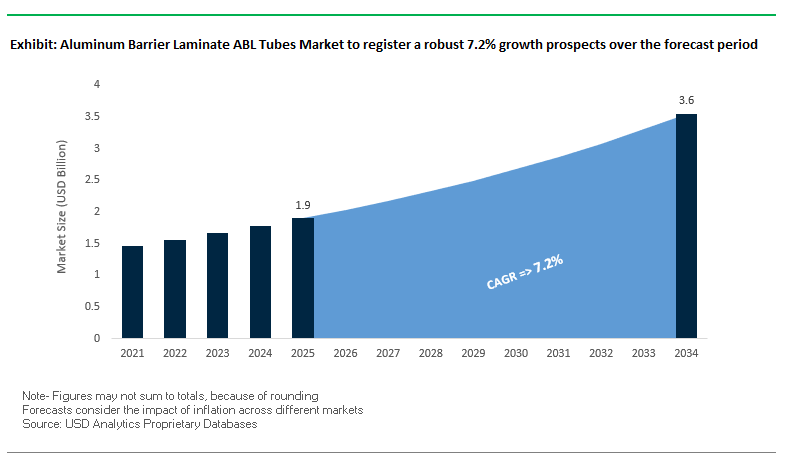

The Global Aluminum Barrier Laminate (ABL) Tubes Market is projected to grow from $1.9 billion in 2025 to $3.6 billion by 2034, at a CAGR of 7.2%. ABL tubes are indispensable in industries where product integrity is paramount, especially in oral care, pharmaceuticals, cosmetics, and food. Their ability to provide superior barrier protection against oxygen, moisture, and UV light makes them the preferred choice for sensitive formulations, while their adaptability to premium branding and decorative finishes strengthens consumer appeal.

The ABL tubes industry has seen strong activity in sustainability, innovation, and M&A consolidation across 2024–2025. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, strengthening its capabilities in Latin America’s fast-growing medical packaging sector. Similarly, Constantia Flexibles (August 2025) announced a €100 million investment to upgrade its global facilities, reinforcing its portfolio of high-barrier laminates and sustainable ABL tube solutions.

On the innovation front, Albéa (February 2025) introduced EcoTop lightweight caps, reducing plastic weight by up to 75%, showcasing the industry’s shift to eco-efficient designs. Earlier in January 2025, Constantia Flexibles won two WorldStar Global Packaging Awards for its EcoPeelCover and EcoLamHighPlus solutions, emphasizing its leadership in sustainability. At the same time, Neopac was recognized for its Polyfoil® Mono-Material Barrier Tube, a recyclable solution with high-barrier properties.

Sustainability credentials were further highlighted when Huhtamaki (July 2025) earned an EcoVadis gold medal for the fifth consecutive year, reinforcing its position as a global leader in responsible packaging. Meanwhile, leadership realignments such as Constantia Flexibles’ CEO appointment in November 2024 underscored the industry’s focus on long-term innovation and operational excellence. Although M&A activity slowed in late 2024, megadeals like Amcor’s acquisition of Berry Global (2024–2025) reaffirmed the appetite for consolidation in high-growth packaging segments.

Premium cosmetic and pharmaceutical brands are increasingly adopting aluminum barrier laminate (ABL) tubes to ensure superior product protection against oxygen, moisture, and light. In the pharmaceutical sector, which accounts for nearly 25% of ABL tube consumption, these tubes are essential for maintaining the efficacy and safety of medicinal creams, gels, and ointments. Sensitive active ingredients like retinoids, Vitamin C, and peptides in cosmetics also benefit from ABL tubes’ airtight, light-blocking properties, which preserve potency and extend shelf life. The superior barrier offered by ABL tubes aligns with strict regulatory compliance requirements, including tamper-evident sealing and hygiene standards, making these tubes a preferred choice for high-value, safety-critical products. This trend is driving market growth as brands focus on delivering quality, efficacy, and trust to discerning consumers.

