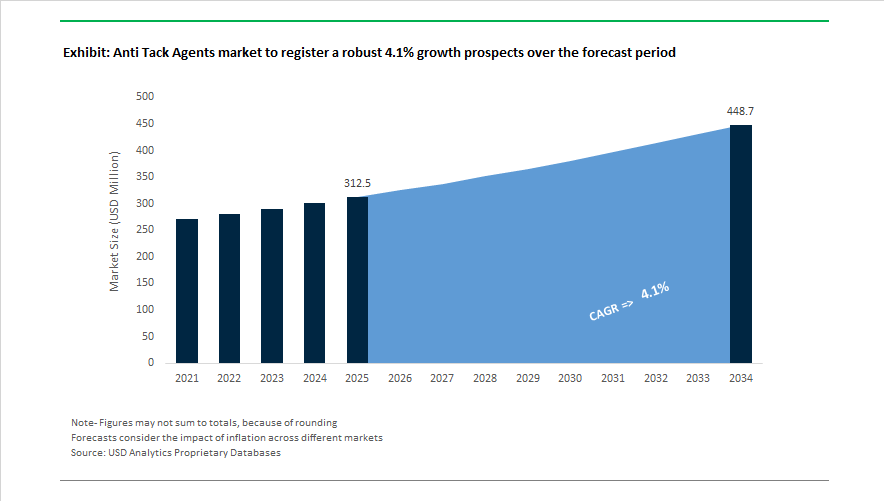

Market Overview: Anti Tack Agents Market Advances Toward $448.6 Million by 2034 as Rubber Processing Efficiency and Sustainable Release Technologies Gain Priority

The anti tack agents market is valued at $312.5 Million in 2025 and is projected to reach $448.6 Million by 2034, expanding at a 4.1% CAGR. Growth is supported by rising demand for rubber processing aids, mold release agents, anti-stick coatings, polymer surface modifiers, and tire manufacturing lubricants used to prevent unwanted adhesion during compounding, calendaring, and extrusion. Modern rubber and elastomer production relies on water-based anti-tack dispersions, zinc stearate alternatives, fatty acid derivatives, and polymer-compatible release chemistries that improve surface finish while minimizing contamination of downstream bonding or coating operations. Market expansion is further linked to stricter environmental standards encouraging the shift from traditional talc and soap-based powders to low-dust, solvent-free, and bio-attributed anti-tack formulations.

Structural realignment began in February 2024 when Barbe Group marked its 75th anniversary and reinforced its “Green Release” portfolio of water-based systems. That same year, Polymer Solutions Group completed integration of Blachford’s G-Block and Antitack lines, strengthening North American supply of anti-tack slurries and powders. Regional expansion followed in June 2024 as Barbe appointed Convip as distributor in Brazil, targeting the growing South American tire sector. Digitalization advanced in January 2025 when Barbe implemented a global information security framework to safeguard proprietary anti-tack formulations. Technology momentum accelerated in March 2025 as Evonik Industries introduced mass-balanced TEGO eCO additives, enabling bio-attributed feedstock substitution in specialty surface agents. During 2025, suppliers such as King Industries and Lion Specialty Chemicals reported rapid adoption of nano-sized anti-tack technologies that improve mold cleanliness and reduce residue.

Competitive strategy intensified in November 2025 when Lanxess advanced its FORWARD cost action plan, optimizing positioning of its Rhenodiv anti-tack range amid soft European demand. The same month, the proposed merger between AkzoNobel and Axalta signaled consolidation of surface-modifier expertise across automotive and plastics additives. Pharmaceutical-grade capability expansion occurred in December 2025 when Croda International partnered with Amino GmbH to refine high-purity fatty and amino chemistries applicable to medical-grade rubber additives. Digital transformation peaked in January 2026 as BASF confirmed the opening of its global Digital Hub in Hyderabad to apply AI modeling for specialty additive optimization, followed by a February 2026 collaboration between BASF and Xfloat to enhance polymer durability and reduce surface tack in floating solar structures.

