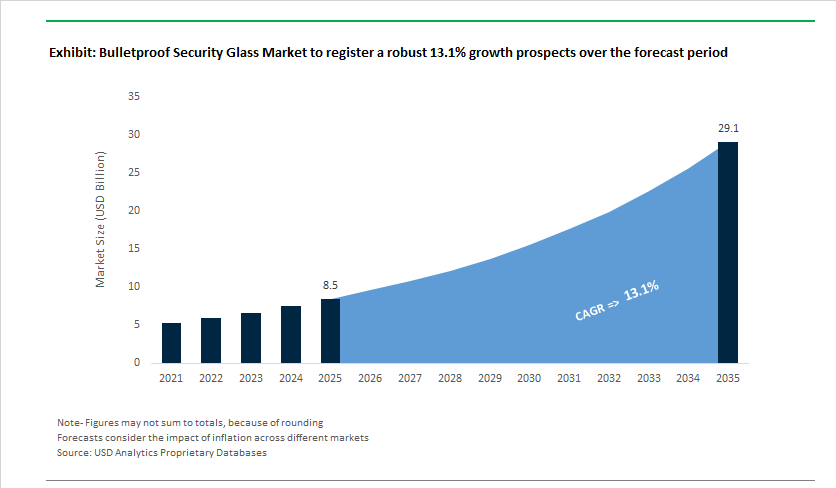

The Bulletproof Security Glass Market is valued at USD 8.5 billion in 2025 and is forecast to grow to USD 29.1 billion by 2035 at a CAGR of 13.1% (2025-2035). Rapid urban infrastructure hardening, expansion of cash-in-transit and VIP armored transport, defense vehicle modernization, and rising architectural requirements for blast- and forced-entry-resistant glazing are the primary demand engines.

Market Analysis: Regulatory Mandates, Capacity Expansion, and Materials Innovation Reshaping Supply Dynamics

The bulletproof security glass sector has seen concentrated investment and product innovation that materially affect supply, specification, and cost dynamics. In September 2024, new U.S. state mandates requiring Level 3 ballistic protection at public service counters catalyzed near-term demand spikes for laminated ballistic glazing in government buildings and service centers. Following regulatory pull, suppliers and converters accelerated capacity - notably an Asian-Pacific glass producer commissioned a third autoclave in February 2025, expanding regional throughput for multi-layer ballistic laminates tailored to banking, luxury armored transport, and CIT fleets. Product innovations have continued in tandem: August 2024 saw a security vehicle OEM introduce a light-armored SUV relying on thinner-gauge ballistic glass by substituting standard PVB with SentryGlas interlayers, demonstrating the market trend toward thinner, higher-performance laminates that preserve optical clarity.

Parallel to capacity and product shifts, R&D breakthroughs are moving ceramic transparent armor and anti-spall technologies closer to mainstream use. An academic-industry consortium published a transparency improvement in ALON ceramics in December 2024, increasing feasibility for lighter aircraft and vehicle transparencies. In April 2025, a specialized security materials firm launched a non-spall coating for polycarbonate-glass laminates that reduces projectile penetration depth by an additional ~5%, enhancing occupant protection after high-velocity impacts. On the investment front, June 2025 included a major European glazing manufacturer announcing a USD 200 million production line investment for blast-resistant and anti-intrusion laminated glass aimed at critical urban infrastructure projects, signaling firm commercial demand from public and private sectors for façade-grade ballistic glazing.

Procurement and Product Development Strategies:

Security architects, defense procurement officers, and fleet spec engineers are evaluating ballistic glazing solutions across four interlocking criteria: threat level certification (ANSI/UL/EN standards), optical clarity and light transmission, weight/space trade-offs for vehicles and facades, and integration with framing and anti-spall systems. Modern solutions blend polycarbonate glazing, PVB/SentryGlas interlayers, and advanced ceramic transparent armor (ALON, spinel) to deliver multi-hit capability, low spall, and minimized thickness for vehicle/aircraft weight control. For building projects, spec writers must balance ANSI Z97.1 performance with visible light transmission and façade aesthetics; more than 85% of new architectural security projects now demand ballistic glazing that meets minimum ANSI standards without compromising transparency.

Key Buyer-Focused Insights

- Performance benchmark: Polycarbonate glazing used in glass-clad laminates offers impact resistance up to ~250× greater than conventional tempered glass at equivalent thickness-critical for forced-entry and CIT (cash-in-transit) vehicle specs.

