Bulk Container Packaging Market Overview: Enabling Global Logistics and Circular Economy

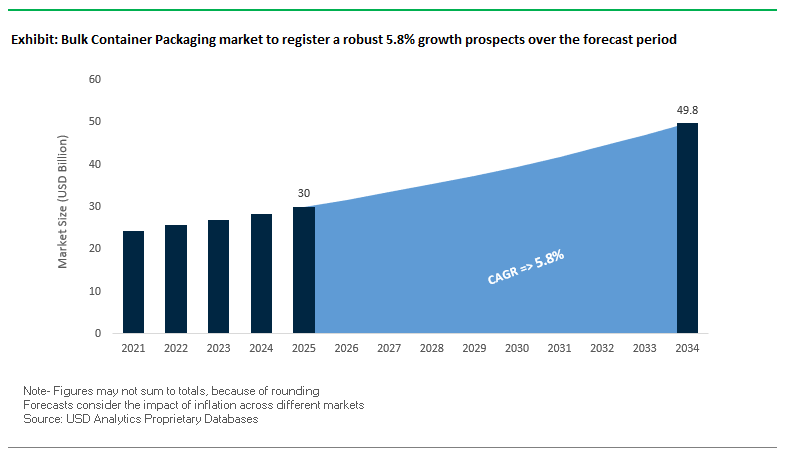

The bulk container packaging market is projected to grow from USD 30 billion in 2025 to USD 49.8 billion by 2034, advancing at a CAGR of 5.8%. As industries seek cost-efficient, safe, and sustainable transport solutions for both liquid and dry commodities, bulk container packaging comprising intermediate bulk containers (IBCs), flexitanks, and liners is playing a pivotal role in reshaping global supply chains. For industry professionals, the key questions are how manufacturers will optimize reusability, recyclability, and efficiency while ensuring regulatory compliance and meeting the surging demand from the chemicals and petrochemicals sector.

Key Insights Defining the Bulk Container Packaging Market

- Plastics Dominate (95% share): High-density polyethylene (HDPE) remains the preferred choice for bulk containers due to its cost-effectiveness, corrosion resistance, and lightweight properties.

- Flexitanks Cut Logistics Costs by 40%: Single-use and recyclable flexitanks provide higher payload capacity than traditional steel drums, reducing transport costs for non-hazardous liquids.

- Reusability Enhances Sustainability: Rigid IBCs can be reconditioned and reused more than 15 times, making them a cornerstone of circular economy practices in industrial logistics.

- Chemicals and Petrochemicals Lead Demand: Bulk container packaging is critical in ensuring contamination-free, spill-proof transport for hazardous and non-hazardous materials.

Market Analysis: Recent Global Bulk Container Packaging Developments

The past year has highlighted the industry’s pivot toward sustainability, smart packaging, and automation to align with both regulatory expectations and industrial needs. In August 2025, reports emphasized the rise of smart FIBCs and bulk containers with RFID and IoT sensors, enabling real-time tracking and supply chain transparency. Similarly, in July 2025, A-B-C Packaging Machine Corporation showcased automated bag-filling and discharge systems that seamlessly integrate with bulk container operations, reducing labor dependence and boosting throughput.

The sector is also undergoing structural changes. The Amcor–Berry Global merger announced in June 2025 is set to create a powerful player in industrial packaging, strengthening global production and distribution networks for bulk containers. In May 2025, academics reported advancements in chemical recycling technologies capable of breaking down multi-layer films used in flexitanks and container liners, a milestone toward circularity. Meanwhile, April 2025 saw a U.S. chemical manufacturer partner with a bulk container supplier to design specialized IBCs for high-purity chemicals, enhancing safety and compliance in sensitive transport applications.

