Market Overview: Sustainability and Innovation Driving Bagasse Tableware Growth

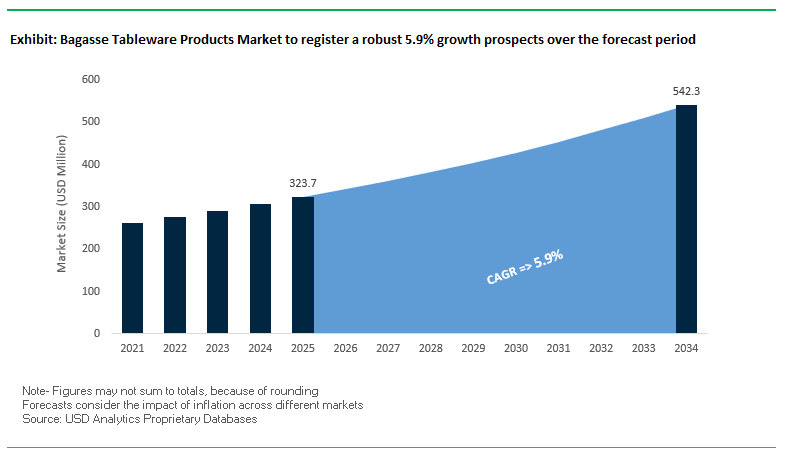

The Global Bagasse Tableware Products Market is projected to grow from $323.7 million in 2025 to $542.3 million by 2034, expanding at a healthy CAGR of 5.9%. This momentum is fueled by regulatory bans on single-use plastics, the rise of eco-conscious consumers, and rapid innovation in molded fiber technologies. Bagasse, a byproduct of sugarcane processing, is increasingly positioned as a premium sustainable material for disposable tableware, offering durability, heat resistance, and compostability.

Key questions for professionals include: How are regulatory frameworks shaping demand? Which material innovations are removing adoption barriers? And how are global brands integrating bagasse into their sustainability commitments? The market is characterized by a balance of regulatory compliance, product innovation, and consumer preference, making it a high-potential segment in the global sustainable packaging industry.

Key Insights for Industry Professionals:

- Policy-Driven Demand: Global bans on single-use plastics are accelerating bagasse adoption in foodservice and retail packaging.

- Product Versatility: From plates and trays to lids and clamshells, bagasse is addressing a broad spectrum of hot and cold food applications.

- Material Advancements: PFAS-free coatings, oil- and water-resistant innovations, and blended fiber technologies are expanding performance capabilities.

- Consumer Appeal: Growing preference for plant-based, compostable solutions makes bagasse a differentiator for brands pursuing green credentials.

Market Analysis: Recent Developments in Bagasse Tableware Products

The bagasse tableware industry is undergoing rapid transformation, marked by expansion projects, regulatory incentives, and high-profile partnerships. In May 2025, a major European foodservice distributor entered into a strategic alliance with an Asian manufacturer, boosting compostable packaging penetration in Europe’s hospitality sector. This cross-regional partnership highlights the importance of scalable supply chains to meet surging demand.

In April 2025, a leading U.S. fast-food chain piloted sugarcane clamshells in California, signaling a decisive shift away from plastics in quick-service dining. Similarly, January 2025 marked a wave of new developments: an Indian automated molding facility achieved a capacity of over 50 million units per month, a UK QSR brand committed entirely to bagasse takeout bowls, and a multinational packaging company unveiled bagasse-bamboo blended molded fiber with enhanced durability. Each of these milestones points to scalability and diversification as central growth drivers.

On the innovation front, March 2025 saw an Australian startup secure funding for R&D into high-performance bagasse with natural moisture barriers. Meanwhile, February 2025 government subsidies in Southeast Asia targeted bagasse manufacturing expansion, supporting a circular economy for agricultural byproducts. Additionally, dry-molded fiber technology launched by a global packaging leader in January 2025 set a new standard for resource-efficient bagasse production, using significantly less water in molding processes.

