Automotive Interior Materials Market Overview: Sustainability Mandates, Lightweighting Targets & VOC Compliance Shaping Long-Term Strategy

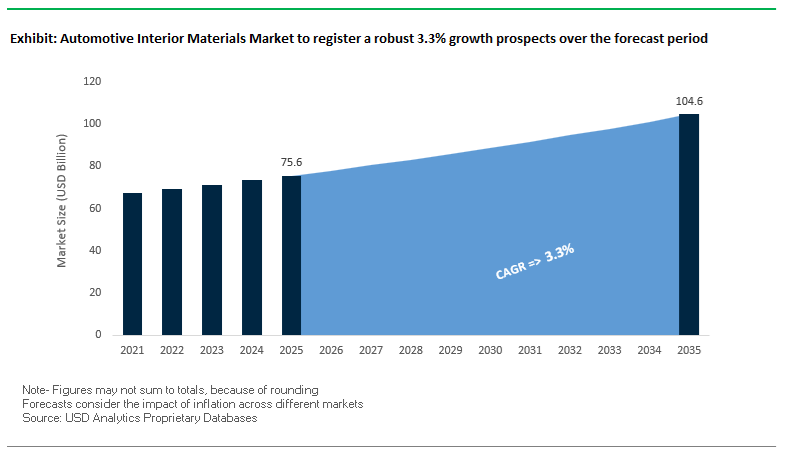

The Automotive Interior Materials Market, valued at USD 75.6 billion in 2025 and projected to reach USD 104.6 billion by 2035 at a 3.3% CAGR, is experiencing a foundational shift as global automakers migrate toward electrified platforms, sustainable material ecosystems, and digitally immersive cabin architectures. As EV adoption accelerates, interior materials are no longer evaluated solely on cost or durability—modern vehicle programs now require lightweight seating systems, low-VOC polymers, smart-touch surfaces, high-acoustic-performance composites, and sensor-ready trim components that support the next generation of software-defined interiors.

For OEMs, Tier-1 suppliers, and procurement teams, strategic selection of automotive interior materials increasingly depends on

- Sustainability performance, including verification of bio-based, recycled, or circular-feedstock polymers aligned with OEM mandates of 25–40% sustainable content by 2030;

- Lightweighting efficiency, driven by EV range optimization, where 5–10% seat weight reduction is becoming an industry-standard benchmark;

- Cabin air quality and regulatory compliance, requiring materials that exceed VDA 278 VOC and fogging thresholds to meet premium interior specifications;

- Integration readiness for smart, digital cabins, enabling haptics, ambient lighting, surface heating, capacitive switches, transparent TPO layers, and embedded sensor networks essential for Software-Defined Vehicles (SDVs).

As EVs eliminate engine noise, NVH (Noise, Vibration, Harshness) materials take on greater importance, with buyers targeting NRC improvements ≥0.4 in key cabin zones to maintain premium acoustic comfort. Interior materials thus evolve from traditional trim components into functional, sustainable, and electronics-compatible subsystems that directly influence consumer experience, regulatory alignment, and platform-level TCO.

Market Analysis: Sustainability Awards, Modular Seating Breakthroughs & Smart Cabin Design Advancing Global Competition

The Automotive Interior Materials Market continued to evolve rapidly across 2024–2025, driven by innovations in sustainability, modular seating, smart surfaces, and digital cockpit integration. In November 2025, FORVIA (Faurecia) unveiled its On-Demand Center Console, showcasing a highly modular EV cabin architecture with reconfigurable panels, surface activation functions, and embedded heating/cooling features. This reflects a broader industry transition toward adaptive cabin environments, especially relevant for autonomous and semi-autonomous vehicle platforms. In October 2025, FORVIA MATERI’ACT received the CLEPA Green Award for its recycled IniCycled-P polymer, achieving 25% CO₂ reduction from cradle-to-gate and already in series production for a major European OEM - signaling a new threshold for sustainable material commercialization.

