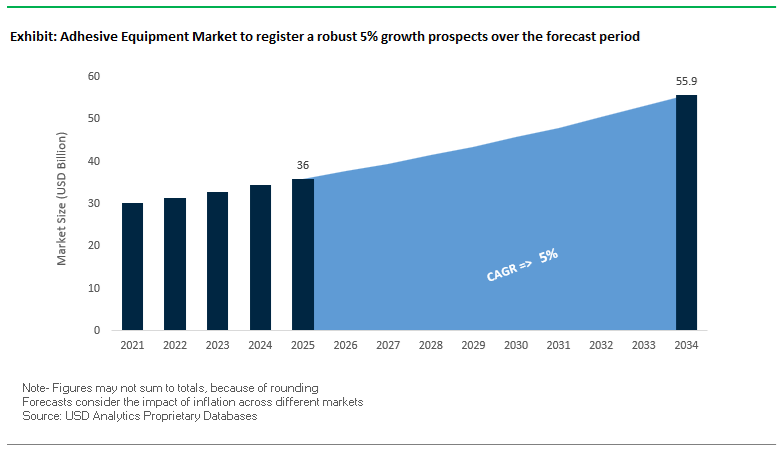

The Global Adhesive Equipment Market, valued at USD 36 billion in 2025 and projected to reach USD 55.8 billion by 2034 at a 5% CAGR, is expanding as adhesive application shifts from manual, operator-dependent processes to fully automated, digitally controlled dispensing architectures. Across automotive, EV battery assembly, electronics, packaging, construction, and industrial manufacturing, adhesive equipment is no longer peripheral machinery—it is a process-defining asset that directly governs bond integrity, material efficiency, line speed, and sustainability compliance.

Leading equipment manufacturers position modern adhesive systems as precision metering and motion-control platforms, capable of handling increasingly complex adhesive chemistries including hot melts, water-based systems, reactive PURs, UV-curables, and structural epoxies. As OEMs transition toward low-VOC, solvent-free, and high-performance adhesives, equipment must deliver tight temperature control, repeatable bead geometry, micro-volume accuracy, and closed-loop process stability at industrial cycle rates. This requirement is accelerating adoption of servo-driven pumps, all-electric hot melt units, non-contact jetting systems, and robotic dispensing cells, particularly in EV platforms and high-throughput packaging lines.

Automation is the dominant growth lever. Roughly 80% of new adhesive equipment demand is tied to automated or semi-automated dispensing, reflecting widespread integration with robotics, vision systems, PLCs, and MES platforms under Industry 4.0 frameworks. Equipment suppliers are embedding real-time sensors, flow monitoring, and predictive maintenance logic directly into dispensers and pumps, enabling manufacturers to reduce downtime, minimize adhesive waste, and maintain consistent bond quality across multi-shift operations. This digital convergence is especially critical in electronics, medical devices, and EV battery production, where adhesive deposition tolerances directly impact safety, thermal performance, and regulatory compliance.

Sustainability pressures are further reshaping equipment design priorities. The rapid shift toward water-based, bio-attributed, and UV-curable adhesives is forcing equipment OEMs to redesign fluid paths, sealing materials, and dosing architectures to handle lower viscosities, faster cure kinetics, and narrower process windows. In parallel, all-electric hot melt systems capable of delivering up to 75% adhesive savings are gaining traction in corrugated packaging and e-commerce fulfillment, where material efficiency and energy consumption directly affect operating margins.

The Adhesive Equipment Market has witnessed a surge in mergers, expansions, and product innovations as manufacturers align with global sustainability standards and automation trends. In July 2025, Graco Inc. completed the acquisition of Color Service S.r.l., a major supplier of precision dosing systems for powders and liquids. This acquisition reinforces Graco’s expertise in automated material handling and dosing technologies, extending its reach into high-precision adhesive and fluid applications.

