Ballistic Protective Equipment Market Overview: Lightweight Armor Systems, Multi-Hit Survivability & Next-Gen NIJ Compliance Driving Global Demand

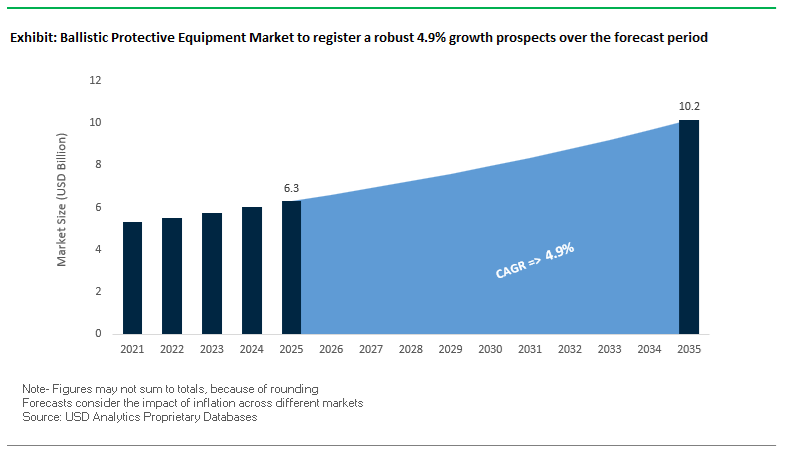

The Ballistic Protective Equipment Market, valued at USD 6.3 billion in 2025 and projected to reach USD 10.2 billion by 2035 at a steady 4.9% CAGR, is entering one of its most significant modernization cycles in decades. Fueled by soldier-system digitalization, stricter NIJ 0101.07 standards, and global defense mobility requirements, the industry is shifting toward lightweight, multi-hit–capable, ergonomically optimized protection systems. Defense forces and law enforcement agencies are rapidly adopting advanced aramid fibers (Kevlar® EXO™), next-generation UHMWPE systems (Dyneema®), and ceramic-graphene hybrid plates, all engineered to reduce weight while enhancing ballistic stopping power, blunt-force mitigation, and long-duration wearability.

This performance shift is redefining procurement criteria: legacy aramid inserts are being replaced with soft armor that is up to 40% lighter, helmets are setting new global benchmarks with the ability to stop hard steel-core AK-47 rounds, and transparent armor solutions now provide A12/CEN B7+ protection against .50 BMG threats at high velocity. Ceramic-graphene hybrid plates—capable of defeating multi-hit 7.62 mm AP rounds at nearly one-third the thickness of traditional ceramics—offer a decisive advantage in weight-sensitive missions, enabling operators to carry additional sensors, communications gear, or ammunition without exceeding load limits. Combined with rising geopolitical tensions and increased defense spending, the next decade positions ballistic protective equipment as a mission-critical category for governments, OEMs, and tactical integrators.

Market Analysis: Material Breakthroughs, Defense Contracts and NIJ .07-Driven Modernization

The Ballistic Protective Equipment Market is being reshaped by both material science innovations and large defense procurement cycles, all converging around the new NIJ 0101.07 standard. In November 2025, DuPont™ Kevlar® EXO™ received a 2025 Edison Award, formally recognizing it as a breakthrough aramid fiber for ballistic and thermal performance. The award underscores industry validation that EXO™ is not just an incremental improvement, but a platform shift in soft armor design, enabling up to 40% weight reduction and dramatic gains in flexibility and comfort. In parallel, July 2025 saw SMPP secure dual contracts valued at ₹300 crore (USD 36 million) from the Indian Army for 27,700 bulletproof jackets and 11,700 advanced ballistic helmets, underlining a strong trend toward indigenous soldier protection solutions and confirming early adoption of cutting-edge helmet capabilities against AK-47 threats.

In July 2025, Avient (Dyneema®) launched HB330 and HB332 unidirectional materials for hard ballistic protection, enabling up to 45% weight reduction in plates and shields compared with legacy systems. The same month, Safe Pro Group secured a contract to deliver ballistic protection and EOD equipment for Indo-Asia Pacific operations, highlighting ongoing demand from active theaters requiring specialized protective kits. Earlier in the cycle, October 2024 brought the launch of D3O Ballistic foam by Delta Three Oscar, explicitly designed to help armor manufacturers meet NIJ 0101.07 backface and blunt-impact criteria while preserving mobility.

Procurement momentum from U.S. programs continues to underpin market growth. In April 2024, the U.S. Department of Defense awarded USD 190 million to Safariland for next-generation soft armor vests meeting stricter flexibility and protection requirements. In March 2024, Point Blank Enterprises secured a USD 215 million contract from the U.S. Army for modular body armor systems, now serving as a key channel for deployment of Kevlar® EXO™-based solutions through its exclusive partnership with DuPont. Complementing torso protection, February 2024 saw Avon Protection receive a USD 204 million Direct OEM contract extension for the Integrated Head Protection System (IHPS), locking in long-term supply of advanced combat helmets.

Key Trends Transforming the Ballistic Protective Equipment Market

Trend 1: Integration of Ballistic Protection with Power, Data, and Sensor Systems to Enable the “Connected Soldier” Market

Modern soldier modernization programs—from the U.S. Integrated Visual Augmentation System (IVAS) to NATO Future Soldier initiatives—are shifting ballistic protective equipment from passive armor to active digital nodes that power, connect, and support mission-critical electronics. Today’s dismounted soldiers routinely carry multiple radios, night-vision systems, GPS receivers, and edge-computing devices, resulting in a battery load of nearly 15 pounds (~6.8 kg) per mission. Integrated Soldier Power & Data Systems (ISPDS) aim to consolidate these power requirements through a centralized hub embedded in the vest or pack, reducing battery carriage by up to 30%, enhancing operational endurance, and lowering physical burden.

This intelligent architecture extends beyond power-sharing. Body armor platforms are increasingly equipped with embedded biosensors capturing metrics such as heart rate variability, thermal stress, and hydration levels. Early field deployments show that machine-learning models using these data streams can reduce overexertion-induced mission halts by approximately 18%, illustrating how physiological analytics can materially improve soldier readiness. The push toward a unified “smart hub” in BPE also simplifies cabling, transitioning from multiple uncoordinated data pathways to a streamlined digital backbone supporting Ethernet or USB-based protocols. This integrated digital layer not only reduces wiring complexity but also ensures consistent device interoperability during high-intensity operations. As battlefield electronics proliferate, the connected soldier ecosystem will fundamentally reshape BPE design, procurement, and performance specifications.

Trend 2: Mandatory Adoption of Female-Specific Body Armor Designs to Eliminate Fit and Protection Gaps

One of the fastest-growing structural shifts in the ballistic protective equipment market is the mandated transition toward female-specific body armor, correcting decades-long reliance on male-scaled sizing that compromised mobility and protection for women in service. Modern programs rely on detailed anthropometric datasets—most notably the U.S. Army’s ANSUR II 3D body-scan database—to design armor geometries that conform to the unique shape and dimensions of female soldiers. These datasets enable refinements such as contoured plate curvature, reduced underarm bulk, and improved torso coverage, directly addressing legacy gaps that contributed to discomfort, restricted mobility, and exposed vital areas.

As women now represent over 15% of U.S. Army personnel and an increasing share of frontline and combat-adjacent roles globally, procurement standards are being rewritten. The Female Body Armor Modernization Act and similar mandates across NATO nations ensure dedicated R&D funding, contract obligations, and production lines for gender-specific armor. Manufacturers are now required to integrate ergonomic shaping, improved belt-line mobility, and enhanced sternum clearance to ensure both ballistic performance and biomechanical compatibility. This trend elevates anthropometric precision to a core differentiator in the BPE market, directly influencing procurement wins and long-term supplier relationships across defense ministries.

High-Value Opportunities Emerging in the Ballistic Protective Equipment Market

Opportunity 1: Next-Generation Helmet Liner Materials for Superior Blast, Impact, and Rotational Force Mitigation

Traumatic Brain Injury (TBI) remains one of the most critical survivability challenges in modern warfare, especially in environments defined by IEDs, blast overpressure, and secondary fragmentation. This opens a significant opportunity for advanced helmet liner materials that surpass the capabilities of traditional EPS foam through improved energy absorption and rotational force mitigation. Emerging liner architectures—based on auxetic metamaterials, fluid-filled channels, and multi-phase structures—are engineered to deform in highly controlled ways, dissipating force more effectively and reducing transmitted peak overpressure to the skull.

Shock-tube testing has shown that liners incorporating fluid or viscoelastic fillers significantly outperform solid foam constructions in suppressing blast overpressure, addressing the primary injury mechanism associated with close-range explosive threats. At the same time, R&D in functionally graded porosity has demonstrated powerful performance gains, with chiral metamaterials delivering 2× to 32× greater energy absorption per unit mass than uniform lattices. These innovations represent the next frontier in protective headgear, enabling military organizations to meet stricter TBI mitigation requirements while maintaining or reducing total helmet weight. The acceleration of blast research and the global rise in asymmetric conflict environments ensure that advanced liner technologies will remain a priority investment domain.

Opportunity 2: Additively Manufactured Ceramic-Composite Hybrid Armor for Rapid, Modular, and Mission-Specific Hard Plate Development

Additive manufacturing is unlocking a new generation of ceramic-composite hybrid hard armor plates that outperform conventional monolithic tile arrays through geometric innovation and functional grading. AM techniques such as stereolithography (SLA) and vat photopolymerization (VPP) allow manufacturers to produce bio-inspired geometries—hexagonal, spherical crown, and interlocking cellular architectures—that redirect projectile penetration paths. Simulation results show that optimized tile configurations can improve penetration resistance by up to 85.11% compared to conventional strike-face arrangements, offering a step-change in protective efficiency without increasing mass.

AM also enables functionally graded (FG) ceramic armor, in which hardness, fracture toughness, and internal porosity vary across layers to better manage shock propagation. This reduces internal stresses, minimizes surface cracking, and improves multi-hit survivability—key performance metrics for next-generation plates. The ability to print ceramic green bodies in under 20 minutes per tile further transforms the design-to-field cycle, enabling rapid prototyping, mission-specific iteration, and localized manufacturing for deployed units.

As defense agencies prioritize modularity, scalability, and rapid response to evolving threats, additively manufactured ceramic-composite armor systems present one of the most commercially promising growth vectors in the ballistic protective equipment market.

Ballistic Protective Equipment Market Share Analysis

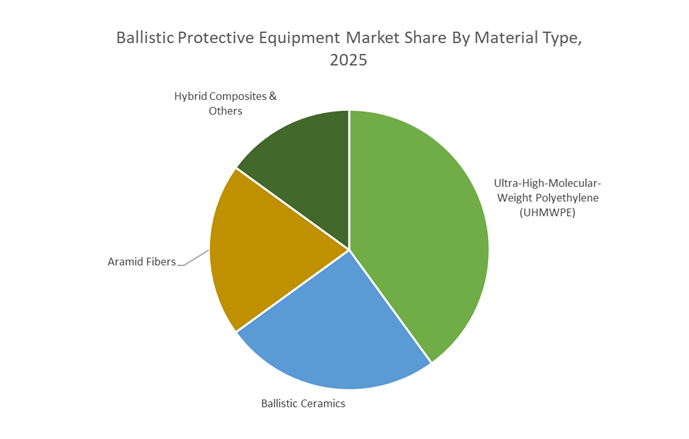

Market Share by Material Type: UHMWPE Leads with 39.6% Share

Ultra-High-Molecular-Weight Polyethylene (UHMWPE) holds the largest share of the Ballistic Protective Equipment Market at 39.6% in 2025, reflecting its position as the premium material for next-generation lightweight armor solutions. Its dominance is driven by the sector’s top procurement priority—maximizing protection while minimizing weight burden, especially for soldiers and law enforcement personnel who require extended-wear comfort and high mobility. UHMWPE’s exceptional energy absorption, tensile strength, buoyancy, and fatigue resistance make it the preferred choice for ballistic plates, helmets, and soft armor panels, accelerating its replacement of traditional aramid-based systems. This shift mirrors a broader materials evolution, where lighter, stronger, and more adaptable polymers outperform legacy fibers in multi-hit and high-velocity threat scenarios. Across the material ecosystem, ballistic ceramics remain indispensable as strike-face materials in hard armor plates; aramid fibers maintain relevance in soft armor and spall liners but are losing share to UHMWPE; and hybrid composites emerge as the engineering solution for complex, multidirectional threat environments. Collectively, these dynamics highlight a market transitioning decisively toward ultra-lightweight, hybridized protection platforms built for modern combat and security operations.

Market Share by Product Type: Hard Armor Leads with 35.4% Share

Hard Armor—primarily ballistic plates and plate carriers—leads the market with a 35.4% share in 2025, underscoring its role as the highest-value, most technologically intensive product category in the ballistic protection landscape. This segment commands a dominant share because it delivers critical rifle-rated protection, where even marginal performance gains in multi-hit capability, weight reduction, ceramic–polymer hybrid construction, and trauma mitigation significantly influence procurement decisions across military, law enforcement, and special forces communities. Hard armor plates represent the apex of material innovation, integrating ceramics, UHMWPE backers, and advanced composite layups to address increasingly sophisticated ammunition threats. Supporting categories shape the industry’s recurring revenue dynamics: soft body armor forms the replacement-driven backbone of the installed base; ballistic helmets are transforming into multi-function headborne systems incorporating sensors, communications, and mounting platforms; and vehicle armor remains essential as militaries adopt lighter, more modular tactical fleets requiring scalable protection kits. The product segmentation illustrates how hard armor remains the strategic center of market innovation, while complementary equipment categories sustain long-term demand cycles.

Country Analysis: Global Ballistic Protective Equipment Market Innovation Hubs

United States: Leadership in Lightweight Ballistic Armor, NIJ Standards, and Soldier System Modernization

The United States remains the world’s anchor for ballistic protective equipment innovation, supported by unmatched defense procurement, industry-leading standards development, and accelerated adoption of next-generation soldier systems. In February 2024, the U.S. Army Contracting Command awarded Avon Protection plc a $204 million IHPS Direct OEM contract, enabling streamlined production of advanced combat helmets and soft armor vests designed under the Integrated Head Protection System (IHPS) program. Complementing head protection modernization, Point Blank Enterprises secured a $215 million modular body armor contract (March 2024) to supply scalable, mobility-enhancing vest systems engineered to reduce user burden and increase flexibility for soldiers operating in multidomain combat environments.

A major structural shift in the U.S. law enforcement ecosystem is occurring with the national transition to the NIJ 0101.07 ballistic standard, published in late 2023. As certifications began in 2024, this standard is driving an extensive replacement cycle for both soft body armor and rifle-rated plates across U.S. police agencies, accelerating demand for high-performance Level III and Level IV armor solutions. The material science landscape is evolving rapidly as well: Avient’s Dyneema division launched its HB330 and HB332 UHMWPE unidirectional (UD) composites in January 2025, offering ~45% weight reduction in hard armor systems—underscoring the U.S.’s central role in lightweight armor technology. With the FY 2025 President’s Budget prioritizing modernization through RDT&E and procurement, the U.S. is solidifying its position as the global benchmark for advanced soldier protection equipment and high-performance ballistic materials.

Poland (Europe): Defense Spending Surge and Rapid Expansion of Ballistic Equipment Procurement

Poland has emerged as one of Europe’s fastest-growing markets for ballistic protective equipment, driven by geopolitical urgency and its strategic role on NATO’s eastern flank. Poland’s military spending rose 31% to $38.0 billion in 2024, equivalent to 4.2% of national GDP, creating one of the most aggressive procurement environments in Europe. This surge is directly fueling large-volume acquisitions of helmets, modular vests, body armor plates, and soldier-carried ballistic systems.

Beyond military modernization, Poland is expanding ballistic protection orders across civil defense and population protection programs. Municipalities such as Plock issued tenders in late 2025 for Type 2 soft bulletproof vests under provincial civil defense initiatives, indicating strong non-military growth segments. Simultaneously, the Border Guard Headquarters launched a tender in September 2025 for internal and external bulletproof vests, reinforcing demand for modern protective solutions across homeland security. Poland’s sustained commitment to defense spending exceeding 4% of GDP highlights ongoing demand for NATO-compatible ballistic helmets, carrier platforms, and lightweight armor technologies, fortifying its role as a critical European innovation hub for protective systems.

India: Aatmanirbhar Bharat Driving High-Volume Domestic Ballistic Vest Production and Indigenous Lightweight Armor Technologies

India is rapidly strengthening its domestic capabilities in ballistic protective equipment, with the government’s Aatmanirbhar Bharat policy accelerating indigenous manufacturing, R&D, and procurement cycles. The Ministry of Defence placed a major order for 27,700 bulletproof vests in July 2025, following an earlier procurement of 186,138 vests, signaling a consistent and large-scale purchasing pattern supporting local industry growth. Parallel to procurement, India’s R&D ecosystem is maturing: the DRDO–IIT Delhi-developed ABHED jackets, particularly the BIS V variant weighing no more than 8.2 kg, represent a milestone in India’s quest to produce lightweight, high-performance ballistic vests comparable to global standards.

Specialized protective equipment procurement is expanding as well. In December 2025, the Border Security Force released tenders for Bomb Blankets compliant with MHA QR (V2) specifications, highlighting increasing investment in fragmentation protection for counter-insurgency, border security, and internal safety operations. Government-led industrial programs, including Defense Industrial Corridors, are accelerating capacity-building in ballistic plate manufacturing, ceramic strike-face production, and vest assembly. With rising domestic capability and consistent procurement, India is quickly evolving into a significant hub for cost-efficient, high-performance ballistic vests, helmets, and fragmentation protection solutions.

Taiwan: Strategic Emphasis on ESAPI-Level Ceramic Armor and NIJ-Compliant Law Enforcement Protection

Taiwan continues to enhance its national defense posture through high-end procurement of advanced ceramic armor plates designed for the highest levels of rifle threat protection. The government is preparing to procure new boron carbide ballistic plates for 2028–2029, chosen for their exceptionally low density and extreme hardness—essential properties for Level IV / ESAPI-grade armor capable of defeating 7.62mm armor-piercing rounds. This focus aligns with Taiwan’s strategic need for lightweight, high-performance materials suited for mobile, rapid-response defense operations.

The National Police Agency (NPA) is concurrently modernizing its protective equipment by shifting from “lowest bidder” procurement to a “most advantageous tender” framework, ensuring higher quality and strict adherence to U.S. NIJ ballistic resistance standards. The NPA’s 2024 procurement cycle introduced new functionality enhancements, including size S availability and MOLLE-compatible outer carriers, demonstrating a shift toward modular, customizable, officer-centric design. Taiwan’s sustained investment in ceramic armor and NIJ-compliant protective systems positions it as a strategically important user and evaluator of high-end ballistic protective technologies.

Ukraine: Wartime Demand Driving Domestic Ballistic Production and Intense NATO Supply Chain Utilization

Ukraine’s ongoing conflict has reshaped the global market for ballistic protective equipment, creating unprecedented demand for helmets, vests, plates, spall liners, and fragmentation-resistant systems. To ensure supply continuity, Ukraine significantly shifted toward domestic production, with the Ministry of Defense reporting in August 2024 that over 80% of materiel contracts had been awarded to Ukrainian manufacturers following the establishment of a State Logistics Operator. This pivot has fueled rapid development in local production capacities for hard armor plates, soft armor carriers, and composite helmet systems.

NATO allies remain under pressure to backfill their own strategic reserves while simultaneously supplying Ukraine with essential protective equipment, tightening the European and U.S. supply chains for key materials such as ceramic strike faces, UHMWPE backers, and aramid fabrics. This environment has reinforced the rapid evolution of Ukraine’s protective equipment ecosystem, driven by urgent operational needs and accelerated procurement cycles. As a result, Ukraine has become a critical influencer in global demand patterns, technology deployment speed, and supply chain resilience for ballistic armor systems.

Competitive Landscape: Leading Aramid, UHMWPE and Integrated System Providers in Ballistic Protective Equipment

The competitive landscape in the Ballistic Protective Equipment Market is anchored by a small group of material science leaders and integrators that control critical technologies across aramid fibers, UHMWPE, advanced ceramics, modular armor systems and head protection. Differentiation now centers on weight reduction, wearability, multi-hit capability, NIJ 0101.07 readiness and system-level integration (vests, plates, helmets and carriers). Below is an overview of key players and their strategic focus.

DuPont de Nemours, Inc. - Kevlar® EXO™ redefining soft armor comfort and durability

DuPont is the foundational supplier of aramid ballistic fabrics, and with Kevlar® EXO™ it has redefined the performance envelope for soft body armor. EXO™ is engineered to be significantly more flexible, requiring 50% less energy to bend and exerting 50% less pressure on the body than traditional aramid armor, which directly improves mobility and reduces fatigue. The fiber retains ballistic performance after five years of use and is inherently flame-resistant, decomposing above 500°C, making it ideal for high-risk tactical environments. DuPont’s exclusive partnership with Point Blank Enterprises (Jan 2025) ensures rapid system-level deployment of EXO™ in next-generation vests.

Avient Corporation (Dyneema®) - UHMWPE innovations driving ultra-light hard armor and carriers

Avient, through Dyneema®, dominates the UHMWPE space for ballistic applications, providing solutions for both soft and hard armor. The launch of Dyneema HB330 and HB332 in July 2025 targets hard armor plates and shields with up to 45% weight savings, while retaining or improving ballistic stopping power. Dyneema® is 15× stronger than steel by weight, and its woven composites offer up to 10× more abrasion resistance for tactical carriers and gear. By combining extreme strength-to-weight ratios with bio-based fiber options in certain grades, Avient supports both operational and sustainability objectives for modern ballistic protection systems.

Point Blank Enterprises - System integrator for EXO™-based soft armor and modular vests

Point Blank Enterprises is a leading manufacturer and assembler of soft and hard body armor as well as full protective systems for global defense and law enforcement. Its USD 215 million contract (March 2024) with the U.S. Army for modular body armor systems (MBAV) validates its large-scale production and integration capabilities. As one of the first to market with soft armor solutions based on Kevlar® EXO™, through its exclusive partnership with DuPont, Point Blank is uniquely positioned to deliver lighter, more flexible and NIJ .07-compliant vests at volume, supporting both domestic and international modernization programs.

3M Company (Ceradyne) - Advanced ceramic plates and transparent armor for multi-hit protection

3M, via its Ceradyne division, supplies advanced Boron Carbide (B4C) and Silicon Carbide (SiC) components for ESAPI plates and vehicle armor. Ceradyne’s IMP/ACT plate series incorporates a stainless steel crack arrestor between the ceramic strike face and backer, significantly improving multi-hit performance against rifle threats such as 5.56 mm M855. 3M’s strength lies in integrating specialized ceramics into lightweight, multi-hit capable hard armor and transparent armor systems for military and law enforcement users requiring high mobility and survivability.

Avon Protection plc - IHPS combat helmets and integrated head protection systems

Avon Protection is a global provider of head protection and respiratory systems, with its IHPS combat helmet program being a cornerstone of modern soldier survivability. The USD 204 million Direct OEM contract (February 2024) from the U.S. Army confirms multi-year demand for its next-generation helmets. The IHPS solution integrates ballistic, blunt-impact and fragmentation protection with modularity for optics, night vision and communications, making Avon a critical player in the head protection segment of the ballistic protective equipment market.

Safariland, LLC - NIJ .07-aligned soft armor vests and tactical carriers for law enforcement and defense

Safariland is a long-established supplier of body armor, shields and tactical gear for U.S. and international law enforcement and military agencies. The USD 190 million contract (April 2024) from the U.S. DoD for next-generation soft armor vests underscores its capability to design and deliver solutions aligned with NIJ 0101.07 requirements, focusing on improved flexibility and protection. Its broad portfolio, including carriers, shields and specialty armor, positions Safariland as a critical vendor for agencies transitioning to updated ballistic standards.

Ballistic Protective Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.3 Billion

|

|

Market Size (2035)

|

$10.2 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Material Type (UHMWPE, Ballistic Ceramics, Hybrid Composites, Specialized Glass Laminates, Steel Alloys), By Product Type (Soft Body Armor, Hard Armor, Head Protection, Ballistic Shields, Vehicle Armor, Infrastructure Protection), By Protection Standard/Level (NIJ Standards, STANAG, V50 Fragmentation), By End User (Military & Defense Forces, Law Enforcement & Homeland Security, Private Security Firms, Civilian), By Application Type (Tactical Gear, Concealed Protection, Multi-Threat Protection, Fragmentation Protection)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avient Corporation, DuPont de Nemours Inc., Point Blank Enterprises Inc., Safariland LLC, Avon Protection plc, BAE Systems plc, Honeywell International Inc., Teijin Limited, Morgan Advanced Materials plc, Hardwire LLC, MKU Limited, Armor Express, NP Aerospace, Integris Composites, Rheinmetall AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ballistic Protective Equipment Market Segmentation

By Material Type

- Ultra-High-Molecular-Weight Polyethylene

- Ballistic Ceramics

- Hybrid Composites

- Specialized Glass Laminates

- Steel Alloys

By Product Type

- Soft Body Armor

- Hard Armor

- Head Protection

- Ballistic Shields

- Vehicle Armor

- Infrastructure Protection

By Protection Standard / Level

- NIJ 0101.07 RF1 / RF2 / RF3

- NIJ 0101.07 HG1 / HG2

- NIJ Level III / III+

- NIJ Level IV

- STANAG

- V50 Fragmentation Standards

By End User

- Military & Defense Forces

- Law Enforcement & Homeland Security

- Private Security Firms

- Civilian

By Application Type

- Tactical Gear

- Concealed Protection

- Multi-Threat Protection

- Fragmentation Protection

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ballistic Protective Equipment Market

- Avient Corporation

- DuPont de Nemours, Inc.

- Point Blank Enterprises Inc.

- Safariland, LLC

- Avon Protection plc

- BAE Systems plc

- Honeywell International Inc.

- Teijin Limited

- Morgan Advanced Materials plc

- Hardwire LLC

- MKU Limited

- Armor Express

- NP Aerospace

- Integris Composites

- Rheinmetall AG

*- List not Exhaustive