable chemistries, including bio-based surfactants and chelating agents that function as environmentally responsible viscosity modifiers in home care and industrial cleaning systems. In early 2025, Innospec’s Oklahoma City manufacturing hub achieved ISO 9001 certification, reinforcing quality standardization in friction reducer production. In February 2026 at Plastindia, BASF demonstrated how viscosity modifiers integrated with light stabilizers enhance flow characteristics and durability in agricultural plastic films.

Trends and Opportunities Shaping the Global Viscosity Reducing Agents Market

Advanced Drag Reducing Agents Transform Heavy Oil Pipeline Throughput Economics

The global viscosity reducing agents market is increasingly anchored in upstream and midstream oil and gas optimization, as operators confront the structural decline of low-viscosity conventional crude reserves. Advanced Drag Reducing Agents are now a strategic lever to sustain throughput, defer capital expenditure, and improve energy efficiency in heavy and ultra-heavy oil pipelines. In March 2025, Innospec announced a major expansion of its proprietary DRA manufacturing capacity at its Pleasanton, Texas facility. This move directly targets rising midstream demand for high-performance polymeric additives that allow operators to increase pipeline flow without installing additional pumping stations or compressors, a critical advantage in mature basins with constrained infrastructure.

Operational data from late 2024 and 2025 demonstrates that polymer-based viscosity reducing agents, injected at parts-per-million concentrations, can reduce turbulent flow friction by up to 60 to 80%. This enables pipeline operators to maintain or even exceed nameplate capacity while lowering pump power requirements, translating into meaningful reductions in electricity consumption and Scope 2 emissions. As carbon intensity metrics increasingly influence capital allocation decisions, DRAs are transitioning from optional flow improvers to core assets in pipeline decarbonization strategies.

Mining Tailings Rheology Management Driven by GISTM Compliance Deadlines

Outside hydrocarbons, the viscosity reducing agents market is seeing structurally driven growth in the global mining sector, where regulatory pressure is reshaping tailings management practices. The August 2025 compliance deadline under the Global Industry Standard on Tailings Management has elevated rheology control from a process optimization tool to a regulatory necessity for high-consequence tailings storage facilities. Mining operators are integrating VRAs to enable thickened and paste tailings systems that support safer dry stacking methodologies.

Peer-reviewed technical literature from 2025 highlights that viscosity modifiers are essential for transporting slurries with solids concentrations approaching 70%. By lowering yield stress and apparent viscosity, VRAs allow ultrafine tailings to remain pumpable, reducing reliance on conventional slurry dams. This approach improves water recovery rates by up to 30%, directly supporting water stewardship targets while lowering the risk profile of tailings facilities. As International Council on Mining and Metals member companies accelerate compliance programs, procurement of specialized rheology modifiers has become a priority within environmental and geotechnical budgets.

High-Solids Waste-to-Energy Feedstocks Create New Demand for Viscosity Control

A major opportunity for viscosity reducing agents is emerging from the rapid expansion of circular economy infrastructure, particularly waste-to-energy and advanced biofuel production. Processing high-viscosity feedstocks such as sewage sludge, food waste, and agricultural residues requires precise rheological control to maintain pumpability at elevated solids content. Research initiatives reported in October 2025 show that the use of targeted VRAs enables an increase in total solids concentration from approximately 10% to 20% without compromising flow characteristics.

This shift toward high-solids logistics materially improves anaerobic digestion efficiency. Co-digestion trials combining maize silage and sludge achieved biogas yields as high as 309 normal cubic meters per kilogram of dry matter, significantly enhancing energy density and overall plant economics. In parallel, industrial trials conducted during 2024 and 2025 indicate that inorganic and environmentally benign viscosity reducers can facilitate extrusion and drying of dewatered sludge while lowering mechanical handling energy requirements. These gains are accelerating the adoption of decentralized bioenergy systems, positioning VRAs as enablers of scalable, low-carbon waste valorization.