Sustainability has been further reinforced by regulatory and corporate initiatives. The European Union’s February 2025 initiative to promote renewable materials in industrial packaging provides strong momentum for bio-based polymers and recyclable container systems. Earlier, in January 2025, Greif, Inc. expanded its global footprint by opening a new IBC facility in Dilovasi, Turkey, catering to rising demand in the region. Beyond plastics, packaging majors are diversifying: in March 2025, 3M launched a recyclable, paper-based padded mailer, signaling a broader shift toward fiber-based protective packaging. Collectively, these developments reflect how bulk container packaging is becoming more automated, circular, and sustainability-driven.

Emerging Trends and Opportunities Reshaping the Bulk Container Packaging Market

Strategic Material and Design Shift to Enable a Circular Service Economy

The bulk container packaging market is experiencing a structural shift as manufacturers transition from one-time product sales to packaging-as-a-service business models. This approach emphasizes reusability, durability, and lifecycle management, where containers are designed for multi-year service and integrated into closed-loop systems. For example, Schoeller Allibert has highlighted its development of reusable intermediate bulk containers (RIBCs) engineered to last over 10 years and withstand multiple trips, drastically reducing single-use waste and lowering customer disposal costs. In parallel, global logistics providers such as CHEP are extending their established pooling models to bulk containers. Under this model, customers lease containers rather than purchase them, with the provider overseeing delivery, collection, cleaning, and maintenance. This reduces upfront capital expenditure for end-users while creating predictable, recurring revenue for suppliers. By embedding containers into circular service economies, companies are not only meeting sustainability objectives but also unlocking a new, more profitable growth model centered on lifecycle management.

Integration of IoT and Smart Technologies for Condition Monitoring and Asset Visibility

Bulk containers are rapidly evolving into intelligent, connected assets through the integration of IoT-enabled monitoring systems. Smart containers equipped with sensors provide real-time data on location, humidity, temperature, and shock critical parameters for industries such as pharmaceuticals, chemicals, and food where product integrity and regulatory compliance are paramount. According to a white paper published by the UNECE, smart packaging technologies provide insurance-grade evidence of shipment conditions, thereby reducing disputes and strengthening trust between shippers and customers. The data collected enables a shift from reactive logistics to predictive logistics, empowering companies to forecast delays, identify bottlenecks, and optimize supply chains proactively. Industry players such as Hapag-Lloyd are equipping fleets with IoT devices that not only ensure traceability but also automate manual processes, improving efficiency and minimizing human errors. These systems further optimize route planning, enabling significant fuel savings and carbon footprint reduction, aligning with ESG commitments. As IoT adoption accelerates, bulk containers are becoming strategic tools for enhancing operational visibility and efficiency across global supply chains.

Development of Advanced, Lightweight Composite Materials for RIBCs

One of the most significant opportunities in the bulk container market is the adoption of lightweight composite materials to replace traditional steel and heavy-duty plastic designs. Research indicates that composite blends such as plastic reinforced with fiberglass offer superior strength-to-weight ratios, enabling containers to withstand aggressive chemical handling while being significantly lighter than conventional alternatives. These innovations directly reduce transportation costs by lowering packaging weight, thereby decreasing fuel consumption and increasing payload capacity per shipment. In industries like specialty chemicals, pharmaceuticals, and food ingredients, these materials also deliver enhanced corrosion resistance, extending container lifespans and minimizing maintenance needs. As companies focus on reducing carbon footprints and improving logistics efficiency, lightweight composite RIBCs are positioned to become a high-growth segment, enabling sustainability and performance advantages simultaneously.

Standardization and Interoperability to Enable Cross-Company Asset Pooling

The lack of interoperability between different bulk container systems is a major barrier to supply chain efficiency, creating underutilized assets and costly empty returns. The industry now has a significant opportunity to embrace standardization and cross-company collaboration to build interoperable pooling systems. Organizations such as the Digital Container Shipping Association (DCSA) are spearheading efforts to create global, vendor-neutral standards for container dimensions and IoT data exchange. By aligning on common specifications, containers from different manufacturers could be shared within the same pooling network. This would allow a company to lease a container from one provider and return it to any certified hub, even if the next user is from another organization. Such interoperability would maximize asset utilization, reduce the cost and emissions of repositioning empty containers, and unlock new efficiencies across global trade networks. For container manufacturers and pooling providers, this represents a transformative opportunity to scale collaborative ecosystems and capture long-term customer loyalty.