Trends and Opportunities Reshaping Formulation Strategies and Procurement Priorities in the Anti Tack Agents Market

Market Trend- Regulatory Shift Accelerating Silicone-Free, Mineral-Based Anti Tack Systems

The Anti Tack Agents Market is moving decisively away from cyclic volatile methyl siloxanes (D4, D5, D6) as global regulatory agencies intensify scrutiny on persistence and bioaccumulation. Under EU REACH Regulation (EU) 2024/1328, vPvB-classified silicones are restricted in rubber processing, pushing manufacturers toward stearate-modified talc, precipitated silica, and low-VOC aqueous dispersions. This transition is proactive as the European Commission aligns these chemistries for potential inclusion under the Stockholm Convention POPs framework by July 2025. Producers report that 23% of the market has already converted to silicone-free outputs to safeguard export continuity and avoid downstream compliance disruptions.

Performance remains a commercial differentiator. 2025 technical validations show amino-modified organopolysiloxane powders achieving surface energy near 22 mN/m, equating silicone-level release characteristics while supporting sustainability-driven procurement standards increasingly embedded in automotive and industrial rubber supply chains.

Market Trend- Dual-Function Anti Tack Agents Advancing Green Tire Processing

A second structural trend is the emergence of anti tack agents as processing aids rather than simple release films. High-silica compounds in Low Rolling Resistance (LRR) tires require better polymer flow, lower mixing temperature, and filler compatibility. Fatty acid ester additives are reducing mixing times by up to 15 percent, directly lifting unit throughput in automated facilities. The rise of Electric Vehicles, which accounted for 13.6% of new European registrations in late 2024, is expanding this requirement to compounds engineered for heat dissipation near battery housings.

To strengthen silica dispersion, PEG and stearate blends are increasingly essential to prevent agglomeration. Demonstrated fuel efficiency gains of up to 15% reinforce why tire OEMs now treat anti tack chemistry as a key performance enabler linked to sustainability credentials and warranty outcomes.

Processing Enabler for Recycled and Bio-Based Rubber in Circular Tire Manufacturing

The adoption of recycled rubber and renewable feedstocks is rising under global sustainability commitments such as the 2025 Recycled Polyester and Rubber Challenge, but these materials introduce high tack variability that jeopardizes factory uptime. Complex compounds utilizing recycled tire rubber (RTR) with bio-based carbon black and reclaimed steel require controlled-viscosity liquid anti tack systems to ensure uniform film formation even on irregular particles.

Commercialization of guayule rubber—highlighted in the 2025 MIDAS Project for its drought resilience—adds another layer of complexity. Its resin-rich composition can cause interlayer contamination unless protected by non-migratory agents, which preserve bonding integrity in multi-layer tire designs. This creates an opportunity for suppliers offering vegetable-oil-based soaps and stearic derivatives that support full bio-based material labelling for premium eco-tire segments.

High-Purity, Low-Migration Agents Supporting Medical and Food-Contact Silicone

Medical device and food packaging regulations are redefining purity standards for anti tack usage in silicone. Under Commission Regulation (EU) 2025/351, additives must demonstrate zero migration into fatty or acidic food simulants, which strengthens demand for USP Class VI-certified agents in gaskets, bakeware, and flexible food-contact components.

Medical applications intensify performance requirements. Devices sterilized using Vaporized Hydrogen Peroxide (VHP) and Gamma irradiation need anti tack agents that do not haze or degrade clarity. Suppliers such as Shin-Etsu are now integrating anti tack characteristics directly into “No Post Cure” silicone systems to minimize contamination risk in surgical fields. In parallel, BPA-free mandates and PFAS removals are triggering resin reformulation, escalating the need for chemically compatible, migration-safe anti tack solutions designed for healthcare and industrial food processing environments.