Precision Rheology Control Enables Industrial-Grade Additive Manufacturing

The most technologically sophisticated opportunity for viscosity reducing agents lies in industrial additive manufacturing, where rheology directly determines print fidelity, mechanical performance, and production yield. As 3D printing expands into regulated medical devices and aerospace components, the demand for advanced rheology modifiers capable of fine-tuning shear-thinning and recovery behavior is accelerating.

At Formnext 2025, Henkel showcased medical-grade and industrial photopolymers under its Loctite 3D Printing portfolio that rely on advanced viscosity control to achieve high feature resolution and low solvent absorption. These formulations require VRAs that allow smooth extrusion under shear while rapidly restoring viscosity to prevent layer collapse and dimensional distortion.

Further highlighting this opportunity, the 2025 collaboration between Nexa3D and Henkel demonstrated the role of precision rheology in the production of additively manufactured connected medical devices. In such applications, viscosity reducing agents are essential to maintaining isotropic mechanical properties and biocompatibility across complex geometries. As additive manufacturing transitions from prototyping to serial production, demand is shifting toward high-value, application-specific VRAs that function as performance enablers rather than commodity additives.

Viscosity Reducing Agents Market Share and Segmentation Insights

Product Type Market Share: Drag Reducing Agents Lead with Pipeline Flow Efficiency Enhancement

Drag reducing agents hold a 32.8% share in the viscosity reducing agents market in 2025, driven by their critical role in minimizing turbulent friction during pipeline transport of crude oil and refined products. These high-molecular-weight polymer additives enable higher flow rates and reduced energy consumption, improving operational efficiency. Polymeric additives, solvents and diluents, surfactants, and dispersants serve complementary roles across industrial processes. A key trend is pipeline capacity optimization, where operators use drag reducing agents to increase throughput by 10 to 30% without major capital investment, supporting demand across mature oil and gas infrastructure networks.

End-User Industry Market Share: Oil and Gas Sector Dominates with Upstream to Midstream Flow Optimization

Oil and gas account for 52.8% of the viscosity reducing agents market in 2025, reflecting the widespread need for flow assurance across upstream production, pipeline transport, and refining processes. These agents are essential for handling heavy and viscous crude oils, improving flow characteristics and reducing operational constraints. Chemical manufacturing, construction, and automotive sectors contribute additional demand across specialized applications. A key market driver is the expansion of unconventional oil production, where hydraulic fracturing, horizontal drilling, and increased water handling requirements necessitate advanced viscosity reducing formulations, sustaining demand across global energy production systems.

Viscosity Reducing Agents Market Competitive Landscape

The Viscosity Reducing Agents market in 2026 is defined by molecular efficiency, energy decarbonization, and AI-driven dosage optimization, with water-based friction reducers and digital flow assurance systems reducing Specific Energy Consumption (SEC) across oil & gas, refining, and industrial fluid transport applications.

Baker Hughes Integrates AI-Driven Chemical-Digital Twin for Refinery Viscosity Optimization

Baker Hughes is strengthening its leadership in the Viscosity Reducing Agents market by integrating advanced chemical solutions with digital asset performance management. Its multiyear agreement with Marathon Petroleum covers 12 refineries, deploying XERIC™ viscosity control and demulsifier technologies to enhance throughput and reduce operational inefficiencies. The company’s AI-powered Asset Performance Management platform enables real-time rheology modeling, reducing unplanned downtime by up to 25%. BIOQUEST™ renewable additives support viscosity control in biofuel processing, aligning with refinery decarbonization strategies. Its Chemical-Digital Twin capability allows simulation of fluid behavior prior to chemical injection, minimizing waste and optimizing dosage. This integration of digital intelligence and specialty chemicals enhances operational efficiency across refining assets.

