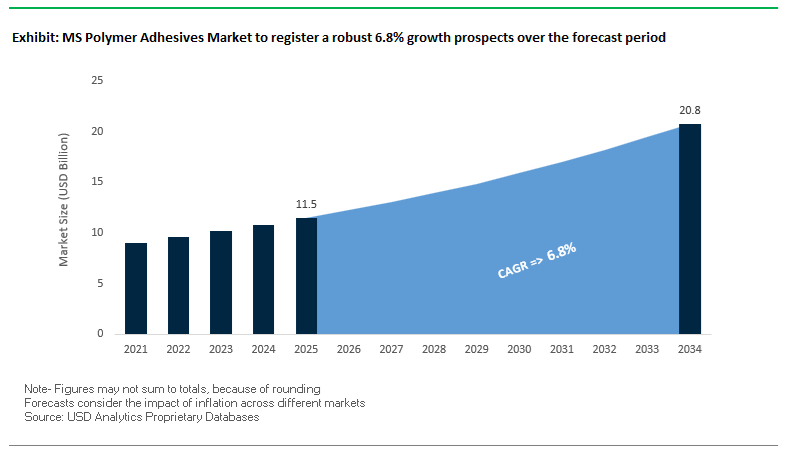

The Global MS Polymer Adhesives Market is projected to expand from USD 11.5 billion in 2025 to USD 20.8 billion by 2034, growing at a CAGR of 6.8%, as silyl-modified polymer (SMP) and silane-terminated polymer (STP) systems increasingly displace traditional polyurethanes and silicones across construction, automotive, marine, and electronics applications. Market growth is being driven less by marginal performance gains and more by regulatory pressure, installation reliability, and total cost of ownership, particularly in environments where VOC exposure, primer dependency, and rework risk carry high operational penalties.

MS Polymer adhesives are gaining specification preference because they remove multiple historical trade-offs associated with conventional chemistries. Their isocyanate-free and solvent-free formulations align with tightening VOC limits and worker-safety requirements under REACH and green building frameworks, while eliminating moisture sensitivity and yellowing issues common in polyurethane systems. In construction and facade engineering, manufacturers such as Sika, Bostik, and Tremco increasingly position MS Polymers as primerless solutions, reducing surface preparation steps and lowering labor variability in large-scale projects.

From a structural and mechanical standpoint, high elongation performance exceeding 100% allows MS Polymer adhesives to absorb movement and thermal cycling in curtain walls, flooring systems, and structural glazing, where differential expansion between substrates is unavoidable. This flexibility, combined with UV stability and long-term weather resistance from −40°C to +90°C, is reinforcing adoption in exterior envelopes and marine environments, where silicone was historically dominant. In parallel, high green strength and instant initial grab are gaining importance in modular and prefabricated construction, enabling vertical bonding and rapid assembly without prolonged clamping or secondary fixation.

Automotive and industrial assembly applications are contributing incremental momentum. As OEMs expand use of mixed material stacks—including coated metals, plastics, glass, and composites—primerless multi-substrate adhesion is increasingly valued to simplify process flows and reduce takt time sensitivity. MS Polymer adhesives’ compatibility with automated dispensing systems further supports their integration into modern production lines, particularly in EV assembly and electronics housings where elastic bonding and vibration damping are required alongside environmental compliance.

The global MS Polymer Adhesives industry is experiencing substantial advancements across manufacturing capacity expansion, acquisitions, sustainability initiatives, and product innovation. Leading companies strengthened their regional presence and invested heavily in R&D to meet surging demand from the construction, automotive, packaging, and marine sectors.

In August 2024, Sika AG completed the acquisition of Vinaldom S.A.S. in the Dominican Republic, expanding its market footprint across the Caribbean construction and industrial adhesives sector. This move aligns with Sika’s broader global strategy to integrate MS Polymer sealants and bonding technologies across emerging markets. In the same month, Sika also expanded its MS Polymer production capacity, citing a sharp rise in global demand for single-component SMP-based construction and industrial adhesives — especially in modular and prefabricated applications.

3M Company, in July 2024, launched a specialized automotive-grade MS Polymer adhesive engineered for multi-substrate bonding under chemical stress, marking a significant entry into high-performance automotive assembly adhesives. Earlier, Henkel AG had bolstered its North American manufacturing footprint (June 2022) through a new facility in Guadalupe, Mexico, enhancing production flexibility across its MS Polymer and hybrid adhesive lines.