- Lightweight ceramic armor: ALON-based transparent armor achieves ~50% reductions in thickness/weight vs traditional glass-polymer laminates-vital for high-security vehicles and aircraft where payload and range matter.

- Architectural integration: Over 85% of new commercial security projects require ballistic glazing that preserves optical clarity (high light transmission/low distortion) while meeting ANSI/UL ballistic ratings.

- Defense adoption: An estimated >40% of some military vehicle procurement budgets are being allocated to transparent armor systems with multi-hit and blast-fragmentation protection.

- Interlayer strategy: High-performance interlayers (SentryGlas, advanced PVB/Trosifol films) enable thinner laminates and better post-impact integrity-key to meeting rifle-level and multi-hit requirements without unacceptable weight penalties.

Bulletproof Security Glass Market Trends and Opportunities

Trend 1: Hybrid Laminated Systems for Forced-Entry and Ballistic Mitigation

Security glazing requirements are being redefined by the evolution of modern threat profiles, which increasingly involve multi-stage attacks that combine ballistic assault with prolonged forced-entry attempts. As a result, glazing systems are no longer specified solely for ballistic resistance but are being engineered as hybrid, multi-hazard barriers. In 2025, security glass manufacturers are prioritizing “blended threat” laminated architectures that simultaneously meet high ballistic ratings—such as UL 752 Level 8—and stringent forced-entry standards like ASTM F1233 Class 5. Industry technical bulletins following recent armored vehicle launches highlight that ballistic impacts alone can compromise traditional glass layers, but advanced interlayer chemistry and laminate sequencing now allow the glass to retain structural integrity long enough to delay or prevent manual breach using tools. This capability is increasingly critical for public-facing assets, including transit systems and financial institutions, where delay time is a core security metric. Civilian infrastructure is already reflecting this shift: public transit authorities have begun deploying multi-hazard protective enclosures for operators, using military-grade laminated glass designed to withstand both small-arms fire and sustained physical assault. At the material level, studies published in 2025 demonstrate that combining high-modulus glass plies with advanced polyurethane or ionoplast interlayers enables thinner, optically clear constructions that dissipate kinetic energy without catastrophic delamination. This balance between aesthetics, transparency, and multi-hit durability is accelerating adoption in high-end retail, government buildings, and critical urban infrastructure.

Trend 2: Integration of Functional Layers for “Smart” Security Glazing

Security glazing is rapidly converging with smart materials engineering, as functional layers are embedded directly into ballistic laminate stacks to address electronic, environmental, and operational threats. In 2025, high-security facilities are increasingly specifying glazing systems with integrated electromagnetic pulse (EMP) and signal-shielding capabilities to meet TEMPEST-level requirements. By embedding micro-fine conductive meshes and metallic coatings within the laminate, manufacturers are enabling windows that attenuate electromagnetic emissions while maintaining ballistic integrity—an essential requirement for data centers, command facilities, and secure financial institutions facing risks of electronic surveillance or interference. At the same time, tactical privacy has emerged as a differentiating feature. Recent demonstrations of switchable transparency technologies show that ballistic glass can transition from fully transparent to opaque in milliseconds, allowing occupants to instantly obscure visibility during a security incident and deny adversaries a clear line of sight. Environmental durability is also being engineered into these systems. Integrated heating elements and UV-stable interlayers are now used to mitigate delamination, haze formation, and microcracking caused by extreme temperature cycling and prolonged UV exposure. Technical evaluations in 2025 indicate that these functional layers can extend the service life of exterior security glazing by 25–30%, materially lowering lifecycle costs for assets deployed in harsh climates while preserving optical clarity and protection levels.