Competitive Landscape: Leading Companies in Bulk Container Packaging

The bulk container packaging market is highly competitive, with global corporations and specialized firms leveraging scale, sustainability, and innovation to strengthen their position.

Greif, Inc. expands IBC capacity with new facility in Turkey

Greif offers a full portfolio of industrial packaging, including IBCs, steel drums, fiber drums, and bulk liners. In January 2025, the company opened a new IBC plant in Dilovasi, Turkey, boosting its regional capacity. Its strength lies in its global scale and diverse product offering, serving chemicals, food & beverage, and pharma. Greif’s focus is on remanufactured and reconditioned IBCs, aligning with circular economy goals.

Mauser Packaging Solutions drives circular economy with reconditioning services

Mauser is a global leader in rigid industrial packaging, producing IBCs, plastic containers, and steel drums. The company has been expanding globally, including its Poland facility expansion in May 2023, alongside earlier projects in Singapore and China. Its core strength is a closed-loop IBC system, offering customers reconditioning and recycling services to extend product lifecycles and reduce waste.

Schoeller Allibert invests in smart, reusable bulk container innovations

Schoeller Allibert specializes in reusable rigid bulk containers, pallet boxes, and foldable large containers. Its R&D teams are pioneering IoT-enabled containers for real-time tracking and monitoring. Known for its durable, circular products, the company’s focus is on helping clients cut logistics costs and enhance sustainability through reusable container systems.

Berry Global Group commits to net-zero and circular plastics

Berry Global has a strong footprint in industrial packaging, with a diverse portfolio including FIBCs, films, and protective solutions. In 2024, Berry committed to net-zero by 2050 and invested in expanding recycling capacity by 6,600 tonnes per year in Europe. Its “B Circular Strategy” drives innovation in bio-based and recycled polymers, reinforcing its position as a sustainability leader.

Nefab AB strengthens global reach with engineered packaging acquisition

Nefab focuses on engineered, multi-material bulk packaging, offering collapsible containers and custom solutions. Recently, the company acquired Szkaliczki & Partners Plastic Processing Ltd. in Hungary, enhancing its design and production capabilities. Nefab’s key strength lies in eco-optimized, cost-efficient solutions that integrate design, engineering, and logistics services, providing a full-service experience for global clients.

DS Smith plc leverages fiber-based bulk packaging to drive sustainability

DS Smith is a leader in corrugated and fiber-based bulk containers, catering to e-commerce, FMCG, and industrial clients. In July 2024, it launched PackRight 2.0, a collaborative platform for sustainable packaging design. Its competitive advantage is its renewable material base and full recyclability, positioning it as a strong player in the circular packaging economy.

Bulk Container Packaging Market Share Insights

Market Share by Product Type in the Bulk Container Packaging Industry

Intermediate Bulk Containers (IBCs) lead the global bulk container packaging market with a 35% share in 2025, reflecting their unmatched efficiency in liquid storage and transportation. IBCs offer 3–4 times the capacity of standard drums while occupying less floor space, making them indispensable for optimizing warehouse and shipping operations. Their integrated features, such as bottom drains for easy dispensing and stackability for space savings, drive adoption in chemicals, food-grade liquids, and other non-hazardous products. Drums and barrels remain close behind with a 30% market share, anchored by their regulatory necessity and versatility. Steel drums are mandated for hazardous and flammable goods, while plastic and fiber drums dominate in food, beverages, and household chemicals. Their durability, reusability, and compliance with global safety standards ensure their continued importance despite growing competition from IBCs and flexitanks. Flexitanks are the fastest-growing product type, disrupting the market for long-distance bulk liquid transport. By fitting inside standard shipping containers and offering 16,000–24,000 liters of capacity, they dramatically cut per-unit shipping costs for non-hazardous liquids like wine, edible oils, and juices. This cost advantage, combined with their single-use hygienic design, is eroding the reliance on traditional drums and IBCs for specific trade flows. Material handling containers hold a steady share, serving as the backbone of in-plant logistics for industries like automotive and manufacturing that require reusable bins, totes, and large boxes for solid parts and components. Bulk liners and pails represent smaller but specialized roles liners ensure contamination-free transport of powders and dry goods, while pails cater to specialty chemicals, adhesives, and paints requiring small, controlled volumes. Together, these diverse packaging solutions highlight the market’s balance between cost efficiency, safety, and application-specific needs.

