Market Overview: Benzyl Chloride Market Expansion Led by India Capacity Buildout, European Consolidation, and High-Purity Intermediates Demand (2025–2034)

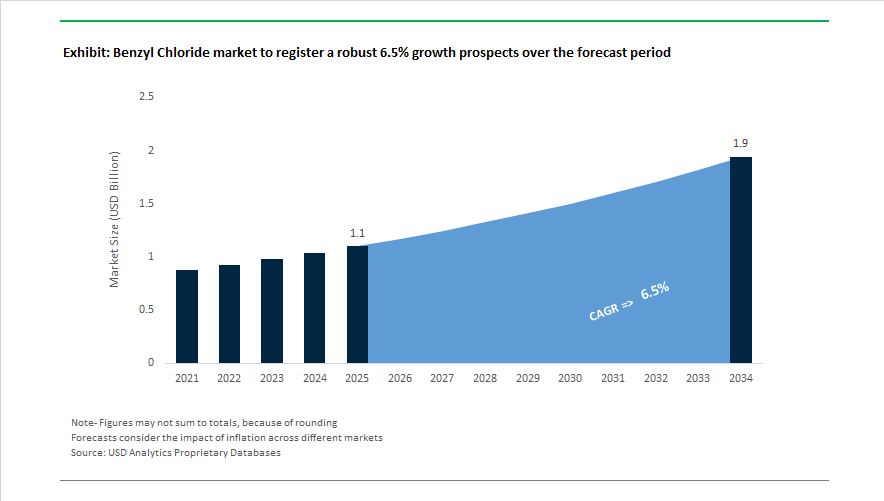

The benzyl chloride market is projected to grow from USD 1.1 billion in 2025 to USD 1.9 billion by 2034, reflecting a CAGR of 6.5% supported by rising consumption of benzyl derivatives in pharmaceuticals, agrochemicals, plasticizers, coatings, and fragrance intermediates. Benzyl chloride remains a critical chlorinated aromatic intermediate used in the production of benzyl alcohol, benzaldehyde, quaternary ammonium compounds, and benzyl esters. Structural supply chain developments began in 2024. In March 2024, Valtris Specialty Chemicals partnered with Barentz to stabilize North American distribution of benzyl-based intermediates. Later in 2024, the Valtris Tessenderlo facility in Belgium reached full operational status following a 15% capacity expansion, strengthening European supply of high-purity benzyl chloride grades for pharmaceutical and personal care sectors. In November 2024, International Chemical Investors Group completed acquisition of Valtris’ European Advanced Organics business, consolidating a key benzyl chloride production hub within its specialty intermediates portfolio.

India emerged as a major growth center in 2025 through integrated capacity additions. In April 2025, Gujarat Alkalies and Chemicals Limited inaugurated India’s largest chlorotoluenes plant in Dahej with 30,000 tonnes annual capacity, followed by dispatch of its first commercial benzyl chloride shipment the same month. The facility is projected to generate substantial export revenue while reducing reliance on imports. In March 2025, Lanxess reported a 73.6% increase in EBITDA within its Advanced Intermediates segment, reflecting stronger margins for high-purity benzyl chloride derivatives. In July 2025, GACL advanced value-chain integration by dispatching benzyl alcohol and benzaldehyde from the same site, converting benzyl chloride into higher-value pharmaceutical and fragrance solvents. Late 2025 expansion approvals by GACL included three additional chlorotoluenes units backed by ₹810 million investment, expected to generate ₹1.56 billion in annual revenue.

Regional production modernization and regulatory shifts are influencing trade and technology adoption. In early 2025, new U.S. tariff measures increased complexity for benzyl chloride imports, encouraging domestic sourcing and new contract structures for coatings and pharmaceutical manufacturers. Between 2024 and 2025, Hubei Phoenix Chemical advanced construction of a modern benzyl chloride production unit in China, replacing older chlorination assets with automated systems that reduce by-product formation and improve yield efficiency. Sustainability-linked research is also shaping long-term demand. In November 2025, UCLA and UCSB secured $23.7 million in funding to develop bio-based polymers using benzyl intermediates, while Ohio and Akron polymer hubs received $51 million in funding during 2024 to 2025 to advance cleaner synthesis technologies for paints, coatings, and adhesives.