H.B. Fuller, in July 2022, established a strategic partnership with Enimac SRL to support the expanding e-commerce packaging segment, leveraging MS Polymer adhesives’ superior strength and resilience for adhesive tapes and sealing applications. Similarly, Arkema Group (Bostik) announced in February 2022 its acquisition of Shanghai Zhiguan Polymer Materials (PMP), reinforcing its presence in engineering adhesives for electronics, where MS Polymer-based solutions play a crucial role in low-VOC, high-reliability assemblies.

Wacker Chemie AG, in October 2021, acquired a 60% stake in SICO Performance Material Co., Ltd., a silane manufacturer in Jining, China, securing vertical integration for silane feedstock critical to MS Polymer production. Shortly thereafter, in December 2021, Sika AG inaugurated its Pune Technology Center and Adhesives Plant in India, enhancing R&D and production for MS Polymer sealants and construction chemicals tailored to Asian market conditions.

Finally, Toyo-Morton Ltd. introduced its ECOAD solvent-free laminating adhesive range (August 2022), highlighting the global market’s collective pivot toward greener adhesive chemistries. While focused on polyurethane systems, the move mirrors the growing shift within the MS Polymer sector toward eco-friendly, non-solvent, and high-elasticity adhesives for industrial and consumer applications.

Market Trend 1: Accelerated Substitution of Polyurethane and Solvent-Based Systems in Construction

The transition toward low-VOC and isocyanate-free sealant systems represents one of the most transformative trends in the global construction adhesives market. The construction and civil engineering industries are increasingly specifying MS Polymer-based adhesives to replace traditional polyurethane (PU) and solvent-based formulations that face growing regulatory and performance limitations.

Comparative studies between PU and MS Polymer systems underscore the clear environmental and operational advantages of MS technology. Unlike PU systems that release CO₂ during curing and can cause bubbling in high-moisture environments, MS Polymers are solvent- and isocyanate-free, ensuring safer indoor application and compliance with Green Building Standards such as LEED and BREEAM. Their inherently low VOC content also supports the broader decarbonization and worker-safety initiatives in major construction economies.

Performance data further solidify the position of MS Polymers in long-term infrastructure applications. These adhesives exhibit superior UV, color, and weathering resistance, outperforming PU sealants in outdoor exposure tests. For movement-absorbing joints in precast concrete, MS Polymer formulations maintain modulus retention at up to 100% joint movement, offering enhanced resilience against temperature cycles and dynamic loads. As regulatory agencies tighten restrictions on hazardous materials and indoor emissions, MS Polymer adhesives are rapidly becoming the preferred choice for both structural and aesthetic bonding applications across residential, commercial, and industrial construction.

Market Trend 2: Formulation Advancements Supporting Lightweight Transportation Manufacturing

The growing adoption of electric vehicles (EVs), lightweight trains, and marine vessels is catalyzing the demand for MS Polymer adhesives in transportation assembly and sealing applications. These polymers enable bonding of dissimilar materials, such as aluminum to composites and painted metals to plastics, eliminating the need for mechanical fasteners and reducing overall vehicle weight.

The trend toward lightweighting for efficiency is underpinned by the superior performance profile of MS Polymers. They exhibit high tensile and shear strength, paintable surfaces, and outstanding vibration and creep resistance—attributes essential for maintaining structural integrity under fatigue loads. For example, MS Polymer-based adhesives are increasingly being used for bonding EV battery housings and body panels, where high strength and environmental sealing are critical.

From a production perspective, major chemical companies are expanding capacity to support the growing demand for silyl-terminated polymers (SMPs)—the chemical foundation of MS adhesives. In 2020, Evonik Industries AG announced a new multi-purpose silicone facility in Germany to produce SMPs used across roofing membranes, electronic encapsulation, and automotive assembly applications, including EV components. The expansion drives the market’s pivot toward high-performance hybrid adhesive systems designed to balance durability, environmental safety, and process efficiency in next-generation transportation platforms.