Anti-Tack Agents Market Share and Segmentation Insights

Market Share by Product Type: Metallic Stearates Lead Volume as Fatty Acid Amides and Synthetic Waxes Gain Ground

Metallic stearates account for approximately 31% of the global anti-tack agents market in 2025, led by zinc stearate, the industry benchmark for rubber and tire manufacturing due to excellent release performance, low cost, and non-migratory barrier formation. Calcium stearate remains widely specified in pharmaceutical and food-contact applications. Fatty acid amides, primarily erucamide and oleamide, rank next, functioning as migratory anti-tack agents that bloom to the surface in polyolefin films and conveyor belts. Silicone polymers serve high-temperature and medical-grade tubing but face adoption limits from cost and paint adhesion concerns. Synthetic waxes, including polyethylene and paraffin dispersions, are gaining share as solvent systems phase out, aligning with sustainability initiatives. Traditional soap-based agents continue to decline due to drying time and wastewater issues, steadily replaced by stearate powders and wax emulsions across modern rubber processing lines.

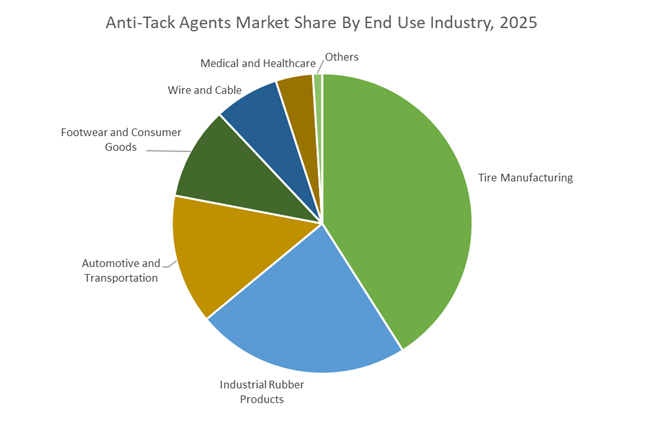

Market Share by End-Use Industry: Tire Manufacturing Dominates While EV Components and Grid Modernization Lift Specialty Demand

Tire manufacturing represents roughly 41% of global anti-tack agent consumption in 2025, driven by large-scale use of zinc stearate dispersions to prevent uncured rubber sheets from sticking during mixing, calendering, extrusion, and storage. Industrial rubber products follow, covering hoses, conveyor belts, gaskets, and seals, with demand closely tied to industrial output. Automotive and transportation applications extend beyond tires into weatherstripping and vibration dampers, supported by rising EV production and the need for high-performance battery and thermal management seals. Footwear and consumer goods rely on anti-tack agents in sole molding and synthetic leather processing, benefiting from ongoing athleisure demand. Wire and cable applications are expanding with grid upgrades and data center construction. Medical and healthcare remains a small but premium segment, requiring USP Class VI compliant stearates and silicones for stoppers, plungers, and surgical tubing.

Anti Tack Agents Market Competitive Landscape

The global anti tack agents market is characterized by increasing demand from tire manufacturing, medical rubber components, industrial hoses, conveyor belts, and EV-specific rubber formulations. Market leaders are prioritizing water-based anti-tack dispersions, biodegradable release agents, zinc-free metallic soaps, and internal anti-tack technologies to comply with tightening environmental regulations across the EU, North America, and Asia-Pacific. Strategic investments in localized production, automated application systems, and high-purity fatty acid esters are reshaping competitive intensity. As rubber processors seek improved slab handling, reduced dusting, and residue-free vulcanization, innovation in polymer-based coatings, dry-film systems, and nanoparticle anti-tacks is driving differentiation in high-growth segments such as EV tires and medical-grade elastomers.