Trends and Opportunities Transforming the Benzyl Chloride Market

Market Trend: Regulatory Pressure in China Driving Structural Supply Tightness

The global Benzyl Chloride Market is undergoing a structural rebalancing as China, historically the dominant supplier, tightens safety and emissions control. In November 2025, the Ministry of Ecology and Environment (MEE) added benzyl chloride to its Third Batch of Priority Controlled Substances, layering restrictions over the September 2025 Hazardous Chemicals Safety Law. This two-stage regulatory framework forces smaller producers to install advanced emission scrubbers, wastewater handling, and leak mitigation systems.

As a result, approximately 10 to 15% of domestic capacity from non-compliant plants has been suspended or permanently exited the market. This has created persistent tightness despite temporary post–Lunar New Year rebounds linked to agrochemical restocking. Although pricing stabilized around $973 per metric ton by September 2025, export flows remain disrupted due to Shanghai Port congestion and heightened customs checks, prolonging lead times and creating significant market inefficiencies for global buyers.

Market Trend: Strategic Migration Toward On-Site and Integrated Production Models

Logistics and safety risks associated with shipping benzyl chloride, a hazardous lachrymatory chemical, are accelerating a shift toward integrated, regionalized production. Large downstream consumers are prioritizing captive manufacturing units or toll-based supply contracts positioned near high-consumption clusters.

In India, Gujarat Alkalies and Chemicals Limited (GACL) has commissioned one of the country’s largest chlorotoluene facilities in Dahej, serving the adjacent pharmaceutical and agrochemical hubs. This strategic positioning lowers transportation risk and provides “just-in-time” feedstock for generic drug manufacturers. Globally, production scale is expanding through new world-class plants: Chongqing Ziguang Tianyuan Chemical has announced a 5,000-ton hydrogen chloride–integrated facility, while Aarti Industries unveiled a 9,000-ton chlorotoluene derivative plant in late 2024. These configurations optimize feedstock utilization, reduce cost-per-ton, and strengthen quality control, signaling a business model shift from bulk merchant trade toward co-located industrial ecosystems.

Market Opportunity: Rising Use in Resistance-Management Agrochemicals

The Agrochemical sector represents one of the most compelling growth avenues for the Benzyl Chloride Market, driven by next-generation active ingredients designed for environmental safety and resistance mitigation. Benzyl-based intermediates are increasingly prioritized for herbicides and fungicides that prevent “resistance drift,” especially in staple crops like wheat and rice.

Policy environments support this pivot. The EU’s Farm to Fork strategy is promoting crop protection chemistries with shorter environmental half-lives, steering R&D away from legacy organochlorines. Asia-Pacific is forecasted to deliver the fastest adoption curve, supported by domestic food security agendas running through 2030. In these markets, benzyl chloride–derived insecticide intermediates are projected to scale at the highest volume CAGR, as precision farming and targeted agrochemical inputs gain traction.

Market Opportunity: High-Value Derivatives for Biocides and Phase-Transfer Catalysts

Benzyl Chloride serves as a foundational precursor for Benzalkonium Chlorides (BAC) and Phase-Transfer Catalysts (PTCs) – segments that command premium pricing due to regulatory compliance and application complexity. In 2025, Quaternary Ammonium Compound production is estimated to represent roughly 40% of global benzyl chloride demand, supported by sustained post-pandemic hygiene standards in healthcare, institutional cleaning, and consumer disinfectants. These BAC products must comply with updated FDA and EMA rules on non-toxic residue and antimicrobial safety, increasing the need for ultra-high purity upstream feedstocks.

In pharmaceuticals, the expanding use of benzyl-based PTCs reflects the market’s transition toward Green Chemistry. These catalysts enable high-yield synthesis in biphasic systems at lower solvent levels and lower energy intensity. As Merck KGaA, LANXESS, and specialty chemical producers upgrade portfolios toward catalytic efficiency additives, demand for benzyl chloride suitable for GMP-adjacent derivatization is expected to accelerate.

