Market Overview: Caproic Acid Market Acceleration Through Bio-Fermentation Routes, Oleochemical Capacity Additions, and C6 Chemistry Realignment

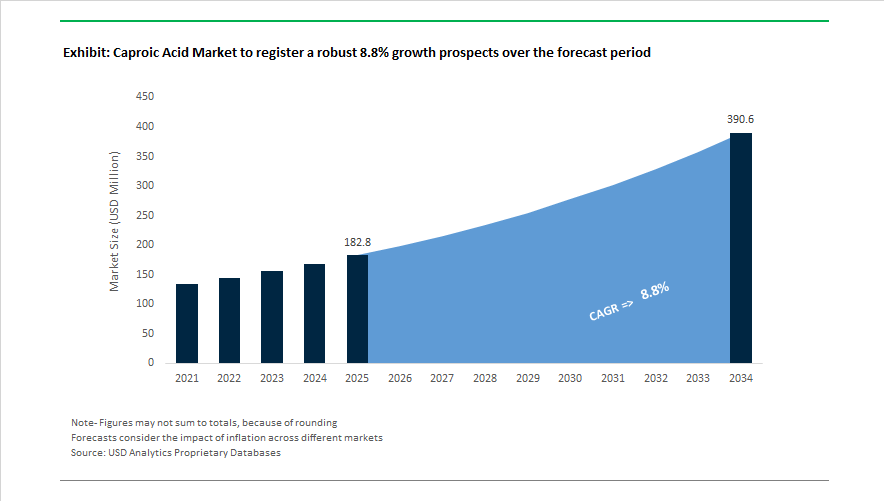

The caproic acid market is projected to expand from USD 182.8 Million in 2025 to USD 390.5 Million by 2034, reflecting a robust CAGR of 8.8% as demand intensifies across bio-based chemicals, specialty esters, personal care intermediates, and pharmaceutical synthesis. In July 2024, KLK OLEO expanded its oleochemical capacity in China to 500,000 tons annually, strengthening Asian supply of high-purity fatty acids including caproic acid for cosmetics, lubricants, and surfactant applications. October 2024 marked a major technology shift when BioVeritas launched its BioVeritas Process, a fermentation platform converting biomass into volatile fatty acids such as caproic acid, targeting renewable aviation fuel and green chemical feedstocks. In November 2024, BioVeritas established full-scale biochemical operations focused on converting organic waste streams into bio-based caproic acid, positioning microbial fermentation as a commercial competitor to palm-derived fatty acid routes.

Structural realignment of the C6 chemical value chain continued through 2025. In January 2025, the United States implemented revised specialty chemical tariffs, encouraging North American buyers to localize sourcing of C6 fatty acids to reduce import exposure. March 2025 saw Mitsui Chemicals partner with Carbon Clean Solutions to pilot a CO₂-to-caproic acid process, targeting a carbon-negative synthesis route for fragrance and pharmaceutical intermediates by late 2026. In August 2025, Evonik Industries restructured site infrastructure into SYNEQT GmbH, streamlining specialty fatty acid derivative production, while inaugurating a world-scale alkoxides plant in Singapore that supports esterification chemistry linked to caproic acid. October 2025 brought the formation of KLK OLEO Life Science, a specialized business unit distributing pharmaceutical-grade caproic acid and esters through a digital platform, aligning oleochemicals with life-science purity standards.

Market pricing and upstream supply stability evolved in late 2025 and early 2026. BASF initiated closures of adipic acid and related intermediates plants in Europe through 2025, reshaping regional C6 derivative flows and tightening supply in downstream polyamide ecosystems. In December 2025, BASF announced price increases for polyamide intermediates effective January 2026, signaling cost pressure across the broader C6 chemical network. July 2025 sustainability upgrades from RAM Sustainability elevated KLK to a Gold1 rating, validating responsible palm kernel oil sourcing that underpins caproic acid production. January 2026 output records from OQ Refineries and Petroleum Industries ensured steady petrochemical precursor supply into Middle Eastern polymer clusters.

Decarbonized Fermentation, EV Lubricant Adoption, and Bio-Nylon Innovation Define Trends and Opportunities in the Caproic Acid Market

Fermentation-Derived Caproic Acid Accelerates as Waste Valorization Becomes Policy-Aligned

The Caproic Acid Market is undergoing a strategic transformation as anaerobic chain elongation technology progresses from academia into commercial pilot deployments. Organic waste—including food scrap streams and agricultural residues—is now acting as a viable industrial feedstock. A 2024 publication in Industrial Crops and Products demonstrated the scalability of this model, reporting yields of 6,175.9 mg/L and 72.9% electron conversion efficiency when biochar was applied as a catalytic enhancer.

