Biodegradable Plastic Packaging Market Overview: Market Size, Growth, and Key Insights

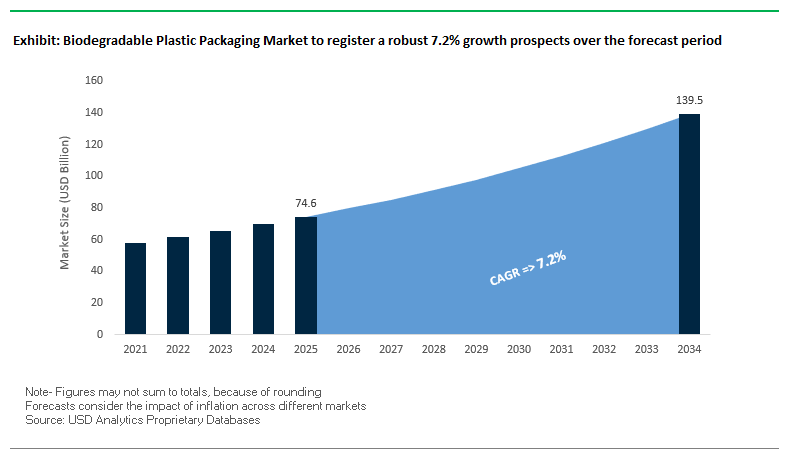

The global biodegradable plastic packaging market is projected to grow from USD 74.6 billion in 2025 to USD 139.5 billion by 2034, at a robust CAGR of 7.2%. This expansion reflects intensifying consumer, corporate, and regulatory efforts to curb plastic pollution and accelerate the adoption of bio-based, compostable, and recyclable packaging solutions.

Unlike conventional plastics that persist in the environment for centuries, certified biodegradable plastics such as polylactic acid (PLA) and polyhydroxyalkanoates (PHAs) can decompose naturally in controlled environments within months. This advantage positions them as a key solution to microplastic pollution and landfill overflow. Furthermore, material science breakthroughs now enable biodegradable plastics to rival traditional plastics in durability, barrier protection, and heat sealability, making them increasingly suitable for food, beverage, pharmaceutical, and agricultural packaging.

Key Insights for Buyers and Industry Leaders

- Renewable sourcing: Corn starch, sugarcane, and cellulose replacing petroleum feedstocks.

- Decomposition advantage: PHAs and PLA break down within months in composting facilities.

- No toxic residues: Certified biodegradable plastics degrade into CO₂, water, and biomass.

- Performance parity: New-generation bioplastics match conventional plastics in durability and protection.

Strategic Mergers and Product Launches Redefine Biodegradable Plastic Packaging Industry

The biodegradable plastic packaging sector is evolving rapidly, with mergers, acquisitions, and product launches reshaping the competitive landscape. In August 2025, Amcor PLC launched a fully home-compostable coffee pod lidding material, offering a sustainable alternative to PET and aluminum lids. That same month, The Greener Tech Group revealed pilots of biodegradable HDPE and LDPE alternatives, marking a breakthrough for beverage and food producers.

Material science innovation continues to dominate industry developments. In June 2025, Mondi introduced new biodegradable packaging for fresh produce, integrating bio-based coatings for product preservation. A month earlier, Eastman and SEE (formerly Sealed Air) unveiled a compostable tray to replace polystyrene foam in protein packaging, while Teknor Apex (March 2025) acquired Danimer Scientific, strengthening its portfolio in PHAs.

Looking back, September 2024 saw Danimer Scientific and Ningbo Homelink Eco-iTech commercialize Nodax PHA coatings for paper cups, and UPM Specialty Papers with Eastman rolled out biopolymer-coated grease- and oxygen-resistant food packaging. In April 2024, NatureWorks LLC launched Ingeo Extend PLA polymer, enabling faster biodegradability and improved efficiency for BOPLA films used in flexible packaging.