Nordson Corporation and Nordson EFD showcased multiple innovations in October 2025, including new melt pump systems and integrated recycling technologies at a major global plastics exhibition—an indication of the company’s strong focus on supporting the circular economy through sustainable, high-throughput adhesive and polymer processing solutions. Similarly, Valco Melton, during the IndiaCorr Expo in September 2025, introduced advanced vision inspection and reversible gluing systems, marking a significant leap toward zero-defect corrugated production for major packaging clients.

In September 2025, Nordson Electronics Solutions enhanced its ASYMTEK Select Coat® platform by integrating actnano PFAS-free coatings, directly addressing environmental compliance requirements while offering precise conformal coating systems for electronics assembly. Earlier in April 2025, Graco Inc. unveiled a major upgrade to its QUANTM Electric Double Diaphragm Pump Line, integrating the new XTREME TORQUE™ (XT™) technology to improve power, efficiency, and control for high-viscosity adhesive applications.

Expansions also continue to reshape the industry landscape. Henkel Adhesives Technologies India completed Phase III of its manufacturing facility near Pune in July 2024, significantly boosting regional capacity for high-performance adhesives and driving parallel growth for complementary adhesive dispensing machinery. Meanwhile, INX Group Limited’s November 2024 acquisition of Coatings & Adhesives Corporation (C&A) reflects ongoing upstream consolidation that influences equipment demand for coating and adhesive applications.

Finally, Nordson Corporation’s October 2025 divestiture of select contract manufacturing products demonstrates its strategic shift toward proprietary precision adhesive dispensing technologies, reaffirming its dominance in the automated adhesive machinery domain.

A key technological revolution in the adhesive equipment market is the integration of Industry 4.0 technologies, enabling manufacturers to convert conventional dispensing tools into intelligent, connected systems. These next-generation systems leverage IoT sensors, real-time data analytics, and predictive maintenance algorithms to maximize uptime, optimize adhesive flow precision, and ensure quality consistency throughout production cycles.

Nordson EFD’s PICO® Nexμs™ Jetting System (2024) exemplifies the digital transformation. Designed for data-driven fluid dispensing, the system incorporates an intuitive web-based interface allowing remote programming, live monitoring of dispensing parameters such as pulse frequency and cycle time, and automatic data logging for performance validation. The integration of digital analytics ensures repeatable adhesive quality control, a critical feature for electronics, automotive, and aerospace manufacturing lines.

Similarly, Henkel Adhesive Technologies’ “Loctite Pulse” platform (2024) represents a paradigm shift in smart adhesive application. By embedding IIoT-based monitoring across rotating equipment, pipelines, and tanks, Henkel enables real-time leak detection and maintenance scheduling, cutting down unscheduled downtime and improving asset reliability. Henkel’s use of nano-sensors in adhesive dispensing units allows early detection of mechanical faults like blockages or blow-throughs, reinforcing predictive maintenance as a major operational advantage.

The connectivity-driven trend signifies the convergence of adhesives engineering and smart manufacturing. As data visibility and automation increase, adhesive equipment is becoming a central part of digital production networks, driving both operational efficiency and product traceability across global industrial supply chains.

The ongoing miniaturization of electronic components — from wearables and smartphones to EV battery modules and ADAS sensors — is accelerating the demand for compact, micro-precision adhesive dispensing systems. These systems must deliver ultra-fine, repeatable adhesive dots and lines with nanoliter accuracy, particularly in applications where component density and performance reliability are critical.

In the context, manufacturers like Musashi Engineering are advancing precision equipment such as the NANO MASTER series, featuring digital volume metering and high-speed control for nano-scale dispensing. The equipment ensures quantitative liquid discharge accuracy, crucial for applications in semiconductor packaging, microelectronic bonding, and optical module assembly.

Market reports highlight that the electronics sector requires micrometer-level accuracy for adhesive deposition — especially in EV battery assembly (fireproof coatings) and ADAS sensor bonding, where any adhesive inconsistency can cause heat buildup or structural defects. The precision trend is pushing equipment developers to adopt non-contact jetting systems and robotic control integration for higher throughput and zero contamination.