This technical progress is intersecting with decarbonization mandates. ChainCraft, a leading circular chemistry player, disclosed that its fermentation-based fatty acids deliver 3 to 6 times lower global warming impact than palm-based or petrochemical routes. Its commercial rollouts—X-Craft for chemical intermediates and SensiCraft for high-purity aroma and taste applications—signal that sustainability is no longer a branding tool but a purchasing criterion. Procurement teams in personal care, food flavor, and surfactant markets are now evaluating suppliers based on Scope 1-3 footprint metrics, forcing fossil-based producers to justify emissions profiles and pricing structures.

Synthetic-Lubricant and EV Cooling Fluid Demand Expands Caproic Derivative Consumption

Synthetic ester lubricants derived from caproic acid are gaining prominence across EV powertrains and data center cooling applications. ExxonMobil and other downstream formulators are introducing caproate-based esters for thermal-stress-resistant lubrication where traditional mineral oils underperform at low viscosity requirements. These esters deliver oxidation control and seal-friendly compatibility profiles that reduce mechanical wear in transmission systems and advanced rotary components used in EV drivetrains.

Metalworking lubricants represent a secondary but expanding channel. In 2025, specialty formulators such as Nelson Brothers Inc. reported growing customer preference for fatty-acid ester emulsions that outperform sulfonate additives in heat dissipation and corrosion management. Caproic-based solutions are becoming particularly attractive in precision machining hubs where downtime costs restrict the adoption of untested chemistries, making reliability a competitive differentiator.

Ionizable Lipids for mRNA Therapeutics Position Caproic Acid as a Critical Pharmaceutical Intermediate

Caproic acid is emerging as a strategic input for next-generation lipid nanoparticles (LNPs), which are essential for mRNA vaccine delivery and gene-editing therapeutics. At the 2025 mRNA Health Conference, Acuitas Therapeutics announced LNP structures utilizing lipid frameworks—many derived from caproic intermediates—that demonstrated a four-fold potency increase when compared with legacy ALC-0315 formulations.

Cold-chain storage has historically constrained global vaccine deployment. New LNP manufacturing methods, presented at the 2025 Controlled Release Society Meeting, demonstrated that vesicle-based lipid formation using caproic-derived ionizable lipids allows mRNA products to remain stable at 2 to 8 degrees Celsius for more than a year. For governments and NGOs pursuing vaccine equity, this eliminates the capital burden of ultra-cold logistics and redefines how mRNA platforms scale across emerging markets.

Bio-Based Nylon 6,6 Pathways Create Long-Term Industrial Demand for Caproic-Derived Adipic Acid

The trajectory toward fossil-free polymers is introducing a new structural demand channel linking caproic acid to adipic acid and nylon 6,6 manufacturing. Geno and Asahi Kasei advanced their commercialization agreement in 2025, building on Geno’s proven capacity to scale plant-based HMD and adipic acid intermediates. The alliance is aligned with automotive OEM and apparel brand timelines, which require sustainable fiber adoption before the decade’s end.

Toray Industries is simultaneously scaling its microbial fermentation process using inedible biomass, reporting a 1,000-fold efficiency increase relative to early-stage prototypes. The ability to bypass benzene-based petrochemical synthesis and move toward 100% bio-derived nylon represents a structural shift with direct implications for long-term caproic acid demand forecasting, particularly for investors modeling ESG-linked polymer capacity.

Caproic Acid (Hexanoic Acid) Market Share and Segmentation Insights

Market Share by Purity Grade: Industrial Volume Leadership Balanced by Food and Pharma Value

Industrial grade accounts for 52% of caproic acid consumption in 2025, reflecting its role as a cost-effective intermediate for metal soaps such as cobalt and zinc caproates, rubber accelerators, lubricant esters, specialty plasticizers, and defoamers. Typical purities of 98–99% support large-scale chemical manufacturing, with demand closely tied to coatings, polymer additives, and broader industrial activity. Food grade represents the second-largest segment, leveraging caproic acid’s natural occurrence in milk fat and plant oils for flavoring cheese, butter, and baked goods, alongside preservative functions. FEMA GRAS status and FDA/EFSA approvals sustain stable uptake as clean-label and natural-identical flavor trends expand. Pharmaceutical grade remains the smallest by volume but highest in value, supplying ultra-high-purity material above 99.5% for antiviral and antifungal API synthesis and controlled-release excipients, where USP, EP, and JP compliance drives consistent, premium-priced demand.