Opportunity 1: Blast-Resistant Glazing for Civilian Critical Infrastructure

Blast-mitigation glazing is transitioning from a defense-specific requirement to a mainstream component of civilian critical infrastructure design. Updated security frameworks and regulatory guidance issued in 2025 emphasize resilience against cascading physical impacts, particularly for transport hubs, energy facilities, and densely populated public buildings. As a result, blast-resistant glazing is being mandated alongside ballistic and forced-entry protection, creating a new compliance-driven demand cycle. Updated design guidance now favors “balanced design” facades, where glazing, frames, and anchoring systems are engineered as an integrated unit to prevent premature failure and secondary hazards such as glass fragmentation. Laminated inner panes with increased thickness are being specified to reduce the risk of flying debris during blast events, even when the outer facade is compromised. High-risk industrial sectors—including oil, gas, and chemical processing—are also accelerating adoption of blast-resistant buildings that incorporate large-format, pressure-absorbing glazing. These systems are designed not only to protect personnel but also to maintain operational continuity after an explosion, aligning safety compliance with business resilience. As regulatory scrutiny intensifies, blast-resistant glazing is becoming a standard feature rather than a discretionary upgrade, particularly for assets classified as nationally or economically critical.

Opportunity 2: Commercialization of Transparent Ceramic and ALON Armor

Transparent ceramics are emerging as one of the most disruptive material opportunities in the security and protection landscape, moving rapidly from niche defense applications into broader commercial deployment. Aluminum oxynitride (ALON) and advanced glass-ceramic systems offer a step-change in performance by delivering equivalent ballistic protection at roughly half the weight and a fraction of the thickness of traditional laminated glass. In 2025, scaled production initiatives are targeting mobility and aerospace platforms where weight reduction directly translates into performance gains, fuel efficiency, and extended operational range. Transparent ceramics also deliver superior hardness and scratch resistance, enabling multi-hit durability and long service life in abrasive or high-speed environments. Product launches in 2025 indicate that manufacturers are increasingly positioning glass-ceramics as cost-effective alternatives to sapphire, balancing extreme hardness with manufacturability at scale. At the industry level, consolidation and strategic acquisitions are accelerating the commercialization curve, as larger materials groups integrate near-net-shape forming and advanced sintering techniques to reduce machining waste and energy consumption. This industrial scaling is expanding addressable markets beyond military platforms into civilian armored vehicles, aviation canopies, and even high-end medical imaging systems where optical clarity and impact resistance are mission-critical.

Bulletproof Security Glass Market Share Analysis

Market Share by Security Level: Medium-Protection Ballistic Glass Sets the Commercial Benchmark

Medium-protection bulletproof security glass accounts for an estimated 42.5% share of the global Bulletproof Security Glass Market, reflecting its role as the default specification for high-traffic commercial and institutional buildings. This segment—typically aligned with UL 752 Level 3 in North America and EN 1063 BR4 in Europe—has become the market standard because it directly addresses the most prevalent real-world ballistic threats, particularly high-velocity handgun attacks, while remaining economically viable for large-scale deployment. From a performance perspective, Level 3 ballistic glass is engineered to stop multiple impacts from a .44 Magnum without penetration or interior spall, a requirement that has elevated “no-spall” performance from a premium feature to a baseline procurement criterion. Market share is further reinforced by material innovation, as manufacturers increasingly replace traditional thick laminated glass with glass-clad polycarbonate (GCP) architectures, delivering up to 40% weight reduction while maintaining certified ballistic ratings. This lower thickness-to-weight ratio is strategically important for retrofitting projects, where existing frames and façades cannot accommodate heavier assemblies. Optical clarity also plays a decisive role in purchasing decisions, as medium-protection glass can achieve visible light transmittance levels approaching 85%, enabling secure yet visually open environments in banks, retail stores, and corporate facilities. Collectively, the segment’s dominance reflects a clear value proposition: certified handgun threat protection, manageable installation costs, architectural compatibility, and long-term durability, making medium-protection ballistic glass the most widely specified and scalable security level globally.

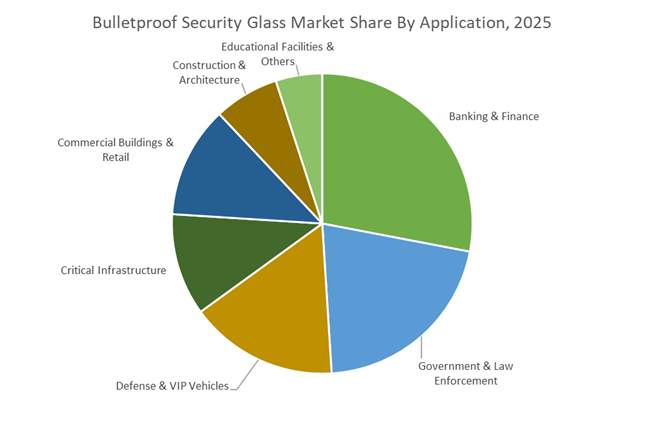

Market Share by Application: Banking & Financial Institutions Remain the Anchor Demand Segment