Key Trends and Strategic Growth Opportunities Shaping the Biodegradable Plastic Packaging Market

Regulatory-Driven Shift Towards Certified Compostable Polymers

A prominent trend in the biodegradable plastic packaging market is the regulatory-driven adoption of certified compostable polymers, particularly in food service applications. Stringent bans on conventional single-use plastics in regions like the European Union and several U.S. states are compelling manufacturers to transition from vague “biodegradable” claims to materials that comply with recognized standards such as ASTM D6400 for industrial composting. According to the U.S. EPA, plastics labeled as compostable must biodegrade within six months in industrial facilities without leaving toxic residues. Companies like Danimer Scientific are developing home-compostable PHA-based packaging for fresh produce, showcasing innovation in meeting regulatory standards while reducing plastic waste. Globally, India’s Central Pollution Control Board (CPCB) has implemented IS 17899 T:2022 for biodegradable plastics, ensuring measurable degradation and disintegration before market entry. These initiatives highlight how certified compostable polymers are central to aligning with environmental regulations, enhancing brand credibility, and addressing rising consumer expectations for sustainable packaging.

Advanced Material Development for High-Barrier Applications

Another significant trend is the development of high-barrier biodegradable plastics designed to compete with conventional plastics in challenging applications. Enhancements in oxygen, moisture, and grease barriers are critical for food safety and shelf-life extension. Early-generation biopolymers like PLA had limited barrier properties, but innovations now incorporate cellulose, proteins, and locally sourced waste materials. For instance, a patented bioplastic derived from dairy industry waste in India demonstrates rapid soil biodegradability (20–30 days), non-toxicity, and high tensile strength. Companies such as Plantic have commercialized starch-based biodegradable trays and flexible packaging that combine high-performance barriers with full compostability. The development of these advanced polymers opens previously untapped segments of the flexible packaging market, including meat, dairy, and ready-to-eat meals, driving broader adoption of eco-friendly, high-performance packaging solutions.

Development of Marine-Degradable Packaging for Waterfront Concessions

A key market opportunity lies in marine-degradable biodegradable plastics, particularly for the waterfront concessions sector. Plastic waste from beaches, cruise ships, and sporting events contributes significantly to ocean pollution. Materials designed to meet ASTM D7081 marine biodegradability principles provide a practical solution for this environmental challenge. Startups like Notpla have developed seaweed- and plant-based packaging that is edible, biodegradable, and suitable for liquid and food products in high-traffic environments. Adoption of marine-degradable packaging not only mitigates oceanic plastic pollution but also offers brand differentiation and public relations advantages, reinforcing a company’s environmental commitment.

Adoption in Agricultural Seed and Fertilizer Packaging

The agricultural sector presents another growth avenue for biodegradable plastic packaging. Traditional LDPE bags used for seeds and fertilizers contribute to soil contamination with microplastics. Biodegradable polymer films designed for plowing directly into the soil eliminate retrieval challenges while returning organic matter to the land. This closed-loop system supports sustainable farming practices and reduces labor costs. Companies developing specialized biodegradable bags for agricultural inputs are enabling farmers to improve soil health, comply with environmental standards, and reduce plastic pollution. By integrating biodegradable plastics into agricultural operations, the market can advance a circular economy model, where packaging materials protect products during transport and seamlessly return nutrients to the soil.

Competitive Landscape: Leading Companies in Biodegradable Plastic Packaging Industry

The global market is shaped by biopolymer specialists, diversified chemical giants, and packaging innovators, each competing through R&D, sustainability commitments, and global expansion.

NatureWorks LLC: Scaling Global PLA Biopolymer Capacity

NatureWorks leads with its Ingeo PLA biopolymer, derived from renewable resources such as corn. In 2025, it committed over USD 600 million to build a 75,000-ton-per-year facility in Thailand, boosting supply for applications in coffee capsules, films, and food serviceware. Its strategy focuses on expanding global access to compostable PLA solutions.

Danimer Scientific (Now Part of Teknor Apex) Strengthens PHA Leadership

Acquired by Teknor Apex in March 2025, Danimer is renowned for its Nodax PHA, certified for biodegradability across marine, soil, and composting environments. The acquisition brings stability and broader commercialization opportunities. With Teknor’s material science expertise, Danimer is positioned to deliver customizable biopolymer formulations for high-performance packaging.

BASF SE Expands with Compostable Ecovio Portfolio

BASF’s ecovio a blend of ecoflex and PLA is a premium compostable polymer widely used in organic waste bags, snack wrappers, agricultural films, and to-go cups. The company’s focus lies in high-performance solutions that integrate seamlessly into existing packaging lines, while addressing global demand for certified compostable applications.