ABL tube manufacturers are engineering thinner, lighter laminate structures without compromising barrier performance, responding to both cost pressures and sustainability mandates. Innovations like EPL’s “Titanium” laminate, which utilizes HDPE foils, reduce tube thickness and overall carbon footprint. Lightweight caps and shoulders further contribute to material savings while maintaining product integrity. This focus on lightweighting balances performance and sustainability, helping brands meet environmental goals while ensuring high-barrier protection against oxygen, moisture, and UV light. The combination of advanced laminate engineering and reduced material usage positions ABL tubes as both eco-friendly and premium packaging solutions.

A key opportunity in the ABL tube market lies in developing fully recyclable, mono-material tubes that replicate the high-barrier performance of traditional multi-layer laminates. Leading packaging companies, such as Mondi Group, are pioneering mono-material solutions certified recyclable under cyclos-HTP standards. Neopac’s Polyfoil® MMB demonstrates the ability to combine a HDPE structure with a high-performance EVOH barrier, achieving oxygen and moisture resistance while enabling end-of-life recyclability. This innovation aligns with global circular economy goals and regulatory pressures, addressing sustainability concerns and meeting the growing demand for environmentally responsible packaging. The development of recyclable ABL tubes represents a strategic advantage for brands seeking to enhance both compliance and consumer appeal.

Embedding smart technology, such as NFC chips or QR codes, directly into ABL tubes presents significant growth opportunities. These features provide anti-counterfeiting solutions, enabling consumers to verify product authenticity via smartphone scans, and creating secure, offline authentication methods. Smart packaging also enhances consumer engagement by offering interactive experiences, including product tutorials, ingredient information, and recycling instructions. Pharmaceutical brands particularly benefit from integrated track-and-trace capabilities, ensuring supply chain transparency and optimized logistics. This integration of digital technology transforms ABL tubes into value-added packaging solutions, providing measurable benefits in consumer trust, brand loyalty, and operational efficiency.

The competitive environment is shaped by five global leaders, each leveraging sustainability, innovation, and design expertise to maintain dominance in the ABL tubes market.

Albéa is a leading producer of ABL tubes for oral care, cosmetics, and pharma. The company’s EcoFusion Top and EcoTop lightweight caps exemplify its innovation in weight reduction and recyclability. Albéa’s commitment is to make all its tubes recyclable by 2025, supported by 23 manufacturing sites across 14 countries. Its global-local model ensures supply chain efficiency for multinational brands.

Huhtamaki provides a comprehensive range of oral care laminates and flexible packaging with recycling-ready PE-based barrier tubes. Its re/cycle Functional Barrier Papers demonstrate innovation in replacing plastics with fiber-based alternatives. The company’s consistent recognition, including an EcoVadis gold medal (July 2025), highlights its leadership in sustainability.

Constantia Flexibles is a pioneer in high-barrier laminates essential for ABL tubes used in pharma and oral care. Its award-winning EcoPeelCover and EcoLamHighPlus (January 2025) underline its leadership in sustainable solutions. With an August 2025 €100 million expansion, Constantia is strategically positioning itself as a top innovator in eco-friendly tube laminates.

Neopac specializes in premium ABL tubes for pharmaceuticals, cosmetics, and dental care. Its proprietary Polyfoil® tubes provide superior protection from air, light, and moisture. Recognized with a WorldStar Award (January 2025) for its recyclable Polyfoil® Mono-Material Tube, Neopac leads in sustainable innovation while maintaining a strong focus on high-performance, child-resistant designs.

