Rising Demand in the Global Wastewater Reverse Osmosis Membrane Market

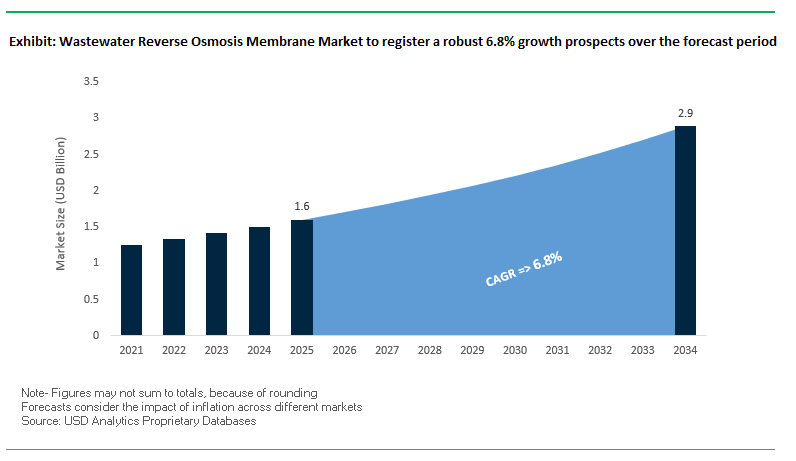

The Wastewater Reverse Osmosis (RO) Membrane Market is forecasted to grow from USD 1.6 billion in 2025 to USD 2.9 billion by 2034, achieving a CAGR of 6.8%. This steady growth is driven by the global water crisis, escalating industrial effluent challenges, and the urgent need for sustainable wastewater treatment technologies.

Key factors shaping the market include:

- Water Scarcity and Reuse Mandates: With 48% of global wastewater still discharged untreated, governments and industries are prioritizing advanced RO-based water reuse systems for agriculture, industrial processes, and even potable applications.

- Industrial Wastewater Regulations: Stricter rules, such as the U.S. EPA’s Effluent Guidelines, are forcing industries to adopt RO membranes for minimal liquid discharge (MLD) and resource recovery, turning wastewater into a valuable resource.

- Energy-Efficient RO Systems: Next-generation RO membranes operate at lower pressures, cutting energy consumption and OPEX for municipal and industrial wastewater treatment plants.

- Advanced Contaminant Removal: Reverse osmosis membranes are increasingly deployed for emerging pollutants such as PFAS, microplastics, and pharmaceutical residues critical for compliance and public health.

Market Analysis: Recent Developments in Wastewater RO Membranes

The wastewater reverse osmosis membrane industry is experiencing accelerated innovation and strategic partnerships, highlighted by major developments between February 2024 and August 2025. These events underscore the industry’s dual focus on sustainability and efficiency.

In August 2025, DuPont Water Solutions received a BIG Sustainability Award for its FilmTec™ Fortilife™ membranes, which are designed for industrial wastewater reuse and minimal liquid discharge (MLD). That same month, Asahi Kasei’s Microza® membrane earned a Gold EcoVadis rating, placing its water processing unit among the top 5% of sustainable businesses globally.

In July 2025, Toray Industries supplied RO membranes for the Shuaibah 3 IWP desalination project in Saudi Arabia, converting an energy-intensive plant into an eco-friendly setup expected to cut 45 million tons of CO₂ annually. Also in July, SUEZ commissioned China’s largest industrial seawater desalination plant for Wanhua Chemical, with RO membranes at its core, while simultaneously securing new SWRO projects in the Philippines to expand its Asian footprint.

Earlier in June 2025, LG Chem announced the sale of its water solutions business, including RO membranes, to Glenwood Private Equity, signaling a strategic retreat from water treatment to focus on batteries and eco-materials. In March 2025, DuPont launched WAVE PRO, an advanced modeling tool for RO and ultrafiltration, enabling engineers to design optimized wastewater treatment systems. Going back to February 2025, Asahi Kasei inaugurated a biogas purification system in Japan, showcasing how membranes extend beyond water to support renewable energy recovery.