As wearable electronics, foldable devices, and IoT sensors proliferate, the need for ultra-precise, compact, and automated dispensing platforms is expected to rise sharply. These advancements not only enhance manufacturing flexibility but also reduce material waste, positioning micro-dispensing as a cornerstone of high-value electronics production.

One of the most promising frontiers for adhesive equipment manufacturers lies in solid-state battery production, where precision adhesive and sealing technologies are integral to safe and efficient assembly. As solid-state batteries (SSBs) transition from pilot-scale to gigafactory-scale production, the demand for equipment capable of applying thermal interface materials (TIMs), polymer electrolytes, and sealing adhesives with sub-millimeter accuracy is expanding rapidly.

Global investment in battery gigafactories continues to surge, with cumulative investment expected to exceed hundreds of billions of dollars by 2030. The exponential capacity expansion will require highly automated adhesive equipment for cell stacking, electrolyte layering, and housing sealing. According to technical studies on All-Solid-State Lithium Batteries (ASSLBs), challenges such as the brittleness of solid electrolytes and the need for low-resistance interfaces necessitate specialized precision dispensing systems to ensure material uniformity and prevent cell defects.

A 2022 case study from a Swiss solid-state battery startup further underscores the opportunity: the company’s CHF 246 million gigafactory investment emphasized the development of a multi-component adhesive ion conductor system — directly linking adhesive application technology with electrochemical performance. As OEMs and startups race to industrialize SSB production, the adhesive equipment sector will play a crucial enabling role in bridging material science and scalable automation.

The construction sector’s evolution toward prefabrication, modular building, and on-site precision bonding is creating substantial opportunities for portable adhesive dispensing systems. Contractors and field engineers are prioritizing battery-powered, ergonomic, and digitally controlled dispensers that offer high accuracy, reduced material waste, and faster curing times for structural silicones, polyurethanes, and MS polymer adhesives.

Hilti’s HDE 500-A12 cordless mortar dispenser has set a benchmark for on-site efficiency. The system enables milliliter-accurate dosing, minimizing mortar wastage while significantly improving installation speed and adhesive anchoring reliability. The aligns with the global shift toward sustainable and efficient job-site automation, where every gram of adhesive contributes to structural performance and cost optimization.

Leading sealant manufacturers like Sika are reinforcing the shift by promoting portable dispensing compatibility for products such as Sikaflex® elastic adhesives, which are replacing mechanical fasteners in both structural and non-structural applications. These materials require flexible yet high-performance equipment capable of handling diverse substrates like concrete, aluminum, and composite panels under variable field conditions.

The adoption of cordless and digitally optimized adhesive applicators not only enhances field efficiency but also supports the industry’s sustainability goals by cutting wastage, energy use, and rework frequency. As modular and prefabricated construction expands globally, the market for portable adhesive equipment is set to witness a multi-year acceleration.