Key Market Dynamics and Strategic Opportunities Driving the Bagasse Tableware Products Market

Legislative Phase-Out of Conventional Plastics Driving Mandatory Demand

Government regulations are the foremost driver for bagasse tableware adoption, creating non-discretionary demand for sustainable alternatives. Global single-use plastic (SUP) bans, such as India’s Plastic Waste Management Amendment Rules, 2021, prohibit items like plates, cups, and cutlery, while similar mandates exist across the EU and U.S. states like California and New York. Governments are also promoting alternatives through initiatives like India’s “India Plastic Challenge – Hackathon 2021,” which supports startups developing plant-based solutions. Granular regulations, such as India’s Single-use Plastic (Regulation) Act, 2024, with time-bound targets for eliminating plastics by 2025, further accelerate the transition across the supply chain. These policies make bagasse tableware a regulatory-compliant and commercially essential choice for businesses worldwide.

Corporate Sustainability Pledges Creating High-Volume B2B Contracts

Major global QSRs and FMCG companies are translating sustainability pledges into high-volume procurement of bagasse tableware. Brands such as McDonald’s, Starbucks, and KFC are actively integrating bagasse packaging to meet ESG targets, ensuring compliance with corporate sustainability goals. The shift involves large-scale, reliable contracts, exemplified by a U.S. meal kit brand reporting 28-day door-to-door lead times for bagasse products. Beyond compliance, adoption of bagasse aligns with circular economy principles: Life Cycle Analysis (LCA) studies indicate 50–70% lower environmental impact compared to single-use plastics, providing quantifiable metrics for corporate sustainability reporting.

Development of Heat-Resistant and Grease-Barrier Coatings Without PFAS

A significant growth opportunity exists in engineering next-generation bagasse products capable of handling hot and greasy foods without using PFAS (“forever chemicals”). Regulatory restrictions on PFAS across multiple U.S. states have catalyzed research into bio-based, non-toxic alternatives, such as the EU-funded “ZeroF” project. Emerging coatings, like a graphene oxide solution developed by a Northwestern University startup, not only provide water and oil resistance but also enhance paper strength by 30–50%, delivering high-performance, sustainable alternatives. Advanced heat-resistant coatings allow bagasse products to maintain integrity with hot foods, offering safe, functional, and environmentally responsible packaging solutions.

Expansion into Industrial and Airline Catering Sectors with Customized Formats

The industrial catering and airline sectors represent a high-value growth opportunity for bagasse tableware. Airlines seeking to reduce plastic use have adopted sugarcane bagasse plates and meal boxes, improving sustainability credentials while maintaining product quality. Industrial catering, corporate cafeterias, schools, and hospitals require large-volume, custom solutions like multi-compartment trays, stackable containers, and tailored meal boxes to fit operational systems. Supplying these sectors provides stable, high-volume contracts, supported by the growing food delivery, catering, and takeaway markets. Customization and reliability in production position manufacturers to capitalize on this expanding B2B market segment.

Competitive Landscape: Key Companies in the Bagasse Tableware Products Market

The competitive landscape is defined by packaging multinationals and specialized eco-friendly brands, each advancing the sector through sustainable innovation, certifications, and capacity expansions.

Huhtamaki Oyj – scaling molded fiber and compostable solutions

Huhtamaki leads with its Chinet Classic® and Envirable® lines, both BPI-certified compostable. In 2025, the company advanced its portfolio with the Bioware fiber lid, a natural fiber-based, compostable alternative to plastic. Backed by global distribution networks and investments in production scale, Huhtamaki integrates recycled PET and plant-based polymers into operations, strengthening its role as a comprehensive eco-packaging provider.