Seating innovation was a dominant theme throughout 2025. In September 2025, Adient introduced its Pure Ergonomics concept claiming up to 60 mm additional knee/foot space and 5–10% seat weight reduction, meeting EV lightweighting imperatives while elevating occupant comfort. In August 2025, Adient launched ModuGo, a modular seating system built on Ultrathin base technology with 100% recyclable material use and full customization options for structural zoning and digital features. Later that same month, Adient partnered with Autoliv to introduce Omni Safety™ into its Z-Guard seating concept, enabling protection for reclined “zero-gravity” positions - a critical safety requirement for autonomous-ready vehicles.

Digital cockpit transformation advanced alongside materials innovation. In October 2025, Yanfeng won a Red Dot Design Award for the XIM25 smart cabin, leveraging AI-based emotion sensing and natural materials to create personalized, human-centric interior spaces. Earlier in April 2025, Marelli presented integrated surface lighting at Auto Shanghai, demonstrating how interior/exterior lighting convergence is becoming central to both safety and vehicle-to-occupant communication. Finally, in March 2025, a major interior supplier signed an 80% renewable-energy PPA for Europe, reinforcing Scope 3 emissions reduction expectations across the interior materials supply chain.

Key Trends Redefining the Automotive Interior Materials Market

Trend 1: Regulatory Enforcement Drives Adoption of Low-VOC, Hypoallergenic, and Flame-Retardant Interior Materials

Global regulators are mandating a dramatic reduction in volatile organic compounds (VOCs), aldehydes, and hazardous flame-retardant chemistries within vehicle cabins—forcing OEMs to redesign material recipes, adhesives, foams, and coatings. The European Union’s upcoming formaldehyde limit under REACH Annex XVII (Entry 77) requires all vehicles placed on the market after August 2027 to maintain cabin concentrations below 0.062 mg/m³ (≈62 μg/m³). This regulation alone triggers a systematic replacement of traditional adhesives, back foams, and textile treatments with advanced low-emission alternatives.

China—one of the most VOC-sensitive automotive markets—further amplifies this shift with its mandatory GB/T 27630 standard, capping TVOC concentrations at 600 μg/m³. Given persistent consumer dissatisfaction related to odor and cabin air quality, OEMs operating in China are aggressively qualifying ultra-low VOC plastics, PU foams, and coatings that comply with both odor and emissions metrics. Health studies highlight that TVOC levels exceeding 3,000 μg/m³, observed in some new-car measurements, cause acute discomfort—making air-quality compliance not just regulatory, but a core customer-experience imperative.

As a result, the automotive interior materials market is accelerating towards low-VOC polymers, aldehyde-scavenging additives, hypoallergenic surfaces, and inherently flame-retardant materials that satisfy safety standards while supporting modern design aesthetics.

Trend 2: OEM Sustainability Narratives Accelerate Demand for Recycled, Bio-Based, and Fully Traceable Materials

Automotive interiors have become a storytelling platform for brand sustainability, especially in the EV and premium segments. OEMs are strategically shifting from isolated recycled components to holistic material ecosystems that integrate recycled plastics, bio-composites, and plant-based polymers—supported by full traceability.

The proposed EU End-of-Life Vehicle (ELV) Directive mandates that vehicles contain at least 25% recycled material by 2030, ensuring long-term, stable demand for recycled PP, PET, and other interior-grade resins. This regulatory certainty is accelerating investment into odor-controlled, color-stable, and process-ready recycled compounds suitable for visible interior trims.

Simultaneously, the market for bio-based polypropylene and other renewable polymers is rapidly scaling as OEMs validate these materials as true drop-in replacements, compatible with existing injection molding and surface-finishing lines. Brands such as Ford, Honda, and Nissan are targeting 20–30% recycled-plastic incorporation across interior and exterior parts by 2030, reinforcing a durable demand pathway for suppliers offering verifiable, traceable, and high-performance sustainable materials.

High-Value Opportunities Emerging in the Automotive Interior Materials Market

Opportunity 1: Multifunctional Integrated Surfaces Enabling Haptics, Illumination, and Embedded Electronics

As EV interiors shift toward minimalist, “living-room-like” design philosophies, large seamless surfaces are replacing traditional mechanical buttons. This creates a high-growth opportunity for multifunctional interior materials that integrate haptic responses, hidden illumination, capacitive sensing, and cleansing/antimicrobial functionalities directly into the surface structure.