Novamont S.p.A.: Pioneering Circular Bioeconomy with Mater-Bi

Novamont, developer of Mater-Bi bioplastics, specializes in renewable, compostable materials for waste bags, food packaging, and mulching films. In October 2023, Versalis acquired full ownership, strengthening its global footprint. Novamont also leads EU-funded projects that integrate bio-based solutions into circular economy models.

Mitsubishi Chemical Corporation: Advancing Marine-Biodegradable BioPBS

Mitsubishi Chemical produces BioPBS, a compostable polymer known for flexibility and heat-sealability. In December 2023, BioPBS earned a marine biodegradable certification in Japan, enhancing its potential for coastal and packaging applications. The company’s R&D strategy centers on high-performance, low-carbon bioplastics for pouches, zipper seals, and paper coatings.

Biodegradable Plastic Packaging Market Share Insights

Flexible Packaging leads Market Share by Packaging Type in the Biodegradable Plastic Packaging Market

Flexible biodegradable plastics hold 55% share as films, pouches, and bags deliver the best combination of barrier, sealability, and downgauging for produce, bakery, snack, and foodservice. Compostable multilayer architectures (e.g., PLA/PHA blends with bio-based tie layers) are extending shelf life without PFAS or aluminum, keeping organics streams viable and reducing landfill fees for food retailers. Rigid at 45% grows on clear PLA bottles, PHA jars, thermoformed trays, and compostable closures that meet branding and functionality requirements; investment in barrier enhancements and heat-resistance is unlocking dairy, refrigerated beverages, and cosmetics where rigidity and transparency drive conversion.

Food Packaging maintains the highest Market Share by Application in the Biodegradable Plastic Packaging Market

At 50%, food packaging is the sector’s anchor, replacing conventional single-use plastics in high-velocity SKUs from compostable cutlery/cups to produce bags and bakery films where compliance risk and consumer preference directly translate into SKU-level switching. Consumer goods (20%) benefits from parcel-centric packaging (biodegradable mailers, protective foams) aligned with retailer sustainability KPIs. Beverages (15%) is the technology frontier focused on bottle performance (CO₂ retention, OTR) and compostable pods/capsules, while personal care exploits bio-polymers to align packaging with “natural” formulations. Medical remains a high-value, regulation-bound niche, concentrating on non-sterile and secondary packs pending broader primary-pack approvals.

United States Biodegradable Plastic Packaging Market Grows Amid EPR Legislation and Bioplastics Innovation

The U.S. biodegradable plastic packaging market is strongly influenced by a complex regulatory environment. The Federal Trade Commission (FTC) enforces “Green Guides” to prevent misleading marketing of degradable or compostable products, while states such as Washington and Maryland passed Extended Producer Responsibility (EPR) laws in 2025. These regulations require producers to manage the end-of-life of their packaging, encouraging the adoption of compostable plastic materials. Corporate investments are accelerating this transition, exemplified by Nestlé Purina’s home-compostable cat litter launched in 2024 and DefenAge Skincare’s adoption of biodegradable packaging in October 2023.

Technological advancements are reshaping the sector, with companies like Danimer Scientific producing polyhydroxyalkanoates (PHAs) that naturally break down in soil and marine environments, offering a sustainable solution where industrial composting facilities are scarce. The growth of e-commerce is also driving demand for sustainable shipping solutions, with Pregis expanding its portfolio of curbside-recyclable biodegradable packaging. Key applications span food and beverage, as well as personal care products, including coffee pods, food containers, and single-use utensils. The U.S. Environmental Protection Agency (EPA) further supports market expansion through its “National Strategy to Prevent Plastic Pollution,” emphasizing source reduction and bio-based alternatives.

Germany Biodegradable Plastic Packaging Market Strengthened by Circular Economy and Regulatory Compliance

Germany’s biodegradable plastic packaging industry operates under the stringent EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating full recyclability or reusability by 2030. Specific requirements for industrially compostable plastics, including tea and coffee bags, encourage innovation in material design. The German Packaging Act (VerpackG) further ensures producer responsibility across the product lifecycle, promoting packaging compatible with recycling streams.