Duni Group – BioPak innovation for foodservice packaging

Through its BioPak brand, Duni Group delivers bagasse bowls and trays, including its flagship Octabagasse line. Recent innovations include the 2-compartment Octabagasse bowl, tailored for fast-casual dining. Operating with a vertically integrated supply chain, Duni ensures end-to-end quality while maintaining its circular economy commitment. Its strong design identity and emphasis on sustainable dining experiences reinforce its leadership.

Pactiv Evergreen Inc. – broad sustainable portfolio under EarthChoice®

Pactiv Evergreen markets its bagasse products under the EarthChoice® brand, with offerings designed for commercial compostability. The company promotes its Greenware® range, supporting waste diversion goals for foodservice operators. Widely adopted in on-the-go foodservice, EarthChoice® aligns with consumer demand for convenient yet sustainable packaging. Its strength lies in providing full-spectrum foodservice solutions, spanning both conventional and biodegradable packaging.

Dart Container Corporation – Solo® brand pushing PFAS-free innovation

Dart Container’s Solo® brand offers compostable hinged containers and PFAS-free bagasse products. Known for their cut-resistant and leak-resistant qualities, these containers meet evolving food safety and environmental regulations. The company’s strategic PFAS-free focus responds to global restrictions on chemical additives, while Solo®’s long-standing brand recognition ensures strong acceptance in both retail and foodservice channels.

Green Paper Products – niche player in 100% compostables

Green Paper Products specializes exclusively in certified compostable bagasse tableware. Its plates, bowls, and cups are designed to meet strict industrial composting standards, making it a preferred partner for zero-waste initiatives across catering, institutional foodservice, and eco-conscious businesses. The company’s niche focus and credibility in compostable certifications make it a trusted supplier in the B2B eco-disposables space.

Bagasse Tableware Products Market Share Insights

Plates Dominate Market Share by Product Type in Bagasse Tableware Products Industry

Plates account for the largest share of the bagasse tableware products industry at 28%, underscoring their role as the universal format across global foodservice. Their flat, simple geometry makes them cost-efficient to manufacture at scale using pulp molding technology, while their versatility allows them to serve both dine-in and takeaway channels. Regulatory bans on plastic plates in the EU, India, and several U.S. states have accelerated adoption, with bagasse plates positioned as the most readily available compostable alternative. Their high heat resistance, microwave safety, and ability to handle greasy foods without leakage make them indispensable in catering, quick-service restaurants, and institutional dining. This dominant position is further cemented by the growing integration of bagasse plates in retail multipacks sold in supermarkets for events and outdoor use, ensuring high visibility and steady volume demand.

Clamshells Capture Market Share by Enabling the Food-to-Go Economy

Clamshells represent the second-largest product type with 22% of the market, driven by the exponential growth of takeaway and delivery platforms like Uber Eats, DoorDash, and Deliveroo. Their hinged-lid format offers superior protection for burgers, sandwiches, salads, and entrees, ensuring spill-free transport during last-mile delivery. Regulatory crackdowns on polystyrene foam clamshells have catalyzed demand for bagasse-based alternatives, particularly in North America and Europe where QSRs face mounting pressure to demonstrate ESG compliance. Their share is also reinforced by urban food consumption trends, where portability, single-use convenience, and tamper-evident sealing are critical. The strength-to-weight ratio of bagasse clamshells makes them viable for both hot and cold foods, further entrenching their role as the packaging backbone of the global food-to-go sector.

Food Service Commands Market Share by End-Use in Bagasse Tableware Industry

The food service sector consumes an overwhelming 75% of bagasse tableware, reflecting the alignment of its sustainability features with the needs of restaurants, cafes, food trucks, and caterers. This dominance is structurally reinforced by municipal and state-level bans on single-use plastics in the U.S., Canada, and Europe, which directly target disposable food packaging. Chain restaurants are shifting procurement policies to include certified compostable products, with bagasse leading adoption due to its balance of cost, performance, and availability. High-volume institutional catering such as stadiums, universities, and corporate cafeterias amplifies this demand, as these organizations must comply with green procurement policies. The sector’s sheer consumption volume ensures it remains the industry’s innovation hub, driving developments in molded compartment trays, grease-resistant coatings, and premium embossing for branded experiences.