Haptic-feedback integration is emerging as a critical safety technology. By embedding tactile response mechanisms into dashboards, steering wheels, and center consoles, OEMs can deliver eyes-on-road control, reducing driver distraction inherent in purely visual touchscreen interfaces. Material suppliers are responding with specialized polycarbonate blends and engineered surfaces capable of transmitting vibration signatures while maintaining structural rigidity.

The aesthetic trend toward “hidden-until-lit” or “secret-till-lit” surfaces relies on advanced polymer blends (e.g., Makroblend® formulations) designed with optimized optical diffusion, allowing displays and icons to remain invisible until activated. Meanwhile, Sustainable Flexible Electronics (SFE) platforms now enable ultra-thin circuitry and capacitive sensors to conform seamlessly to 3D contoured surfaces such as door panels, steering wheel spokes, and overhead consoles—capabilities unattainable with rigid PCBs.

Opportunity 2: High-Performance Acoustic Materials Address EV Cabin Noise from Wind, Road, and Powertrain Whine

Electric Vehicles eliminate combustion noise but simultaneously unmask structural, road, tire, inverter, and wind noises that were previously masked in ICE platforms. Studies indicate that 70–80% of in-cabin noise in EVs originates from these secondary sources, forcing a shift in NVH engineering from engine-bay isolation to body acoustic insulation and lightweight sound-absorbing materials integrated across the full interior.

Next-generation acoustic foams and multilayer composites are designed to specifically target high-frequency ranges (800–2500 Hz) associated with electric motor tonalities and inverter switching harmonics. Some ultra-silent underbody systems now demonstrate up to 2 dB overall noise reduction, a meaningful improvement in cabin refinement without adding prohibitive mass.

Given that a typical mid-sized EV uses up to 40 kg of acoustic insulation materials—covering the underbody, cabin panels, cargo areas, and battery enclosures—OEMs face a dual challenge: maintaining NVH performance while minimizing weight to preserve driving range. This requirement is driving investment into advanced engineered foams, aerogels, and ultra-light acoustic composites that deliver high absorption coefficients at lower densities.

As consumer expectations for quiet, premium EV cabins increase, advanced acoustic materials will remain a defining competitive differentiator across EV brands.

Automotive Interior Materials Market Share Analysis

Market Share by Material Type: Polymers & Plastics Lead with 43.9% Share

Polymers & Plastics dominate the Automotive Interior Materials Market with a 43.9% share in 2025, reflecting their irreplaceable role as the structural and functional backbone of modern vehicle interiors. Their leadership is driven by a unique combination of lightweighting capability, cost efficiency, design flexibility, and compatibility with mass manufacturing, making them essential for dashboards, door panels, consoles, trims, HVAC components, and interior structural housings. As automotive OEMs push toward higher fuel efficiency, reduced vehicle weight, and modular interior architecture, polymers such as PP, ABS, PU, and TPEs remain the preferred solutions due to their ability to deliver complex geometries, durability, safety compliance, and recyclability. The dominance of polymer-based materials is further reinforced by the industry’s rapid shift toward sustainable interior materials, accelerating adoption of bio-based plastics, recycled polymers, and low-VOC formulations. Surrounding material categories highlight evolving consumer and regulatory priorities—surface coverings (leather, synthetics, textiles) drive premium aesthetics and brand positioning, foams and cushioning define ergonomic comfort and safety performance, acoustic materials address noise reduction challenges in EVs, and high-performance composites enable lightweight structural reinforcement.