Emerging Trends and Growth Opportunities in the Wastewater Reverse Osmosis Membrane Market

Rising Impact of Strict Government Regulations on Wastewater RO Adoption

The wastewater reverse osmosis (RO) membrane market is heavily influenced by government mandates pushing industries and municipalities toward sustainable water management. The U.S. Environmental Protection Agency (EPA) continuously updates its technology-based “Effluent Guidelines,” requiring advanced treatment processes such as RO to reduce industrial wastewater pollutants. Similarly, in India, the National Green Tribunal (NGT) has imposed substantial penalties on state authorities for failing to meet wastewater treatment standards, reinforcing the need for RO systems in municipal and industrial sectors. This growing enforcement framework is expected to accelerate the deployment of wastewater RO membranes worldwide.

Technological Advancements in Anti-Fouling RO Membranes

Membrane fouling remains one of the most persistent challenges in wastewater treatment. Recent R&D breakthroughs are addressing this limitation, with nanomaterial-enhanced RO membranes showing significantly higher resistance to fouling. Research published in ACS Applied Materials & Interfaces highlights the effectiveness of titanium dioxide and graphene oxide-modified RO membranes, which substantially reduce organic and biological fouling. These membranes not only cut down cleaning frequency but also extend system lifespan, making them highly attractive for cost-sensitive industries facing complex wastewater streams.

Strategic Corporate Investments Strengthening Market Position

Leading membrane manufacturers are investing aggressively in capacity expansion and R&D to meet rising demand. LG Chem recently committed multi-million-dollar funding to expand its RO membrane production, targeting industrial and wastewater reuse applications. Likewise, Toray Industries broadened its membrane manufacturing capabilities in China, specifically focusing on advanced wastewater treatment. These large-scale investments reflect a growing confidence in the long-term profitability of wastewater RO technologies and highlight intensified competition in the market.

Expanding Application in Municipal and Industrial Water Reuse

Beyond traditional industrial wastewater treatment, RO membranes are playing a transformative role in municipal water reuse. In California, large-scale reclamation plants now use RO membranes as a key purification step for groundwater recharge, enabling “toilet-to-tap” projects that secure sustainable urban water supplies. In the industrial sector, alumina production facilities have successfully deployed RO systems to recycle complex wastewater, significantly reducing freshwater demand. This expansion into potable reuse and high-value industrial recycling demonstrates the growing versatility and critical role of wastewater RO membranes in achieving circular water economy goals.

Market Share Analysis of the Wastewater Reverse Osmosis Membrane Market

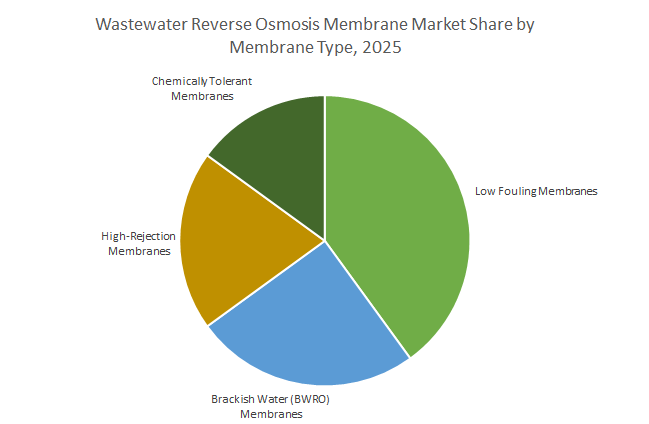

Market Share by Membrane Type

Low Fouling Membranes are projected to command the largest share at 40% due to their ability to resist organic and biological fouling, the most critical operational challenge in wastewater treatment. Brackish Water RO (BWRO) membranes will hold around 25%, serving less aggressive effluents or second-stage treatment. High-Rejection Membranes, with a 20% share, are indispensable for applications requiring >99.5% salt removal, particularly in potable reuse and compliance with stringent discharge standards. Chemically Tolerant Membranes will account for 15%, providing essential resistance to aggressive effluents such as textile, pharmaceutical, and landfill leachate wastewater. The dominance of low-fouling solutions underscores the market’s prioritization of operational reliability, while specialized membranes address extreme industrial conditions.

