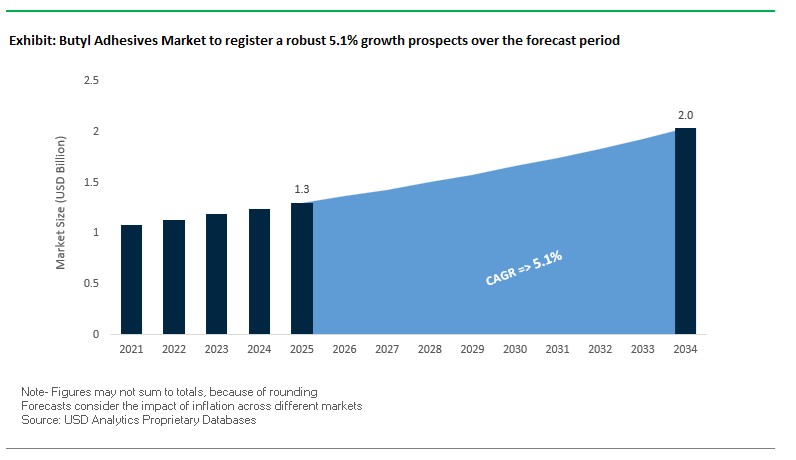

The global butyl adhesives market has gained strategic relevance as airtightness, moisture control, and durability become non-negotiable performance criteria across construction, automotive, and energy infrastructure systems. Valued at USD 1.3 billion in 2025 and projected to reach USD 2 billion by 2034 at a CAGR of 5.1%, market growth reflects the essential role of butyl-based sealing technologies in enabling energy-efficient buildings, long-life glazing systems, and vibration-resistant vehicle assemblies. For OEMs, façade engineers, and automotive integrators, butyl adhesives are not discretionary materials; they are core enablers of system-level performance tied directly to energy loss prevention, acoustic comfort, and lifecycle reliability.

The structural shift reshaping demand is the replacement of curing, rigid sealants with permanently plastic, low-permeability butyl systems in applications where long-term airtightness and moisture resistance are critical. Based on isobutylene isoprene rubber (IIR) chemistry, butyl adhesives deliver among the lowest moisture vapor transmission rates of any commercial sealant class, a property that underpins their dominant use in insulating glass units (IGUs), façade joints, and air barrier assemblies. Their non-hardening, tacky profile allows continuous movement accommodation without cohesive failure, maintaining air, water, and sound sealing performance over decades of thermal cycling. Service temperature capability from −35°C to +125°C supports reliable deployment in metal roofing, flashing, HVAC ducting, and curtain wall interfaces across diverse climate zones, where seal integrity must be preserved despite substrate expansion and contraction.

These material attributes translate directly into business and performance outcomes. In the building envelope, butyl-based primary sealants are essential to IGU gas retention and condensation control, reducing energy losses and extending window service life. In automotive and electric vehicle platforms, low gas permeability and inherent damping properties support tire innerliners, battery pack sealing, and NVH mitigation, aligning with OEM priorities for lightweighting, passenger comfort, and efficiency. The widespread adoption of butyl waterproof tapes—used in roughly 80% of self-adhering membranes for commercial roofing, façades, and air barrier systems—underscores their role as a default sealing technology in modern construction. Looking forward, competitive positioning in the butyl adhesives market will hinge on formulation stability, compatibility with multi-material assemblies, and compliance with evolving energy-efficiency and sustainability standards, as manufacturers increasingly integrate butyl systems into high-performance, code-driven envelope and mobility designs.

The global butyl adhesives industry is evolving through strategic expansions, product innovations, and sustainability-focused partnerships across the supply chain. In January 2025, a major chemical producer announced a 5% capacity expansion for halogenated butyl rubber at its North American facility. This expansion addresses rising global demand from the pharmaceutical stoppers, tire innerliner, and high-performance sealant markets, ensuring greater feedstock availability for butyl adhesive manufacturers amid tightening supply.

In February 2025, the industry witnessed a major leap in insulating glass sealant technology with the launch of a hot-melt butyl sealant featuring i-Boost™ Technology, engineered for automated IGU production lines. The new formulation delivers 15% faster application speed and enhanced resistance to high-temperature slump, directly improving manufacturing throughput in window, façade, and glass bonding applications. Similarly, March 2025 marked a strategic acquisition by a European construction group, expanding its butyl-based flashing tape and window sealant portfolio to strengthen its presence in North American weatherproofing and air barrier systems.