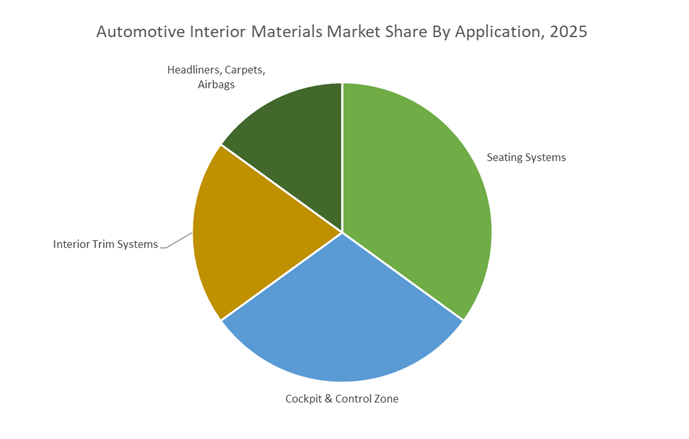

Market Share by Application Component: Seating Systems Lead with 36.1% Share

Seating Systems account for the largest application share at 36.1% in 2025, underscoring their status as the most material-intensive, cost-sensitive, and consumer-influential component within the automotive interior ecosystem. Seating commands this share because it integrates multiple material families—structural polymers, high-resilience foams, advanced textiles, synthetic leathers, natural fiber composites, and acoustic modules—making it both the comfort anchor and brand identity driver of vehicle interiors. OEMs increasingly leverage seat design as a competitive differentiator, using lightweight frames, ergonomic foams, cooled/ventilated seat technologies, and premium surface coverings to elevate user experience in both ICE and EV platforms. The shift to electrified vehicles further reinforces seating’s centrality, as EV automakers optimize cabin space, reduce NVH levels, and introduce lounge-style configurations that rely on advanced materials for functionality and comfort. Surrounding segments shape the broader design strategy: the cockpit and control zone drives innovation in HMI materials suited for capacitive touch and integrated displays; interior trim systems lead in sustainable material substitution using natural fibers and recycled polymers; and headliners, carpets, and airbag fabrics incorporate acoustic dampening and safety-enhancing materials. Collectively, the application mix demonstrates how seating systems anchor material demand while the rest of the interior increasingly evolves around user experience, sustainability, and digital functionality.

Country Analysis: Global Automotive Interior Materials Market Innovation Hubs

China: Smart Surface Integration and NEV-Centric Interior Material Demand Accelerating Digital Cockpit Innovation

China remains the world’s most dynamic and high-volume market for automotive interior materials, driven by explosive New Energy Vehicle (NEV) adoption and rapidly expanding demand for smart, functional interior surfaces. Between January and September 2024, smart-surface-equipped vehicle sales surged 105.1% YoY to 525,000 units, highlighting China’s aggressive shift toward integrated touch interfaces, ambient lighting surfaces, and multi-functional digital cockpit materials. The rise of curved OLED displays—exemplified by models like the Yangwang U7 with an R800 curvature center console—is creating strong demand for scratch-resistant polymers, reinforced optical-grade glass, flexible display substrates, and high-durability coatings.

China is also emerging as a global hub for foldable and rollable cockpit displays, with BOE Varitronix and LG Display showcasing mature OLED cockpit solutions requiring flexible substrates, elastomer coatings, IME-compatible polymers, and robust thin-film encapsulation materials. Mass-market adoption depends heavily on cost optimization, accelerating the industry pivot toward plastic-based touch interfaces and IME (In-Mold Electronics) technologies, which allow lighter weight, seamless integration, and complex 3D functional surfaces. A major strategic shift occurred in 2024, when Chinese OEMs such as BYD and Great Wall Motor invested more in overseas manufacturing plants than domestic ones for the first time—driving global demand for localized interior material supply chains covering Brazil, Southeast Asia, and Europe. This positions China as both the largest consumer and fastest-scaling exporter of next-generation interior materials for digital cockpits and NEVs.

Germany (Europe): Sustainability Regulations and Premium Cockpit Engineering Driving Bio-Based and Lightweight Interior Materials

Germany and the broader European Union are shaping the global automotive interior materials landscape through strict sustainability mandates, advanced materials engineering, and premium cockpit innovation. The EU’s End-of-Life Vehicles Directive, requiring interiors to be 85% recyclable and 95% recoverable by weight, has accelerated the adoption of bio-based polymers, recycled fabrics, and circular composite solutions across European OEMs. Leading suppliers like FORVIA (Faurecia) are at the forefront of this transformation. In 2025, FORVIA was recognized by Stellantis as the Carbon Footprint Reduction Supplier of the Year, emphasizing OEM preference for low-embodied-carbon interior materials.