Market Opportunity 1: Capitalizing on Prefabricated and Modular Construction Growth

The global shift toward prefabricated and modular construction is unlocking new demand for MS Polymer adhesives that offer high initial bond strength, gap-filling capability, and rapid curing even under high humidity. These features make them ideal for factory-based, off-site construction, where fast assembly cycles and consistent quality are key success factors.

In modular housing and prefabricated infrastructure, MS Polymer sealants and adhesives are used extensively in bonding structural sandwich panels, bathroom pods, curtain walls, and interior fit-outs, offering primer-free adhesion to a variety of substrates including concrete, glass, aluminum, and composite laminates. Their ability to cure quickly upon exposure to moisture enhances productivity on the production floor, supporting high-speed assembly operations and standardized output critical for scalable modular construction.

The global construction sector, projected to surpass USD 14 trillion by 2030, is increasingly leveraging MS Polymers to meet low-emission and high-performance material standards. Their broad applicability—from waterproofing and window sealing to load-bearing joints in precast concrete—makes them integral to the industry’s transformation. With urbanization and sustainability at the forefront of infrastructure investment, MS Polymer adhesives are emerging as the benchmark technology for long-lasting, energy-efficient modular construction systems.

Market Opportunity 2: Infrastructure Rehabilitation and Retrofitting of Aging Public Assets

The mounting need for infrastructure rehabilitation and repair across developed and emerging economies presents one of the most lucrative long-term opportunities for MS Polymer adhesives and sealants. Governments worldwide are investing heavily in programs aimed at restoring aging bridges, tunnels, and public buildings, where polymer-based materials are increasingly specified for their durability, weathering resistance, and compatibility with reinforced concrete.

Research on advanced polymeric joint sealants, which share chemical similarities with MS Polymers, demonstrates superior resistance to UV exposure, alkali environments, and prolonged water immersion. These materials maintain bonding strength retention of up to 85% even after extreme durability tests—outperforming traditional asphaltic or silicone sealants that often suffer from cracking, debonding, or chemical degradation.

Global policy initiatives, such as the U.S. Infrastructure Investment and Jobs Act and EU Green Infrastructure Plan, emphasize the use of long-life, sustainable repair materials. MS Polymer-based systems are particularly valued for bridge deck sealing, façade refurbishment, and structural joint rehabilitation, where longevity and movement accommodation are critical to extending service life. Their adhesion versatility and corrosion resistance also make them ideal for parking structures, tunnels, and marine infrastructures, ensuring high-value, low-maintenance performance.

As public infrastructure modernization becomes a strategic national priority, MS Polymer adhesives and sealants are expected to play an essential role in civil engineering restoration and corrosion mitigation, supported by both government funding and sustainability-driven design mandates.

MS Polymer Adhesives Market Share Insights, 2025-2034

Market Share by Application

The sealants segment dominates the global MS polymer adhesives market, commanding a projected 53.9% share in 2025, owing to the material’s unmatched versatility, elasticity, and weather resistance across construction, automotive, and industrial applications. MS polymer sealants are increasingly preferred over conventional polyurethane and silicone sealants due to their isocyanate-free, solvent-free, and odorless formulations, aligning with global VOC emission regulations and green building standards. Their ability to adhere strongly to a wide range of substrates — including glass, metal, wood, and concrete — without primers gives them a technical advantage in façade sealing, window installation, roofing, and flooring joints. Additionally, their UV stability, paintability, and long-term durability make them ideal for external sealing applications, where performance under thermal cycling and exposure to weathering is critical. These features have led MS polymer sealants to become the material of choice for architectural façades, curtain walls, and waterproofing systems, particularly in Europe and Asia-Pacific where sustainable construction materials are prioritized.

The adhesives segment represents a substantial share of the MS polymer market, driven by its ability to form strong, vibration-resistant, and flexible bonds suitable for industrial, automotive, and marine assembly operations. Unlike reactive adhesives, MS polymer-based formulations cure via moisture without emitting VOCs or requiring heat, offering a unique balance of workability and structural strength. In the automotive and transportation sectors, these adhesives are being rapidly adopted for panel bonding, vehicle glazing, and component assembly, replacing conventional polyurethane due to their superior weathering and chemical resistance. The coatings segment plays a niche yet growing role in protective, waterproofing, and anti-corrosion applications. MS polymer-based coatings are valued for their elasticity, UV resistance, and strong adhesion to porous materials, making them effective in roof coatings, bridge protection, and industrial flooring systems.

