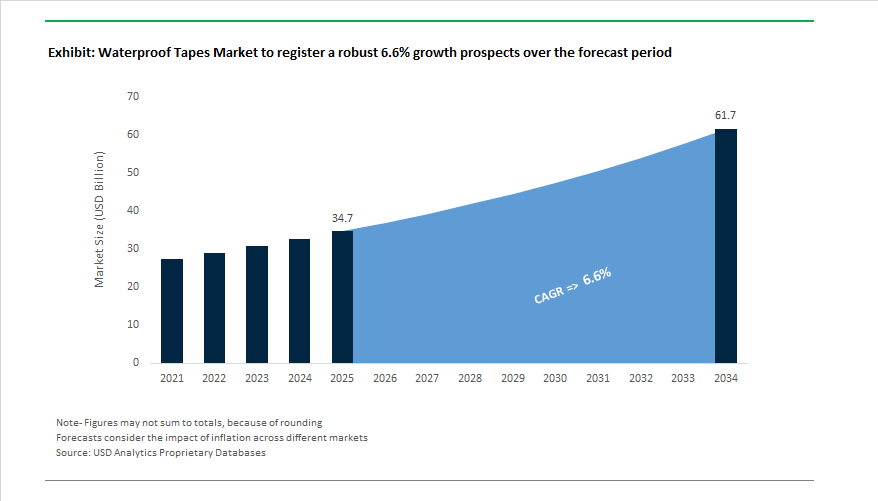

The Global Waterproof Tapes Market is projected to expand from USD 34.7 billion in 2025 to USD 61.7 billion by 2034, advancing at a CAGR of 6.6%, as waterproof tapes evolve into critical performance materials across construction envelopes, electric mobility platforms, outdoor infrastructure, and ruggedized electronics. Market momentum is being driven less by incremental usage and more by specification upgrades, where tapes are selected to deliver airtightness, long-term environmental resistance, and assembly efficiency under increasingly demanding operating conditions.

From a materials standpoint, the market is consolidating around high-performance acrylic foam tapes, butyl rubber sealing tapes, and silicone-based waterproof tapes, each optimized for distinct stress profiles. Manufacturers such as 3M, tesa, Nitto, Avery Dennison, and Saint-Gobain have expanded structural-grade tape platforms designed to replace screws, rivets, and liquid sealants in applications requiring uniform load distribution, vibration damping, and permanent sealing. Acrylic foam tapes used in façades, curtain walls, and EV assemblies typically deliver high shear strength combined with viscoelastic energy absorption, while butyl-based systems remain preferred for air and vapor barriers due to their low permeability and cold-temperature tack. Silicone waterproof tapes are increasingly specified where UV stability, wide service temperature windows, and chemical resistance are mandatory.

A structural shift is underway in construction and building envelopes, where waterproof tapes are being specified as part of integrated air-barrier and moisture-management systems rather than as temporary sealing aids. High-rise and modular construction projects increasingly rely on tapes that maintain adhesion and elasticity over 20+ year service lives, accommodate substrate movement, and perform across wide thermal cycles. In parallel, infrastructure and renewable energy installations—such as solar farms and outdoor electrical enclosures—are driving demand for tapes with long-term UV exposure resistance and stable adhesion under heat, humidity, and freeze–thaw conditions.

Electric mobility and advanced electronics are further elevating performance requirements. In EV battery packs, wire harnessing, and chassis sealing, waterproof tapes are selected for their ability to provide instant sealing, electrical insulation, and vibration isolation while supporting high-throughput automated assembly. OEMs are increasingly standardizing on solvent-free, low-VOC tape systems to align with occupational safety and sustainability targets, reinforcing the shift away from liquid-applied sealants and mechanical fastening. To support these applications, suppliers are investing in digitized supply chains, regional converting capacity, and application-engineered tape formats, reducing lead times and enabling just-in-time deployment.

Key product Insights

- Lead-time advantage: Digitalized distribution and analytics cut order-to-delivery by 15–20% for priority construction/automotive accounts (2025).

- UV endurance: New solvent-free UV-cured modified acrylic grades retain >95% adhesion after 2,000 hours of accelerated weathering.

- Low-VOC adoption: >65% of new high-performance specs in NA/EU use low-VOC waterproof tapes (2025), aligning with tightening air-quality rules.

- Healthcare pull-through: Medical-grade waterproof tapes for wound care/diagnostics growing 7% YoY (early 2025) on aging populations and transdermal therapies.

- Airtight buildings: Premium airtight tapes cut air leakage by >30% vs traditional methods—key for green building compliance and energy savings.

Market Analysis: Sustainability-Led Reformulation, Policy Acceleration, and Substrate-Specific Performance Reshaping Waterproof Tapes

The waterproof tapes segment is undergoing a structural shift from commodity sealing products to application-engineered systems, driven by sustainability mandates, faster construction methods, and the proliferation of low-surface-energy (LSE) substrates in electronics and mobility. Product innovation in 2025 illustrates this inflection clearly. In October 2025, a leading producer introduced bio-based polyol waterproof foam tapes derived from nut-shell oils, achieving 60–70% bio-content while retaining flame resistance for EV battery sealing. This launch marked a critical convergence of renewable chemistry, fire safety, and e-mobility qualification. One month earlier, in September 2025, European Commission policy revisions elevated the use of solvent-free compositions for external waterproofing membranes and tapes in new residential construction, triggering immediate reformulation, testing, and certification activity across European construction sealing portfolios.

Supply-chain strategy and co-development models are reinforcing these material shifts. In July 2025, a top chemical major entered a co-development agreement with a North American construction multinational to deliver an integrated water-ingress prevention system centered on butyl rubber sealing tapes for modular buildings. The initiative reflects growing demand for repeatable, system-level sealing solutions compatible with offsite fabrication and accelerated installation timelines. Earlier, in May 2025, an Asian manufacturer commissioned a new Mexico facility to strengthen North American supply of high-strength automotive bonding and vibration-damping foam tapes, reducing lead times and insulating OEM programs from cross-border logistics risk.

Materials science continues to define competitive differentiation, particularly in moisture-intensive and emerging electronics environments. March 2025 research demonstrated the integration of antimicrobial agents into silicone waterproof formulations, effectively suppressing mold and fungal growth in HVAC systems and select medical equipment—expanding the addressable market into environments where moisture control and hygiene intersect. Addressing a long-standing adhesion bottleneck, a January 2025 launch from a specialty player introduced die-cut precision waterproof tapes with nano-coating technology to improve bonding on LSE plastics such as polypropylene, enabling reliable sealing in consumer electronics and waterproof IoT devices. These advances underscore a broader trend toward substrate-specific engineering, where adhesion performance on difficult plastics determines product qualification.

Consolidation and process optimization provide the backdrop to this evolution. In November 2024, a U.S. packaging major acquired a German reinforced duct tapes specialist to scale all-weather MRO waterproofing solutions, broadening reach in maintenance-intensive end markets. Complementing portfolio expansion, an October 2024 high-speed process pilot for double-sided PVC waterproof tapes delivered approximately 25% throughput improvement while reducing material waste—demonstrating that manufacturing efficiency is becoming as decisive as formulation chemistry.

Market Trend 1: Integration of Superabsorbent Polymer (SAP) Technology for Enhanced Flood Protection in Submarine Cables

The evolution of Superabsorbent Polymer (SAP) technology represents one of the most significant advancements in the Water Blocking Tapes Industry, particularly in protecting submarine cables and offshore power connections. As subsea communication and inter-array power cables face extreme environmental conditions, manufacturers are engineering next-generation non-woven SAP tapes capable of ultra-fast swelling and saltwater resistance.

Recent performance benchmarks indicate that these advanced SAP-based water blocking tapes can achieve a swelling height of ≥9.5 mm within one minute of contact, a key requirement for immediate flood sealing under deep-sea conditions. Premium products are engineered to reach ≥10 mm swell height at the one-minute mark, ensuring rapid capillary blockage in both vertical and longitudinal cable directions.

Material innovation is being led by key developers like Nippon Shokubai, whose AQUALIC™ CS technology utilizes salt-tolerant SAP formulations that can absorb 20–30 times their weight in artificial seawater. The performance is crucial for offshore wind farm cable systems and subsea interconnects that are continuously exposed to saline conditions.

In addition, semi-conductive longitudinal water-blocking tapes have begun replacing traditional paste-based filling systems. These tapes are integrated into the outer conductor layers of submarine cables to enhance vertical and radial water-blocking performance, offering long-term stability, reduced maintenance, and improved insulation reliability under hydrostatic pressure.

Market Trend 2: Development of Non-Yellowing, Low-Migration Water Blocking Tapes for Aerial and Indoor Fiber Optic Cables

The global rollout of Fiber-to-the-Home (FTTH) and 5G small-cell infrastructure is accelerating demand for non-yellowing, non-migrating water-blocking tapes designed for both indoor and aerial fiber optic applications. These high-performance tapes are critical for maintaining signal clarity, low optical attenuation, and long-term mechanical reliability in compact cable constructions.

In advanced fiber optic cables, even minimal water ingress can cause hydrogen ion formation, leading to significant optical attenuation. Research studies confirm that dry, non-migrating water-blocking tapes effectively prevent hydrogen-induced losses by eliminating water diffusion along the fiber strand.

A critical design innovation is the optimization of SAP particle size distribution in coatings—ensuring that less than 7% of the total weight fraction exceeds 300 microns. The fine-tuned granularity reduces microbending losses, a major source of signal degradation in optical fibers.

Thermal performance has also become a vital differentiator. Premium fiber optic water-blocking tapes are engineered for continuous service temperatures up to 90°C, short-term peaks up to 160°C, and instantaneous resistance up to 230°C, preventing chemical migration and maintaining dimensional stability under high-load conditions.

The convergence of thermal endurance, optical clarity, and mechanical integrity has positioned non-migrating water-blocking tapes as essential components in FTTH networks, data centers, and 5G backhaul infrastructure.

Market Opportunity 1: Development of Halogen-Free, Flame-Retardant Tapes for Plenum and EV Battery Cables

The convergence of fire safety standards and electrification trends in both the construction and automotive industries is creating a high-value opportunity for halogen-free, flame-retardant water blocking tapes (HFFR tapes). These solutions ensure that cables used in plenum spaces and EV battery systems meet strict smoke toxicity and flammability standards without relying on halogenated compounds.

In the electric vehicle (EV) segment, the demand for flame-retardant insulation and sealing tapes has surged due to the fire risk associated with battery module thermal propagation. Manufacturers are developing UL 94 VTM-0 compliant halogen-free compounds that ensure superior thermal stability and insulation integrity. Similarly, in building applications, plenum-rated HFFR water blocking tapes are replacing PVC-based materials to reduce smoke density during fire events.

Material innovation in the domain is largely driven by the use of polyolefin-based HFFR compounds that provide low-smoke, halogen-free protection for both optical fiber and power cables. In addition, silicone-based flame-resistant sealing materials, used in EV charging cables and battery pack penetrations, are meeting the UL 94 V-0 standard, reinforcing the industry’s shift toward non-toxic, flame-retardant insulation systems.

Market Opportunity 2: Engineering of Thermally Conductive Water Blocking Tapes for Underground Power Transmission Systems

As power grids evolve to handle high-voltage direct current (HVDC) and renewable energy integration, there is a growing demand for thermally optimized water blocking tapes capable of efficient heat dissipation in underground and submarine power transmission systems. Conventional water blocking tapes often act as thermal bottlenecks, impeding heat flow from the conductor to the ambient environment.

Thermal modeling of high-voltage cables reports that the buffer layer (including the water blocking strip and air gap) has a thermal conductivity as low as 0.09 W/(m·K)—significantly below the 0.286 W/(m·K) of XLPE insulation and 402 W/(m·K) of copper conductors. The disparity highlights the urgent need for highly thermally conductive yet moisture-blocking materials to prevent local overheating and ensure long-term operational stability.

Manufacturers are developing composite water blocking tapes infused with thermally conductive fillers such as boron nitride, aluminum oxide, and graphene, improving overall thermal performance without compromising electrical insulation. The development of such advanced tapes is especially critical for smart grid applications, HVDC interconnects, and renewable energy transmission corridors.

In HVDC design frameworks, core water-blocking materials are recognized for influencing not just moisture resistance but also current-carrying efficiency and system heat management—making thermally conductive water blocking tapes a crucial component in next-generation cable architectures.

Waterproof Tapes Market Share Insights, 2025-2034

Market Share by Functionality/Form

The single-sided waterproof tapes segment dominates the global market, accounting for approximately 34.4% of total share in 2025, underlining its broad utility and cost-effectiveness across multiple industries. These tapes are extensively used for sealing, patching, protection, and surface repair in both industrial and consumer applications. Their simplicity, combined with excellent adhesion to varied substrates such as concrete, metal, plastic, and glass, makes them indispensable in construction, automotive maintenance, and packaging. The widespread use of single-sided waterproof tapes in roofing membranes, window sealing, and surface protection reflects their adaptability to both temporary and permanent sealing requirements. Additionally, the global trend toward infrastructure modernization and housing renovation continues to support their steady consumption, especially in humid and coastal regions where moisture ingress prevention is critical.

Flashing and sealing tapes represent another dominant segment within the market, primarily fueled by the building and construction industry’s rising focus on energy efficiency and building envelope integrity. These tapes are specifically designed to provide long-term waterproof barriers in areas such as window perimeters, door openings, wall penetrations, and roofing assemblies. The construction industry’s growing transition toward advanced materials and sustainable insulation systems further accelerates the adoption of flashing tapes as they enhance vapor control and air-tightness, contributing to improved building performance. On the other hand, double-sided waterproof tapes hold a significant share as a preferred mechanical fastener alternative, enabling seamless bonding for panel lamination, flooring, and structural applications. They provide clean, invisible joints and strong adhesion even under challenging environmental conditions.

Meanwhile, self-fusing and self-amalgamating tapes serve highly specialized markets, especially in electrical, plumbing, and industrial maintenance applications. Their ability to form a homogenous, waterproof seal without adhesive makes them invaluable in protecting cables, pipes, and connectors exposed to high voltage or underwater conditions. This segment’s growth is particularly strong in utility maintenance, telecommunications, and marine applications, where reliability under extreme conditions is non-negotiable. Lastly, structural glazing tapes form a premium, performance-driven category, primarily used in facade bonding, curtain walling, and advanced architectural systems. With the global rise in modern, glass-intensive construction and lightweight automotive design, this segment is witnessing increased adoption, thanks to its exceptional dimensional stability, UV resistance, and long-term bonding performance.

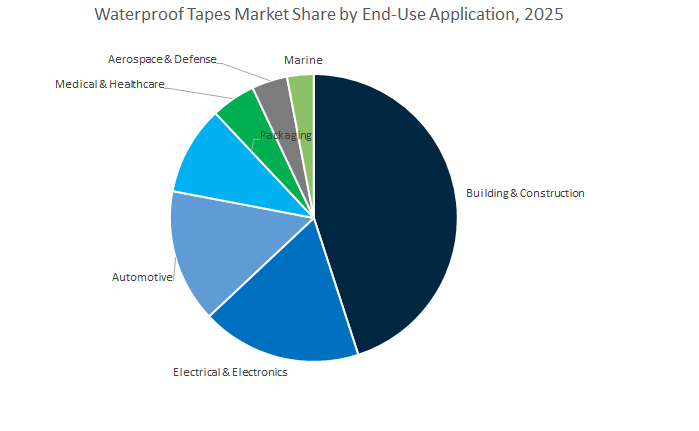

Market Share by End-Use Industry

The building and construction industry remains the largest consumer of waterproof tapes globally, holding an estimated 42.6% share in 2025, driven by surging investments in infrastructure, urban housing, and green building development. Waterproof tapes are integral to ensuring moisture control, air sealing, and structural durability in modern construction. Their use spans roofing systems, flashing joints, vapor barriers, facade bonding, foundation waterproofing, and concrete curing applications. The push for net-zero and energy-efficient buildings is also reinforcing the demand for advanced waterproof and vapor-sealing tapes that enhance thermal insulation and prevent structural degradation. Moreover, the ongoing renovation and maintenance of aging infrastructure, particularly in North America and Europe, is sustaining steady demand for repair-oriented waterproof tapes used in retrofitting, sealing leaks, and improving envelope performance.

The electrical and electronics (E&E) sector represents a critical high-value segment, leveraging waterproof tapes for wire harnessing, cable insulation, and component protection against moisture, dust, and chemical ingress. With the growing adoption of smart electronics, EV batteries, and renewable energy systems, these tapes have become indispensable for thermal and electrical insulation in compact, high-performance assemblies. The automotive industry is another major end-user, relying on waterproof tapes for weather sealing, noise-vibration-harshness (NVH) control, and wire harness protection. The accelerating shift toward electric and hybrid vehicles is expanding the need for specialized tapes used in battery pack sealing, connector protection, and module insulation, where resistance to heat, fluids, and environmental stress is paramount.

Beyond these core sectors, packaging applications utilize waterproof tapes for carton sealing, cold-chain logistics, and moisture-sensitive product protection, especially in e-commerce and food distribution channels. In medical and healthcare, waterproof tapes are increasingly applied in wound dressings, wearable sensors, and medical device assembly, emphasizing biocompatibility and breathability. Meanwhile, aerospace, defense, and marine industries comprise specialized, performance-intensive niches where durability under extreme conditions—temperature fluctuations, saltwater exposure, and mechanical vibration—is critical. These sectors rely on engineered waterproof tapes designed to meet stringent safety and reliability standards.

Leading vendors compete on adhesion science, UV and weathering durability, low-VOC credentials, converting capability, and global footprint. Partnerships with converters and OEMs—plus rapid die-cut prototyping—are central to capturing growth in EV, modular construction, renewables, marine, and electronics.

Overview: Across the top players, strategies converge on viscoelastic acrylic foam (AFT/VHB) performance, butyl sealing for building envelopes, solventless production to cut emissions, and application-specific portfolios (marine, HVAC, medical). Expect continued investment in bio-based polyols, phthalate-free foams, debond-on-demand concepts, and nano-coatings for LSE substrates.

3M’s VHB™ viscoelastic acrylic foam platform enables structural bonding that replaces fasteners in glazing and transportation. The firm supports 40+ industrial tape families and has introduced next-gen VHB™ tailored for EV chassis to improve lightweighting and vibration damping. A global push into advanced die-cutting/converting delivers custom waterproof gaskets for complex electronics assemblies, tightening tolerances and accelerating program ramps.

Nitto’s Niche Top strategy focuses on optical films/tapes and mobility sealing, leveraging proprietary adhesives for ultra-thin, low-outgassing waterproof materials used in sensitive devices. With 85%+ sales outside Japan, Nitto’s footprint enables rapid global support. Under “Nitto for Everyone 2025”, the company advanced hydrogen-powered boiler initiatives to decarbonize production—aligning tape manufacturing with lower CO₂ and strengthening its sustainable tape positioning.

Tesa delivers Acrylic Foam Tapes (AFT) and PE foam tapes engineered for gap-filling, NVH damping, and waterproof barriers across automotive and construction. Deep automotive integration covers seven+ exterior/interior mounts (roof rails, emblems, sensors). A global converter network enables rapid die-cut customization and regional tech support, while ongoing development of PVC/Neoprene foams targets weathering/petrochemical resistance and electrolysis barriers between dissimilar metals.

Avery Dennison’s Core Series™ spans acrylic and rubber constructions with high repulsion resistance and superior LSE (PP) adhesion. The company fields marine-validated waterproof tapes resistant to salt spray, UV, and prolonged immersion, serving hulls and enclosure sealing. A rapid shift to solvent-free technology reduces VOCs without sacrificing bond strength, while products like FM 2454 PE foam deliver gap-filling moisture resistance on glass/ceramic in high-humidity window and mirror mounting.

Saint-Gobain emphasizes solventless acrylic foam tape production to cut flammables and CO₂. Its Norseal V730 is phthalate-free, aligning with safer-materials mandates while preserving seal integrity. The company prioritizes co-development with OEMs for tailor-made systems—including debond-on-demand concepts—and taps Saint-Gobain’s materials platform to embed flame resistance and low embedded carbon for infrastructure-grade sealing.

Shurtape’s industrial heritage anchors MRO sealing/repair with T-Rex® lines featuring extra-thick butyl and clear repair tapes for extreme all-weather hold and UV resistance. The portfolio includes high-mil butyl repair tapes with TPO backings rated for 50 °F to 200 °F application. A recent professional-grade Flashing Tape targets weatherproof window/door seals in premium residential and commercial builds, strengthening its building-envelope presence.

Country Analysis – Global Waterproof Tapes Industry

China – Expanding Infrastructure and Green Construction Policies Drive Waterproof Tape Innovation

China continues to dominate the Global Waterproof Tapes Market as large-scale infrastructure development and industrial modernization fuel consistent demand for advanced adhesive and sealing materials. Under the “Made in China 2025” initiative, heavy investments in urban rail networks, tunnels, and high-rise residential projects are driving widespread adoption of self-adhering modified bitumen waterproof tapes and high-durability butyl sealant tapes for sub-surface construction and external sealing applications. Domestic giants like Oriental Yuhong are significantly increasing capacity across Shandong and Jiangsu provinces, supporting mega public works and private real estate expansion with a focus on rapid-installation waterproofing membranes.

Moreover, updated urban building codes in Tier-1 cities now mandate high-specification sealing materials for energy-efficient façades and window joints, catalyzing demand for acrylic foam tapes with superior tensile strength and long-term weatherability. Parallelly, the surge in 5G base station and data center infrastructure is driving the consumption of high-temperature-resistant silicone waterproof tapes used for EMI shielding and thermal insulation of electronic systems. A strong policy shift toward solvent-free, low-VOC water-based acrylic adhesives aligns with China’s environmental sustainability goals, prompting major R&D activity in green polymer formulations for waterproofing applications.

United States – Infrastructure Modernization and Advanced Manufacturing Boost Waterproof Tape Adoption

The United States waterproof tapes industry is expanding at a rapid pace, propelled by the Infrastructure Investment and Jobs Act (IIJA) and a nationwide focus on resilient, long-lasting construction materials. Billions in federal funding for highway and bridge rehabilitation projects have accelerated the use of rubberized asphalt tapes and butyl rubber waterproofing tapes that deliver excellent adhesion and watertight performance in structural joints and pavement seams. In addition, coastal and hurricane-prone regions are increasing adoption of UV- and saltwater-resistant waterproof tapes for roof membranes and exterior cladding, essential for enhancing climate resilience in building systems.

The U.S. automotive sector, concentrated across the South and Midwest, continues to utilize acrylic foam tapes for lightweighting and NVH (Noise, Vibration, and Harshness) reduction, as part of EV and mobility platform innovation. Cutting-edge R&D programs are exploring nanotechnology-enhanced adhesive formulations, which improve shear strength, fatigue resistance, and waterproof performance for demanding industrial applications. At the same time, smart city infrastructure projects and telecommunications modernization are bolstering demand for waterproof electrical and fiber-optic tapes with extended durability.

Germany – Sustainable Construction Standards and Automotive Engineering Shape the Waterproof Tapes Market

Germany stands as a European innovation hub in the high-performance waterproof tapes segment, guided by its Green Building Certification systems and strict energy-efficiency mandates. Passive house construction standards demand vapor-permeable yet waterproof tapes for airtight sealing of façades and building envelopes, driving significant innovation from domestic leaders like tesa SE. The companies are advancing bio-based adhesives and solvent-free production technologies, aligning with the EU’s environmental directives and circular economy objectives.

Germany’s automotive sector—renowned for its precision and performance engineering—is increasingly adopting acrylic foam waterproof tapes in Electric Vehicle (EV) assemblies for exterior trims, battery modules, and emblems requiring both high-shear strength and thermal stability. R&D efforts are also exploring sensor-embedded tape systems for monitoring structural integrity and humidity levels in next-generation smart buildings. The blend of sustainability, advanced materials, and technological integration positions Germany as a leading market for eco-friendly and intelligent waterproof tapes.

Japan – Precision Engineering and Seismic Safety Propel High-Performance Waterproof Tape Demand

Japan’s waterproof tapes industry is characterized by precision manufacturing, seismic resilience, and advanced electronics integration. The country’s focus on earthquake-resistant infrastructure drives demand for EPDM- and silicone-based waterproof tapes in tunneling, water management, and underground utilities. The tapes provide excellent flexibility, chemical resistance, and long-term adhesion, making them ideal for the nation’s rigorous safety standards in public works.

In parallel, Japan’s advanced electronics and optics sectors rely heavily on ultra-thin, precision-die-cut waterproof tapes for smartphones, displays, and semiconductor devices. Companies like Nitto Denko Corporation continue to pioneer functional waterproof tapes with thermal dissipation and UV stability, supporting both consumer electronics and EV battery thermal management. As the Japanese government promotes longer infrastructure lifespans and sustainability, UV-resistant acrylic tapes and transparent window flashing products are increasingly being adopted for residential renovation and façade sealing projects.

India – Rapid Urbanization and Smart City Development Fuel the Waterproof Tapes Market

India’s construction and infrastructure boom is propelling unprecedented growth in the waterproof tapes industry, with large-scale demand stemming from metro rail, smart city, and industrial development projects. Government-backed initiatives like Smart Cities Mission and PM Awas Yojana (Housing for All) have significantly increased consumption of bitumen-backed and butyl sealant tapes for concrete waterproofing, expansion joints, and roofing. Simultaneously, rising awareness of construction standardization and quality assurance is shifting demand toward certified, branded waterproof tapes over unorganized, lower-grade alternatives.

The automotive manufacturing sector, particularly in two-wheelers and commercial vehicles, is driving the use of mid-performance waterproof tapes for cable harnessing and moisture sealing in humid operating environments. The ‘Make in India’ policy is further strengthening domestic manufacturing capacity, with local producers expanding facilities for synthetic rubber-based and acrylic adhesive tapes to meet both domestic and export demand. India’s rapid construction pipeline and industrialization trajectory make it one of the most promising emerging markets for waterproof tapes.

South Korea – Display Technology and Energy-Efficient Building Solutions Accelerate Tape Demand

South Korea’s waterproof tape industry benefits from its leadership in display technology, semiconductor manufacturing, and smart construction systems. Major electronics brands require ultrathin polyimide and acrylic waterproof tapes for foldable and flexible devices, ensuring superior water and dust protection (IP-rated performance). The precision manufacturing segment has positioned South Korea as a global benchmark for micro-layer waterproofing solutions in next-gen consumer electronics and automotive displays.

The domestic construction sector’s commitment to energy-efficient and air-tight building standards is driving the widespread use of vapor barrier and exterior façade sealing tapes that combine strong adhesion with long-term elasticity. Korean manufacturers are also innovating low-VOC, eco-certified acrylic tapes to comply with indoor air quality and environmental health regulations, reinforcing the country’s dedication to sustainable building practices.

Canada – Harsh Climate Conditions and Utility Projects Spur Waterproof Tape Innovations

Canada’s waterproof adhesive tapes market is driven by the country’s extreme climate conditions, requiring durable, weather-resistant sealing solutions for both residential and commercial building envelopes. The use of self-adhering modified bitumen flashing tapes and weather-resistive barriers (WRBs) is standard practice for protecting against heavy snow, moisture intrusion, and freeze-thaw damage. In colder regions, contractors prefer rubberized asphalt tapes for superior adhesion on irregular surfaces under low-temperature installation conditions.