Halliburton Advances Closed-Loop Automation for Real-Time Viscosity Control in Drilling Operations

Halliburton is a dominant force in the Viscosity Reducing Agents market, focusing on closed-loop automation and precision fluid management in upstream operations. Its collaboration with ExxonMobil achieved fully automated well placement, utilizing advanced viscosity modifiers to control equivalent circulating density in real time. The StreamStar™ wired drill pipe system enables continuous downhole monitoring of fluid viscosity, supporting dynamic chemical dosing. The NEX Lab℠ partnership with A*STAR is accelerating development of high-performance friction reducers for HPHT environments. Expansion into Indonesia through Pertamina highlights its focus on unconventional reservoirs requiring advanced fluid mobility solutions. This combination of automation, sensing, and chemical innovation strengthens Halliburton’s upstream leadership.

ChampionX Enhances Flow Assurance with Emulsion Viscosity Reduction and Multifunctional Chemistry

ChampionX is a specialized leader in the Viscosity Reducing Agents market through its advanced flow assurance technologies targeting complex production environments. Its Emulsion Viscosity Reduction (EVR) chemistry has demonstrated production increases of 750 BOPD by resolving water-in-oil emulsions in subsea pipelines. The company’s multifunctional formulations combine viscosity reducers with scale and wax inhibitors, enabling single-point treatment in offshore systems. The ParaClear system addresses wax deposition challenges, maintaining pipeline flow without thermal intervention. Its proprietary modeling platform identifies optimal wells for chemical application, ensuring measurable production uplift. This data-driven approach enhances efficiency in challenging subsea and midstream operations.

Innospec Develops Water-Based Friction Reducers for Sustainable Midstream and Fuel Applications

Innospec Inc. is advancing the Viscosity Reducing Agents market through environmentally clean, water-based friction reducer technologies. Its AquaBourne™ formulation eliminates hydrocarbons and is fully compatible with high-TDS produced water, supporting sustainable oilfield operations. The LaZuli™ product line addresses deepwater viscosity challenges, preventing hydrate formation and paraffin deposition in subsea pipelines. Strong demand for cold flow improvers is driving growth in fuel specialties, particularly in low-temperature logistics environments. The company’s Dry-on-the-Fly polymer technology reduces transportation emissions by enabling onsite hydration of friction reducers. This focus on sustainability and operational flexibility strengthens Innospec’s competitive positioning.

Clariant Expands Digital Viscosity Control and Circular Feedstock Processing Technologies

Clariant is strengthening its role in the Viscosity Reducing Agents market through digital monitoring platforms and advanced specialty chemicals. Its CLARITY™ platform provides real-time performance data across 38 countries, enabling optimized use of viscosity modifiers in industrial processes. Expansion of its Clear Lake facility enhances production of pharmaceutical-grade PEG for viscosity control in healthcare and personal care applications. The company is developing agrochemical formulations that maintain sprayability under high active ingredient concentrations. Its collaboration with Borealis on pyrolysis oil upgrading demonstrates expertise in managing viscosity for circular feedstocks. This integration of digital analytics and specialty chemistry supports high-performance industrial and sustainability-driven applications.

United States Viscosity Reducing Agents Market Driven by Pipeline Throughput Optimization and Digital Flow Assurance

The United States viscosity reducing agents market is experiencing structurally higher demand, anchored in midstream capacity expansion, refinery efficiency mandates, and digitally enabled flow assurance. In March 2025, Innospec Inc. announced a multi-million-dollar expansion of its proprietary drag reducing agent production at its Pleasanton, Texas facility, with commissioning targeted for Q4 2025. The expansion directly responds to rising domestic requirements for pipeline throughput optimization as operators seek to maximize capacity utilization without capital-intensive pipeline duplication. Drag reducing agents and polymeric viscosity modifiers are increasingly positioned as strategic tools to unlock incremental volumes across crude oil, refined products, and NGL transport systems.