Sustainability continues to define the market’s direction. In June 2025, two major Asia-Pacific chemical companies formed a joint venture to develop bio-based isobutylene, a precursor for butyl rubber, reinforcing the sector’s long-term commitment to renewable polymer chemistry. This was followed by July 2025’s innovation milestone, where a new low-temperature butyl sealant demonstrated 400%+ elongation at −40°C, designed for the transportation and heavy-vehicle sector operating in extreme climates. Meanwhile, April 2025 saw the introduction of a UV-resistant butyl tape tailored for solar panel mounting systems and HVAC duct sealing, solving a long-standing issue of UV degradation in exterior exposure applications.

Automation is another defining trend. In August 2025, a multinational manufacturer announced a multi-million-dollar investment to deploy robotic dispensing equipment across its APAC production sites. The goal: to enhance 6σ process control, reduce production waste, and meet surging demand for precision-engineered butyl tapes and mastics in construction and automotive assembly lines. Furthermore, September 2025 marked the entry of butyl-based acoustic dampening pads for the automotive NVH market, showcasing butyl’s growing role in vibration isolation and EV cabin noise reduction—a key quality parameter in next-generation electric vehicles.

The demand for high-temperature butyl adhesives and sealants is intensifying across advanced industries such as electric vehicles (EVs), automotive manufacturing, and energy infrastructure. Traditional butyl rubber systems—known for their superior impermeability and flexibility—are being reformulated into cross-linked variants to enhance their thermal resistance, oxidative stability, and mechanical durability under prolonged heat exposure. Independent research demonstrates that cross-linking agents such as alkylphenol resins substantially improve thermal endurance, with cross-linked butyl rubbers exhibiting a tensile strength retention rate 2.7 times higher than sulfur-cured equivalents after 96 hours at 177°C.

The advancement is critical for next-generation applications such as EV battery seals, tire bladders, HVAC gaskets, and under-hood automotive components, where consistent sealing performance is required under both high thermal and chemical stress. The ability of advanced cross-linked butyl systems to maintain elasticity and adhesion at temperatures above 170°C has broadened the performance envelope of butyl adhesives, directly challenging alternative elastomer classes like EPDM and silicone. Further, the inherent low gas permeability and chemical resistance of butyl compounds provide an additional layer of protection in critical environments such as battery housings, fuel cells, and electronic enclosures.

The market momentum for cross-linked butyl systems aligns closely with the global push for durable, heat-resistant materials in high-value industrial applications. As electric mobility and renewable energy infrastructure expand, the thermal management capabilities of these butyl systems will position them as essential materials in achieving safety, longevity, and operational reliability in demanding service conditions.

The global construction sector is witnessing a shift toward high-efficiency building envelopes that balance airtightness with controlled vapor permeability. In the transition, specialty butyl sealants and tapes are emerging as preferred materials for achieving durable and compliant air- and moisture-control systems. Unlike traditional asphalt-based sealing systems, butyl adhesives exhibit cold flow and self-sealing properties, allowing them to maintain water and air resistance even around fasteners and irregular substrates.

Energy efficiency regulations—such as those introduced under ASHRAE 90.1 and the International Energy Conservation Code (IECC)—are mandating stringent air leakage rates and moisture control standards for new buildings. Butyl-based flashing tapes and vapor barriers meet these requirements due to their unique combination of adhesion strength, elasticity, and aging resistance, often achieving service lifespans exceeding 25 years under UV, water, and thermal exposure testing. Their performance advantages are especially critical in passive and zero-energy buildings, where airtight continuity and long-term seal durability directly influence the overall energy performance of the structure.

Additionally, innovations in vapor-permeable butyl formulations allow for controlled moisture diffusion, preventing mold growth and ensuring the longevity of wall assemblies. These breathable systems are increasingly being adopted in European building codes that emphasize both airtightness and moisture management, supporting the industry’s transition to resilient, energy-efficient, and sustainable building design. The widespread adoption of butyl adhesives in façade sealing, window flashing, and membrane overlaps drives their expanding role in modern building envelope science.