FORVIA’s MATERI’ACT achieved Top Innovator status at the 2025 CLEPA Innovation Awards, thanks to solutions such as IniCycled-P ELV materials and NAFILean-R, a breakthrough automotive composite made from 20% natural hemp fiber and 100% recycled polypropylene, delivering an 87% CO₂ reduction versus conventional injection-molded parts. The European shift toward comfort-centric interiors is also driving adoption of tactile and thermal innovations such as VIBE® responsive seating technology and Thermal Cocoon ultrathin heated surfaces, which integrate embedded sensors and heating layers under premium textiles and foams. Germany’s Federal Lightweighting Strategy, supported by national events like the April 2025 Lightweighting Summit, continues to promote advanced composites, bio-resins, and polymer innovation for lightweight, sustainable interior components.

United States: CAFE-Driven Lightweighting and Federal R&D Accelerating Composite and Bio-Material Adoption

The U.S. automotive interior materials market is heavily shaped by stringent CAFE standards targeting 49 mpg fleetwide by 2026, compelling automakers to deploy aggressive lightweighting measures. This has driven widespread adoption of advanced polymers, lightweight composites, natural fiber-reinforced plastics, and bio-based interior materials for dashboards, door trims, seating frames, and structural interior modules. Accelerating EV adoption further intensifies this demand, as OEMs seek materials that offset the weight of large battery packs while maintaining crashworthiness and interior comfort.

Federal investment plays a major role. The U.S. Department of Energy continues funding research aimed at reducing the cost of carbon fiber by up to 50%, enabling mass-market use of lightweight composites in both interior and structural vehicle components. Bio-based material integration is rising, with OEMs increasingly adopting bio-polyesters, PLA blends, and sustainable thermoplastic elastomers in headliners, visors, carpets, and floor mats to meet both sustainability targets and consumer expectations. Geopolitical trade shifts are reshaping supply chains: 25% U.S. tariffs on Chinese automotive components (2025) have prompted OEMs such as Stellantis to shift sourcing to Mexico and Southeast Asia, impacting material suppliers across trim, electronics, and polymer-based interior components. The U.S. remains a major innovation hub for lightweight interiors, sustainable composites, and regulatory-driven advanced materials adoption.

Japan: Bio-Plastics Leadership and Functional Fiber Innovation Supporting Long-Term Sustainable Interiors

Japan continues to lead in bio-based polymers, recyclable plastics, and functional fibers for automotive interior applications, supported by its strong materials science heritage and long-term commitment to sustainable manufacturing. Companies like Toyota pioneered early adoption of bio-polyesters and PLA blends in mass-produced vehicles—including the Prius and Lexus HS 250h—using eco-friendly materials in headliners, sun visors, seat fabrics, and floor mats. This early leadership has established Japan as a global benchmark for sustainable interior material deployment.

Japan’s auto supply chain is also expanding globally. Toyoda Gosei’s announcement in September 2024 to build a new manufacturing facility in Karnataka, India, is a strategic move to strengthen its regional production network and support local OEMs with advanced interior and exterior polymer components. Additionally, Japanese firms remain highly competitive in developing functional automotive fibers, including high-strength, flame-retardant, anti-static, and filtration-grade materials used in seats, cabin air filtration, and NVH-reducing textile components. With its focus on circular materials, high-quality polymers, and functional interior fabrics, Japan remains a pivotal innovation hub in sustainable and performance-driven automotive interior materials.

Competitive Landscape: Leaders in Sustainable Materials, Seating Innovation & Smart Cabin Electronics

The competitive landscape is shaped by companies advancing bio-sourced materials, lightweight seating architectures, smart surface technologies, and integrated lighting/electronics platforms. Differentiation is increasingly defined by sustainability certification, digital cockpit integration capability, and global production footprint.

FORVIA (Faurecia) - Leading Sustainable Interiors & Digital Cockpit Integration

FORVIA is a global leader in cockpit systems and intelligent seating solutions, with its MATERI’ACT division pioneering recycled and bio-based interior materials. Its SIMPLIFY program drives cost optimization while sustaining high R&D intensity. Recognition such as Stellantis’ 2025 Carbon Footprint Reduction Supplier of the Year confirms FORVIA’s leadership in low-carbon interior components, including instrument panels, trims, and door modules.