Operational intelligence is further reshaping chemical deployment strategies. Throughout 2025, Gulf of Mexico operators integrated ChampionX SMARTEN XE digital control platforms with viscosity modifier injection systems. This chemical-digital convergence enables second-by-second monitoring of injection rates and pressure differentials, reducing surfactant overuse by an estimated 12% while improving flow stability in deepwater tiebacks. Market dynamics in base oils are also influencing demand. In 2025, U.S. N220 mid-viscosity base oils traded at an unprecedented discount to lighter N100 grades, creating margin pressure in heavy-duty engine oil formulations. Refiners are responding by adopting more advanced viscosity reducing additives to fine-tune rheology without sacrificing performance. At the same time, U.S. refiners have increased procurement of water-based viscosity reducers to comply with tighter Environmental Protection Agency effluent guidelines, particularly when processing heavy Canadian dilbit with elevated carbon intensity profiles.

China Viscosity Reducing Agents Market Accelerated by Heavy Oil Recovery and Gas Infrastructure

China’s viscosity reducing agents market is expanding rapidly, driven by breakthroughs in heavy oil recovery and aggressive natural gas infrastructure development. In 2025, researchers at the Tahe Oilfield in western China successfully deployed a multi-component synergistic viscosity reduction system utilizing coal tar and washing oil by-products. The solution achieved a reported 99.8% viscosity reduction for extra-heavy crude, materially lowering the cost of cold recovery methods and reducing reliance on energy-intensive thermal techniques. This advancement positions viscosity reducing chemistry as a core enabler of China’s domestic heavy oil production strategy.

Gas sector growth is reinforcing demand. Under the 14th Five-Year Plan, China’s natural gas consumption is projected to reach 430 billion cubic meters by 2025, triggering large-scale investments in hydraulic fracturing across the Sichuan basin. Friction reducers and polymeric viscosity modifiers are being deployed extensively to improve pumping efficiency and proppant transport in unconventional reservoirs. Capacity localization supports this trend. In 2025, Clariant expanded its One Clariant Campus in Shanghai, allocating more than one-third of global growth capital expenditure to China. The site focuses on localized production of sustainability-oriented EcoTain-labeled rheology modifiers, aligning performance optimization with China’s tightening environmental expectations.

India Viscosity Reducing Agents Market Shaped by Chemical Industrial Policy and Offshore E&P

India’s viscosity reducing agents market is entering a policy-driven expansion phase, supported by national chemical sector ambitions and upstream energy projects. The 2025 roadmap released by NITI Aayog outlines a strategy to raise India’s share of the global chemicals value chain to 5–6% by 2030. Central to this plan is a dedicated Chemical Fund for infrastructure development across eight high-potential clusters, with viscosity reducing agent manufacturing identified as a priority segment for value addition and import substitution.

Economic incentives are accelerating capacity build-out. To address a persistent specialty chemicals trade deficit, the Indian government introduced an operating expenditure subsidy scheme in July 2025 that specifically encourages domestic production of high-molecular-weight polymeric flow improvers. These additives are critical for lubricants, fuels, and pipeline transport. Offshore energy developments add another demand layer. In 2025, Oil and Natural Gas Corporation initiated new deepwater projects in the Krishna-Godavari basin, deploying advanced cationic viscosity reducers to manage high-pour-point crudes in subsea pipelines. This convergence of policy, manufacturing, and upstream activity positions India as a fast-emerging production and consumption hub for viscosity reducing agents.

Norway Viscosity Reducing Agents Market Defined by Bio-Based Solutions and Arctic Operations

Norway’s viscosity reducing agents market is distinguished by its sustainability orientation and extreme-environment engineering. In 2025, Borregaard leveraged its integrated biorefinery platform to supply wood-derived lignosulfonates as bio-based viscosity reducers for construction materials and oilfield applications. These products demonstrated a materially lower product carbon footprint compared with petroleum-derived alternatives, aligning with Norway’s stringent climate objectives and the procurement standards of international operators.