The banking and finance sector holds approximately 28% of total bulletproof security glass demand, positioning it as the single largest application segment and a structural anchor for market stability. Financial institutions continue to prioritize physical security investments as a frontline deterrent against armed robberies, with teller lines and transaction counters increasingly reinforced by certified ballistic glazing systems. Empirical operational data show that branches equipped with visible bulletproof barriers experience materially lower robbery incidence, as hardened environments shift attacker behavior toward less protected targets. Within this segment, non-spalling performance is non-negotiable, given the close proximity of staff to the glass; polycarbonate-backed or film-reinforced interior layers are now standard to eliminate secondary injury risks from glass fragmentation. Market share is further supported by the evolution of multifunctional security glass, which integrates ballistic resistance with thermal insulation and acoustic damping. Banks adopting these solutions can simultaneously enhance security, reduce ambient noise at teller stations, and lower energy consumption—often achieving 15–20% savings in heating and cooling costs through improved U-values. Durability also underpins long-term adoption, as professionally coated security glass resists surface abrasion and discoloration, extending service life beyond a decade and lowering total cost of ownership compared to acrylic substitutes. As banks balance security, customer experience, and operational efficiency, bulletproof security glass remains a core infrastructure investment, sustaining the segment’s leading share in the global market.

Competitive Landscape: Market Leaders’ Strategic Strengths and Product Differentiation

The competitive landscape for ballistic and security glazing is anchored by vertically integrated glassmakers, specialty interlayer suppliers, and aerospace/defense coating specialists. Leading players differentiate through certified ballistic solutions (FB/BR/UL ratings), proprietary interlayers and films, curved and complex armor capabilities for vehicles, and integrated glass+frame certified systems for critical infrastructure tenders.

Saint-Gobain (Vetrotech) - Certified Multi-Functional Ballistic Glazing With Integrated Façade Systems

Saint-Gobain’s Vetrotech division provides high-security glazing certified up to FB7/BR7 and integrates lamination, fire-rating, and solar control into unified systems-critical for tenders that demand whole-assembly certification rather than glass-only claims. The company leverages large float glass capacity and in-house lamination technologies to deliver multi-functional security glazing, while expanding localized manufacturing in high-growth regions (e.g., India) to meet defense and infrastructure requirements. Vetrotech’s focus on integrated certified systems (glass + framing) makes it a preferred partner for banking, government, and high-security architectural projects where end-to-end compliance is mandatory.

AGC Inc. - Curved Transparent Armor and Low-Spall Laminates For Vehicle Armoring

AGC combines deep automotive glass expertise with transparent armor capabilities for VIP and law-enforcement vehicles, producing complex-shaped, curved ballistic glass and glass-resin laminates engineered for low spall performance. R&D emphasis on chemically strengthened glass and advanced PVB/polycarbonate interlayers has reduced weight by up to 15% for equivalent protection levels-an advantage for cash-in-transit fleets and armored transport where payload and drivability are critical. AGC’s targeting of CIT and law-enforcement segments underlines its mix of optical clarity, certification, and manufacturability for high-volume armored vehicle conversions.

Guardian Glass (Koch) - Architectural Security Glazing With Digital Specification Tools

Guardian supplies core laminated glass solutions (e.g., LamiGlass) used widely in forced-entry, hurricane, and lower-level ballistic applications, with a strong emphasis on aesthetic façades that require blast mitigation without sacrificing transparency. The firm has enhanced its technical services and digital specification tools to accelerate correct thickness/performance calculations against international ballistic standards-streamlining procurement for architects and security consultants. Integration capabilities with high-performance coatings (solar/UV management) mean Guardian’s systems support dual-purpose façades that balance energy performance with security requirements.

PPG Industries - Aerospace-Grade Transparencies and Defense-Spec Laminates For Extreme Impacts

PPG is a leading supplier of high-performance transparencies and coating systems for aerospace and defense applications, producing multi-ply acrylic and glass-polycarbonate laminates used in cockpits and armored enclosures. Its products are engineered to meet stringent military specifications (bird-strike, high-velocity projectile resistance) and PPG’s advanced surface hard coatings extend the service life and scratch resistance of polycarbonate layers used in security laminates. PPG’s portfolio is optimized for defence platforms where weight optimization, optical performance, and military certification are non-negotiable.