Market Share by Application: Flavor Leadership Reinforced by Antibiotic-Free Feed Adoption

Flavor and fragrance applications command 34% of global caproic acid demand in 2025, utilizing its intense cheesy and waxy notes across dairy flavors and fruit compositions such as strawberry and pineapple, while adding depth to chypre and animalic fragrance accords. Chemical manufacturing forms the second-largest segment, converting caproic acid into caproyl chloride, caproate esters, and metal caproates for paints, coatings, surfactants, and rubber processing, with volumes tracking industrial output. Animal feed is a rapidly expanding channel, deploying caproic acid as a medium-chain fatty acid to improve gut health and suppress Salmonella and E. coli in poultry, swine, and aquaculture, aligned with global antibiotic-free production trends and MCFA blend commercialization. Personal care continues to grow through caproic esters in premium skincare, while pharmaceuticals remain niche but high value in drug synthesis and permeability-enhanced delivery systems.

Market Share By Application, 2025.png)

Competitive Landscape of the Caproic Acid Market

The global caproic acid (n-hexanoic acid) market in 2026 is shaped by a clear divide between synthetic oxo-based producers and bio-based fermentation innovators, with demand accelerating across aviation lubricants, refrigeration oils, flavor & fragrance intermediates, animal nutrition additives, sustainable aviation fuel (SAF), cosmetics, and agrochemical synthesis. Competitive advantage increasingly hinges on feedstock security, ultra-high purity control, circular economy manufacturing, and sustainability traceability. Market leaders are differentiating through integrated oxo chains, plantation-to-product transparency, mass-balance chemistry, carbon-negative C6 acids, and biotech-driven waste valorization, positioning caproic acid as a critical building block for both performance chemicals and low-carbon specialty applications.

Oxo-chain purity leadership in synthetic caproic acid by Oxea

Oxea enters 2026 as the world’s leading pure-play Oxo Performance specialist following its rebranding and acquisition by Strategic Value Partners and Blantyre Capital. The company supplies high-purity synthetic caproic acid that serves as the global benchmark for aircraft turbine lubricants and premium refrigeration oils. Through its world-scale integrated oxo chains in Oberhausen and Bay City, Oxea tightly controls aldehyde precursor purity, enabling ultra-clean n-hexanoic acid production. Its 2026 transformation program strengthens German manufacturing while accelerating specialty acid portfolio expansion. Strategically, Oxea emphasizes operational excellence and supply security, positioning synthetic caproic acid as a weather-independent alternative to plant-based oleochemicals for critical industrial customers.

Plantation-to-product green chemistry scale from KLK OLEO

KLK OLEO leads the nature-derived caproic acid segment in 2026, leveraging vertically integrated palm and lauric oil plantations to deliver traceable C6 fatty acids. Its Emmerich, Germany facility reached full utilization of a high-purity fatty acid expansion, supplying sustainable caproic acid to European food and cosmetics markets. PALMAC™ Caproic Acid is widely adopted in animal nutrition gut-health formulations, replacing antibiotics across EU and North American livestock systems. Backed by its “Plantation Verbund,” KLK OLEO tracks material flows from seed to finished product, providing unmatched transparency for sustainability audits. Its participation in global palm and lauric oil outlook forums reinforces commitments to zero-deforestation sourcing.

Mass-balance C6 integration within the Verbund by BASF SE

BASF approaches the caproic acid market through its Monomers and Nutrition & Care divisions, embedding C6 chemistry inside its massive Verbund network. In 2026, BASF scales its Mass Balance model, replacing fossil feedstocks with bio-circular inputs such as pyrolysis oil from plastic waste. High-purity caproic acid is a key intermediate for flavor and fragrance esters, especially natural-identical fruit notes used in premium beverages. BASF also deployed AI-driven supply chain digitization in early 2026 to forecast demand from EV battery coolants and specialty coatings. Internal consumption for plasticizers and polyamide additives provides a captive market, buffering volatility in global caproic acid pricing.