Amcor is a leading global supplier of ABL tubes, strengthened by its acquisition of Berry Global (2024–2025). With over 40-country presence, Amcor integrates sustainability with scale, offering recyclable, reusable, and compostable tube solutions. Its strategy emphasizes circular economy leadership, making it a key partner for both global and regional consumer brands

Oral care accounts for approximately 40% of the aluminum barrier laminate tubes industry, making it the single largest end-use sector. This dominance is directly tied to the global toothpaste market, where ABL tubes are the undisputed standard due to their superior protection of active ingredients like fluoride, triclosan, and herbal actives against oxygen and moisture ingress. With over 5 billion toothpaste units sold annually worldwide, the scale of oral care demand alone secures ABL’s leadership position. Furthermore, collapsibility ensures efficient dispensing, while high-quality surface printing supports strong brand visibility on crowded retail shelves. Regulatory compliance also plays a central role oral care formulations must maintain stability across global climates, from humid Asia-Pacific to arid Middle East regions, making ABL the most technically reliable option. Continuous investments in recyclable and thinner-gauge laminates further reinforce this segment’s entrenched dominance.

The 50–100 ml capacity segment represents nearly half of the ABL tubes market, reflecting its role as the industry standard across oral care, pharmaceuticals, and personal care. This range is optimized for consumer use large enough to hold a month’s supply of toothpaste or cream, yet compact enough for convenience and portability. In oral care, the standard 75 ml toothpaste tube anchors this segment’s volume, while in pharmaceuticals, topical ointments and dermatological gels are most frequently packaged in 50–100 ml formats. The economics are also decisive: this size range minimizes per-unit material cost while maximizing production line efficiency on high-speed filling machines. Sustainability trends are accelerating demand for lighter laminates within this capacity band, ensuring it remains the workhorse size range of the ABL tubes market.

The U.S. aluminum barrier laminate (ABL) tubes market is witnessing rapid evolution driven by stringent regulations, sustainability trends, and advanced packaging technologies. States such as California are implementing laws like the Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54), which encourages a shift toward recyclable and reusable ABL tube solutions. Sustainability initiatives are gaining momentum, supported by the U.S. Department of Energy, which has allocated over $52 million toward the development of cellulose-based films as next-generation alternatives to traditional ABL laminates.

Technological advancements in multilayer barrier films are enhancing protection against oxygen, light, and moisture, extending the shelf life of sensitive pharmaceutical ointments and premium cosmetic products. Key applications are heavily driven by the pharmaceutical sector, with rising demand for portable, user-friendly packaging for home-based treatments. Furthermore, EPA regulations targeting PFAS in packaging are compelling manufacturers to reformulate grease-resistant papers and other food-contact materials, strengthening the trend toward environmentally responsible ABL tube solutions.

Germany’s ABL tubes industry is strongly influenced by a stringent regulatory landscape, including the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025. These regulations are pushing for eco-friendly, fully recyclable packaging, which aligns with Germany’s leadership in the circular economy. The Packaging Act (Verpackungsgesetz) mandates that producers assume responsibility for the entire lifecycle of their packaging, encouraging innovations in high-recyclability multilayer laminates.

Technological collaboration is a key trend, exemplified by Hoffmann Neopac AG partnering with Saperatec GmbH to develop processes capable of separating multilayer composite materials into individual plastic and aluminum layers for high-quality recycling. Regulatory mandates under EU PPWR, including 2030 recyclability targets and minimum recycled content requirements, are significantly shaping product design and manufacturing practices in the German ABL tubes market, driving both sustainability and material efficiency.

China’s ABL tube market is advancing under government initiatives linked to the “dual carbon” goal, promoting eco-friendly and reusable packaging materials. Policies restricting non-degradable plastics are driving demand for recyclable laminates. Technological adoption, including automation, AI, and 5G-enabled industrial internet solutions, is improving production efficiency and supporting flexible manufacturing for pharmaceutical, cosmetic, and personal care applications.

Sustainability remains a central focus, with new laminate materials being developed for easier recycling. The rapid growth of domestic e-commerce platforms is further accelerating demand for tamper-proof, secure, and durable ABL tubes, particularly in the cosmetics and personal care segments. Additionally, China’s “Made in China 2025” plan aims to increase domestic content in core materials to 70%, fostering high-tech, sustainable manufacturing practices in the country’s ABL tube industry.