Innovation is at the forefront, with Sappi Europe introducing high-barrier recyclable papers and Mondi Group developing FunctionalBarrier Paper as mono-material alternatives to multilayer plastics. The sector sees strong demand in food and beverage, pharmaceutical, and hygiene applications, particularly for compostable packaging of fresh produce and short-shelf-life goods. Germany also remains a global hub for research and development, with companies and institutions collaborating to create stronger, lighter, and more sustainable biodegradable plastic solutions.

China Biodegradable Plastic Packaging Market Expands on Dual Carbon Goals and Domestic Innovation

China’s biodegradable plastic packaging market is driven by the government’s “dual carbon” initiative and the five-year plan (2021–2025), focusing on eliminating single-use plastics and promoting bio-based materials. The State Administration for Market Regulation (SAMR) has implemented evolving regulatory frameworks and GB standards to align with global safety and consumer protection benchmarks, providing clear guidance for sustainable packaging development.

Technological innovation, including AI and “5G plus industrial internet” integration, is enhancing production efficiency and flexibility. Domestic manufacturing is prioritized, reducing dependence on imported technologies while meeting the growing demand for biodegradable packaging in e-commerce and food delivery sectors. Biodegradable plastics are widely applied in food, beverage, and consumer goods packaging. China ranks second globally in patents for biodegradable plastics, reflecting strong research contributions and continuous innovation in sustainable plastic materials.

India Biodegradable Plastic Packaging Market Driven by Sustainability Initiatives and Corporate Investments

India’s biodegradable plastic packaging sector is supported by government programs such as “Make in India” and “Zero Effect Zero Defect,” promoting domestic quality production. The National Mission on Sustainable Packaging Solutions by CSIR emphasizes development of sustainable materials and recycling methods. Regulatory support from MoEFCC and FSSAI, including amendments to the Plastic Waste Management (PWM) Rules, requires Central Pollution Control Board (CPCB) certification for compostable materials.

Adoption of automated packaging systems is rising, with companies like UFlex Ltd. achieving USFDA approval in March 2025 for recycled material use in food packaging. Eco-conscious corporations such as Bambrew are producing biodegradable alternatives for e-commerce and food service sectors. Key applications include snacks, ready-to-eat meals, and dairy products, driven by India’s expanding food processing industry and governmental focus on food safety, quality, and environmental sustainability.

Brazil Biodegradable Plastic Packaging Market Strengthened by EPR Framework and Green Manufacturing

Brazil’s biodegradable plastic packaging market is shaped by the National Solid Waste Policy (2010), which mandates reverse logistics under Extended Producer Responsibility (EPR). A 2024 law bans single-use disposable items and sets a 2030 target for packaging to be returnable, recyclable, or fully compostable. Companies like Qualy margarine are reintegrating recycled polypropylene into their packaging chains, demonstrating commitment to circular economy practices.

Technological advancements, including robotics and AI, improve operational efficiency, defect detection, and automated sorting. Products like Klabin’s Wicket Paper Bag for diapers, which is fully recyclable and repulpable, exemplify the market’s sustainable packaging innovation. The food, beverage, and cosmetics sectors are major demand drivers, supported by Brazil’s expanding food processing industry. Governmental initiatives targeting 30% mandatory recycling in the short term and 50% by 2040 provide strong policy support for biodegradable plastic adoption.

Japan Biodegradable Plastic Packaging Market Advances Through Bioplastics Roadmap and Smart Packaging Technology

Japan’s biodegradable plastic packaging market leverages advanced manufacturing technologies and government guidance. The Plastic Resource Circulation Act (2022) emphasizes eco-design and single-use plastic reduction, while the bioplastics roadmap targets mass adoption by 2030. Smart packaging adoption is increasing, integrating sensors and digital monitoring to improve product safety and shelf life, relying on advanced biodegradable materials.

Innovation in functionality focuses on dimensional stability, deformation resistance, and high-performance applications. Leading companies like Toppan are developing recyclable, lightweight, and biodegradable paper-plastic hybrid packaging with high barrier properties. Academic research in Japan further supports innovation through biopolymer and natural agent development, strengthening the market’s capacity for sustainable and functional packaging solutions across food, consumer goods, and specialized applications.