Market Share by Wastewater Source

Industrial Wastewater Treatment will dominate the market with approximately 65% share, driven by zero-liquid discharge (ZLD) regulations, escalating disposal costs, and corporate sustainability commitments. Within this category, industries such as pharmaceuticals, textiles, oil & gas, and microelectronics face highly diverse contamination challenges ranging from heavy metals to solvents and dyes, necessitating advanced RO configurations. Municipal Wastewater Reuse will capture 30%, expanding rapidly due to rising demand for irrigation, aquifer recharge, and potable reuse in water-stressed urban centers. Industrial applications drive the bulk of volume, but municipal reuse projects are emerging as the flagship growth driver, shaping public policy and infrastructure investment.

Market Share by System Integration & Process

Integrated Membrane Systems (IMS), combining RO with pre-treatment processes such as microfiltration (MF) or ultrafiltration (UF), will account for nearly 85% of the market. This dominance reflects the industry’s recognition that successful wastewater RO treatment depends heavily on robust pre-treatment, which reduces fouling, increases recovery rates, and extends membrane life. Standalone RO systems will represent just 15%, mostly in niche applications where influent wastewater is already highly polished or where retrofits limit pre-treatment integration. Despite higher upfront capital costs, IMS configurations deliver superior long-term return on investment (ROI), making them the preferred design in both municipal and industrial projects worldwide.

China: Regulatory Push and Industrial Adoption of Reverse Osmosis Membranes

China’s wastewater reverse osmosis membrane market is strongly influenced by stringent environmental regulations and strategic government investments. The Ministry of Ecology and Environment (MEE) enforces strict guidelines on industrial wastewater discharge, compelling companies to adopt advanced reverse osmosis membrane technologies to meet compliance standards. In 2024, Chinese researchers developed hollow-fiber ultrafiltration membranes with enhanced antifouling properties, which are increasingly integrated as pretreatment for RO systems in membrane bioreactors (MBRs), reducing maintenance costs and improving efficiency. The textile industry is also a key application area, with membrane-based recycling systems recovering over 95% of process water from dyeing effluents containing high total dissolved solids (TDS), showcasing RO membranes’ critical role in industrial water reuse. Government-backed investments in zero-liquid discharge (ZLD) systems further bolster demand for high-performance RO membranes across China’s industrial sector.

Saudi Arabia: Desalination Infrastructure and Energy-Efficient RO Technologies

Saudi Arabia is a leading market for wastewater reverse osmosis membranes, driven by large-scale desalination projects and energy-efficient innovations. ACWA Power’s Jubail 3A desalination plant, an independent water project (IWP), produces 600,000 cubic meters of freshwater daily using advanced RO membranes, highlighting the country’s infrastructure-driven demand. The Saline Water Conversion Corporation (SWCC) pioneers energy-efficient seawater reverse osmosis (SWRO) membranes, exemplified by the Yanbu 4 plant producing 450,000 cubic meters of water per day. Government initiatives by the Saudi Water Partnership Company (SWPC), such as the Rabigh 4 project, reinforce the strategic adoption of RO-based membrane solutions, cementing Saudi Arabia’s position as a hub for large-scale, membrane-driven water treatment.

United States: Government Funding and Private Sector Innovation

The United States wastewater reverse osmosis membrane market benefits from robust government funding, academic research, and private sector deployment. The Bipartisan Infrastructure Law allocates over $50 billion to the EPA for upgrading drinking water, wastewater, and stormwater infrastructure, including advanced RO membrane technologies to address emerging contaminants like PFAS. NSF-funded research centers focus on innovative membranes for water purification, chemical separations, and biopharmaceutical processing, driving technical advancements. Companies like Veolia Water Technologies have deployed reverse osmosis systems to deliver PFAS-compliant water to over 140,000 Americans, demonstrating the integration of advanced RO membranes in municipal and industrial applications.

India: Policy Support and Strategic Infrastructure Investments

India’s wastewater reverse osmosis membrane market is growing due to government programs, urban infrastructure development, and industrial adoption. The Jal Jeevan Mission and the Department of Science & Technology’s Water Technology Initiative promote R&D in filtration technologies, including reverse osmosis, to ensure affordable access to safe water in rural areas. The Ghaziabad Nagar Nigam raised ₹150 crore through India’s first Certified Green Municipal Bond for a Tertiary Sewage Treatment Plant (TSTP) utilizing RO and other membrane technologies for wastewater reuse. Additionally, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant in Chennai, valued at INR 415 crores, underscores significant investment in membrane-based water infrastructure, highlighting the growing reliance on RO membranes for industrial and municipal applications.