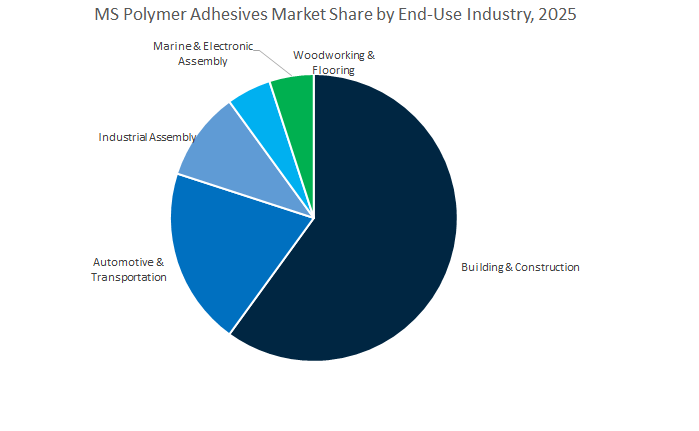

Market Share by End-Use Industry

The building and construction segment overwhelmingly leads the global MS polymer adhesives market, capturing a projected 61.9% share in 2025, driven by expanding infrastructure development, green building initiatives, and the shift toward low-VOC and solvent-free bonding solutions. MS polymer adhesives are integral to sealing expansion joints, bonding façade panels, waterproofing roofs, and installing glazing systems, offering a unique combination of high elasticity, UV resistance, and long-term weatherability. Their broad substrate compatibility enables usage across glass, aluminum, concrete, and stone, reducing material waste and simplifying on-site installation. The growing trend of modular and prefabricated construction has further accelerated adoption, as MS polymer adhesives facilitate fast-curing, flexible joints essential for transportable structures and high-rise buildings. Major regional growth drivers include rapid urbanization in Asia-Pacific and retrofit construction in Europe, where environmental compliance and performance reliability are top priorities.

The automotive and transportation industry represents the next largest segment, propelled by the need for lightweight, vibration-dampening, and corrosion-resistant bonding materials. MS polymers are increasingly used in direct glazing, interior panel bonding, and exterior sealing applications, offering OEMs improved performance and reduced processing complexity compared to polyurethane or silicone systems. In the industrial assembly and woodworking sectors, MS polymer adhesives have carved out strong positions for bonding dissimilar materials, providing gap-filling capacity, and maintaining durability under dynamic stress. These properties make them particularly useful in machinery, furniture, and appliance assembly. Additionally, marine and electronic assembly applications—though niche—are gaining traction due to the adhesives’ superior resistance to water, salt spray, and temperature fluctuations, making them ideal for boat construction, ship deck sealing, and electronic module encapsulation.

The MS Polymer Adhesives Market is moderately consolidated, led by Henkel AG & Co. KGaA, Sika AG, Wacker Chemie AG, Arkema Group (Bostik SA), H.B. Fuller Company, and 3M Company. These companies combine chemistry expertise, regional integration, and sustainability leadership to redefine adhesive performance across construction, automotive, marine, and industrial assembly.

Henkel offers an extensive range of one- and two-component MS Polymer adhesives and sealants under its Loctite and Pattex brands. With a strong focus on automotive assembly, facade sealing, and structural glazing, Henkel is integrating MS Polymer solutions into robotic and automated manufacturing lines. Its ongoing investments in dispensing and automation technologies ensure consistent bond integrity in high-volume production. The company continues to tailor MS Polymer formulations for OEM specifications, delivering flexible, durable, and environmentally compliant adhesive systems.

Sika AG is a market leader in SMP-based adhesives and sealants through its Sikaflex and Sikasil product lines. With the August 2024 acquisition of Vinaldom S.A.S., Sika reinforced its Caribbean footprint and expanded regional access to its MS Polymer technologies. Its product portfolio dominates construction applications such as roofing, flooring, facade joints, and marine bonding, offering superior UV stability and elasticity. Sika’s strategy revolves around regional production expansion and integration of MS Polymers into its Building Envelope and Industrial Solutions portfolio for accelerated global growth.