United States: Sustainability-Driven Growth in Bagasse Tableware

The U.S. bagasse tableware market is witnessing rapid growth due to stringent environmental regulations and increasing consumer demand for eco-friendly food packaging solutions. States like California are enforcing laws such as the Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54), mandating a shift toward recyclable and reusable tableware. Technological advancements, including automated molding systems and precision temperature control, are improving moisture resistance, rigidity, and consistency of bagasse products.

The rise of e-commerce and the growing food service sector, including restaurants and catering companies, is boosting the adoption of compostable and microwave-safe tableware. Leading corporations such as McDonald's, Starbucks, and KFC have integrated bagasse products to replace single-use plastics, aligning with sustainability goals. Additionally, manufacturers are reformulating products to be PFAS-free, responding to EPA regulations and rising consumer demand for chemical-free, biodegradable packaging.

Germany: Circular Economy and Regulatory Mandates Fuel Bagasse Adoption

Germany's bagasse tableware market is heavily shaped by the EU Packaging and Packaging Waste Regulation (PPWR) 2025, which enforces full recyclability and reuse targets. The country’s focus on a circular economy encourages manufacturers to innovate in sustainable materials and packaging design, ensuring products comply with stringent recyclability and environmental standards.

Technological innovation is advancing product capabilities, including recycled content integration and durable, microwave-safe tableware. Germany’s e-commerce and catering sectors are rapidly adopting bagasse solutions, reflecting rising eco-conscious consumer awareness. Manufacturers are responding with compostable, heat-resistant, and high-performance tableware, meeting both regulatory requirements and consumer expectations.

China: Government Policies and E-Commerce Expansion Driving Bagasse Tableware Market

China’s bagasse tableware market is influenced by the dual carbon policy, targeting carbon peak and carbon neutrality, which encourages the adoption of eco-friendly and reusable packaging. Manufacturers are investing in automation, AI, and 5G-enabled industrial technologies, optimizing production efficiency and flexibility.

Policies restricting non-degradable plastics, particularly in the express delivery and food sectors, are creating strong demand for lightweight, sustainable tableware. Domestic producers are innovating to improve mechanical properties and cost efficiencies, serving global export markets while meeting international compostability standards. Regulatory reforms under Made in China 2025 aim to increase domestic content in core materials to 70%, further strengthening local production capabilities.

India: Government Initiatives and Growing Urban Consumer Base Accelerate Market Expansion

India's bagasse tableware market benefits from initiatives like Make in India and Zero Effect Zero Defect, which promote quality domestic production and industrial infrastructure investments. The PLI Scheme for the food processing industry, with an outlay of INR 10,900 crore, incentivizes high-quality and standardized tableware manufacturing.

Rising disposable income, urbanization, and consumer preference for convenient, single-serve products are driving the adoption of eco-friendly tableware. The country’s abundant sugarcane production, especially in Uttar Pradesh, Gujarat, and Maharashtra, ensures a reliable supply of raw materials for bagasse products, enabling both domestic consumption and export opportunities. New regulations under the Plastic Waste Management (Amendment) Rules further stimulate demand for compostable and reusable packaging solutions.

Brazil: Sustainable Practices and Regulatory Push Fuel Bagasse Tableware Adoption

Brazil’s bagasse tableware market is expanding under the National Solid Waste Policy (PNRS), which promotes a circular economy and mandates recycling, reuse, and waste reduction. Technological advancements, including AI and robotics, are enhancing manufacturing efficiency, quality control, and defect detection in production lines.