Benzyl Chloride Market Share and Segmentation Insights

Market Share by Grade: Technical and Industrial Material Leads Volume While Electronic Grade Accelerates on Semiconductor Expansion

Technical and industrial grade dominates the Benzyl Chloride Market with a 58% share in 2025, reflecting its role as a high-volume chemical intermediate in the production of plasticizers such as butyl benzyl phthalate, quaternary ammonium compounds, and benzyl alcohol. Demand in this segment is tightly linked to industrial manufacturing activity and agrochemical output. Pharmaceutical grade represents a significant secondary segment, supported by its use in synthesizing active pharmaceutical ingredients, including antihistamines, antispasmodics, and penicillin precursors, where stringent impurity control and high purity specifications command pricing premiums. Electronic grade, although smallest by volume, is the fastest-growing category, driven by rising consumption of ultra-high-purity benzyl chloride in photoresist systems and specialty etching chemistries for semiconductor fabrication. Growth here closely tracks advanced node capacity additions and broader investments in electronics manufacturing.

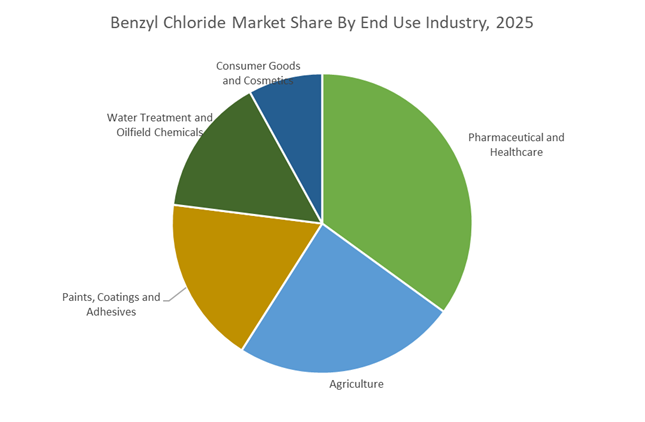

Market Share by End Use Industry: Healthcare Leadership Balanced by Agriculture and Specialty Chemicals

Pharmaceutical and healthcare applications account for 35% of benzyl chloride consumption in 2025, positioning this sector as the primary demand driver. The compound serves as a key intermediate for benzyl esters, benzylamines, and quaternary ammonium compounds used in antiseptics, antihistamines, and muscle relaxants, with generic drug manufacturing in Asia providing strong volume momentum. Agriculture forms the second-largest segment, utilizing benzyl chloride in fungicides, herbicides, and plant growth regulators, with demand closely aligned to crop protection cycles and commodity pricing. Paints, coatings, and adhesives consume benzyl chloride derivatives such as benzyl alcohol and benzyl esters as solvents, coalescing agents, and plasticizers, with water-borne formulations increasing requirements for high-performance coalescents. Water treatment and oilfield chemicals rely on benzyl chloride for biocides and corrosion inhibitors, while consumer goods and cosmetics represent a smaller but rising segment, supported by growing use of preservative-grade materials in fragrances and hair care amid clean beauty trends.

Competitive Landscape Analysis of the Benzyl Chloride Market

The benzyl chloride market is driven by tight feedstock integration with toluene and chlorine, rising demand from pharmaceutical intermediates, epoxy resin systems, quaternary ammonium compounds, and specialty preservatives. Competitive advantage increasingly depends on backward integration, high-purity manufacturing, continuous chlorination technology, and ESG-aligned production practices. Leading producers are differentiating through AI-enabled process optimization, green factory certification, internal chlorine security, and downstream value capture into benzyl alcohol, biocides, and high-performance resins. As global buyers prioritize supply reliability and low-carbon intermediates, the market is consolidating around vertically integrated players capable of delivering consistent purity, scale-driven economics, and application-specific benzyl chloride grades.

LANXESS sets the global benchmark for low-carbon, high-purity benzyl chloride

LANXESS remains the reference producer for high-performance benzyl chloride, supported by full backward integration into toluene and chlorine. During 2025 and 2026, the company divested its Urethane Systems business to become a pure-play specialty chemicals supplier, sharpening its focus on high-margin intermediates. In early 2026, LANXESS deployed AI-driven chlorination control, reducing benzal chloride by-products by fourteen% and improving premium-grade yields. Aligned with its Climate-Neutral 2040 roadmap, key European aromatics sites now operate on renewable energy, enabling certified low-carbon benzyl chloride for ESG-focused pharmaceutical clients. LANXESS also supplies critical precursors for Lanthenas and biocides used in water treatment and animal health.