Integrated water-based anti-tack systems reinforce Polymer Solutions Group global dominance

Following the strategic integration of SASCO Chemical and Blachford’s rubber business during 2024 to 2025, Polymer Solutions Group has emerged as the undisputed global leader in anti tack solutions. Its PolyBatch® and SASCO® brands, particularly the SASCO® Slab Dip series, use advanced polymer technology to deliver uniform, non-dusting coatings on unvulcanized rubber. In late 2025, PSG completed major capacity expansions in Georgia and Europe to support rising demand from the EV tire sector. The company’s strength lies in process engineering, supplying automated dip tanks and spray systems alongside chemicals. Its strategic shift toward 100% water-soluble, biodegradable dispersions eliminates mechanical scraping and secondary cleaning, reinforcing water-based dominance.

Nanoparticle efficiency and sustainable stearates define Lion Specialty Chemicals Co., Ltd. leadership

Lion Specialty Chemicals remains the technology benchmark in Asia-Pacific, focusing on environment-friendly esters and high-purity metallic soaps. In 2025, Lion introduced a nanoparticle anti-tack formulation that uses 30% less material while delivering 20% higher release efficiency, particularly suited for thin-walled medical rubber components. The company dominates medical and hygiene applications such as plungers, syringes, and pharmaceutical stoppers, where biocompatibility is critical. In early 2026, Lion collaborated with Southeast Asian rubber producers to pilot palm-oil derived stearates, strengthening regional sustainability. Its surfactant science expertise ensures continuous anti-tack films on complex-molded geometries, improving release consistency in precision rubber manufacturing.

Zero-zinc transition and internal migration technology strengthen Schill + Seilacher Struktol GmbH positioning

Struktol differentiates itself as a specialty-driven innovator in anti tack agents that double as rubber processing aids. Its Struktol® anti-tack agents for latex are essential for high-elasticity bands and medical gloves, preventing former contamination during production. By 2026, nearly 80% of its zinc-based portfolio has been replaced with potassium and sodium soaps, aligning with stricter EU environmental regulations. The 2025 expansion of its Hamburg research center supports development of internal anti-tacks that migrate to the rubber surface during storage, eliminating external dipping tanks. Deep integration into rubber compounding ensures these additives remain invisible during vulcanization, preventing delamination in multilayer rubber systems.

Residue-free ester innovation advances King Industries, Inc. in industrial rubber

King Industries focuses on high-durability anti-tack agents designed for extreme thermal cycles in industrial rubber processing. Its K-LUBE® and DISPARLON® lines offer liquid and paste release agents that prevent caking and sediment buildup in batch-off systems. In late 2025, the company opened a new fatty acid ester facility to produce high-purity alternatives to paraffin waxes, enhancing sustainability and performance. King Industries serves conveyor belt and industrial hose manufacturers where high-viscosity compounds demand aggressive anti-tack functionality. Its residue-free formulations leave zero ash or carbon deposits, a critical requirement in aerospace-grade seals and gaskets requiring flawless thermal and mechanical integrity.

Concentrated dry-film logistics innovation elevates Barbe Group

Barbe Group is recognized for pioneering dry-film anti-tack technology and concentrated delivery systems that lower logistics costs. In 2025, the company scaled its water-soluble bag solution, supplying pre-measured powders in biodegradable packaging that can be directly introduced into dip tanks, minimizing worker dust exposure. Its LUBOTRACK series emphasizes 100% active concentrates and pastes, reducing shipping water by up to 60% and significantly lowering transport-related carbon emissions. Barbe plays a major role in high-volume tire manufacturing, offering pigmented slurries that allow visual inspection of coating uniformity. Expansion of its Chinese production site in 2025 strengthened its position in the domestic premium tire segment.