Market Share by End-Use Industry in the Bulk Container Packaging Industry

The chemicals and petrochemicals industry dominates the bulk container packaging market with a commanding 40% share in 2025, driven by its need for regulatory-compliant, high-performance packaging solutions. This sector requires the full portfolio of packaging formats from steel drums for hazardous chemicals to IBCs for industrial liquids and flexitanks for specific solvents making it the most critical end-user. The food and beverage industry follows with 25% of the market, emerging as a volume powerhouse. Demand here is centered on food-grade IBCs, flexitanks, and drums for edible oils, juices, concentrates, and wine, with absolute requirements for purity and compliance with FDA and EU food safety standards. Growth in international trade of bulk liquids makes flexitanks a preferred option for cost-sensitive but high-volume exports. The industrial and automotive sectors form another cornerstone of demand, utilizing bulk packaging for lubricants, coatings, paints, and manufacturing chemicals, as well as relying on reusable material handling containers to streamline in-plant logistics. Pharmaceuticals represent a smaller but high-value share of the market, requiring single-use or dedicated containers with validated sterility, full traceability, and strict adherence to Good Manufacturing Practices (GMP). The agriculture industry also accounts for a notable share, using IBCs and liners for fertilizers, pesticides, and agrochemicals, while drums cater to smaller-volume packaging needs. Finally, construction and other sectors contribute steady demand for bulk packaging solutions, particularly for adhesives, coatings, and building materials. Across these industries, the balance of regulatory compliance, logistics efficiency, and product integrity defines the distribution of market share.

United States: Sustainable, Smart, and Specialized Bulk Container Packaging Solutions

The U.S. bulk container packaging market is undergoing a significant transformation as sustainability becomes a central focus across industries. Corporations are aligning with circular economy principles by adopting reusable and recyclable bulk containers, moving away from single-use options. This trend is particularly strong in the chemical, agricultural, and food and beverage sectors, where both regulatory compliance and consumer expectations are pushing companies toward eco-friendly alternatives. Demand for intermediate bulk containers (IBCs) and drums with superior barrier properties is also on the rise, especially for transporting high-value goods such as chemicals and high-purity liquids.

In addition to sustainability, the U.S. market is rapidly embracing smart packaging technologies. Manufacturers are integrating IoT sensors and RFID tags into bulk containers, enabling real-time monitoring of temperature, humidity, fill levels, and geographic location. These innovations are improving supply chain visibility, reducing losses, and enhancing product safety for sensitive goods like pharmaceuticals and perishable foods. Furthermore, strategic investments by industry leaders such as Greif underscore the country’s growing production capacity, with expansions designed to meet increasing demand for both standard and specialized bulk container solutions.

China: Manufacturing Powerhouse with Regulatory-Driven Innovation in Bulk Containers

China dominates the global bulk container packaging market as both the leading producer and consumer, supported by its expansive chemical, agricultural, and industrial base. This vast industrial output creates consistent demand for bulk containers, positioning China at the core of international trade and supply chain activity. The country’s manufacturing strength, combined with its cost-efficient production capabilities, allows it to supply both domestic and export markets at scale.