Valtris Specialty Chemicals expands benzyl chloride applications across oilfield and specialty chemistry

Valtris Specialty Chemicals is the dominant North American supplier, leveraging benzyl chloride’s high reactivity for diverse industrial applications. In early 2026, Valtris strengthened its Asian presence at PLASTINDIA, highlighting its integrated benzyl-based plasticizers and sanitizing agents. The company is a primary supplier for oil and gas quaternary ammonium compounds, where benzyl chloride serves as a vital intermediate for shale extraction fluids and corrosion inhibitors. Following the 2025 divestment of its renewables unit, Valtris redirected capital into expanding chlorotoluene capacity to support domestic pharmaceutical precursor demand. Its core strength lies in addition chemistry, enabling high-end soaps, dyes, and heat-exchange fluid production.

Wuhan Youji Industries leverages vertical integration to scale global benzyl derivatives

Wuhan Youji Industries is a historic leader in toluene derivatives and one of the world’s most vertically integrated benzyl chloride producers. By 2026, it ranks second globally in benzyl alcohol output, manufactured directly from its in-house benzyl chloride streams. Under its Xuefeng brand, the company offers over one hundred aromatic chlorination and oxidation products spanning food preservatives to defense-grade rubber additives. A proprietary continuous chlorination process introduced in 2026 enables round-the-clock production while cutting energy consumption by 9%. Strategically, Wuhan Youji is prioritizing downstream pharmaceutical intermediates and food antisepsis derivatives, positioning itself as a global preservation solutions provider.

Hubei Greenhome Materials Technology scales green manufacturing for epoxy and composite applications

Hubei Greenhome Materials Technology has rapidly emerged as a top-tier global benzyl chloride supplier through large-scale capacity expansion completed in late 2025 and early 2026. The company dominates epoxy resin diluent markets, supplying benzyl derivatives essential for low-viscosity systems used in wind turbine blades and aerospace composites. Significant investment in wastewater treatment and VOC recovery earned Green Factory certification in 2026, strengthening its appeal to environmentally regulated European buyers. Greenhome’s scale-driven model supports competitive pricing while maintaining purity levels above 99.5 percent, reinforcing its reputation for reliability in industrial-grade benzyl chloride supply.

Gujarat Alkalies and Chemicals Limited anchors India’s benzyl chloride self-reliance through integrated chlorotoluene

Gujarat Alkalies and Chemicals Limited plays a central role in India’s Make in India aromatics strategy. In late 2025, GACL commissioned the country’s largest integrated chlorotoluene facility at Dahej, achieving 95% operational efficiency by early 2026 and sharply reducing import dependence. The company is positioning Dahej as an export hub for benzyl derivatives serving South Korea, Japan, and the European Union. Its bundled offerings of benzyl cyanide and benzyl alcohol support India’s pharmaceutical synthesis of antibiotics and analgesics. Backed by in-house chlor-alkali operations, GACL internalizes chlorine supply, insulating benzyl chloride margins from merchant chlorine volatility.

Nippon Light Metal Holdings specializes in ultra-pure benzyl chloride for high-tech Japanese industries

Nippon Light Metal Holdings operates as a precision-focused supplier of benzyl chloride for Japan’s electronics, machinery, and advanced materials sectors. In 2026, its high-purity intermediates support specialty resins used in 5G and 6G infrastructure as well as electric vehicle components. NLM’s integrated explore-create-make-sell workflow enables rapid customization of benzyl derivatives for automotive and machinery OEMs. The company leads Japan’s sanitation and high-value quaternary ammonium markets, supplying semiconductor-grade cleaning intermediates. Rather than competing on volume, NLM’s strategy centers on ultra-low impurity benzyl chloride for niche, engineering-critical applications.

India Benzyl Chloride Market: Integrated Capacity, Export Orientation, and API-Led Demand

India’s benzyl chloride industry has crossed a structural milestone with the commissioning of large-scale, integrated capacity aligned to export-grade purity and pharmaceutical downstreams. In March 2025, Gujarat Alkalies and Chemicals Limited inaugurated the country’s largest integrated chlorotoluene complex at Dahej, backed by an investment of ₹350 crore. The facility includes a dedicated 30,000-tonne annual capacity for benzyl chloride and key derivatives such as benzyl alcohol and benzaldehyde. This integration improves yield control, enhances safety in chlorination, and lowers unit costs through shared utilities and feedstock optimization.