Wacker Chemie AG plays a foundational role in the MS Polymer value chain through its GENIOSIL silyl-terminated polyether (STPE) materials. The company’s 2021 acquisition of SICO Performance Materials provided vital silane feedstock security, strengthening cost control and production stability. Wacker’s latest R&D efforts focus on enhanced curing kinetics and tensile strength, enabling MS Polymer formulations with superior weathering and structural performance. As a technology enabler, Wacker partners with downstream formulators to co-develop high-performance, low-VOC adhesives for industrial and construction applications.

Under its Bostik division, Arkema delivers premium MS Polymer-based adhesive solutions under the Simson and Gripfil brands. Its R&D roadmap prioritizes bio-based and recycled content integration to support the circular economy transition. Arkema’s adhesives find strong adoption in transportation, rail, and wood flooring, where elasticity, low odor, and durability are critical. The company’s focus on low-migration and low-odor formulations also makes it a leading choice in indoor construction and sensitive electronics assembly applications.

H.B. Fuller continues to strengthen its MS Polymer adhesive portfolio with a focus on industrial assembly, white goods, and consumer applications. Its 2022 strategic partnership with Enimac SRL underscores a diversification strategy that includes e-commerce and packaging adhesives—a non-traditional but rapidly growing segment for MS Polymer technology. Fuller’s one-component adhesives are widely used for gap filling, filter bonding, and millwork, combining flexibility with water resistance. The company’s approach centers on expanding MS Polymer utility into electronics and advanced consumer goods manufacturing.

3M Company has successfully integrated MS Polymer chemistries into its diverse adhesive portfolio, focusing on multi-substrate bonding in automotive, aerospace, and electronics sectors. Its July 2024 automotive MS Polymer launch demonstrated superior chemical resistance and vibration damping, ideal for high-stress vehicle applications. By combining MS Polymer and acrylic adhesive science, 3M continues to push the boundaries of lightweight, low-VOC, and high-impact bonding systems, reinforcing its role as a frontrunner in innovation-driven adhesive solutions.

Country Analysis: Global MS Polymer Adhesives Industry

China: Expansion of Silane-Modified Polymer Production and EV Integration

China has emerged as the largest production and application hub for Silane-Modified Polymer (SMP) adhesives, leveraging its expanding EV manufacturing and construction infrastructure. The acquisition of a 60% stake in SICO Performance Material Co., Ltd by Wacker Chemie AG (October 2021) has strengthened China’s domestic capability in silane precursor production, a critical raw material for MS polymer adhesives. The investment directly supports the localization of high-performance SMP adhesives required in the electric vehicle (EV) battery pack assembly sector, where flexible, high-elongation polymer sealants enable efficient bonding of dissimilar substrates such as aluminum, composites, and thermoplastics.

In parallel, the Chinese façade and infrastructure market continues to drive high-volume consumption of low-modulus, weather-resistant MS polymer sealants used in curtain wall, structural glazing, and waterproof joint applications. Local producers like Guangzhou Baiyun Chemical are increasing output capacity to meet The demands, while regulatory focus on VOC reduction and sustainable building materials further accelerates the transition away from solvent-based sealants. China’s simultaneous expansion in EV manufacturing and construction megaprojects ensures continued dominance in both production and end-use innovation for moisture-cured silane-modified polymers.

Germany: Automotive Lightweighting and Advanced Low-VOC Formulations

Germany remains the technological nucleus of the European MS Polymer Adhesives Market, with deep expertise in automotive lightweighting, high-performance hybrid bonding, and REACH-compliant chemistry. German manufacturers are pioneering primerless, fast-curing MS polymer adhesives engineered for robotic automotive assembly lines, offering excellent tensile strength and tack-free properties crucial for structural bonding in next-generation vehicles. The advanced formulations are integral to the electrification of the automotive sector, supporting hybrid bonding between metals, composites, and engineered plastics used in EV architectures.

The nation’s strict compliance with REACH regulations and Blue Angel eco-label standards continues to push the envelope for ultra-low VOC and solvent-free SMP technologies, phasing out conventional solvent-based adhesives in construction and transportation. Moreover, German adhesive companies are investing heavily in flame-retardant MS polymer systems, exemplified by Bostik’s Simson ISR line, which meets EN 45545 HL3 fire safety requirements for trains and public transport interiors. The convergence of lightweighting, automation, and environmental responsibility cements Germany’s leadership in the European market for high-performance silane-based adhesive technologies.