Japan: Academic and Corporate Leadership in RO Membranes

Japan is a key player in the wastewater reverse osmosis membrane market, leveraging both academic excellence and corporate innovation. The Membrane Engineering Group at Kobe University continues to develop novel functional membranes for water and atmospheric applications, including RO systems. Toray Industries, a global leader, supplies high-performance RO membranes for large-scale projects such as desalination plants in Saudi Arabia, where these membranes often serve as essential pretreatment or main filtration units. Japan’s focus on research and global deployment reinforces its leadership in RO membrane technology for water and wastewater applications.

Australia: Water Recycling and Advanced RO Research

Australia faces chronic water stress, driving strong adoption of wastewater reverse osmosis membranes. Facilities like the Sydney Water Wollongong Water Resource Recovery Facility employ integrated microfiltration and RO systems to treat wastewater for irrigation and industrial reuse. Academic research at Victoria University’s Institute for Sustainable Industries and Liveable Cities (ISILC) focuses on increasing water recovery from desalination processes and minimizing membrane fouling and scaling, critical challenges in sustainable water management. These initiatives position Australia as a leader in membrane-based water recycling and advanced RO technology adoption.

Competitive Landscape: Key Players in the Wastewater RO Membrane Market

The wastewater RO membrane market is highly competitive, with leading players focusing on technological innovation, sustainability strategies, and large-scale project execution. Below is an in-depth look at the key companies shaping the industry:

DuPont Water Solutions: Driving Wastewater Reuse with FilmTec™ Fortilife™

DuPont is at the forefront of industrial wastewater reuse and minimal liquid discharge (MLD). Its FilmTec™ Fortilife™ membranes are engineered for challenging effluents, achieving higher recovery rates and reduced cleaning costs. The launch of WAVE PRO in March 2025 exemplifies DuPont’s integration of digital optimization tools into membrane design, enabling operators to maximize efficiency. The company’s recognition with the BIG Sustainability Award in August 2025 further reinforces its leadership in sustainable wastewater RO solutions.

Toray Industries: Scaling Energy-Efficient Desalination and Wastewater Projects

Toray is a leading supplier of high-performance RO membranes for desalination and wastewater reclamation. Its July 2025 Shuaibah 3 IWP project in Saudi Arabia transformed a conventional plant into a low-carbon facility, reducing emissions by 45 million tons of CO₂ annually. With its Water Treatment Technology Center in Saudi Arabia, Toray delivers localized technical expertise, supporting diverse applications ranging from industrial wastewater treatment to agricultural reuse.

SUEZ Water Technologies & Solutions: Large-Scale Wastewater RO Expertise

SUEZ, part of the Veolia group, leverages its expertise in integrated water and waste management to deliver RO membrane projects at scale. In July 2025, it commissioned China’s largest industrial seawater desalination facility, cementing its role in high-capacity RO deployments. With additional SWRO projects in the Philippines and smart digital platforms for water grid optimization, SUEZ continues to expand its influence in Asia’s growing wastewater treatment market.

LG Chem: Strategic Exit from the RO Membrane Business

LG Chem historically played a significant role in the RO membrane market, with applications in industrial wastewater treatment and desalination. Its membranes were widely recognized for high salt rejection and low energy demand. In June 2025, LG Chem sold its water solutions business to Glenwood Private Equity, pivoting its focus toward eco-materials and battery technologies. Despite its exit, LG Chem’s legacy includes major contracts, such as supplying membranes to the world’s largest fertilizer complex in Morocco.

Koch Separation Solutions (KSS): Advanced PURON® Membrane Technology

Operating as Kovalus Separation Solutions, KSS specializes in engineered wastewater treatment systems. Its PURON® reinforced hollow fiber membranes are known for low fouling, high productivity, and minimal cleaning, making them ideal for challenging industrial effluents. With plans to expand production by 50% through a new Mexico facility, KSS is strengthening its supply chain while serving industries such as food and beverage, life sciences, and automotive wastewater treatment.