India’s ABL tubes market is being propelled by government initiatives like “Make in India” and “Zero Effect Zero Defect”, promoting high-quality domestic production. Investments under the Production Linked Incentive (PLI) Scheme for the food processing and pharmaceutical sectors are enhancing manufacturing capabilities, supporting the production of standardized, high-quality ABL tubes.

Regulatory measures, including the Plastic Waste Management (Amendment) Rules, are driving the adoption of eco-friendly laminates. Rising disposable income and urbanization are shifting consumer demand toward convenient, single-serve, and portable packaging, further boosting adoption. India is also emerging as a key exporter of ABL tubes, particularly to the Middle East and Africa, reflecting the country’s competitive manufacturing advantages and growing international market share.

|

Parameter |

Details |

|

Market Size (2025) |

$1.9 Billion |

|

Market Size (2034) |

$3.6 Billion |

|

Market Growth Rate |

7.2% |

|

Segments |

By Material Type (Aluminum, Polyethylene, Co-polymer, EVOH), By End-Use Industry (Oral Care, Cosmetics & Personal Care, Pharmaceuticals, Food & Beverages, Household & Industrial), By Capacity (Less than 50 ml, 50–100 ml, 101–150 ml, Above 150 ml), By Cap Type (Flip-Top Cap, Stand-Up Cap, Fez Cap, Nozzle Cap, Other Cap Types) |

|

Study Period |

2019- 2024 and 2025-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Huhtamaki Oyj, Amcor plc, Berry Global Inc., Sonoco Products Company, Albéa S.A., Hoffmann Neopac AG, Essel Propack Limited (EPL), Montebello Packaging, DNP (Dai Nippon Printing Co., Ltd.), TUBE-TEC S.p.A., CCL Industries Inc., EPL Limited, Libo Group, Tubex GmbH, Unette Corporation |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

* List Not Exhaustive

USDAnalytics conducted an extensive and structured research methodology to provide an in-depth analysis of the global Aluminum Barrier Laminate (ABL) Tubes Market. The study combined primary research, including interviews with packaging manufacturers, pharmaceutical and cosmetic brand owners, and supply chain experts, with secondary research from company reports, regulatory publications, and industry news. Market sizing, forecasts, and growth trends were determined using historical sales data, innovations in barrier laminates, sustainability initiatives, and evolving regulatory standards across regions such as the U.S., Germany, China, and India. Segmentation was evaluated by material type, end-use industry, tube capacity, and cap type, while competitive intelligence examined strategic expansions, mergers and acquisitions, and technology-driven product developments by leading players including Albéa, Huhtamaki, Constantia Flexibles, Hoffmann Neopac, and Amcor. The methodology also incorporated analysis of consumer demand for premium packaging, lightweighting, recyclable mono-materials, and smart packaging features, ensuring industry professionals receive actionable insights on operational efficiency, sustainability compliance, and market opportunities in the ABL tubes sector.

Table of Contents: Aluminum Barrier Laminate (ABL) Tubes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Aluminum Barrier Laminate (ABL) Tubes Market Landscape & Outlook (2025–2034)

2.1. Introduction to ABL Tubes Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Industry Developments and Strategic Investments

2.4. Regulatory Framework Impacting Market Growth

2.5. Sustainability and Circular Economy Trends

3. Innovations Reshaping the ABL Tubes Market

3.1. Trend: Accelerated Adoption by Premium Cosmetic and Pharma Brands

3.2. Trend: Material Reduction and Lightweighting Through Advanced Laminate Engineering

3.3. Opportunity: Development of Full-Polyethylene, Recyclable Barrier Laminate Structures

3.4. Opportunity: Integration of Smart Features for Consumer Engagement and Anti-Counterfeiting

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers, Acquisitions and Strategic Alliances