Biodegradable Plastic Packaging Market Report Scope

Biodegradable Plastic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$74.6 Billion

|

|

Market Size (2034)

|

$139.5 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Material Type (Bioplastics), By Packaging Type (Flexible Packaging, Rigid Packaging), By End-Use Industry (Food & Beverages, Pharmaceuticals & Medical, Personal Care & Cosmetics, Consumer Goods, Agriculture & Horticulture, Others), By Application (Food Packaging, Beverages Packaging, Consumer Goods Packaging, Personal Care Packaging, Medical Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mondi Group, Amcor plc, DS Smith Plc, Smurfit Kappa Group, International Paper Company, WestRock Company, Huhtamäki Oyj, Stora Enso Oyj, Sonoco Products Company, NatureWorks LLC, Danimer Scientific, Innovia Films, Novamont S.p.A., Biome Bioplastics Ltd., Elevate Packaging

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biodegradable Plastic Packaging Market Segmentation

By Packaging Type

- Flexible Packaging

- Rigid Packaging

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Medical

- Personal Care & Cosmetics

- Consumer Goods

- Agriculture & Horticulture

- Others

By Application

- Food Packaging

- Beverages Packaging

- Consumer Goods Packaging

- Personal Care Packaging

- Medical Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Biodegradable Plastic Packaging Market

- Mondi Group

- Amcor plc

- DS Smith Plc

- Smurfit Kappa Group

- International Paper Company

- WestRock Company

- Huhtamäki Oyj

- Stora Enso Oyj

- Sonoco Products Company

- NatureWorks LLC

- Danimer Scientific

- Innovia Films

- Novamont S.p.A.

- Biome Bioplastics Ltd.

- Elevate Packaging

* List Not Exhaustive

Research Coverage

This report investigates the Global Biodegradable Plastic Packaging Market in depth, examining market dynamics, breakthrough material innovations, and strategic developments that define the shift toward sustainable packaging. Compiled by USDAnalytics, this analysis reviews how emerging biopolymers such as PLA (Polylactic Acid) and PHA (Polyhydroxyalkanoates) are reshaping the packaging value chain across food, beverages, personal care, and pharmaceutical sectors. It highlights the impact of regulatory shifts, R&D investments, and corporate sustainability commitments driving large-scale biodegradable adoption. The report underscores how compostable and bio-based packaging aligns with the circular economy, helping brands achieve net-zero waste objectives. Through detailed company profiling, competitive benchmarking, and technology tracking, this report is an essential resource for packaging manufacturers, converters, sustainability leaders, and investors navigating the transition toward eco-efficient packaging solutions. It provides actionable insights into compostability standards, feedstock substitution, and product innovations redefining global packaging strategies. Scope Includes

- Segmentation: By Material Type (Bioplastics), Packaging Type (Flexible, Rigid), End-Use Industry (Food & Beverages, Pharmaceuticals & Medical, Personal Care & Cosmetics, Consumer Goods, Agriculture & Horticulture, Others), and Application (Food Packaging, Beverages Packaging, Consumer Goods Packaging, Personal Care Packaging, Medical Packaging).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Frame: Historic data from 2021–2024 and forecast data from 2025–2034.

- Companies Covered: 15+ leading players, including Amcor, Mondi, DS Smith, Smurfit Kappa, WestRock, Stora Enso, NatureWorks LLC, and BASF SE.

Methodology

USDAnalytics employs a robust, multi-tiered research methodology to ensure precision, credibility, and practical relevance for decision-makers. The approach integrates primary research through direct interviews with material scientists, packaging manufacturers, sustainability executives, and regulators across major regions, alongside secondary research from annual reports, certified compostability databases, trade journals, and patent analyses. Quantitative and qualitative insights are synthesized through data triangulation to validate market size, technology adoption rates, and competitive positioning. The study applies both top-down and bottom-up forecasting models, considering macroeconomic variables, carbon reduction targets, and policy incentives. Scenario-based projections account for innovations in bio-based polymers, degradation efficiency, and end-of-life management systems. By incorporating cross-sector insights and real-time developments, USDAnalytics delivers a holistic and data-driven view of the biodegradable plastic packaging landscape, enabling stakeholders to strategize confidently in a rapidly evolving regulatory and technological environment.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.