Carbon-negative ester science distinguishes Hallstar

Hallstar leads the market in ester-based anti-tack agents that also enhance rubber flow and extrusion efficiency. Its portfolio of fatty acid amides and high-purity esters acts as both external anti-tack coatings and internal lubricants, improving processing stability. Hallstar dominates non-pigmented anti-tack applications where rubber products are not re-milled, ensuring flawless surface finishes in precision molding. In 2026, the company transitioned its MAGLITE® and anti-tack lines to carbon-negative sourcing, utilizing bio-based feedstocks derived from non-food agricultural waste. Hallstar serves automotive and electronics precision components where anti-tacks must not interfere with conductivity, thermal resistance, or dimensional accuracy.

China Anti Tack Agents Market: Tire Megascale, Water-Based Conversion, and EV-Specific Formulations

China remains the largest global demand center for anti tack agents, anchored by its massive tire manufacturing base. With tire output surpassing 940 million units during 2024–2025, domestic consumption of anti-tack agents used in calendering, extrusion, and batch-off processes has risen sharply to maintain compound flow consistency and prevent surface adhesion. Capacity expansion has followed demand, with PMC Group announcing a 25% increase in fatty acid amide production capacity at its Chinese facilities in late 2025, supporting wire, cable, and industrial rubber applications alongside tires.

Environmental policy is accelerating a decisive formulation pivot. Under China’s Blue Sky initiatives, more than 70% of new production lines in Jiangsu and Zhejiang have transitioned to water-based anti-tack dips, eliminating airborne dust risks associated with powder systems. Feedstock security is improving through localized upstream integration, as the BASF Zhanjiang Verbund site reached operational milestones in late 2025, enabling domestic supply of high-purity precursors for non-toxic, next-generation anti-tack formulations. Product specialization is also increasing, with Chinese manufacturers launching high-thermal-stability anti-tack agents in 2025 tailored for heavy-load, high-torque electric vehicle tires. This evolution is reinforced by university-industry collaboration, including FUNO Group-led research into nano-sized anti-tack agents that deliver uniform surface coverage at lower application rates.

India Anti Tack Agents Market: Tire Capacity Expansion, Standards Enforcement, and Bio-Based Momentum

India’s anti tack agents market is expanding in parallel with tire manufacturing investments and regulatory standardization. Bridgestone announced the addition of 1.1 million tires per year capacity at its Pune plant by 2029, with early-phase execution in 2025 already driving higher demand for automated batch-off anti-tack systems. National tire output exceeded 180 million units in the 2024–2025 cycle, intensifying the need for advanced anti-tack lubricants that reduce scrap rates in high-throughput environments.

Policy alignment is reshaping supply chains. The Indian government’s Notification No. 30/2025-26 amended import rules for key chemical precursors, stabilizing availability for high-end polymer additives. At the same time, mandatory BIS certification deadlines set for March 31, 2026 are forcing exporters and domestic suppliers to align anti-tack formulations with Indian quality benchmarks. Sustainability is emerging as a parallel growth vector. Under the National BioE3 Policy, startups and specialty chemical firms are receiving federal grants to develop plant-based anti-tack substitutes for petroleum-derived stearates, signaling a gradual transition toward renewable processing aids.

United States Anti Tack Agents Market: Automation, Metal-Free Reformulation, and Portfolio Consolidation

In the United States, the anti tack agents industry is being reshaped by automation, regulatory pressure on metallic additives, and consolidation among specialty suppliers. By late 2025, industry reports indicated that 21% of U.S. rubber manufacturers had fully automated anti-tack application systems, replacing open powder dusting with enclosed liquid emulsion dips to improve worker safety and process control.

Product innovation remains strong. Struktol Company of America introduced a silicone-polymer anti-tack agent in 2025 offering 30% higher heat resistance, addressing aerospace and military-grade rubber processing requirements. Regulatory momentum is accelerating reformulation, as the U.S. Environmental Protection Agency’s 2026 outlook includes stricter limits on lead and zinc dust, prompting the phase-out of traditional metallic stearates. Competitive dynamics are also shifting through consolidation. Polymer Solutions Group completed the integration of Blachford’s rubber business in 2025, strengthening the SASCO brand’s position in clean-delivery anti-tack systems. Upstream synergy is reinforced by Cabot Corporation, which expanded specialty carbon black production in November 2025 to support high-performance tire compounds used alongside advanced anti-tack lubricants.