United States: Green Building Expansion and Bio-Based Polymer R&D

The United States MS Polymer Adhesives Industry is witnessing accelerated adoption across construction, transportation, and sustainable product design, driven by green building mandates and R&D in bio-based silane chemistries. Regulations under California Air Resources Board (CARB) and LEED certification frameworks are pushing the replacement of isocyanate-containing sealants with non-toxic, hybrid SMP formulations. The adhesive systems provide superior weatherability, elasticity, and crack-bridging performance, making them ideal for architectural façades, window assemblies, and flooring systems.

Leading American manufacturers are channeling significant R&D toward bio-based MS polymer adhesives that reduce reliance on petrochemical feedstocks, aligning with corporate net-zero sustainability goals. Innovation in low-viscosity hybrid polymers enables seamless adhesion to porous materials like concrete, wood, and gypsum, supporting large-format tile installations and acoustic floor systems. Furthermore, U.S. research in solvent-free hybrid SMP adhesives underscores a shift toward eco-friendly industrial bonding solutions, reflecting a broader trend in sustainable manufacturing and high-performance green construction.

India: Infrastructure Modernization and Local Manufacturing Expansion

India’s MS Polymer Adhesives market is undergoing rapid transformation, underpinned by infrastructure expansion, automotive localization, and smart city development. The establishment of Sika AG’s technology center and manufacturing plant in Pune (December 2021) marked a pivotal step in scaling domestic production of SMP adhesives, reducing reliance on imports and enabling cost-effective supply for construction and industrial assembly sectors.

Government-led initiatives such as the Smart Cities Mission and National Infrastructure Pipeline (NIP) are driving demand for long-lasting, weatherproof MS polymer sealants in bridge construction, concrete expansion joints, and highway repair projects. The growing emphasis on low-VOC and solvent-free materials in urban building codes is also catalyzing adoption of MS polymer window and door frame sealants, which offer superior UV resistance, flexibility, and paintability compared to traditional silicone or polyurethane-based products. The combination of industrial modernization and policy-driven sustainability positions India as a key emerging hub for MS polymer adhesive manufacturing in Asia.

Brazil: Strategic Acquisitions and Wet-Condition Bonding Innovation

Brazil is quickly becoming a focal point for hybrid MS polymer adhesives and sealants, particularly within construction and woodworking applications. The acquisition of Poliplas by Arkema’s Bostik division in February 2021 exemplifies the strategic expansion of global chemical companies into Brazil’s fast-growing hybrid-technology adhesive market. The acquisition enhances Bostik’s regional manufacturing capacity and strengthens its position in moisture-curing, solvent-free sealant solutions.

A key growth area lies in parquet and engineered wood flooring installation, where high-tack hybrid MS polymer adhesives are gaining prominence for their ability to bond to damp or uneven substrates without primer—an essential advantage in Brazil’s humid climate. Local manufacturers are increasingly developing moisture-resistant, fast-curing SMP sealants to meet The conditions, addressing construction challenges in coastal and tropical environments. As infrastructure investments and housing projects expand, Brazil is emerging as a strategic Latin American market for next-generation environmentally compliant MS polymer adhesives.

Japan: Pioneer in Silane-Terminated Polymer Technology and Seismic Applications

Japan holds a historic and technological edge in the MS Polymer Adhesives industry, being the originator of Silane-Terminated Polymer (STP) technology through Kaneka Corporation. The country continues to lead in the development of high-durability SMP formulations designed for solar panel sealing, weatherproofing, and earthquake-resistant construction. The high-elasticity sealants play a crucial role in absorbing seismic stress, ensuring long-term waterproof integrity for critical infrastructure in earthquake-prone regions.

The market also demonstrates strong innovation in aesthetic and high-transparency SMP adhesives, ideal for structural glass bonding and decorative architectural applications. Japanese manufacturers’ R&D programs are advancing UV-resistant, non-yellowing MS polymer technologies with superior optical clarity, targeting applications in interior design, photovoltaic assembly, and high-end residential construction. The intersection of durability, precision, and sustainability makes Japan a global benchmark for premium silane-based polymer adhesive systems.