However, regulatory frameworks are reshaping the industry. The upcoming mandatory national standard GB 45835 2025, governing the packaging of dangerous goods (effective June 2026), is compelling manufacturers to adopt new safety features and improve container integrity. This shift is expected to spark innovation in areas such as anti-leakage technologies, impact resistance, and compliance-driven designs. Additionally, automation and robotics are being widely adopted to enhance production efficiency and quality control. With a parallel push toward the circular economy, Chinese manufacturers are investing in recyclable and reusable bulk container solutions to reduce plastic waste and meet both government mandates and sustainability goals.

Germany: Sustainability and IoT-Enabled Bulk Container Packaging at the Forefront

Germany’s bulk container packaging market is strongly shaped by the European Green Deal and related sustainability regulations, making the country a frontrunner in reusable and environmentally friendly packaging innovations. Companies are increasingly focusing on bulk container solutions that are not only durable but also recyclable, ensuring compliance with EU directives aimed at advancing the circular economy. This regulatory-driven focus on eco-friendly packaging is reinforced by Germany’s leadership in high-value industries such as chemicals, automotive, and pharmaceuticals, where specialized bulk container packaging plays a critical role.

Digitalization is also a defining factor in Germany’s bulk container market. Companies such as Packwise are pioneering IoT-enabled monitoring platforms for intermediate bulk containers, enabling global leaders like BASF and Merck to track container conditions in real time. This digital transformation improves logistics, reduces waste, and enhances operational efficiency. At the same time, Germany is innovating in high-performance bulk container solutions with features such as anti-static properties and advanced thermal insulation, further supporting industries where safety and precision are paramount.

Brazil: Industrial Growth and Smart, Eco-Friendly Bulk Container Packaging Solutions

Brazil is witnessing rapid expansion in the bulk container packaging market, driven by a growing industrial base and surging international trade, particularly in agricultural commodities and chemicals. The demand for robust bulk containers is growing alongside the country’s role as a leading exporter of grains, sugar, and industrial raw materials. Companies are increasingly adopting bulk containers designed to optimize transport efficiency and ensure safety across long-distance shipments.

Sustainability is becoming a dominant theme in Brazil’s packaging landscape, with manufacturers shifting to reusable and recyclable solutions to comply with emerging regulations aimed at reducing plastic waste. Investment is also accelerating, with companies like Rishi FIBC establishing new, high-capacity production facilities in Brazil to serve both domestic demand and export markets. Additionally, the adoption of smart technologies such as RFID-enabled bulk containers and IoT-based condition monitoring is enhancing supply chain efficiency, lowering costs, and strengthening Brazil’s competitiveness in the global bulk container packaging industry.

India: Expanding Manufacturing Base and Growing Demand for Specialized Bulk Containers

India’s bulk container packaging market is expanding rapidly under the “Make in India” initiative, which is fueling growth in domestic manufacturing and industrial output. Demand is particularly strong from the chemical, pharmaceutical, and food and beverage sectors, where bulk containers play a crucial role in ensuring cost-effective and safe transportation. The country’s rapid industrialization is boosting local demand while simultaneously creating opportunities for export-oriented growth in container manufacturing.

A major trend in India is the growing emphasis on sustainability, reinforced by government-driven plastic waste management rules that encourage the adoption of recyclable and reusable packaging. This push is opening doors for both domestic manufacturers and international players investing in sustainable solutions. At the same time, the demand for specialized products such as UN-certified bulk containers for hazardous goods and food-grade packaging for exports is increasing significantly. By combining sustainability initiatives, regulatory compliance, and export-focused innovation, India is establishing itself as a competitive and fast-growing hub in the global bulk container packaging market.