Sustainability initiatives, including a ban on imported solid waste, are driving innovation in eco-friendly packaging materials. Investments in new facilities and supply chain traceability are fortifying the food and beverage sector, with bagasse tableware emerging as a preferred sustainable alternative. The Brazilian market emphasizes durable, reusable, and compostable products, aligning with both regulatory compliance and consumer demand for green solutions.

Japan: Bio-Based Materials and High-Performance Innovations Lead Market Growth

Japan’s bagasse tableware market is being transformed by advanced recycling systems and regulatory policies that encourage bio-based and reusable packaging. Under the Containers and Packaging Recycling Law, businesses are responsible for collecting and repurposing plastics and glass, creating a robust recycling infrastructure.

New updates under the Food Sanitation Act (2025) set stringent migration limits for synthetic resins, promoting safer and bio-based tableware. Companies such as LyondellBasell are integrating bio-based polypropylene in products for brands like Shiseido, highlighting a trend toward sustainable and high-performance packaging. Japanese manufacturers focus on dimensional stability, heat resistance, and deformation-free designs, meeting the needs of premium food service, catering, and institutional applications.

Bagasse Tableware Products Market Report Scope

Bagasse Tableware Products Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$323.7 Million

|

|

Market Size (2034)

|

$542.3 Million

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Product Type (Plates, Bowls, Clamshells, Containers, Cups & Lids, Cutlery, Trays), By Material (Sugarcane Bagasse Pulp, Wheat Straw, Bamboo, Palm Leaf, Other Natural Fibers), By End-Use Industry (Food Service, Retail, Households, Institutional), By Application (Commercial Use, Household Use, Institutional Use)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamaki Oyj, Novolex, Dart Container Corporation, Pactiv Evergreen Inc., Vegware, Eco-Products, Inc., DS Smith plc, Sustainables, BioPak, Genpak LLC, Bionatic GmbH & Co. KG, Biotrem, PAPSTAR, Sumkoka, Growood

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bagasse Tableware Products Market Segmentation

By Product Type

- Plates

- Bowls

- Clamshells

- Containers

- Cups & Lids

- Cutlery

- Trays

By Material

- Sugarcane Bagasse Pulp

- Wheat Straw

- Bamboo

- Palm Leaf

- Other Natural Fibers

By End-Use Industry

- Food Service

- Retail

- Households

- Institutional

By Application

- Commercial Use

- Household Use

- Institutional Use

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bagasse Tableware Products Market

- Huhtamaki Oyj

- Novolex

- Dart Container Corporation

- Pactiv Evergreen Inc.

- Vegware

- Eco-Products, Inc.

- DS Smith plc

- Sustainables

- BioPak

- Genpak LLC

- Bionatic GmbH & Co. KG

- Biotrem

- PAPSTAR

- Sumkoka

- Growood

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive, multi-faceted research approach to analyze the global Bagasse Tableware Products Market, integrating primary interviews with industry leaders, manufacturers, distributors, and foodservice operators alongside secondary research from government policies, regulatory frameworks, corporate sustainability reports, trade journals, and market press releases. Our methodology focused on evaluating the impact of single-use plastic bans, innovations in molded fiber technologies, and the integration of bio-based coatings such as PFAS-free, oil- and water-resistant solutions. Market sizing and forecasts were derived from historical growth trends, adoption rates across regions including North America, Europe, Asia-Pacific, India, Brazil, and Japan, and consumption patterns across food service, retail, household, and institutional sectors. Segmentation analysis covered product type, raw material, end-use industry, and application, while competitive intelligence examined key players such as Huhtamaki Oyj, Dart Container Corporation, Duni Group, and Pactiv Evergreen Inc., assessing their product innovations, sustainability commitments, and capacity expansions. Additionally, USDAnalytics incorporated strategic opportunities arising from airline and industrial catering adoption, cross-regional partnerships, and emerging technologies like dry-molded fiber and moisture-barrier coatings, ensuring a robust, data-driven assessment tailored for industry professionals seeking actionable insights into growth drivers, regulatory compliance, and market dynamics.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.