Eastman Chemical Company - Interlayer Technology That Enables Thinner, Higher-Rigidity Ballistic Laminates

Eastman dominates the essential interlayer market with PVB (Trosifol) and high-performance films such as SentryGlas, which are significantly stiffer and stronger than conventional PVB-enabling thinner, lighter laminate constructions that still meet UL Level 7/8 rifle-level protection. Eastman’s R&D focuses on energy-absorbing interlayers for blast and repeated impacts, positioning its materials as the backbone for multi-layer assemblies used in government buildings, executive protection, and CIT vehicles. Their interlayers are critical enablers for designers seeking to reconcile high ballistic ratings with slim sightlines and façade aesthetics.

The United States remains the most influential market for bulletproof security glass, driven by a combination of legislative mandates, federal funding, and defense-led material innovation. In 2025, state-level school safety regulations have become a structural demand driver, particularly in states mandating ballistic-resistant glazing at public building entry points. This has accelerated procurement of UL 752 Level 3 and Level 8 bulletproof glass for schools, courthouses, and transportation hubs. Federal “target hardening” programs under the Bipartisan Safer Communities Act are reinforcing long-term demand visibility for laminated ballistic glass and polycarbonate-clad security glazing. On the defense side, lightweight transparent armor is emerging as a critical innovation theme, with ceramic-based composites significantly reducing vehicle weight while maintaining ballistic integrity. Industry participants such as Armitek are increasingly positioned as system integrators rather than commodity glass suppliers, reflecting the U.S. market’s shift toward performance-certified, application-specific security glazing.

India’s Atmanirbhar Bharat Strategy and Defense-Oriented Glass Manufacturing

India’s bulletproof security glass market is scaling rapidly as national security priorities and manufacturing localization converge. The expansion of the Production Linked Incentive (PLI 1.2) scheme to include specialty coated steels and laminated safety glass has elevated armored glazing into a strategically incentivized segment. This policy framework is encouraging domestic production of multi-layer ballistic glass for military vehicles, VIP transport, and law enforcement infrastructure. India’s growing engagement with global homeland security ecosystems, highlighted by international defense roadshows and technology showcases, is accelerating the adoption of integrated ballistic partitions and situational-awareness glazing. From a market standpoint, India is transitioning from an import-dependent consumer to a regional manufacturing base for cost-competitive yet specification-compliant bulletproof glass, particularly for defense and internal security applications.

Germany’s Leadership in Sustainable and High-Performance Bulletproof Glass

Germany anchors the European bulletproof security glass market through its focus on sustainability, optical performance, and advanced materials engineering. German manufacturers are actively aligning ballistic glazing production with EU Green Deal objectives, emphasizing recycled glass substrates and bio-based polycarbonate interlayers. This sustainability-driven approach does not compromise performance; instead, it supports multi-hit resistance and long-life durability required in government buildings and diplomatic facilities. Companies such as Schott AG and Saint-Gobain (via German operations) are leading innovations in decarbonized glass melting and hydrogen-powered furnaces. Germany’s role in the market is defined less by volume and more by premium, regulation-compliant bulletproof glass solutions tailored for European security and infrastructure standards.

South Korea’s AI-Integrated and Export-Oriented Defense Glass Strategy

South Korea is differentiating its bulletproof security glass market through the integration of electronics, AI, and defense technologies. National defense exhibitions and funding programs are accelerating the development of smart ballistic glass capable of displaying real-time tactical data on vehicle windshields and command platforms. This convergence of transparent armor and digital interfaces reflects South Korea’s broader strategy to embed electronics leadership into materials innovation. By designating ballistic-resistant materials as a critical strategic technology, the government is supporting export-oriented production aimed at NATO-aligned armored vehicle and defense markets. South Korea’s competitive advantage lies in its ability to combine ballistic resistance, optical clarity, and electronic functionality within a single security glass system.

Israel’s Deep-Tech Innovation in Urban and Homeland Security Glass

Israel continues to set global benchmarks in high-threat protection and homeland security glass technologies. In 2025, strong investment inflows into defense and HLS sectors have translated into rapid commercialization of hybrid glass-ceramic panels designed for urban environments. These systems are engineered to withstand both ballistic impacts and blast pressures, addressing the complex threat landscape faced by dense urban infrastructure. Israel’s bulletproof security glass market is highly innovation-driven, with a focus on modular “safe room” solutions and rapid-deployment armored partitions. This positions Israel as a technology exporter rather than a volume producer, influencing global design standards for urban protection glazing.