Adhesive Equipment Market Share Insights, 2025-2034

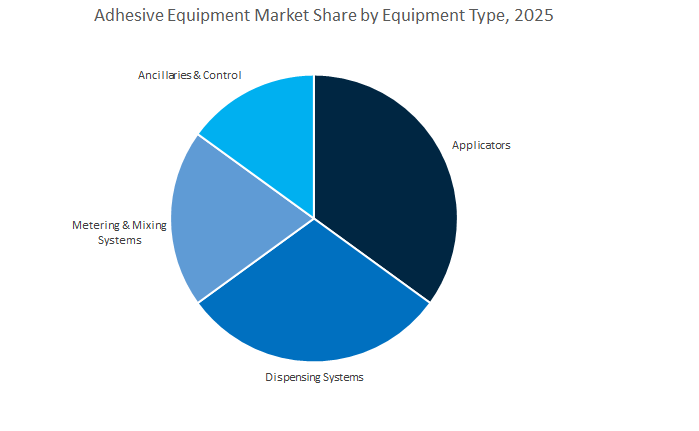

The applicators segment dominates the global adhesive equipment industry, accounting for approximately 35% of the total market share in 2025. This segment’s leadership is anchored in its essential role as the primary interface between adhesive technology and End-Use Industrys. Applicators are indispensable in high-volume production environments, where they deliver speed, consistency, and material efficiency. The widespread adoption of industrial hot melt applicators in packaging, paper converting, and disposable hygiene production—combined with cold glue systems for woodworking, labeling, and corrugated packaging—has solidified this category’s position. The segment also benefits from the ongoing trend toward automated and energy-efficient application systems, which reduce adhesive waste and downtime. Innovations such as precision nozzles, pattern control technology, and temperature-optimized designs are enhancing production line productivity and quality control. As industries prioritize throughput optimization and sustainable adhesive usage, applicators remain the central technology driving efficiency across mass-production sectors.

The dispensing systems segment, holding around 30% market share, is the fastest-growing category and represents the future of automation in adhesive application. These systems, which include robotic and automated dispensing cells, are increasingly deployed across automotive, electronics, and medical device manufacturing—industries where precision, repeatability, and controlled material flow are critical. Advanced dispensing technologies enable dot, bead, and spray pattern accuracy down to microliter levels, facilitating applications such as semiconductor encapsulation, PCB assembly, and EV battery potting. The shift toward Industry 4.0 and smart manufacturing is accelerating adoption, as integrated sensors and digital control interfaces allow real-time process monitoring and predictive maintenance. The ability of automated dispensing systems to reduce labor costs while improving product uniformity makes them a strategic investment for manufacturers pursuing lean, high-speed, and quality-assured production environments.

The metering and mixing systems segment plays a pivotal but smaller role within the global adhesive equipment market, serving high-performance applications that demand precision formulation control and material homogeneity. These systems are critical in industries utilizing two-component (2K) adhesives, such as epoxies, polyurethanes, and silicones—materials commonly used in aerospace composites, automotive structural bonding, and electronics encapsulation. Their importance has surged with the increasing adoption of reactive adhesive chemistries, which require accurate, on-demand mixing ratios to achieve consistent curing and bond strength. The growth of electric vehicles, wind turbines, and advanced composites is further amplifying demand for automated 2K dispensing and metering units. Technological advancements, including servo-driven pumps, volumetric dosing systems, and closed-loop control, ensure precision delivery and minimize waste, aligning perfectly with modern manufacturing’s sustainability and process reliability goals.

The packaging segment leads the global adhesive equipment market, commanding approximately 28% of total industry share in 2025. This dominance stems from the explosive growth in e-commerce, consumer goods packaging, and high-speed manufacturing lines. Adhesive equipment plays a central role in case sealing, carton closing, labeling, and flexible film lamination processes, where reliability, speed, and clean application are crucial. The transition toward sustainable and recyclable packaging materials has spurred innovation in energy-efficient hot melt applicators and cold glue systems designed for reduced adhesive waste and eco-friendly operations. Furthermore, the global rise of automated packaging lines and smart logistics is driving the integration of sensor-based dispensing systems that optimize adhesive usage per package. As consumer brands emphasize sustainability and speed-to-market, adhesive equipment suppliers are investing in AI-enabled control units and robotic applicators to meet the packaging industry’s evolving demands for precision and productivity.

The automotive and transportation segment, holding nearly 20% market share, represents a high-value, technology-intensive segment for adhesive equipment manufacturers. The automotive sector’s ongoing shift toward lightweight materials, electric vehicle assembly, and modular production architectures has elevated demand for precision dispensing and metering solutions. Adhesive equipment is fundamental in applications such as structural bonding, glass and trim assembly, battery potting, and thermal interface material (TIM) dispensing. As automakers increasingly replace mechanical fasteners with high-performance adhesives to improve safety, fuel efficiency, and design flexibility, automated adhesive application systems have become indispensable. Similarly, the aerospace and rail industries rely on advanced metering and mixing systems for composite bonding, insulation, and vibration damping. The adoption of robotic dispensing arms, closed-loop flow control, and AI-driven monitoring systems is further enhancing precision and throughput in these mission-critical industries.