Additionally, Canada’s expanding oil and gas pipeline infrastructure and utility network upgrades are boosting the market for specialized corrosion-protection and waterproof wrapping tapes, engineered for below-ground and submerged applications. The emphasis on energy efficiency and building code compliance continues to reinforce the country’s strong demand for premium, high-tensile waterproof tapes designed to withstand severe environmental exposure.

Waterproof Tapes Market Report Scope

Waterproof Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34.7 Billion

|

|

Market Size (2034)

|

$61.7 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Adhesive Type (Acrylic, Butyl, Silicone, Rubber, Asphalt), By Backing Material (Film, Foam, Cloth, Foil, Rubber, Paper), By Functionality (Single-Sided, Double-Sided, Self-Fusing, Flashing, Repair, Structural), By End-User (Building & Construction, Automotive, Electrical, Medical, Packaging, Marine, Aerospace), By Technology (Solvent-Based, Water-Based, Hot Melt, Radiation Curing

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, tesa SE, Nitto Denko Corporation, Avery Dennison Corporation, Henkel AG & Co. KGaA, Berry Global Group, Inc., Sika AG, Intertape Polymer Group Inc., Lohmann GmbH & Co. KG, Saint-Gobain S.A., Flex Seal, LLC, Scapa Group plc, Tremco Incorporated, Sekisui Chemical Co., Ltd., Lintec Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Adhesive Type

- Acrylic

- Butyl

- Silicone

- Rubber

- Asphalt

By Backing Material

- Film

- Foam

- Cloth

- Foil

- Rubber

- Paper

By Functionality

- Single-Sided

- Double-Sided

- Self-Fusing

- Flashing

- Repair

- Structural

By End-Use Industry

- Building & Construction

- Automotive

- Electrical

- Medical

- Packaging

- Marine

- Aerospace

By Technology

- Solvent-Based

- Water-Based

- Hot Melt

- Radiation Curing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Waterproof Tapes Market-

- 3M Company

- tesa SE

- Nitto Denko Corporation

- Avery Dennison Corporation

- Henkel AG & Co. KGaA

- Berry Global Group, Inc.

- Sika AG

- Intertape Polymer Group Inc.

- Lohmann GmbH & Co. KG

- Saint-Gobain S.A.

- Flex Seal, LLC

- Scapa Group plc

- Tremco Incorporated

- Sekisui Chemical Co., Ltd.

- Lintec Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Waterproof Tapes Market, connecting demand signals from EV platforms, outdoor infrastructure, and high-performance building envelopes with the underlying shifts to low-VOC chemistries, UV-durable backings, and digitalized supply chains; our analysis reviews functional performance under moisture, heat, and mechanical stress, assesses regulatory readiness across priority regions, and traces supply risk and converting capacity, while it highlights breakthroughs in bio-attributed foams, LSE bonding nano-coatings, and high-swelling water-blocking designs for cables—making this report an essential resource for procurement leaders, specifiers, and product managers seeking faster qualification, resilient sourcing, and margin-safe adoption, etc……

Scope Highlights

Segmentation:

- By Adhesive Type: Acrylic; Butyl; Silicone; Rubber; Asphalt

- By Backing Material: Film; Foam; Cloth; Foil; Rubber; Paper

- By Functionality: Single-Sided; Double-Sided; Self-Fusing; Flashing; Repair; Structural

- By End-Use Industry: Building & Construction; Automotive; Electrical; Medical; Packaging; Marine; Aerospace

- By Technology: Solvent-Based; Water-Based; Hot Melt; Radiation Curing

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast 2025–2034.

Companies (analysis/profiles of 15+): 3M Company; tesa SE; Nitto Denko Corporation; Avery Dennison Corporation; Henkel AG & Co. KGaA; Berry Global Group, Inc.; Sika AG; Intertape Polymer Group Inc.; Lohmann GmbH & Co. KG; Saint-Gobain S.A.; Flex Seal, LLC; Scapa Group plc; Tremco Incorporated; Sekisui Chemical Co., Ltd.; Lintec Corporation.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.