4.2. R&D and Material Innovation

4.3. Sustainability and Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: ABL Tubes Market

5.1. By Material Type

5.1.1. Aluminum

5.1.2. Polyethylene

5.1.3. Co-polymer

5.1.4. EVOH

5.2. By End-Use Industry

5.2.1. Oral Care

5.2.2. Cosmetics & Personal Care

5.2.3. Pharmaceuticals

5.2.4. Food & Beverages

5.2.5. Household & Industrial

5.3. By Capacity

5.3.1. Less than 50 ml

5.3.2. 50–100 ml

5.3.3. 101–150 ml

5.3.4. Above 150 ml

5.4. By Cap Type

5.4.1. Flip-Top Cap

5.4.2. Stand-Up Cap

5.4.3. Fez Cap

5.4.4. Nozzle Cap

5.4.5. Other Cap Types

6. Country Analysis and Outlook of ABL Tubes Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. ABL Tubes Market Size Outlook by Region (2025–2034)

7.1. North America ABL Tubes Market Size Outlook to 2034

7.1.1. By Material Type

7.1.2. By End-Use Industry

7.1.3. By Capacity

7.1.4. By Cap Type

7.2. Europe ABL Tubes Market Size Outlook to 2034

7.2.1. By Material Type

7.2.2. By End-Use Industry

7.2.3. By Capacity

7.2.4. By Cap Type

7.3. Asia Pacific ABL Tubes Market Size Outlook to 2034

7.3.1. By Material Type

7.3.2. By End-Use Industry

7.3.3. By Capacity

7.3.4. By Cap Type

7.4. South America ABL Tubes Market Size Outlook to 2034

7.4.1. By Material Type

7.4.2. By End-Use Industry

7.4.3. By Capacity

7.4.4. By Cap Type

7.5. Middle East and Africa ABL Tubes Market Size Outlook to 2034

7.5.1. By Material Type

7.5.2. By End-Use Industry

7.5.3. By Capacity

7.5.4. By Cap Type

8. Company Profiles: Leading Players in the Aluminum Barrier Laminate (ABL) Tubes Market

8.1. Huhtamaki Oyj

8.2. Amcor plc

8.3. Berry Global Inc.

8.4. Sonoco Products Company

8.5. Albéa S.A.

8.6. Hoffmann Neopac AG

8.7. Essel Propack Limited (EPL)

8.8. Montebello Packaging

8.9. DNP (Dai Nippon Printing Co., Ltd.)

8.10. TUBE-TEC S.p.A.

8.11. CCL Industries Inc.

8.12. EPL Limited

8.13. Libo Group

8.14. Tubex GmbH

8.15. Unette Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Growth in the ABL tubes market is fueled by superior barrier protection, rising demand from oral care and pharmaceutical segments, and the push for sustainable, recyclable packaging. Lightweighting, premium decoration, and regulatory compliance further accelerate adoption across cosmetics, personal care, and food industries.

Sustainability drives development of recyclable mono-material tubes, lightweight laminates, and eco-friendly caps. Companies like Neopac and Albéa are pioneering fully recyclable barrier tubes and reducing plastic use, aligning with circular economy principles and consumer demand for environmentally responsible packaging.

The U.S., Germany, China, and India are key markets. Regulatory frameworks, e-commerce growth, and government initiatives like “Make in India” and dual-carbon policies in China are boosting demand for high-barrier, eco-friendly, and tamper-proof ABL tubes in oral care, pharma, and cosmetics.

Technological integration, such as smart caps, NFC chips, and QR codes, enables anti-counterfeiting, product traceability, and interactive consumer experiences. Advanced multilayer laminates and aseptic barriers also preserve sensitive ingredients, extend shelf life, and ensure regulatory compliance.

Major players include Albéa, Huhtamaki, Constantia Flexibles, Hoffmann Neopac, and Amcor. Their strategies focus on high-barrier laminates, sustainable and recyclable solutions, lightweight designs, and smart packaging innovations, strengthening market leadership across oral care, pharmaceutical, and premium cosmetic segments.