The Dahej complex is explicitly export-facing. It is positioned to generate approximately ₹130 crore in annual foreign exchange, targeting high-purity aromatics demand from North American and European pharmaceutical customers that require consistent impurity profiles and robust documentation. Policy alignment is reinforcing this momentum. Under the July 2025 NITI Aayog report, benzyl chloride is a priority beneficiary of the S&T Clusters initiative, which is expanding specialized chemical clusters from 8 to 25 to accelerate domestic self-sufficiency in toluene-based intermediates. Downstream integration is deepening as well. Indian firms such as Benzo Chem Industries and Anupam Rasayan are moving beyond toll manufacturing to strategic supply chain partnerships, supplying benzyl chloride as a precursor for antihistamines and antibiotic APIs. To stabilize margins, the Department of Chemicals and Petrochemicals has prioritized mechanisms to smooth toluene feedstock pricing, reducing exposure to crude oil volatility.

China Benzyl Chloride Market: Compliance-Driven Process Upgrades and Electronic-Grade Pivot

China’s benzyl chloride industry is entering a compliance-led transition phase marked by stricter emissions standards, digital process control, and a pivot toward electronic-grade applications. Effective June 1, 2026, two mandatory national standards, GB 30981.1-2025 and GB 30981.2-2025, will cap hazardous aromatic compounds in architectural and industrial coatings. These requirements are compelling producers to adopt low-VOC distillation and tighter fractionation to meet downstream customer specifications without sacrificing throughput.

Industrial consolidation and digitalization are advancing in parallel. The Ministry of Industry and Information Technology has prioritized smart factory upgrades across chlorination loops in Nantong and Wuhan, deploying advanced controls to improve selectivity toward high-purity benzyl chloride while suppressing low-value byproducts. Demand-side shifts are reinforcing this upgrade cycle. Chinese manufacturers are increasingly scaling electronic-grade benzyl chloride for use in photoresist formulations and dielectric solvent production, supported by the national semiconductor self-sufficiency roadmap. Environmental enforcement is tightening simultaneously. Under the 2025–2026 Petrochemical Work Plan, provincial authorities in Shandong have implemented fenceline monitoring to curb chlorine emissions during photo-chlorination of toluene, raising the compliance bar for legacy plants and accelerating modernization.

United States Benzyl Chloride Market: Specialty Additives, Energy-Efficient Reactors, and Near-Shoring

The United States benzyl chloride market is characterized by a shift toward specialty additives, energy-efficient processing, and resilient sourcing. Valtris Specialty Chemicals, headquartered in Independence, Ohio, intensified its Sustainable Solutions Provider Strategy in late 2025, emphasizing benzyl chloride as a precursor for quaternary ammonium salts used in oilfield chemicals and sanitizing applications. This focus reflects steady demand from industrial hygiene and energy services rather than commodity aromatics.

Process efficiency is improving across the sector. Leading U.S. producers are upgrading photo-chlorination reactors with high-efficiency LED-based UV systems, reducing energy consumption while improving reaction selectivity toward benzyl chloride fractions. Supply chains are also being reconfigured. Amid tightening reporting requirements related to chemical precursors, including PFAS-linked disclosures, U.S. buyers are increasingly sourcing benzyl chloride from domestic or near-shored facilities to minimize logistics risk and regulatory exposure. This trend favors producers with localized capacity and transparent compliance frameworks.

Germany and the European Union Benzyl Chloride Market: High-Margin Intermediates, Circular Feedstocks, and Safety Automation

Germany and the broader European Union are repositioning benzyl chloride production toward high-margin intermediates, circular feedstocks, and automated handling. In August 2025, LANXESS announced a restructuring of its aromatics network, streamlining selected sites while concentrating investment on advanced intermediates derived from benzyl chloride. This strategy is intended to offset rising energy costs and sustained pricing pressure from Asian suppliers.