The global electrification trend is redefining the materials landscape, creating an unprecedented growth opportunity for butyl-based adhesives in EV battery pack sealing and protection systems. Electric vehicle batteries demand robust, chemically resistant sealants that can prevent water ingress, dust intrusion, and gas leakage—while maintaining flexibility across extreme temperatures and vibration conditions. Butyl adhesives and sealants, particularly in hot-melt formulations, are emerging as the preferred choice due to their exceptional moisture resistance, low permeability, and serviceable application.

Manufacturers are actively commercializing removable, reapplicable butyl-based sealing systems to support battery serviceability—a critical design requirement as the EV sector moves toward repairable and recyclable battery architectures. These advanced formulations meet stringent protection ratings such as IP67 and IP69K, ensuring complete water and dust resistance under real-world driving conditions. Additionally, as EV performance standards evolve, with new test protocols simulating extreme temperature cycles and mechanical shock, butyl’s thermal and chemical durability makes it indispensable for gasket sealing, module encapsulation, and pack perimeter sealing applications.

The combination of safety, longevity, and repairability requirements in EV battery systems places butyl adhesives in a unique market position, bridging the gap between performance reliability and lifecycle sustainability. With global EV production expected to surpass 20 million units annually by 2030, the segment offers a multi-billion-dollar opportunity for butyl adhesive manufacturers that can deliver tailored, thermally resilient, and reworkable sealing systems.

The growing emphasis on sustainability, recyclability, and the circular economy is reshaping the global pressure-sensitive adhesive (PSA) market. Regulatory pressures targeting single-use plastics, VOC emissions, and non-recyclable packaging materials are driving adhesive manufacturers to reformulate around bio-based and recyclable butyl chemistries. In the context, bio-derived butyl PSAs are emerging as a next-generation alternative to conventional petroleum-based adhesives, delivering comparable or superior performance in diverse environments.

Breakthroughs in polymer chemistry have produced recyclable PSAs capable of maintaining adhesion even under challenging wet or humid conditions. In one comparative test, an advanced bio-based PSA formulation maintained bond integrity on stainless steel for over seven days under static load, while a conventional butyl acrylate–acrylic acid adhesive failed in less than two minutes—underscoring the potential of sustainable formulations to outperform legacy materials.

Global adhesive producers are launching USDA BioPreferred-certified, plant-based hot-melt PSA lines for use in labels, flexible packaging, and tapes. These formulations are microplastic-free and fully compatible with paper and polymer recycling streams, aligning with corporate sustainability mandates and upcoming EU Packaging and Packaging Waste Regulations (PPWR). The shift toward eco-friendly, circular butyl-based adhesives thus represents one of the most promising commercial frontiers in the market, combining performance reliability with environmental responsibility.

As consumer product companies, packaging converters, and logistics brands adopt low-carbon, recyclable adhesive systems, the demand for green butyl PSAs will expand rapidly across global packaging and labeling value chains—positioning butyl adhesives as a cornerstone in the transition toward sustainable materials engineering.

Butyl Adhesives Market Share Insights, 2025-2034

Butyl Tapes Lead the Global Market with Over 54% Share

The Butyl Tapes segment holds a commanding 54.3% share of the global butyl adhesives market in 2025, underscoring its dominance as the most versatile and user-friendly form of butyl adhesive technology. This leadership is attributed to its ease of application, high tackiness, excellent weatherproofing, and long-term elasticity, making it indispensable across construction, transportation, and renewable energy applications. Unlike liquid sealants, butyl tapes offer instant sealing performance without curing, ensuring immediate adhesion to a variety of substrates including metals, plastics, and glass. In building and construction, they are the standard for sealing roof joints, curtain walls, and window perimeters, helping to achieve airtight and watertight building envelopes. In automotive and transportation, they are used for body panel seams, tail light assemblies, and cabin sealing, enhancing acoustic insulation and structural longevity. The growing shift toward pre-fabrication, modular construction, and easy-install waterproofing systems continues to fuel the adoption of butyl tapes as they align with faster, cleaner, and safer installation practices. Moreover, their solvent-free composition and compatibility with environmental and safety regulations make them a preferred choice over solvent-based sealants in green construction and energy-efficient retrofitting.

Butyl Pastes and Caulks Gain Traction for Flexible Sealing Solutions

The Butyl Pastes and Caulks segment commands a significant share due to its ability to address complex sealing tasks requiring gap-filling, contour shaping, and adhesion to irregular substrates. These formulations offer thixotropic flow properties, allowing them to be extruded, tooled, or brushed into voids and joints. Their exceptional adhesion and flexibility make them ideal for HVAC duct sealing, window perimeter caulking, metal building joints, and general waterproofing applications. They are also favored for their non-hardening, reworkable nature, which enables maintenance and reapplication without the need for complete removal. Butyl caulks are widely used in commercial construction, RV and trailer assembly, and industrial repair, where reliable adhesion under varying temperature and humidity conditions is crucial. Their resistance to UV, ozone, and temperature extremes ensures long service life in outdoor environments. Additionally, with the increased emphasis on sustainable building materials, low-VOC butyl mastic formulations are finding greater acceptance as compliant, cost-effective alternatives to solvent-based sealants.

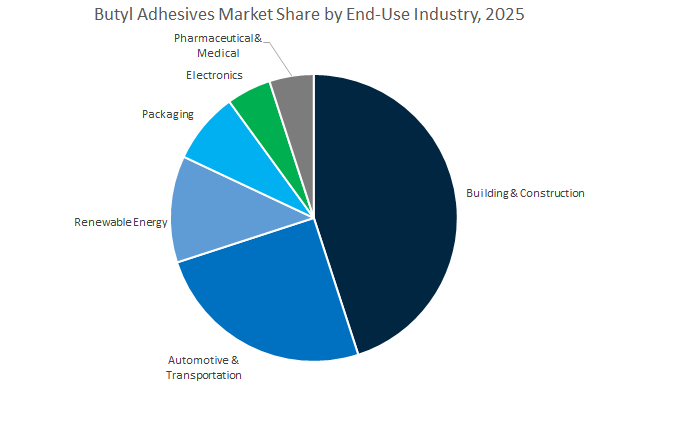

Building & Construction: The Cornerstone of Butyl Adhesive Demand (42.3% Share)

The Building & Construction industry remains the dominant end-use sector for butyl adhesives, accounting for over 42% of global demand. This dominance stems from the material’s unmatched ability to provide airtight and watertight seals, critical for modern building envelopes designed to enhance energy efficiency and durability. Butyl-based products are extensively used in roofing membranes, curtain walls, window sealing, façade panels, and flashing systems, where they protect structures from moisture ingress and improve overall thermal performance. Their excellent UV and weather resistance makes them indispensable in exterior applications, while their flexibility ensures durability through building movements and thermal cycling. The adoption of green construction standards (LEED, BREEAM) and rising demand for sustainable, solvent-free sealing solutions have further cemented butyl’s role as a key component in the global shift toward environmentally responsible construction. As prefabricated and modular buildings gain traction, pre-applied butyl tapes and sheets are increasingly used for faster, cleaner, and more reliable sealing solutions.

Automotive & Transportation: A Vital Segment Driven by Lightweighting and NVH Control (25.9% Share)

The Automotive & Transportation sector represents a major application base for butyl adhesives, contributing roughly 26% of the global market. Butyl-based tapes and mastics are essential for sealing, bonding, vibration damping, and acoustic insulation across vehicles, helping manufacturers meet stringent comfort, safety, and emission standards. In automotive manufacturing, butyl adhesives are used for windshield sealing, tailgate bonding, sunroof installation, and panel joints, providing both structural integrity and waterproofing. Their viscoelastic damping characteristics make them integral to NVH (Noise, Vibration, and Harshness) reduction, a key differentiator in passenger vehicle design. Moreover, in the era of electric mobility, butyl materials are finding increased use in battery enclosures, cable sealing, and underbody protection, thanks to their resistance to thermal expansion, chemicals, and moisture. As global vehicle electrification accelerates, the need for thermally stable and durable sealants in EV battery pack sealing and soundproofing is expected to drive further market expansion.

The global butyl adhesives market is moderately consolidated, with key players such as ExxonMobil, H.B. Fuller, Arkema (Bostik), 3M Company, Sika AG, and Soudal NV leading through vertical integration, automation, and sustainable product portfolios. These companies are innovating in butyl rubber feedstock processing, IGU sealing systems, UV-resistant tapes, and modular construction applications.

ExxonMobil remains the world’s foremost producer of butyl, chlorobutyl, and bromobutyl polymers, forming the foundation of the butyl adhesives industry. With production hubs in the U.S., Europe, and APAC, ExxonMobil ensures a robust global feedstock supply for downstream manufacturers. Its proprietary polymerization process operates efficiently at −75°C instead of −95°C, reducing energy consumption and production costs. This energy-efficient manufacturing capability underpins its leadership in elastomer technology and raw material security for sealant, tire, and pharmaceutical applications.

H.B. Fuller stands out as a pure-play adhesives manufacturer with a vast portfolio of 100+ butyl tape and sealant formulations designed for metal building joints, HVAC systems, and roofing membranes. Its solvent-free, 100% solids formulations comply with global low-VOC regulations and align with green construction standards such as LEED and BREEAM. The company’s expertise in custom formulation and global distribution allows it to address niche applications like low-temperature flexible tapes and high-tack mastics for fast sealing in damp conditions, ensuring strong adoption in roofing and industrial insulation projects.

Bostik, an Arkema subsidiary, continues to lead the insulating glass (IGU) market with its i-Boost™ hot-melt butyl technology, enabling high-speed automated glazing production. Its Bostik 6000 system is engineered for superior thermal stability and mechanical performance in multi-layer façade and IG applications. Arkema’s integrated approach combines butyl, polyurethane, and acrylic systems for comprehensive building envelope waterproofing. The company’s strategic focus on automation and thermal efficiency solutions supports its leadership in smart adhesives and energy-efficient building systems.

3M leverages its world-class pressure-sensitive adhesive (PSA) and tape technology to deliver premium butyl mastic and double-sided tapes used in membrane splicing, window sealing, and modular construction. Its products are validated under ASTM and AAMA standards, with proven 1,000-hour UV resistance and high shear strength for durable outdoor applications. 3M’s R&D investments focus on advanced butyl tapes that offer immediate handling strength, long-term elasticity, and clean removability, making them essential in architectural panel bonding and roofing maintenance.

Sika AG integrates its butyl flashing and sealing tapes into complete roofing and waterproofing systems such as Sarnafil® and Sikaplan® membranes, offering certified, warrantied performance. These systems deliver long-term chemical, water, and UV resistance essential for below-grade, façade, and tunnel waterproofing. Sika’s expertise in system compatibility ensures seamless bonding with polyurethane and liquid-applied membranes, while its low-temperature butyl variants enhance workability in cold environments.

Soudal NV, a key European adhesives manufacturer, has strengthened its distribution footprint across Central and Eastern Europe (2024–2025), making professional-grade butyl mastic and tape products more accessible to renovation and retrofit contractors. The company recently introduced recyclable packaging formats for its extruded butyl rope sealants, reducing on-site waste by 20% and supporting sustainable construction practices. Its butyl formulations are valued for easy tooling, strong adhesion, and aging resistance, making them popular in window frame sealing and roof renovation.

The United States butyl adhesives market is expanding rapidly, propelled by technological advancements, sustainability mandates, and large-scale investments in infrastructure and EV production. The U.S. Department of Energy’s Vehicle Technologies Office allocated $3.1 billion (2022–2026) to enhance domestic electric vehicle (EV) battery manufacturing, significantly increasing demand for advanced butyl sealants used in EV battery pack assembly and thermal management.

According to the U.S. Census Bureau, residential construction expenditure reached $853 billion in 2023, driving robust consumption of butyl-based roofing, flashing, and waterproofing materials across the country’s commercial and residential building sectors. H.B. Fuller’s acquisition of GSSI Sealants (2022) has strengthened its technological base in high-performance butyl tapes for the roofing and industrial sealing markets, while ExxonMobil’s 2025 Proxxima™ butyl polymer expansion in Texas will ensure a consistent domestic supply of high-grade butyl rubber feedstocks for adhesive producers.

Moreover, EPA’s Corporate Average Fuel Economy (CAFE) standards continue to push for lightweighting solutions in vehicle manufacturing, where butyl adhesives offer a durable yet weight-saving alternative to traditional mechanical fasteners. Innovative solutions such as EternaBond® Dry MicroSealant® butyl tapes are increasingly replacing liquid sealants in RV and trailer manufacturing, eliminating cure times and enhancing assembly efficiency.

China remains the global leader in butyl adhesive consumption and manufacturing, with accelerating growth across automotive, electronics, and large-scale construction industries. The nation’s dominance in electric vehicle (EV) manufacturing—led by giants such as BYD and CATL—has created a surge in demand for high-performance butyl sealants for battery moisture protection, vibration damping, and thermal management.

The Chinese government’s infrastructure expansion initiatives, including urban megaprojects and high-speed rail development, have amplified the requirement for durable butyl waterproofing membranes and structural joint sealants for bridges, tunnels, and public facilities. Sinopec’s expansion of butyl rubber capacity has ensured a stable domestic feedstock supply, supporting both export-oriented manufacturers and domestic converters of butyl-based products.

The electronics sector is a growing application area, where precision-applied butyl adhesives are utilized for dust-proofing, acoustic sealing, and component stabilization in consumer devices. Emerging bio-based butyl rubber pilot projects, projected to produce up to 5,000 metric tons by 2025, underline China’s strategic alignment with global sustainability goals. Additionally, the rising production of insulating glass (IG) units—driven by energy efficiency mandates—has strengthened the market for secondary butyl sealants in green-certified buildings.

Germany remains a core innovation hub in the global butyl adhesives market, leveraging its strength in automotive engineering, green construction, and high-performance materials R&D. The country’s automotive manufacturing ecosystem demands butyl tapes and sealants that provide superior NVH (Noise, Vibration, Harshness) reduction and moisture resistance, supporting both conventional and electric vehicle production lines.

The EU Energy Performance of Buildings Directive (EPBD) and Germany’s national Energiewende policy have accelerated the adoption of airtight butyl sealing solutions in energy-efficient building envelopes. LANXESS, one of the world’s top butyl rubber producers, continues to supply halobutyl rubber grades that serve as core raw materials for advanced adhesive systems. Furthermore, Henkel AG & Co. KGaA and BASF SE are pioneering low-VOC and bio-compatible butyl adhesive chemistries, reinforcing Germany’s leadership in sustainable bonding technologies.

The building renovation and retrofitting sector—supported by EU subsidy programs—has become a key growth driver for roofing membranes, expansion joint tapes, and restoration sealants. In aerospace, butyl-based formulations are being used for chemical-resistant sealing and insulation in lightweight composites, underscoring Germany’s focus on high-precision, multi-sector adhesive performance.

India’s butyl adhesives market is witnessing strong expansion, driven by the Make in India initiative, rapid urban infrastructure projects, and growing demand for energy-efficient materials. Government-led investments in smart cities, roads, bridges, and affordable housing have accelerated adoption of butyl-based waterproofing membranes and expansion joint sealants, essential for long-term structural performance.

The renewable energy sector, which recorded 9.83% year-on-year growth in 2022, is also a major growth avenue. Butyl adhesives are increasingly used in photovoltaic (PV) solar module assembly, providing critical weather and moisture protection for India’s expanding solar energy infrastructure.

The automotive sector, supported by increasing domestic and export vehicle production, continues to utilize butyl sealants and body tapes in two-wheelers, commercial vehicles, and EV manufacturing. Meanwhile, the fast-growing e-commerce-driven packaging industry—dominated by food and grocery retailing (70% of sales)—is fueling demand for butyl adhesives in flexible packaging and industrial lamination applications.

With rising foreign direct investment (FDI) and technology partnerships, India is transitioning toward international-quality butyl tape manufacturing, ensuring consistent product standards for the country’s evolving construction, defense, and aerospace sectors.

The United Kingdom butyl adhesives and sealants market has gained renewed momentum through consolidation and sustainability-focused investments. In 2024, H.B. Fuller acquired HS Butyl, a leading UK-based butyl tape manufacturer, expanding its presence in the European waterproofing and construction tape segment. HS Butyl’s established plant in Lymington, England, acts as a strategic production and distribution hub for H.B. Fuller’s global operations.

The UK’s emphasis on retrofitting and improving existing housing stock—aligned with national energy efficiency goals—has created strong demand for airtight butyl sealing tapes used in window, door, and roof junctions. Moreover, the country’s offshore wind energy sector continues to utilize high-durability butyl-based cable sealing and marine protection solutions, vital for withstanding corrosive environmental conditions.

Rising investment in the aerospace sector has further spurred the use of lightweight butyl adhesives and sealants for advanced aircraft components. The combination of government incentives, private innovation, and M&A expansion positions the UK as a key hub for sustainable butyl tape technology across Europe.

Japan’s butyl adhesives industry remains defined by precision engineering, quality assurance, and continuous material innovation. In the automotive sector, leading OEMs are integrating butyl sound-deadening sheets and vibration-absorbing sealants to improve NVH performance in luxury and electric vehicles. Concurrently, ENEOS Corporation is advancing R&D into high-barrier, heat-resistant butyl polymers, vital for tire performance, gas impermeability, and industrial sealing systems.

Japan’s electronics and precision equipment sectors demand ultra-clean, dust-resistant butyl adhesives to ensure reliability in sensitive assemblies, including sensors, circuit housings, and micro-components. Additionally, Japan’s aging infrastructure and seismic safety regulations continue to drive the market for flexible butyl expansion joint sealants used in bridges, tunnels, and building reinforcement.

The country’s ongoing shift toward circular and sustainable material use has led to the development of eco-friendly, recyclable butyl adhesive formulations, aligning with Japan’s national carbon neutrality goals for 2050. The advancements solidify Japan’s position as a global benchmark for high-performance and sustainable butyl bonding solutions.

Butyl adhesives market, waterproofing sealants, butyl tapes, EV battery sealing, sustainable adhesives, low-VOC butyl sealants, construction waterproofing membranes, automotive NVH adhesives, H.B. Fuller butyl tapes, Sinopec butyl rubber, LANXESS halobutyl, ENEOS polymers, renewable energy adhesives, flexible packaging adhesives, global butyl adhesive manufacturers.

Butyl Adhesives Market Report Scope

Butyl Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2034)

|

$2 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product Type (Butyl Tapes, Butyl Pastes/Caulks, Reactive Butyl Systems), By End-Use Industry (Building & Construction, Automotive & Transportation, Packaging, Renewable Energy, Pharmaceutical & Medical, Electronics), By Application Technology (Pressure-Sensitive Adhesives, Hot-Melt Adhesives, Solvent-Based, Water-Based Emulsions

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

H.B. Fuller Company, Henkel AG & Co. KGaA, Sika AG, ExxonMobil Corporation, Dow Inc., LANXESS, 3M Company, Bostik, Arlanxeo, RENOLIT SE, Sinopec, Mapei S.p.A., Wacker Chemie AG, RPM International Inc., General Sealants

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Butyl Tapes

- Butyl Pastes/Caulks

- Reactive Butyl Systems

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Packaging

- Renewable Energy

- Pharmaceutical & Medical

- Electronics

By Application Technology

- Pressure-Sensitive Adhesives

- Hot-Melt Adhesives

- Solvent-Based

- Water-Based Emulsions

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Sika AG

- ExxonMobil Corporation

- Dow Inc.

- LANXESS

- 3M Company

- Bostik

- Arlanxeo

- RENOLIT SE

- Sinopec

- Mapei S.p.A.

- Wacker Chemie AG

- RPM International Inc.

- General Sealants

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how modern butyl adhesives—rooted in IIR chemistry—are enabling long-term airtightness, IGU reliability, EV battery sealing, and moisture-safe building envelopes under tighter energy and sustainability codes. Our analysis reviews demand drivers across construction, automotive, packaging, renewable energy, electronics, and pharma, and tracks price/margin dynamics as feedstock, capacity additions, and automation reshape cost-to-serve. It highlights performance differentiators such as ultra-low MVTR, cold-flow self-sealing, and wide service temperatures that reduce rework and extend service life in roofs, façades, HVAC, and under-hood assemblies. We map supplier moves in bio-based isobutylene, robotics-ready hot-melts, and UV-stable tapes, and surface the commercialization breakthroughs that lift throughput (faster IGU lines), durability (cross-linked butyl), and sustainability (recyclable PSAs). With side-by-side technology and end-use benchmarking, this report is an essential resource for specifiers, OEMs, converters, and procurement leaders seeking code-compliant, low-VOC, and high-reliability sealing solutions across global programs.

Scope Highlights

Segmentation

- By Product Type: Butyl Tapes; Butyl Pastes/Caulks; Reactive Butyl Systems

- By End-Use Industry: Building & Construction; Automotive & Transportation; Packaging; Renewable Energy; Pharmaceutical & Medical; Electronics

- By Application Technology: Pressure-Sensitive Adhesives; Hot-Melt Adhesives; Solvent-Based; Water-Based Emulsions

-

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.