The electronics and semiconductor segment continues to serve as a major growth driver, requiring micro-precision dispensing and controlled adhesive deposition for miniaturized assembly, conformal coating, underfill, and die-attach processes that ensure heat dissipation, shock absorption, and component stability. As semiconductor packaging, 5G systems, and consumer electronics trend toward denser, smaller architectures, manufacturers are deploying jet dispensing and laser-assisted curing technologies capable of sub-millimeter accuracy, with accelerating demand fueled by electric vehicles, wearables, and smart devices. Complementing this high-tech growth, the disposable hygiene products segment remains a stable, high-volume market reliant on high-speed hot melt adhesive systems for diapers, feminine hygiene items, and adult incontinence products, driving innovation in slot die applicators, fiberized spray systems, and melt-on-demand units that reduce waste and enhance product consistency. Meanwhile, the medical devices segment requires highly precise, sterile, and repeatable adhesive application equipment for syringes, catheters, diagnostic tools, and wearable monitors, reinforcing its position as a specialized but essential application

The competitive landscape of the Adhesive Equipment Market is defined by advanced automation, integration of Industry 4.0 capabilities, and strong R&D pipelines across global players such as Nordson Corporation, Graco Inc., Valco Melton, Dymax Corporation, and Robatech AG. These companies are continuously innovating in hot melt, cold glue, UV-curable, and electronic dispensing systems, catering to diverse industries including automotive, packaging, electronics, construction, and medical device manufacturing.

Nordson Corporation dominates the adhesive dispensing systems market, offering a broad portfolio under Nordson EFD and Nordson Adhesive Dispensing Systems. Its innovations—such as the VersaBlue II Melter and ProBlue Flex Melter with BBconn Controls—showcase its focus on precision, IoT connectivity, and high energy efficiency. The company invests heavily in the e-Mobility sector, developing solutions for EV battery assembly and thermal interface material (TIM) dispensing. Nordson’s MiniBlue II Hot Melt Applicator and ASYMTEK Select Coat conformal coating systems continue to set industry benchmarks for high-speed, reliable operations in packaging and electronics manufacturing.

Graco Inc. is a major force in industrial fluid handling and dispensing systems, offering solutions that move, measure, control, and apply high-viscosity and reactive adhesive materials. Its July 2025 acquisition of Color Service S.r.l. strengthened its automation capabilities in powder and liquid dosing. Graco’s relocation of key operations in May 2025 enhanced manufacturing efficiency and global distribution capacity. With products like the QUANTM Electric Diaphragm Pump line, Graco emphasizes energy efficiency and power optimization for automotive, construction, and industrial adhesive applications.

Valco Melton specializes in automated adhesive dispensing and quality assurance systems, serving corrugated, packaging, and graphic arts sectors. Its EcoStitch electric hot melt system—launched in August 2025—is designed to cut adhesive use by up to 70% and reduce downtime. The company’s Kube Zero melt-on-demand system and ClearVision inspection platforms ensure zero-defect carton production. Valco Melton’s patented reversible contact gluing solutions enable rapid production changeovers, addressing modern manufacturers’ demand for flexible and efficient adhesive application systems.

Dymax Corporation stands out for its integrated approach—offering both UV-curable adhesives and specialized dispensing and curing equipment. Its product range includes precision volumetric dispensers, UV spot curing systems, and LED UV curing conveyors, optimized for electronics and medical device manufacturing. Dymax’s ongoing innovations in low-heat LED curing systems deliver energy efficiency and fast curing cycles, enabling manufacturers to streamline operations while maintaining high bond integrity. The company’s process integration expertise ensures synchronized adhesive application and curing, crucial for high-speed production lines.