France: Flame-Retardant SMP Sealants for Transportation Safety

France’s MS Polymer Adhesives market is heavily influenced by stringent transportation safety regulations, particularly within the rail and aerospace sectors. Major chemical manufacturers, led by Arkema (Bostik), are pioneering flame-retardant (FR) SMP sealants that meet the EN 45545-2 HL3 standard—a mandatory certification for materials used in railcar interiors and structural bonding. The innovative adhesives offer low smoke density, non-toxic emission characteristics, and superior mechanical adhesion, ensuring compliance with Europe’s most rigorous passenger safety standards.

Beyond transportation, French adhesive research focuses on eco-friendly hybrid formulations designed for marine, construction, and defense applications. With Arkema’s broader commitment to sustainable specialty materials and bio-based innovation, the French market is setting a new standard in high-performance, safety-certified MS polymer adhesives, bridging performance, environmental responsibility, and advanced engineering.

MS Polymer Adhesives Market Report Scope

MS Polymer Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.5 Billion

|

|

Market Size (2034)

|

$20.8 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Chemical Composition (Polyurethane, Silane-Terminated Polymers, Cyanoacrylate, Polyolefin), By Product Type (One-Component, Two-Component), By Technology (Reactive Hot-Melt Polyurethane, Liquid Adhesives, Water-Borne Dispersions), By End-Use Industry (Building & Construction, Automotive & Transportation, Woodworking & Furniture, Flexible Packaging & Lamination, Electronics & Electrical, Footwear & Textile, Aerospace & Defense, Medical Devices), By Substrate (Metals, Plastics & Composites, Wood & Engineered Wood, Glass, Paper & Paperboard

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Dow Inc., Arkema Group (Bostik S.A.), 3M Company, Wacker Chemie AG, Huntsman International LLC, BASF SE, Shin-Etsu Chemical Co., Ltd., Covestro AG, Jowat SE, Nan Pao Resins Chemical Group, Selena Group, Soudal N.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemical Composition

- Polyurethane

- Silane-Terminated Polymers

- Cyanoacrylate

- Polyolefin

By Product Type

- One-Component

- Two-Component

By Technology

- Reactive Hot-Melt Polyurethane

- Liquid Adhesives

- Water-Borne Dispersions

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Woodworking & Furniture

- Flexible Packaging & Lamination

- Electronics & Electrical

- Footwear & Textile

- Aerospace & Defense

- Medical Devices

By Substrate

- Metals

- Plastics & Composites

- Wood & Engineered Wood

- Glass

- Paper & Paperboard

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies MS Polymer Adhesives Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Dow Inc.

- Arkema Group (Bostik S.A.)

- 3M Company

- Wacker Chemie AG

- Huntsman International LLC

- BASF SE

- Shin-Etsu Chemical Co., Ltd.

- Covestro AG

- Jowat SE

- Nan Pao Resins Chemical Group

- Selena Group

- Soudal N.V.

*- List not Exhaustive

Research Coverage

This report investigates the MS Polymer Adhesives Market through decision-grade competitive intelligence and end-use mapping, delivers analysis reviews on demand catalysts from modular construction to EV assembly, and curates breakthroughs in silyl-terminated/silane-modified polymer chemistries that enable primerless, isocyanate-free, low-VOC bonding across metals, glass, plastics, wood, and composites; it highlights cure kinetics, elongation/green-strength benchmarks, durability in UV/temperature extremes, and automation-ready dispensing that reduce cycle time and total cost of ownership; developed by USDAnalytics, this report is an essential resource for product managers, sourcing leaders, application engineers, and investors seeking route-to-market clarity, regulatory alignment, and defensible country-level forecasts in a rapidly evolving SMP/STP adhesives landscape.

Scope Highlights

Segmentation:

- By Chemical Composition: Polyurethane; Silane-Terminated Polymers; Cyanoacrylate; Polyolefin.

- By Product Type: One-Component; Two-Component.

- By Technology: Reactive Hot-Melt Polyurethane; Liquid Adhesives; Water-Borne Dispersions.

- By End-Use Industry: Building & Construction; Automotive & Transportation; Woodworking & Furniture; Flexible Packaging & Lamination; Electronics & Electrical; Footwear & Textile; Aerospace & Defense; Medical Devices.

- By Substrate: Metals; Plastics & Composites; Wood & Engineered Wood; Glass; Paper & Paperboard.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies (strategies, portfolios, recent moves, and SWOT-style takeaways).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.