Germany Anti Tack Agents Market: Bio-Based Leadership, Zinc-Free Systems, and REACH Alignment

Germany represents the regulatory and sustainability frontier of the anti tack agents industry in Europe. In late 2025, Evonik Industries launched a bio-based stearate line derived entirely from renewable resources, targeting medical and automotive rubber applications that demand clean-label processing aids. This move aligns with Europe’s broader decarbonization and materials transparency agenda.

Metal-free innovation is gaining traction. Baerlocher GmbH commercialized a zinc-free anti-tack formulation in 2025, designed to comply with Euro 7 emissions standards by reducing metallic leaching in tire-wear particles. Performance requirements are also tightening in infrastructure-linked rubber components. Deutsche Bahn updated its 2025 technical specifications for vibration-damping rubber parts, favoring bloom-resistant anti-tack agents that preserve long-term integrity. These developments are underpinned by regulatory discipline, with German manufacturers achieving approximately 95% compliance with updated REACH Annexes governing VOC content in rubber processing aids.

Structural Drivers Shaping the Anti Tack Agents Industry

Anti Tack Agents market County Level Snapshot

|

Country

|

Core Demand Driver

|

Strategic Industry Shift

|

|

China

|

Tire megascale and EV growth

|

Water-based, nano-enabled, export-oriented formulations

|

|

India

|

Tire capacity build-out and BIS enforcement

|

Automated systems and bio-based substitutes

|

|

United States

|

Automation and metal dust regulation

|

Liquid emulsions, silicone polymers, supplier consolidation

|

|

Germany

|

REACH and emissions compliance

|

Bio-based, zinc-free, bloom-resistant solutions

|

Anti Tack Agents Market Report Scope

Anti Tack Agents market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$312.5 Million

|

|

Market Size (2034)

|

$448.6 Million

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Product Type (Stearates, Fatty Acid Esters, Fatty Acid Amides, Soaps, Silicone Polymers, Metallic Stearates, Synthetic Waxes), By Physical Form (Powder, Liquid, Paste and Slurry, Masterbatches), By End Use Industry (Tire Manufacturing, Industrial Rubber Products, Footwear and Consumer Goods, Medical and Healthcare, Automotive and Transportation, Wire and Cable), By Application Method (Batch Off Systems, Extrusion and Calendering, Molding Processes)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Polymer Solutions Group, Evonik Industries AG, Baerlocher GmbH, Croda International Plc, Lanxess AG, Struktol Company of America, Lion Specialty Chemicals, Barbe Group, King Industries Inc, Kettlitz Chemie, Blachford, PMC Group, FUNO Group, Tianjin Xiongguan Technology, Hallstar Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti Tack Agents Market Segmentation

By Product Type

- Stearates

- Fatty Acid Esters

- Fatty Acid Amides

- Soaps

- Silicone Polymers

- Metallic Stearates

- Synthetic Waxes

By Physical Form

- Powder

- Liquid

- Paste and Slurry

- Masterbatches

By End Use Industry

- Tire Manufacturing

- Industrial Rubber Products

- Footwear and Consumer Goods

- Medical and Healthcare

- Automotive and Transportation

- Wire and Cable

By Application Method

- Batch Off Systems

- Extrusion and Calendering

- Molding Processes

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Anti Tack Agents Industry

- Polymer Solutions Group

- Evonik Industries AG

- Baerlocher GmbH

- Croda International Plc

- Lanxess AG

- Struktol Company of America

- Lion Specialty Chemicals

- Barbe Group

- King Industries Inc

- Kettlitz Chemie

- Blachford

- PMC Group

- FUNO Group

- Tianjin Xiongguan Technology

- Hallstar Company

*- List not Exhaustive