Carbon-negative bio-based caproic acid innovation by Afyren SA

Afyren stands out in 2026 as the sector’s primary disruptor, producing 100% bio-based caproic acid via non-GMO anaerobic fermentation. Its optimized Afyren Neox process converts agricultural byproducts into seven organic acids, including AFYREN® C6, one of the few commercially available carbon-negative caproic acids. Targeting clean-label cosmetics and sustainable lubricants, Afyren offers drop-in replacements for petrochemical C6 without formulation changes. The company is expanding globally through joint venture discussions in North America and Southeast Asia, replicating its circular manufacturing model near diverse biomass sources. Waste valorization remains central to Afyren’s strategy to de-fossilize specialty chemical supply chains.

Biomass upcycling for SAF and food-grade C6 by BioVeritas

BioVeritas is a North American innovator transforming underutilized biomass into medium-chain fatty acids, with caproic acid positioned at the core of its SAF and food preservation strategy. By 2026, its sustainable aviation fuel pathway reached pilot-scale viability, using C6 as a critical intermediate. The company also supplies food-grade caproic acid for natural mold inhibition and antimicrobial preservation, supporting clean-label initiatives among US processors. A proprietary microbial consortium developed in 2025 increased MCFA yields by 30% , making bio-based caproic acid cost-competitive with synthetic grades. Regional feedstock flexibility allows BioVeritas to operate resiliently despite volatility in agricultural commodity markets.

Biomedicine-plus-fine-chemicals integration from Hebei Yanuo Bioscience

Hebei Yanuo Bioscience combines biotechnology with fine chemical manufacturing to serve agrochemical and biopharmaceutical markets with industrial and technical-grade caproic acid. Operating three major production bases in Shijiazhuang, Cangzhou, and Wuhai, the company supports complex multi-step reactions for next-generation herbicides and pharmaceutical active compounds. Its dual-engine “Biomedicine + Fine Chemicals” model enables custom synthesis and continuous large-scale production of caproic-derived intermediates. Following ISO 9001, 45001, and 14001 certifications, Hebei Yanuo positions itself in 2026 as a safety-first Chinese supplier for Western markets, emphasizing regulatory compliance, environmental stewardship, and strategic partnerships with global agrochemical leaders.

Netherlands: Circular Fermentation Infrastructure and Industrial-Scale Caproic Acid Commercialization

The Netherlands is positioning itself as Europe’s epicenter for sustainable caproic acid production, anchored in circular fermentation and waste-to-value infrastructure. In June 2025, ChainCraft entered a long-term exclusive supply agreement with Innovad Group to provide bio-fermented fatty acids, including caproic acid (C6) and butyric acid, derived from upcycled food waste for premium animal health formulations. This agreement validates the scalability of fermentation-derived medium-chain fatty acids (MCFAs) for high-margin feed additives and gut health solutions.

In August 2025, ChainCraft finalized preparations for a full-scale industrial plant in Ter Apelkanaal, marking a transition from pilot-scale fermentation to commercial-scale production of circular chemical intermediates. Strategic downstream integration is also accelerating: an April 2025 collaboration between ChainCraft and Eternis Fine Chemicals aims to develop low-carbon aroma chemicals using caproic acid as a foundational building block for sustainable fragrance compounds. The multibillion-euro 10x10x10 covenant, signed by 20 northern Dutch companies in late 2025, further expands valorization of residual potato juice and food waste into organic acids. In December 2025, the first full industrial-scale delivery of circular fatty acids to the animal nutrition sector was completed, confirming commercial feasibility of bio-based C6 chains. Consumer brands such as Ecover are incorporating fermentation-based fatty acids into high-performance surfactants under circular product lines, reinforcing downstream adoption.

India: BioE3 Policy and API Park Expansion Accelerate Bio-Based Caproic Acid Manufacturing

India’s caproic acid industry is entering a policy-driven expansion phase under the BioE3 (Biotechnology for Economy, Environment, and Employment) framework approved in August 2024. This policy prioritizes high-performance biomanufacturing for bio-based chemicals, functional foods, and specialty intermediates, directly supporting the domestic production of hexanoic acid and related medium-chain fatty acids. Complementing this initiative, the National Bioenergy Programme allocated approximately ₹140 crore (~$17 million) for Phase-I through 2025–26, incentivizing biomass-based cogeneration and biochemical extraction projects that can supply renewable feedstocks for caproic acid fermentation and distillation.