Bulk Container Packaging Market Report Scope

Bulk Container Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$30 Billion

|

|

Market Size (2034)

|

$49.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Product Type (Intermediate Bulk Containers, Drums & Barrels, Pails, Flexitanks, Bulk Container Liners, Material Handling Containers), By Material (Plastic, Metal, Paper & Paperboard, Others), By End-Use Industry (Chemicals & Petrochemicals, Food & Beverage, Pharmaceuticals, Industrial, Agriculture, Automotive, Construction, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Greif, Inc., Berry Global Inc., Mauser Packaging Solutions, DS Smith plc, Schütz GmbH & Co. KGaA, Nefab Group, Schoeller Allibert, RPC Group, RDA Bulk Packaging Ltd., The Mondi Group, Braid Logistics, Bulk Lift International, Sonoco Products Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bulk Container Packaging market Segmentation

By Product Type

- Intermediate Bulk Containers

- Drums & Barrels

- Pails

- Flexitanks

- Bulk Container Liners

- Material Handling Containers

By Material

- Plastic

- Metal

- Paper & Paperboard

- Others

By End-Use Industry

- Chemicals & Petrochemicals

- Food & Beverage

- Pharmaceuticals

- Industrial

- Agriculture

- Automotive

- Construction

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bulk Container Packaging market

- Greif, Inc.

- Berry Global Inc.

- Mauser Packaging Solutions

- DS Smith plc

- Schütz GmbH & Co. KGaA

- Nefab Group

- Schoeller Allibert

- RPC Group

- RDA Bulk Packaging Ltd.

- The Mondi Group

- Braid Logistics

- Bulk Lift International

- Sonoco Products Company

*List not Exhaustive

Research Coverage

This comprehensive report by USDAnalytics investigates the global bulk container packaging market, highlighting breakthroughs, technological advancements, and emerging strategies that are reshaping industrial logistics. The analysis reviews the evolution of intermediate bulk containers (IBCs), flexitanks, drums, liners, and material handling containers, with a focus on innovations in IoT-enabled monitoring, smart materials, reusability, and circular economy adoption. It highlights key drivers, competitive strategies, and regulatory developments shaping the market, emphasizing sustainability, safety, and operational efficiency. This report is an essential resource for manufacturers, logistics providers, and end-users aiming to optimize cost, performance, and environmental compliance. It also covers market dynamics, competitive insights, and global adoption trends, providing actionable intelligence for decision-makers seeking to enhance supply chain visibility, reduce environmental impact, and capitalize on growth opportunities across high-demand sectors such as chemicals, petrochemicals, food & beverage, pharmaceuticals, and industrial applications.

Scope Highlights:

- Segmentation: By Product Type (Intermediate Bulk Containers, Drums & Barrels, Pails, Flexitanks, Bulk Container Liners, Material Handling Containers); By Material (Plastic, Metal, Paper & Paperboard, Others); By End-Use Industry (Chemicals & Petrochemicals, Food & Beverage, Pharmaceuticals, Industrial, Agriculture, Automotive, Construction, Others)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies Covered: In-depth analysis and profiles of 15+ key companies including Greif, Inc., Berry Global Inc., Mauser Packaging Solutions, DS Smith plc, Schütz GmbH & Co. KGaA, Nefab Group, Schoeller Allibert, RPC Group, RDA Bulk Packaging Ltd., The Mondi Group, Braid Logistics, Bulk Lift International, and Sonoco Products Company.

Methodology

This report employs a multi-step research methodology integrating both primary and secondary sources to ensure accuracy and actionable insights. Primary research involved consultations with bulk container manufacturers, suppliers, distributors, and industry experts, capturing real-time data on production, capacity utilization, technological adoption, and market preferences. Secondary research reviewed company reports, industry journals, regulatory frameworks, government databases, and trade publications. Market sizing and forecasting were performed using a bottom-up approach, incorporating historical shipment volumes, production capacities, adoption rates, and emerging industry trends. Competitive benchmarking and market share analysis were conducted using proprietary models, factoring product types, material compositions, and end-use segmentation. All projections from 2025 to 2034 incorporate macroeconomic assumptions, industrial growth patterns, and sustainability-driven adoption, ensuring the findings provide a realistic and strategic roadmap for stakeholders in the global bulk container packaging market.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.