Robatech AG is renowned for its eco-efficient adhesive equipment, offering a wide range of hot melt and cold glue systems. Its GreenLine melters minimize energy use and adhesive degradation, aligning with global sustainability standards. Robatech’s modular system architecture and intuitive controls simplify maintenance and process adaptation. With a strong international service network, the company supports diverse industries—from packaging and nonwovens to product assembly—emphasizing precision, energy savings, and operational reliability across all equipment lines.

China continues to dominate as the Asia-Pacific hub for adhesive equipment manufacturing and automation, underpinned by the nation’s strong industrial policy and global leadership in electronics, robotics, and EV manufacturing. The government’s “Made in China 2025” strategy remains the cornerstone of industrial advancement, driving widespread adoption of smart, automated adhesive dispensing and dosing systems across production lines. China accounts for over half of all global industrial robot installations, and The unprecedented level of automation has created enormous demand for high-speed, precision-controlled adhesive application solutions for electronics, automotive, and packaging sectors.

In the rapidly growing EV battery segment, multi-billion-dollar investments in battery Gigafactories have intensified the need for thermal interface material (TIM) dispensing and structural bonding systems, ensuring accurate potting and cell encapsulation at scale. Domestic suppliers are increasingly developing cost-efficient automation technologies, reducing dependency on imports for precision adhesive dispensing equipment.

The boom in e-commerce packaging continues to drive upgrades in hot-melt spray and bead applicators for corrugated box manufacturing and flexible packaging lines. Simultaneously, state-backed semiconductor expansion—part of China’s strategic tech independence plan—is generating robust demand for ultra-high-precision die-attach, underfill, and micro-volume dispensing equipment. As a result, China is transitioning from a large-scale manufacturing hub to a global leader in adhesive equipment innovation, automation, and precision engineering.

Germany’s adhesive equipment industry exemplifies Industry 4.0 integration, combining precision engineering with digital transformation. The nation’s Industry 4.0 national strategy has accelerated the adoption of IoT-enabled adhesive dispensing systems that offer real-time process monitoring, predictive maintenance, and automated quality control. German manufacturers are pioneering digitalized production ecosystems where adhesive application machinery is networked with analytics platforms to improve material efficiency and reduce downtime.

In the automotive sector, leading OEMs are transitioning to lightweight multi-material structures that require advanced metering and mixing equipment for epoxy, polyurethane, and acrylic adhesives. Government programs supporting SME digitalization are boosting the uptake of robotic and pneumatic adhesive dispensing systems among mid-sized manufacturers, modernizing production floors nationwide.

Germany’s strict environmental regulations under EU REACH are also driving innovation in eco-compliant equipment designed to process high-viscosity, bio-based, or low-VOC adhesive formulations. Meanwhile, the aerospace industry’s focus on structural bonding demands precision-engineered epoxy dispensing equipment validated for critical components. Leading firms are introducing digital twin technology to simulate adhesive application scenarios before production, significantly enhancing process reliability and operational efficiency. The synergy of sustainability, digitalization, and engineering makes Germany the epicenter of intelligent adhesive machinery in Europe.

The United States adhesive equipment market is witnessing unprecedented technological evolution, driven by investments in aerospace, defense, semiconductors, and electric vehicle manufacturing. The surge in aerospace contracts continues to generate robust demand for two-component (2K) epoxy and polyurethane dispensing systems, critical for assembling airframes, satellites, and missile systems where microgram-level accuracy is essential.

Simultaneously, the CHIPS and Science Act has catalyzed over $50 billion in semiconductor manufacturing investments, fueling the expansion of high-precision liquid dispensing systems for photoresist coating, die-attach, and microelectronic packaging. In the automotive sector, next-generation EV platforms are integrating specialized sealing and potting systems for battery packs, adhesives, and gap fillers used in thermal management and structural bonding.

U.S.-based adhesive equipment manufacturers are channeling R&D into proprietary valve technology and automated controller systems that enhance accuracy, repeatability, and material flow consistency. Moreover, the booming e-commerce and packaging sector continues to adopt advanced hot-melt adhesive systems capable of high-speed application with real-time pattern control. The medical device manufacturing sector, governed by stringent FDA standards, is expanding its use of validated low-volume micro-dispensing systems for precision bonding in catheters and microfluidic assemblies.