Wastewater Reverse Osmosis Membrane Market Report Scope

Wastewater Reverse Osmosis Membrane Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$2.9 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

Membrane Type (BWRO Membranes, Low Fouling Membranes, High-Rejection Membranes, Chemically Tolerant Membranes), Wastewater Source (Municipal Wastewater Reuse, Industrial Wastewater Treatment, Food & Beverage, Power Generation, Microelectronics, Pharmaceuticals, Textiles, Landfill & Leachate, Oil & Gas), System Integration & Process (Standalone RO Systems, Integrated Membrane Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., SUEZ, Veolia, Toray Industries, Inc., Pentair plc, Xylem Inc., Asahi Kasei Corporation, Kubota Corporation, LG Chem, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, Hydranautics (a Nitto Group Company), Koch Industries, V.A. TECH WABAG Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wastewater Reverse Osmosis Membrane Market Segmentation

By Membrane Type

- Wastewater-Ready Brackish Water (BWRO) Membranes

- Low Fouling Membranes

- High-Rejection Membranes

- Chemically Tolerant Membranes

By Wastewater Source

- Municipal Wastewater Reuse

- Industrial Wastewater Treatment

- Food & Beverage

- Power Generation

- Microelectronics

- Pharmaceuticals

- Textiles

- Landfill & Leachate

- Oil & Gas

By System Integration & Process

- Standalone RO Systems

- Integrated Membrane Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Wastewater Reverse Osmosis Membrane Industry include-

- DuPont de Nemours, Inc.

- SUEZ

- Veolia

- Toray Industries, Inc.

- Pentair plc

- Xylem Inc.

- Asahi Kasei Corporation

- Kubota Corporation

- LG Chem

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- Hydranautics (a Nitto Group Company)

- Koch Industries

- V.A. TECH WABAG Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the global wastewater RO membrane market, delivering analysis reviews on how water-scarcity risk, reuse mandates, and industrial effluent complexity are accelerating RO adoption from MLD/ZLD plants to potable-reuse trains. It highlights breakthroughs in low-pressure/high-permeance sheets, chemically tolerant layers, and anti-fouling surface chemistries that cut OPEX and extend cleaning intervals, while digital design tools improve staging, recovery, and brine-management economics. The study also highlights policy tightening (effluent guidelines, reuse targets), integrated pretreatment (MF/UF) that stabilizes SDI and protects RO, and emerging contaminant control (PFAS, pharmaceuticals, microplastics) shaping specification trends. With stack-level reliability metrics and country rollouts, USDAnalytics converts technology performance into bankable outcomes making this report an essential resource for utilities, EPCs, and industrial owners planning resilient wastewater-to-resource projects. Scope Includes-

- Segmentation: By Membrane Type (Wastewater-Ready BWRO; Low Fouling; High-Rejection; Chemically Tolerant); By Wastewater Source (Municipal Reuse; Industrial Wastewater Food & Beverage, Power, Microelectronics, Pharmaceuticals, Textiles, Landfill & Leachate, Oil & Gas); By System Integration & Process (Standalone RO Systems; Integrated Membrane Systems)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

- Companies: Profiles of 15+ companies (e.g., DuPont, SUEZ, Veolia, Toray, Pentair, Xylem, Asahi Kasei, Kubota, LG Chem, Dow, MANN+HUMMEL, Evoqua, Hydranautics/Nitto, Koch, VA TECH WABAG)

Methodology

We employ a mixed-methods design: primary interviews with utilities, industrial operators, OEMs/EPCs, and regulators; and secondary research across standards, patents, filings, and peer-reviewed literature. Market sizing blends top-down triangulation (installed base, retrofit cycles, reuse mandates, disposal cost curves) with bottom-up BOM models for RO trains (element area, flux, TMP, recovery, specific energy, cleaning frequency, replacement intervals). Forecasts incorporate learning rates for sheet manufacturing, pretreatment quality (SDI/turbidity) sensitivity, electricity/chemicals pricing, and policy cadence for discharge/reuse. Competitive benchmarking evaluates membrane classes on normalized permeability, salt/TOC rejection, fouling propensity, chemical/thermal envelopes, and lifecycle cost per 1,000 m³. All results pass cross-validation against commissioning data, project announcements, and scenario stress-tests (PFAS compliance, high-TDS leachate, textile dyes).