China’s Intelligent Manufacturing and High-End Security Glass Scale-Up

China’s bulletproof security glass market is evolving from large-scale production toward intelligent manufacturing of high-end functional glazing. National exhibitions and government roadmaps emphasize ultra-thin, lightweight ballistic layers and advanced aluminosilicate glass compositions for armored surveillance vehicles, aerospace, and VIP transport. Research institutions and manufacturers such as CNBM are investing in next-generation glass substrates that combine ballistic resistance with photoelectric and anti-halo properties. China’s strategic focus on supply chain dominance and material self-sufficiency reinforces its role as both a high-volume producer and an emerging supplier of advanced bulletproof security glass systems.

National Strategic Development Matrix: Bulletproof Security Glass Market (2025)

Bulletproof Security Glass Market Development Matrix by Country

|

Country

|

Primary Strategic Driver

|

Key 2025 Development

|

Core Application Focus

|

|

United States

|

Public safety mandates & defense R&D

|

School safety laws and lightweight transparent armor

|

Schools, public buildings, military vehicles

|

|

India

|

Manufacturing localization & defense

|

PLI 1.2 incentives and defense collaboration

|

Military, law enforcement, VIP transport

|

|

Germany

|

Sustainability & EU compliance

|

Decarbonized ballistic glass production

|

Government buildings, diplomatic facilities

|

|

South Korea

|

Smart defense integration

|

AI-enabled transparent armor designation

|

Armored vehicles, export defense platforms

|

|

Israel

|

Homeland security innovation

|

Hybrid ballistic–blast-resistant panels

|

Urban safe rooms, critical infrastructure

|

|

China

|

Intelligent manufacturing

|

Ultra-thin and functional security glass scale-up

|

Surveillance vehicles, aerospace, VIP use

|

Bulletproof Security Glass Market Report Scope

Bulletproof Security Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.5 Billion

|

|

Market Size (2035)

|

$29.1 Billion

|

|

Market Growth Rate

|

13.1%

|

|

Segments

|

By Material (Polycarbonate, Glass-Clad Polycarbonate, Laminated Glass, Acrylic, Hybrid Systems), By Security Level (Low Protection, Medium Protection, High Protection), By Application (Defense & VIP Vehicles, Banking & Finance, Construction & Architecture, Government & Law Enforcement, Critical Infrastructure, Commercial Buildings & Retail, Educational Facilities, Others), By Final Product (Flat Glass, Curved Glass, Door Glazing, Transfer Devices)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Key Companies: Saint-Gobain S.A., AGC Inc., Nippon Sheet Glass Co., Ltd., SCHOTT AG, Guardian Industries Corp., PPG Industries Inc., Apogee Enterprises Inc., AGP Group, Armortex, Taiwan Glass Ind. Corp., Total Security Solutions, Consolidated Glass Holdings Inc., Fuyao Glass Industry Group Co., Ltd., Isoclima S.p.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bulletproof Security Glass Market Segmentation

By Material

- Polycarbonate

- Glass-Clad Polycarbonate

- Laminated Glass

- Acrylic

- Hybrid Systems

By Security Level

- Low Protection

- Medium Protection

- High Protection

By Application

- Defense and VIP Vehicles

- Banking and Finance

- Construction and Architecture

- Government and Law Enforcement

- Critical Infrastructure

- Commercial Buildings and Retail

- Educational Facilities

- Others

By Final Product

- Flat Glass

- Curved Glass

- Door Glazing

- Transfer Devices

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bulletproof Security Glass Market

- Saint-Gobain S.A.

- AGC Inc.

- Nippon Sheet Glass Co., Ltd.

- SCHOTT AG

- Guardian Industries Corp.

- PPG Industries, Inc.

- Apogee Enterprises, Inc.

- AGP Group

- Armortex

- Taiwan Glass Ind. Corp.

- Total Security Solutions

- Consolidated Glass Holdings, Inc.

- Fuyao Glass Industry Group Co., Ltd.

- Isoclima S.p.A.

*- List not Exhaustive