India’s adhesive equipment market is experiencing rapid expansion fueled by infrastructure megaprojects, industrial localization, and the e-commerce packaging boom. The government’s focus on smart cities, metro systems, and national infrastructure development is generating immense demand for rugged, high-capacity adhesive and sealant dispensing equipment used in large-scale construction and waterproofing applications.

The “Make in India” initiative is accelerating industrial equipment adoption across automotive and electronics manufacturing, encouraging domestic producers to install automated and semi-automated adhesive assembly systems for local component manufacturing. Meanwhile, India’s packaging industry, driven by FMCG growth and e-commerce logistics, is a major consumer of cost-effective hot-melt and cold-glue dispensing equipment optimized for continuous, high-speed production lines.

In addition, the furniture and woodworking sectors are transitioning toward automated lamination and edge-banding systems, enhancing production efficiency and product consistency. The electronics assembly sector, especially in mobile and consumer device manufacturing, is adopting imported precision dispensing and curing units for display and circuit assembly. Backed by state-level subsidies and fiscal incentives, India is rapidly becoming a competitive hub for adhesive machinery manufacturing and technology adoption in emerging markets.

South Korea’s adhesive equipment industry is advancing in lockstep with its global dominance in display, semiconductor, and electric vehicle technologies. The nation’s leadership in OLED and flexible display production has spurred high-volume demand for optically clear adhesive (OCA) dispensing and laminating equipment, capable of micron-level precision to ensure bubble-free bonding and optical clarity.

As labor costs rise, South Korea’s manufacturing ecosystem has embraced fully automated robot-integrated adhesive application systems for electronics, automotive components, and high-end consumer goods. Major domestic conglomerates are investing in EV battery production, leading to substantial capital expenditure on precision gasketing, sealing, and thermal interface material dispensing systems that enhance performance and safety in energy storage systems.

The semiconductor packaging segment, especially in Fan-Out Wafer-Level Packaging (FOWLP), demands sub-micron dispensing systems for underfill and encapsulation processes. Continuous corporate R&D is also focused on machine vision-equipped intelligent dispensers capable of on-the-fly defect detection and automated process optimization. With such advancements, South Korea has established itself as a global benchmark for high-precision adhesive dispensing in electronics and energy manufacturing.

Japan’s adhesive equipment market reflects its core strengths in precision manufacturing, robotics, and materials engineering. The nation’s advanced industries—ranging from optics and micro-mechanics to automotive electronics—rely on ultra-precise micro-dispensing systems capable of sub-nanoliter adhesive application. The country’s robust industrial robotics sector continues to integrate adhesive dispensing heads directly into collaborative and high-speed robotic arms, significantly enhancing production flexibility and throughput in high-mix, low-volume manufacturing environments.

Continuous progress in UV-curable adhesives and fast-cycle dispensing systems supports Japan’s high-speed electronics production, minimizing downtime while improving assembly accuracy. The automotive sector is investing heavily in robotic structural adhesive systems for next-generation EVs and autonomous vehicle components, where reliability and precision bonding are paramount.

Collaborations between domestic adhesive manufacturers and equipment suppliers are fostering the development of integrated application systems for electrically conductive adhesives (ECAs), used in electronic interconnections and sensor assemblies. By combining robotics innovation, material science, and application precision, Japan maintains its status as a global leader in high-accuracy adhesive dispensing technologies.