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Wastewater Reverse Osmosis Membrane Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Wastewater Reverse Osmosis Membrane Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.6 Billion

2.2.2. Forecasted Market Size (2034): $2.9 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 6.8%

2.3. Key Factors Shaping Market Growth

2.3.1. Water Scarcity and Reuse Mandates

2.3.2. Stricter Industrial Wastewater Regulations

2.3.3. Advancements in Energy-Efficient RO Systems

2.3.4. Demand for Advanced Contaminant Removal

3. Recent Developments and Strategic Shifts

3.1. Market Trend: Sustainability and Digitalization

3.1.1. DuPont Receives BIG Sustainability Award for FilmTec™ Fortilife™

3.1.2. Asahi Kasei Earns Gold EcoVadis Rating

3.1.3. DuPont Launches WAVE PRO Digital Optimization Tool

3.2. Market Opportunity: Large-Scale Project Execution

3.2.1. Toray Supplies Membranes for Saudi Arabia’s Shuaibah 3 IWP

3.2.2. SUEZ Commissions China’s Largest Industrial Desalination Plant

3.3. Corporate Strategy: Acquisitions and Divestments

3.3.1. LG Chem Exits Water Solutions Business

3.3.2. Asahi Kasei Expands into Renewable Energy with Membranes

4. Competitive Landscape: Leading Companies

4.1. Market Overview: Technological Innovation and Strategic Realignment

4.2. Key Competitive Factors

4.2.1. Fouling Resistance and Operational Efficiency

4.2.2. Global Project Portfolio and Technical Support

4.2.3. R&D in New Materials and Digital Solutions

4.3. Profiles of Top Players

4.3.1. DuPont Water Solutions

4.3.2. Toray Industries, Inc.

4.3.3. SUEZ (Veolia)

4.3.4. LG Chem (Divested Business to Glenwood PE)

4.3.5. Kovalus Separation Solutions (formerly Koch Separation Solutions)

5. Wastewater Reverse Osmosis Membrane Market – Segmentation Insights

5.1. By Membrane Type

5.1.1. Low Fouling Membranes

5.1.2. Wastewater-Ready Brackish Water (BWRO) Membranes

5.1.3. High-Rejection Membranes

5.1.4. Chemically Tolerant Membranes

5.2. By Wastewater Source

5.2.1. Industrial Wastewater Treatment

5.2.2. Municipal Wastewater Reuse

5.3. By System Integration & Process

5.3.1. Integrated Membrane Systems (IMS)

5.3.2. Standalone RO Systems

6. Country Analysis and Outlook: Wastewater Reverse Osmosis Membrane Market

6.1. China: Regulatory Push and Industrial Adoption

6.2. Saudi Arabia: Desalination Infrastructure and Energy-Efficient RO Technologies

6.3. United States: Government Funding and Private Sector Innovation

6.4. India: Policy Support and Strategic Infrastructure Investments

6.5. Japan: Academic and Corporate Leadership in RO Membranes

6.6. Australia: Water Recycling and Advanced RO Research

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Wastewater Reverse Osmosis Membrane Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Membrane Type

7.1.2. By Wastewater Source

7.2. Europe Market Size Outlook to 2034

7.2.1. By Membrane Type

7.2.2. By Wastewater Source

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Membrane Type

7.3.2. By Wastewater Source

7.4. South America Market Size Outlook to 2034

7.4.1. By Membrane Type

7.4.2. By Wastewater Source

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Membrane Type

7.5.2. By Wastewater Source

8. Company Profiles: Additional Leading Players

8.1. DuPont de Nemours, Inc.

8.2. SUEZ

8.3. Veolia

8.4. Toray Industries, Inc.

8.5. Pentair plc

8.6. Xylem Inc.

8.7. Asahi Kasei Corporation

8.8. Kubota Corporation

8.9. LG Chem

8.10. The Dow Chemical Company

8.11. MANN+HUMMEL

8.12. Evoqua Water Technologies

8.13. Hydranautics (a Nitto Group Company)

8.14. Koch Industries

8.15. V.A. TECH WABAG Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures