Market Overview: Benzyl Benzoate Market Growth Driven by High-Purity Grades, Renewable Feedstocks, and Pharma Demand Expansion (2025–2034)

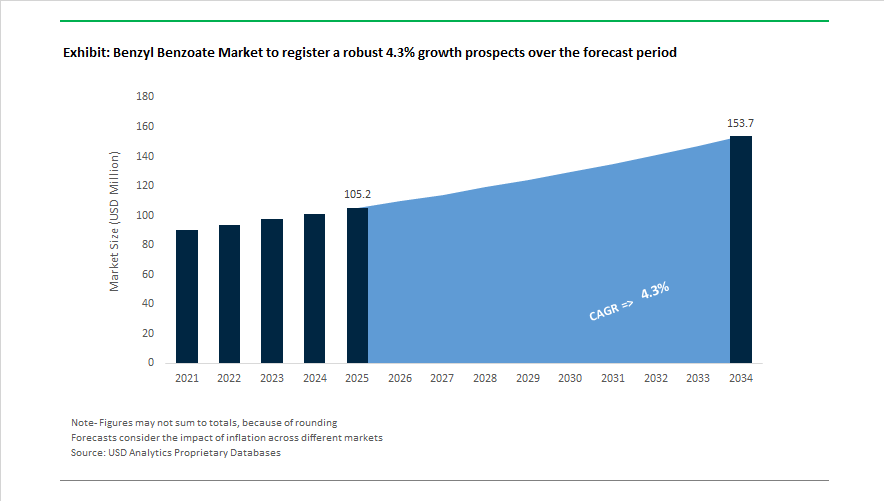

The benzyl benzoate market is projected to rise from USD 105.2 Million in 2025 to USD 153.7 Million by 2034, registering a CAGR of 4.3% , supported by expanding use in fragrance fixatives, cosmetic solvents, pharmaceutical excipients, and topical scabicide formulations. Benzyl benzoate serves as a key aromatic ester derived from benzoic acid and benzyl alcohol, linking upstream toluene chemistry with high-value downstream personal care, dermatology, and specialty chemical applications. Sustainability and purity differentiation began influencing competitive positioning in 2024. Between August 2023 and 2024, Sinteza S.A. commissioned an energy-efficiency waste-to-steam system to improve environmental performance in benzoic acid and ester production. In October 2024, Eastman Chemical expanded U.S. benzoic acid capacity, reinforcing domestic supply of a critical precursor for benzyl benzoate. In late 2024, Finar completed integration into Actylis, strengthening distribution of pharmaceutical-grade benzyl benzoate across Europe and Asia.

High-purity and renewable variants are reshaping product portfolios. In October 2024, Thermo Fisher Scientific introduced a 99% + purity benzyl benzoate grade aimed at analytical and drug formulation markets requiring ultra-low impurity profiles. In March 2025, LANXESS launched Kalama Ultrapure Scopeblue benzyl benzoate, certified under ISCC PLUS mass-balance standards to incorporate renewable feedstocks with reduced carbon intensity. The same month, LANXESS highlighted the role of benzyl benzoate as a stabilizing fixative alongside its Kalama Azuril fragrance platform, reinforcing demand from premium perfumery segments. Bio-based aromatic chemistry also advanced in March 2025 when BASF introduced fermentation-derived aroma molecules through its Isobionics line, signaling a gradual transition toward bio-synthetic aromatic supply chains that could influence benzyl benzoate production routes by the end of the decade.

Pharmaceutical demand and regional supply security remain strong drivers. The World Health Organization reaffirmed benzyl benzoate as an essential scabies treatment in its 2024 to 2025 health guidelines, stimulating procurement across developing regions. In July 2025, Gujarat Alkalies and Chemicals Limited began dispatching benzyl alcohol from its 30,000 MTPA Dahej facility, securing domestic precursor availability for Indian benzyl benzoate producers. In August 2025, Bausch Health Companies expanded Canadian public coverage for CABTREO dermatology therapy, indirectly raising demand for benzyl benzoate-containing excipient systems. Capacity expansion is also underway in China through Hubei Youji’s subsidiary Hubei Xinxuanhong, where Phase I for toluene chlorination derivatives started in late 2024 and Phase II is targeted for completion in the second half of 2026. Market access models are evolving as well. In December 2025, VedaOils launched a direct-to-manufacturer pure grade benzyl benzoate line for clean beauty and artisanal fragrance brands, reflecting demand diversification across premium, pharmaceutical, and specialty consumer sectors.

Trends and Opportunities Transforming the Benzyl Benzoate Market

Market Trend: Pharmaceutical-Grade Expansion Driven by cGMP and Biopharma Growth

The Benzyl Benzoate Market is experiencing a structural transition as biopharmaceutical supply chains increasingly demand USP and EP-compliant high-purity intermediates. This shift aligns with global cGMP enforcement, where benzyl benzoate is used as a pharmaceutical solvent in hormone injectables and as a stabilizer in parenteral delivery systems.

Throughout 2025, industry leaders including LANXESS and Spectrum Chemical invested in facilities capable of consistently delivering 99% or higher purity material. ISO 9001:2015 and cGMP protocol integration within U.S. and Japan-based facilities is enabling secure supply for steroidal APIs and antispasmodic manufacturing. Demand is quickly consolidating toward these grades, demonstrated by a 31% shift in global ordering patterns toward USP and EP-compliant formulations. For suppliers, this represents a margin expansion inflection point, as “pharma-only” capacity frequently sells at price points that are two to three times higher than industrial-grade equivalents.

Market Trend: EU Fragrance Allergen Policy Accelerating Cosmetic Reformulations

Cosmetic and personal care producers face a compliance deadline under EC Regulation 2023/1545, compelling brands to reassess formulations that use benzyl benzoate as a fragrance fixative. The amendment to Annex III expands allergen-listing obligations and mandates that benzyl benzoate be disclosed when exceeding 0.001% in leave-on products or 0.01% in rinse-off formats.

This regulatory evolution has become a commercial trigger. To retain EU market access beyond July 31, 2026, formulators are transitioning toward reduced concentrations or alternative fixatives to avoid mandatory allergen labeling, which impacts brand perception among clean-beauty consumers. Nearly one-third of incremental personal care product growth in 2025 is linked to reformulated SKUs marketed as dermatology-safe and allergen-aware. For benzyl benzoate suppliers, this dynamic signals a gradual volume shift away from fragrance-heavy applications and toward segments where purity and performance command premium pricing.

Market Opportunity: Leading Acaricide for Scabies and Public Health Interventions

Benzyl benzoate maintains a strategically important role in global public health, particularly in regions dealing with neglected tropical diseases. Its continued relevance is supported by comparative efficacy data: a 2025 meta-analysis published in Frontiers in Medicine found that 25% topical benzyl benzoate achieves cure rates similar to oral ivermectin for scabies.

The value driver lies in affordability and logistics. Benzyl benzoate is 30 to 50% cheaper per course than permethrin or ivermectin, and unlike oral treatments it allows direct topical deployment in emergency or low-resource settings. This makes it the preferred procurement item for health ministries, NGOs, and emergency response agencies in refugee camps and densely populated urban communities throughout Africa and Southeast Asia. The category is therefore insulated from typical cosmetic and industrial volume cycles, behaving more like a steady government-funded pharmaceutical commodity.

Market Opportunity: Plasticizer Functionality for High-Performance Polymers

Industrial and specialty manufacturing sectors represent a high-growth, high-margin niche, where benzyl benzoate is valued as a plasticizer with exceptional solvating power, transparency, and stability. In cellulose acetate, adoption has risen by about 28% in eyewear, hand tools, and premium consumer accessories, where manufacturers prioritize dimensional stability and glossy finishes over cost minimization.

Additionally, market traction is building behind bio-based benzyl benzoate variants produced using renewable benzoic acid feedstocks. Roughly 43% of new industrial launches in 2025 are tied to these formulations, targeting high-performance C.A.S.E. (Coatings, Adhesives, Sealants, Elastomers) applications where sustainability credentials are increasingly used as a procurement filter. As ESG-driven procurement expands, suppliers offering verified renewable sourcing and lifecycle carbon data have a significant competitive advantage.

Benzyl Benzoate Market Share and Segmentation Insights

Market Share by Grade: Flavor and Fragrance Leadership Supported by Rising Specialty Applications

Flavor and fragrance grade holds the largest share of the Benzyl Benzoate Market at 38% in 2025, reflecting its widespread use as a fixative and solvent in perfumery and as a synthetic flavoring agent in food and beverages. Its characteristic sweet, balsamic profile makes it a preferred ingredient in jasmine and ylang-ylang fragrance compositions, supporting consistent demand from premium personal care brands. Pharmaceutical grade represents a substantial secondary segment, driven by its use as a topical scabicide and pediculicide listed on the WHO Model List of Essential Medicines, alongside growing adoption as a penetration enhancer and plasticizer in dermatological formulations. Technical grade consumption remains steady across industrial applications, including cellulose plasticizers and chemical synthesis solvents, closely tracking manufacturing output. Specialty grade, while smallest by volume, is expanding fastest, fueled by high-purity requirements in advanced intermediates, electronic cleaning agents, and premium cosmetic formulations.

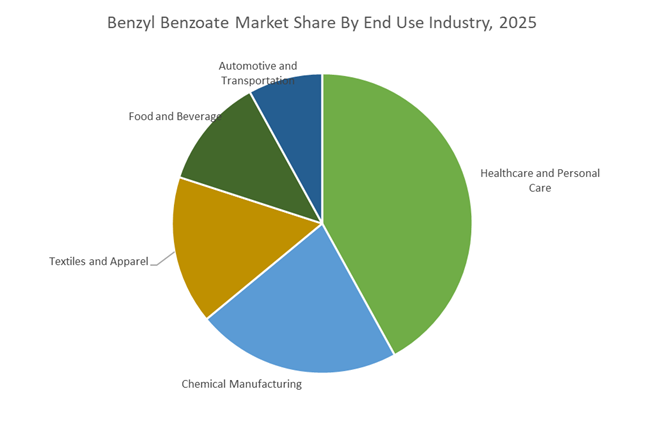

Market Share by End Use Industry: Healthcare and Personal Care Anchor Volume While Chemicals Sustain Baseline Demand

Healthcare and personal care dominate benzyl benzoate consumption with a 42% share in 2025, underpinned by stable pharmaceutical demand for scabies and lice treatments and accelerating growth in fragrances, lotions, and hair care products. Emerging markets with improving healthcare access represent key expansion corridors. Chemical manufacturing forms a critical downstream segment, utilizing benzyl benzoate as a solvent, plasticizer, and intermediate in cellulose processing, ink formulations, and specialty ester production. Textiles and apparel consume the compound as a dye carrier and leveling agent in polyester dyeing, with demand increasingly concentrated in Asia’s textile hubs amid tightening effluent regulations. Food and beverage applications account for flavor-grade volumes, supporting cherry, vanilla, and berry profiles, subject to regional regulatory limits despite FEMA GRAS status. Automotive and transportation remain niche, using benzyl benzoate in interior trim plasticizers and specialty lubricants, with growth linked to premium vehicle production.

Competitive Landscape Analysis of the Benzyl Benzoate Market

The benzyl benzoate market is defined by vertical integration across benzoic acid and benzyl alcohol value chains, purity differentiation between industrial and pharmaceutical grades, and growing demand from perfumery, personal care, agrochemical, and polymer applications. Leading producers compete on odor profile control, mass balance certified sustainable variants, regulatory compliance across USP, BP, EP, and JP standards, and multi-site supply resilience. Sustainability metrics such as renewable feedstock adoption, wastewater recovery, Scope 3 emission reduction, and green factory certification are increasingly influencing procurement decisions. Market leadership now hinges on distillation precision, feedstock security, and integration into fragrance, textile, coatings, and dermatological value chains.

LANXESS leads the global benzoate value chain through vertical integration and sustainable innovation

Following the acquisition of Emerald Kalama Chemical, LANXESS has established itself as the undisputed global leader in the benzyl benzoate market, backed by full backward integration into benzoic acid and benzyl alcohol. In 2025 and 2026, the company launched Ultrapure Scopeblue, a sustainable benzyl benzoate containing at least 50% renewable raw materials, certified under ISCC PLUS mass balance standards. Its portfolio includes Regular, Performance, Ultrapure, and Scopeblue grades, with nearly odorless Ultrapure variants targeting pharmaceutical and luxury fragrance markets. LANXESS operates synchronized manufacturing across the USA, Europe, and India, ensuring localized sourcing, supply security, and reduced Scope 3 transport emissions.

Valtris Specialty Chemicals positions benzyl benzoate as a high-performance additive for coatings and polymers

Valtris Specialty Chemicals plays a critical role in the high-performance additives segment, positioning benzyl benzoate as a premium plasticizer and coalescing agent in advanced coatings and polymer systems. In 2026, the company emphasizes low volatility and high thermal stability formulations tailored for demanding industrial applications. Valtris dominates industrial solvent and textile markets, where its benzyl benzoate serves as a dye carrier and leveling agent for synthetic fibers. Following leadership restructuring in late 2025, the firm is transitioning toward a customer-first specialty model, offering bundled additive solutions that integrate benzyl benzoate with polymer stabilizers for plastics manufacturers and pharmaceutical clients.

Hubei Greenhome Fine Chemical scales global supply with high-capacity distillation expertise

Hubei Greenhome Fine Chemical ranks among the world’s largest benzyl benzoate producers, operating 6,000 metric tons per year capacity alongside 42,000 tons of benzyl alcohol production. In late 2025, the company upgraded its 500-ton-per-day biochemical wastewater treatment system to comply with 2026 Green Factory regulations in China. It supplies perfumery grade benzyl benzoate with minimum 99.9% purity and pharmaceutical grade conforming to BP2000 standards. Known for high-vacuum distillation and wastewater recovery systems, Greenhome maintains ultra-low impurity levels, including minimal chlorinity, making it a preferred supplier for textile auxiliaries in Southeast Asia and Russia.

Tessenderlo Group strengthens agrochemical and pharmaceutical solvent integration

Tessenderlo Group operates within the fine chemicals segment, emphasizing high-value benzyl benzoate intermediates for agrochemical and pharmaceutical applications. In late 2025, it consolidated its specialty chemical activities under the Tessenderlo Kerley identity, streamlining its global market presence. The company supplies benzyl benzoate as a solvent and vehicle in topical medications for scabies and pediculosis treatments. In 2026, Tessenderlo focuses on bio-valorization and circular production at Belgian and French facilities to offset energy cost pressures. Through its Industrial Solutions segment, the company integrates coagulants, solvents, and water treatment chemicals into a synergistic production model.

Spectrum Chemical safeguards pharmaceutical-grade purity through regulatory excellence

Spectrum Chemical serves as a high-margin supplier in the USP and NF compliant benzyl benzoate segment across North America. The company specializes in ultra-high purity grades between 99.8 and 99.9 percent, meeting USP, BP, EP, and JP standards required for injectable drug solvents and bacteriostatic preservatives. During 2025 and 2026, Spectrum expanded its Safety and Supplies segment, integrating benzyl benzoate distribution with laboratory equipment solutions for pharmaceutical R&D facilities. Its 2026 strategy centers on lifecycle risk management and complete batch traceability, aligning with clean label and regulatory transparency requirements in medical, biopharmaceutical, and personal care industries.

Wuhan Youji Industries advances catalytic esterification for cost-efficient aroma chemical production

Wuhan Youji Industries is a historic leader in benzoic acid derivatives and a major global supplier under its Xuefeng brand. In 2025, the company developed an advanced catalytic esterification process that was fully scaled in 2026, producing benzyl benzoate with a lower carbon footprint compared to traditional acid-catalyzed routes. It expanded international sales into Europe and South America, reinforcing its status as a cost-competitive aroma chemical supplier. Its benzyl benzoate is widely used in synthetic musks and fine fragrances for improved dissolution and clarity. Vertical integration into toluene-derived feedstocks enables price stability amid global raw material volatility.

Germany Benzyl Benzoate Market: ISCC-PLUS Circularity, Ultrapure Grades, and Fragrance-Led Value Capture

Germany’s Benzyl Benzoate industry is advancing through certified circular feedstocks, ultrapure innovation, and stringent compliance with EU sustainability frameworks. In March 2025, LANXESS unveiled the Scopeblue variant of Kalama Benzyl Benzoate at the FAFAI exhibition. This ISCC PLUS–certified grade leverages bio-based or circular feedstocks to materially reduce lifecycle carbon intensity versus petroleum-derived synthesis, aligning with premium customer procurement mandates across fragrances and personal care. Later in 2025, LANXESS launched an Ultrapure grade tailored for high-end fragrance fixatives and sensitive pharmaceutical applications, eliminating the need to mask the characteristic sweet balsamic note seen in lower-purity variants and enabling consistent olfactive performance.

Operational excellence underpins these product moves. Following the EU’s 2025 chemical strategy for sustainability, German producers transitioned to closed-loop aromatics fractionation to meet tightening occupational exposure limits for benzene-derived precursors. Investments in advanced vacuum distillation across Mannheim-area clusters have reduced thermal degradation during benzoyl peroxide and benzyl benzoate processing, increasing yields of 99.9% purity grades. Demand-side pull is strong in high-end fragrance fixatives, where benzyl benzoate serves as a non-toxic solvent for artificial musks supporting Europe’s clean-label movement. Cross-industry synergies with Germany’s polyurethane sector further anchor demand, with the ester used as a high-performance plasticizer in specialized engineering resins.

India Benzyl Benzoate Market: O2C Feedstock Security, MSME Scale-Up, and Pharma-Centric Localization

India’s Benzyl Benzoate industry is scaling on the back of oil-to-chemical integration, MSME clusterization, and pharmaceutical localization. In early 2025, Reliance Industries Limited and other domestic majors intensified O2C investments, securing steady toluene supply for benzoic acid oxidation and downstream esterification into benzyl benzoate. The government’s Science and Technology Clusters initiative, expanding from 8 to 25 clusters by 2026, includes specialized chemical zones in Gujarat where producers such as Krishna Chemicals are scaling USP-grade output in the 99.0 to 100.5% range.

Export readiness and pharma demand are reinforcing capacity utilization. Ganesh Benzoplast Ltd. upgraded terminal infrastructure in late 2025 to facilitate bulk exports of high-purity aromatics to Southeast Asia and Europe. Under PLI Scheme 2.0, firms like Benzo Chem Industries expanded benzyl-derivative capacity for use as critical solvents in injectable formulations. Public health demand adds a domestic floor. In early 2026, the Ministry of Health and Family Welfare highlighted expanded benzyl benzoate use in national antiparasitic programs, lifting demand for dermatological-grade emulsions. Custom synthesis capabilities are also advancing, with Anupam Rasayan acting as a strategic supply chain partner for multinational originators seeking high-purity benzyl esters.

United States Benzyl Benzoate Market: Pharmacopeial Tightening, Green Esterification, and New Use Cases

The United States Benzyl Benzoate industry is shaped by pharmacopeial tightening, greener synthesis, and diversification into energy storage. Effective February 13, 2025, the United States Pharmacopeia revised its monograph for benzyl benzoate, mandating stringent benzaldehyde impurity limits and refined spectroscopic identification, raising compliance expectations for pharma-grade supply. Concurrently, industry findings from 2025 indicate that roughly 38% of U.S. producers have transitioned to greener esterification catalysts that reduce hazardous byproducts.

Application breadth is widening. Research published in Ionics in January 2025 confirmed benzyl benzoate at 0.3 wt% as an effective sulfation inhibitor in lead-acid batteries, extending HRPSoC cycling life substantially. In dermatology, 2025 clinical studies validated stabilized benzoyl peroxide and benzyl benzoate blends incorporating antioxidants such as BHT to address benzene exposure concerns and preserve shelf-life stability. Procurement is also shifting. Late-2025 sustainable sourcing mandates from major U.S. fragrance and personal care brands now favor suppliers with verified bio-based carbon content. On the industrial side, Valtris Specialty Chemicals increased R&D spending by an estimated 27% in 2025 to develop specialized plasticizers for construction and vehicle applications.

China Benzyl Benzoate Market: Smart Manufacturing, Electronic-Grade Expansion, and Environmental Enforcement

China’s Benzyl Benzoate industry is prioritizing purity efficiency, smart controls, and downstream specialization under the MIIT Petrochemical Work Plan 2025–2026. The policy emphasis is on capacity debottlenecking rather than raw expansion, ensuring large complexes in Shandong and Hubei operate at high-purity efficiencies. Producers including Nantong Tianshi and Wuhan Youji integrated AI-driven smart factory controls in late 2025 to optimize toluene oxidation pathways, improving yield consistency and energy efficiency.

Downstream demand is steering product mix. China is scaling electronic-grade benzyl benzoate above 99.9% purity for dielectric solvent use and photoresist manufacturing as electronics and semiconductor supply chains localize. Textile auxiliaries are also evolving. Following a 2025 shift toward high-performance synthetic fibers, benzyl benzoate’s role as a polyester dye carrier has been upgraded to reduce VOC emissions. Policy signals reinforce localization. Beijing’s 2026 roadmap for specialty chemicals prioritizes domestic aroma chemical precursors, reducing reliance on European high-end supply. Environmental enforcement is tightening in parallel, with 2025 fenceline monitoring rules compelling older benzyl chloride and benzoate units to adopt vapor recovery and catalytic oxidation systems.

Country-Level Strategic Snapshot: Benzyl Benzoate Industry

Benzyl Benzoate Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Developments

|

|

Germany

|

Circular feedstocks and ultrapure innovation

|

ISCC PLUS Scopeblue grade, Ultrapure launches, closed-loop fractionation, vacuum distillation

|

|

India

|

O2C security and pharma localization

|

Gujarat MSME clusters, export terminals, PLI-backed capacity, public health demand

|

|

United States

|

Pharmacopeial rigor and diversification

|

USP monograph updates, green synthesis, battery additive use, sustainable sourcing

|

|

China

|

Smart manufacturing and electronic-grade scale

|

AI-controlled oxidation, >99.9% purity expansion, textile VOC reduction, fenceline enforcement

|

Benzyl Benzoate Market Report Scope

Benzyl Benzoate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$105.2 Million

|

|

Market Size (2034)

|

$153.7 Million

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Grade (Pharmaceutical Grade, Flavor and Fragrance Grade, Technical Grade, Specialty Grade), By Application (Pharmaceuticals, Flavors and Fragrances, Textile Auxiliaries, Industrial Solvents, Plasticizers, Battery Additives), By End Use Industry (Healthcare and Personal Care, Textiles and Apparel, Automotive and Transportation, Chemical Manufacturing, Food and Beverage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LANXESS, Nouryon, Wuhan Youji Industries, Benzo Chem Industries, Emerald Kalama Chemical, Hubei Greenhome Fine Chemical, Valtris Specialty Chemicals, Eternis Fine Chemicals, Zibo Zengrui Chemical, Tianjin Dongda Chemical Group, Vertellus, Tennants Fine Chemicals, Sabari Chemicals, Krishna Chemicals, Wuhan Sinocon Pharmaceutical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Benzyl Benzoate Market Segmentation

By Grade

- Pharmaceutical Grade

- Flavor and Fragrance Grade

- Technical Grade

- Specialty Grade

By Application

- Pharmaceuticals

- Flavors and Fragrances

- Textile Auxiliaries

- Industrial Solvents

- Plasticizers

- Battery Additives

By End Use Industry

- Healthcare and Personal Care

- Textiles and Apparel

- Automotive and Transportation

- Chemical Manufacturing

- Food and Beverage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Benzyl Benzoate Industry

- LANXESS

- Nouryon

- Wuhan Youji Industries

- Benzo Chem Industries

- Emerald Kalama Chemical

- Hubei Greenhome Fine Chemical

- Valtris Specialty Chemicals

- Eternis Fine Chemicals

- Zibo Zengrui Chemical

- Tianjin Dongda Chemical Group

- Vertellus

- Tennants Fine Chemicals

- Sabari Chemicals

- Krishna Chemicals

- Wuhan Sinocon Pharmaceutical

*- List not Exhaustive