Circular economy pilots are gaining traction. German chemical majors are exploring synthesis routes that use circular toluene derived from chemically recycled plastic waste, with the objective of achieving ISCC PLUS certification by late 2026. Worker safety standards are also tightening. New recommendations issued by the European Chemicals Agency in late 2025 have driven adoption of fully automated, zero-emission drumming and transfer lines for benzyl chloride at major logistics hubs such as Antwerp and Rotterdam. These investments reduce occupational exposure risks while improving throughput consistency for export-oriented operations.

Japan Benzyl Chloride Market: Ultra-Pure Specialization and Green Chlorination Chemistry

Japan’s benzyl chloride industry remains anchored in ultra-high purity specialization and process innovation aligned with sustainability goals. Companies such as Nippon Light Metal Holdings continue to dominate the ultra-pure segment required for premium fragrance fixatives and specialized plasticizers used in automotive interiors and advanced polymers. These applications demand exceptionally low impurity profiles and stable supply relationships.

Green chemistry initiatives are reshaping production methods. The Japan Chemical Industry Association reported a 2025 industry-wide shift toward catalytic chlorination techniques that minimize formation of chlorinated byproducts. This approach improves atom efficiency, reduces waste treatment loads, and aligns benzyl chloride production with Japan’s long-term carbon neutrality objectives. As a result, Japanese producers are reinforcing their reputation as suppliers of choice for critical, specification-driven benzyl chloride applications.

Country-Level Strategic Snapshot: Benzyl Chloride Industry

Benzyl Chloride market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

India

|

Integrated capacity and pharma exports

|

Dahej chlorotoluene complex, S&T clusters, API partnerships, feedstock stabilization

|

|

China

|

Compliance upgrades and electronic-grade scale

|

GB 30981 standards, smart factories, semiconductor-linked demand, fenceline monitoring

|

|

United States

|

Specialty additives and resilient sourcing

|

Quats precursors, LED-based reactors, near-shoring for compliance

|

|

Germany / EU

|

High-margin intermediates and circularity

|

Network restructuring, circular toluene pilots, automated zero-emission handling

|

|

Japan

|

Ultra-pure grades and green chlorination

|

Catalytic chlorination, fragrance and automotive specialization

|

Benzyl Chloride Market Report Scope

Benzyl Chloride market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$1.9 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Grade (Pharmaceutical Grade, Technical and Industrial Grade, Electronic Grade), By Production Process (Photo Chlorination of Toluene, Chloromethylation of Benzene, Catalytic Chlorination), By Application (Chemical Intermediates, Pharmaceutical Precursors, Agrochemicals, Quaternary Ammonium Compounds, Industrial Additives, Personal Care), By End Use Industry (Pharmaceutical and Healthcare, Agriculture, Paints Coatings and Adhesives, Water Treatment and Oilfield Chemicals, Consumer Goods and Cosmetics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LANXESS, Valtris Specialty Chemicals, Gujarat Alkalies and Chemicals, Wuhan Youji Industries, Hubei Phoenix Chemical, Benzo Chem Industries, Nippon Light Metal Holdings, Shanghai Xinglu Chemical Technology, KLJ Group, Charkit Chemical Company, Danyang Wanlong Chemical, Paushak, Kemin Industries, Delta Finochem, Hubei Greenhome Fine Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Benzyl Chloride Market Segmentation

By Grade

- Pharmaceutical Grade

- Technical and Industrial Grade

- Electronic Grade

By Production Process

- Photo Chlorination of Toluene

- Chloromethylation of Benzene

- Catalytic Chlorination

By Application

- Chemical Intermediates

- Pharmaceutical Precursors

- Agrochemicals

- Quaternary Ammonium Compounds

- Industrial Additives

- Personal Care

By End Use Industry

- Pharmaceutical and Healthcare

- Agriculture

- Paints Coatings and Adhesives

- Water Treatment and Oilfield Chemicals

- Consumer Goods and Cosmetics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Benzyl Chloride Industry

- LANXESS

- Valtris Specialty Chemicals

- Gujarat Alkalies and Chemicals

- Wuhan Youji Industries

- Hubei Phoenix Chemical

- Benzo Chem Industries

- Nippon Light Metal Holdings

- Shanghai Xinglu Chemical Technology

- KLJ Group

- Charkit Chemical Company

- Danyang Wanlong Chemical

- Paushak

- Kemin Industries

- Delta Finochem

- Hubei Greenhome Fine Chemical

*- List not Exhaustive