Adhesive Equipment Market Report Scope

Adhesive Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$36 Billion

|

|

Market Size (2034)

|

$55.8 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Equipment Type (Applicators, Dispensing Systems, Metering & Mixing, Ancillaries & Control), By Technology (Hot Melt (HM), Cold Glue, Reactive, UV/LED Cure, Solvent-Based), By Automation Level (Fully Automated Systems, Semi-Automated Systems, Manual Systems), By End-use Industry (Packaging, Automotive & Transportation, Electronics & Semiconductor, Disposable Hygiene Products (DHP), Construction & Infrastructure, Woodworking & Furniture, Medical Devices, Non-Wovens & Technical Textiles), By Distribution Channel (Original Equipment Manufacturers (OEMs), Aftermarket/System Integrators

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nordson Corporation, Graco Inc., Illinois Tool Works Inc. (ITW) - ITW Dynatec, Robatech AG, Valco Melton, The Dover Corporation - Dymax Corporation, SAMES KREMLIN SAS, Dymax Corporation, Henkel AG & Co. KGaA (Equipment Unit), Sika AG (Equipment Systems), ViscoTec Pump and Dosing Technology GmbH, Delo Industrial Adhesives (Dosing Equipment), Glue Machinery Corporation, Kawasaki Heavy Industries, Ltd. (Robotics Division), Techcon Systems

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Equipment Type

- Applicators

- Dispensing Systems

- Metering & Mixing

- Ancillaries & Control

By Technology

- Hot Melt (HM)

- Cold Glue

- Reactive

- UV/LED Cure

- Solvent-Based

By Automation Level

- Fully Automated Systems

- Semi-Automated Systems

- Manual Systems

By End-use Industry

- Packaging

- Automotive & Transportation

- Electronics & Semiconductor

- Disposable Hygiene Products (DHP)

- Construction & Infrastructure

- Woodworking & Furniture

- Medical Devices

- Non-Wovens & Technical Textiles

By Distribution Channel

- Original Equipment Manufacturers (OEMs)

- Aftermarket/System Integrators

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Nordson Corporation

- Graco Inc.

- Illinois Tool Works Inc. (ITW) - ITW Dynatec

- Robatech AG

- Valco Melton

- The Dover Corporation - Dymax Corporation

- SAMES KREMLIN SAS

- Dymax Corporation

- Henkel AG & Co. KGaA (Equipment Unit)

- Sika AG (Equipment Systems)

- ViscoTec Pump and Dosing Technology GmbH

- Delo Industrial Adhesives (Dosing Equipment)

- Glue Machinery Corporation

- Kawasaki Heavy Industries, Ltd. (Robotics Division)

- Techcon Systems

*- List not Exhaustive

Research Coverage

This report investigates the global Adhesive Equipment Market as automation, Industry 4.0 connectivity, and eco-friendly chemistries reshape dispensing, metering, and curing on high-speed lines; it consolidates breakthroughs in closed-loop process control, micro-precision jetting, electric hot-melt platforms, and PFAS-free/low-VOC compatibility into decision-grade intelligence. Produced by USDAnalytics, the study delivers analysis reviews of capital spending patterns, uptime and yield levers, and spec-in strategies across EV battery assembly, corrugated packaging, electronics, and construction. It highlights how predictive maintenance, digital traceability, and energy-efficient melters shift total cost of ownership, benchmarking R&D intensity, cycle-time reduction, and adhesive savings for competitive advantage. By translating engineering KPIs into commercial outcomes, this report is an essential resource for operations leaders, process engineers, procurement teams, and OEMs aligning equipment roadmaps with sustainability, throughput, and quality-by-design objectives.

Scope Highlights

- By Equipment Type (Product): Applicators; Dispensing Systems; Metering & Mixing; Ancillaries & Control

- By Technology/Chemistry: Hot Melt (HM); Cold Glue; Reactive; UV/LED Cure; Solvent-Based

- By Automation Level: Fully Automated; Semi-Automated; Manual

- By Application/End-use: Packaging; Automotive & Transportation; Electronics & Semiconductor; Disposable Hygiene Products (DHP); Construction & Infrastructure; Woodworking & Furniture; Medical Devices; Non-Wovens & Technical Textiles

- By Distribution Channel: OEMs; Aftermarket/System Integrators

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic & Forecast Window: Historic data 2021–2024; forecasts 2025–2034.

- Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.