Adient - Global Seating Powerhouse Advancing Lightweighting & Safety Integration

Adient, the world’s largest seating supplier, continues to anchor the global interior materials ecosystem through advanced modular seating architectures. Its Pure Ergonomics and ModuGo programs introduce substantial space gains, material circularity, and digital-ready structural zones. With over 200 global facilities, Adient provides unmatched scale and supply reliability across foam, trim, metal frames, and safety integrations.

Lear Corporation - Vertically Integrated Seating & E-Systems with Proprietary Leather/Textiles

Lear combines advanced seating with in-cabin electronics, leveraging proprietary materials such as Eagle Ottawa Leather and Guilford Performance Textiles. Innovations like INTU™ thermal comfort systems and Configure+™ enhance individualized seating experiences for EVs and SDVs. Lear’s vertical integration ensures consistent quality across the seating materials value chain - from leather/textiles to electronics.

Yanfeng - Smart Cabin Innovator with AI-Driven Material & UX Integration

Yanfeng is a global leader in smart cabin systems, merging lightweight materials with advanced electronics for next-generation user interfaces. Its XIM25 concept integrates AI emotion recognition, ambient lighting, sustainable surfaces, and haptic feedback, demonstrating deep capability in transforming raw materials into holistic, digitally enriched experiences. Winning the 2025 Red Dot Design Award underscores its global design leadership.

Continental AG - Pioneering Sustainable Surface Materials & Functional Surfaces

Continental provides sustainable surface materials (Benova, skai) engineered for low VOCs, bio-based formulations, and enhanced durability. Its Benova Eco Protect line is PETA-approved vegan and optimized for instrument panels and door trims. With solutions like Xpreshn Hylite (translucent functional surfaces) and thermal cocoon heating, Continental is at the forefront of converting static interior surfaces into functional interaction platforms.

Marelli - Advanced Lighting & Display Integration for Next-Generation Interiors

Marelli specializes in intelligent lighting and in-cabin display systems, enabling new communication and personalization modes. Innovations such as the Pixel Rear Lamp, integrated Near-Field Ground Projection, and thin-line LED lighting underscore Marelli’s ability to merge optical, electronic and material technologies. Its strong production focus ensures rapid commercialization of complex in-cabin lighting modules.

Automotive Interior Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$75.6 Billion

|

|

Market Size (2035)

|

$104.6 Billion

|

|

Market Growth Rate

|

3.3%

|

|

Segments

|

By Material Type (Polymers & Plastics, High-Performance Composites, Surface Coverings, Foams & Cushioning, Acoustic/Dampening Materials), By Application Component (Seating Systems, Cockpit & Control Zone, Interior Trim Systems, Headliners & Sun Visors, Carpets & Floor Mats, Airbags & Seatbelts), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Luxury Vehicles), By Technology/Function (Sustainable/Bio-Based Materials, Acoustic & Thermal Insulation, Lightweighting Materials, Smart Surfaces, Low VOC Materials)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

FORVIA, Adient plc, Lear Corporation, Yanfeng Automotive Interiors, Toyota Boshoku Corporation, BASF SE, Covestro AG, Trèves SAS, Daimler AG, Grupo Antolin-Irausa S.A., Continental AG, Toyoda Gosei Co. Ltd., DSM Engineering Plastics, Milliken & Company, Toray Industries Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Automotive Interior Materials Market Segmentation

By Material Type

- Polymers & Plastics

- High-Performance Composites

- Surface Coverings

- Foams & Cushioning

- Acoustic / Dampening Materials

By Application Component

- Seating Systems

- Cockpit & Control Zone

- Interior Trim Systems

- Headliners & Sun Visors

- Carpets & Floor Mats

- Airbags & Seatbelts

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Luxury Vehicles

By Technology / Function

- Sustainable / Bio-Based Materials

- Acoustic & Thermal Insulation

- Lightweighting Materials

- Smart Surfaces

- Low VOC Materials

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Automotive Interior Materials Market

- FORVIA

- Adient plc

- Lear Corporation

- Yanfeng Automotive Interiors

- Toyota Boshoku Corporation

- BASF SE

- Covestro AG

- Trèves SAS

- Daimler AG

- Grupo Antolin-Irausa S.A.

- Continental AG

- Toyoda Gosei Co., Ltd.

- DSM Engineering Plastics

- Milliken & Company

- Toray Industries, Inc.

*- List not Exhaustive