Offshore innovation remains central. Norwegian operators are actively testing low-temperature surfactant systems designed to preserve fluidity under sub-zero seabed conditions. These viscosity modifiers reduce dependence on high-energy thermal heating in Arctic and near-Arctic fields, improving operational efficiency while lowering emissions. Norway’s role is therefore less about volume scale and more about setting performance benchmarks for sustainable flow assurance in harsh operating environments.

Saudi Arabia Viscosity Reducing Agents Market Anchored in Downstream Integration and Water Management

Saudi Arabia’s viscosity reducing agents market is closely linked to downstream integration strategies and industrial water management. In 2025, Saudi Aramco intensified its Liquids-to-Chemicals program, embedding large-scale viscosity reduction units within integrated refining complexes. These systems enable more efficient conversion of heavy residuum into higher-value light olefins, positioning viscosity reduction as a yield-optimization lever rather than solely a flow assurance tool.

Water sustainability initiatives further support chemical demand. Across Saudi industrial clusters, 2025 saw a marked increase in the deployment of mechanical vapor recompression evaporators to achieve Zero Liquid Discharge targets. These systems rely on specialized anti-scalants and viscosity modifiers to maintain operational efficiency under high-salinity conditions. As a result, viscosity reducing agents are increasingly embedded in both hydrocarbon processing and industrial water treatment strategies across the Kingdom.

Summary of Country-Level Viscosity Reducing Agents Market Dynamics

Viscosity Reducing Agents Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Core Applications

|

Market Positioning

|

|

United States

|

Pipeline optimization and digital flow assurance

|

Midstream pipelines, refining

|

Technology-driven efficiency leader

|

|

China

|

Heavy oil recovery and gas expansion

|

Extra-heavy crude, hydraulic fracturing

|

Scale-driven deployment hub

|

|

India

|

Chemical policy and offshore development

|

Lubricants, subsea pipelines

|

Emerging manufacturing and demand center

|

|

Norway

|

Bio-based innovation and Arctic operations

|

Oilfield, construction

|

Sustainability and extreme-environment benchmark

|

|

Saudi Arabia

|

Downstream integration and ZLD

|

Refining, industrial water

|

Integrated process optimization market

|

Viscosity Reducing Agents Market Report Scope

Viscosity Reducing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$189.5 Million

|

|

Market Size (2034)

|

$309.4 Million

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Type (Polymeric Additives, Surfactants, Dispersants, Solvents and Diluents, Drag Reducing Agents), By Chemistry (Oil-Based Reducers, Water-Based Reducers, Bio-Based Formulations), By Application (Extraction and Production, Transportation and Pipelines, Refining and Petrochemical Processing, Industrial Applications), By End-User Industry (Oil and Gas, Automotive and Transportation, Construction and Infrastructure, Chemical and Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Innospec Inc., ChampionX Corporation, Baker Hughes Company, Clariant AG, BASF SE, Halliburton Company, Evonik Industries AG, Nalco Champion, Dow Inc., Croda International Plc, Arkema S.A., Lubrizol Corporation, SNF Group, Chevron Phillips Chemical Company, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Viscosity Reducing Agents Market Segmentation

By Product Type

- Polymeric Additives

- Surfactants

- Dispersants

- Solvents and Diluents

- Drag Reducing Agents

By Chemistry

- Oil-Based Reducers

- Water-Based Reducers

- Bio-Based Formulations

By Application

- Extraction and Production

- Transportation and Pipelines

- Refining and Petrochemical Processing

- Industrial Applications

By End-User Industry

- Oil and Gas

- Automotive and Transportation

- Construction and Infrastructure

- Chemical and Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Viscosity Reducing Agents Market

- Innospec Inc.

- ChampionX Corporation

- Baker Hughes Company

- Clariant AG

- BASF SE

- Halliburton Company

- Evonik Industries AG

- Nalco Champion

- Dow Inc.

- Croda International Plc

- Arkema S.A.

- Lubrizol Corporation

- SNF Group

- Chevron Phillips Chemical Company

- Huntsman Corporation

*- List not Exhaustive