Indian oleochemical players such as VVF Ltd have modernized distillation units to achieve 99% purity hexanoic acid, targeting the flavor and fragrance sector’s pivot toward natural-origin ingredients. Under the BioE3 framework, the establishment of Biofoundry and Biomanufacturing Hubs is accelerating the transition from conventional petrochemical routes to regenerative bio-based acid production. Parallel expansion of Active Pharmaceutical Ingredient (API) parks is stimulating pharma-grade caproic acid demand as a solvent and intermediate in antibiotic and fungicide synthesis. This convergence of policy support, infrastructure investment, and specialty chemical upgrading is structurally strengthening India’s position in the global C6 fatty acid value chain.

Malaysia: Palm-Based Oleochemical Fractionation and EUDR-Compliant Caproic Acid Exports

Malaysia’s caproic acid market is deeply integrated into its palm-based oleochemical ecosystem, with capacity expansion and sustainability certification shaping export competitiveness. KLK OLEO launched a dedicated Life Science business unit in 2025 to supply high-purity caproic acid for nutraceuticals and “Conscious Beauty” applications. Parent company Kuala Lumpur Kepong Berhad secured a Gold1 Sustainability Rating upgrade from RAM Sustainability in July 2025, underscoring traceable, palm-derived medium-chain fatty acid (MCFA) supply chains.

Producers such as IOI Oleochemical and Pacific Oleochemicals have integrated advanced SCADA monitoring systems to optimize C6–C10 acid fractionation from palm kernel oil, improving yield precision and energy efficiency. In 2025, Malaysian firms expanded distribution footprints in the Middle East and Vietnam, including participation in VietnamPlas 2025, to supply caproic acid-based additives for plastics processing and specialty lubricants. Blockchain-based traceability systems are now deployed to comply with the EU Deforestation Regulation (EUDR), ensuring continued market access for Malaysian caproic acid exports into Europe’s sustainability-sensitive markets.

United States: Recycled Chemical Infrastructure and Synthetic Ester Innovation Elevate Caproic Acid Demand

The United States caproic acid industry is influenced by pricing adjustments, circular chemical infrastructure, and downstream innovation in synthetic esters. In May 2025, Eastman Chemical Company implemented price increases across its acid portfolio, reflecting geopolitical trade tensions and elevated logistics costs. Eastman’s Kingsport methanolysis facility achieved operational milestones in 2025, producing 2.5 times more recycled content than in 2024, increasing availability of sustainable chemical building blocks for North American manufacturers.

Tariff adjustments in 2025 have accelerated nearshoring strategies, prompting distributors such as GreenChem Industries to reconfigure supply chains for imported fatty acids. The U.S. remains a primary market for synthetic lubricant esters, with caproic acid increasingly utilized in high-performance polyol esters for automotive and aerospace applications requiring thermal stability and oxidative resistance. Concurrently, ketogenic dietary trends are driving production of C6-rich medium-chain triglyceride (MCT) oils for functional foods and dietary supplements, reinforcing caproic acid demand in nutraceutical formulations.

Sweden: Renewable Carboxylic Acids and Low-Carbon Polyol Esters Define Premium C6 Applications

Sweden is advancing renewable caproic acid applications through decarbonized chemical manufacturing and high-performance ester innovation. Perstorp expanded its “Pro 100” portfolio to include 100% renewable carboxylic acids produced via a traceable mass-balance model, targeting Finite Material Neutral objectives. Sustainable building blocks for polyol esters introduced in 2023–2024 have enabled Swedish producers to claim among the lowest product carbon footprints for acids used in synthetic lubricants.

In early 2026, Swedish firms are showcasing caproic acid-based esters as core components in immersion cooling fluids for high-density data centers, particularly in London and Atlanta technology hubs, reflecting next-generation thermal management demand. Sweden also maintains strong positioning in the global animal protein sector, with Perstorp emphasizing caproic acid as an antimicrobial solution in antibiotic-free farming systems. This dual focus on renewable chemistry and high-value technical applications reinforces Sweden’s premium positioning in the global hexanoic acid market.

China: Baijiu-Driven Hexanoic Acid Consumption and Export-Focused Regulatory Streamlining

China remains the largest volume producer of refined-grade caproic acid (99% purity), underpinned by robust domestic demand from the liquor industry, where hexanoic acid is a key flavor compound in “strong-aroma” Baijiu fermentation. Industrial scale-up at coastal refineries has optimized recovery of synthetic caproic acid as a byproduct of large-scale oxidation processes, reinforcing China’s cost leadership in bulk C6 fatty acid production.

In 2025, draft regulations from the Ministry of Agriculture streamlined registration of terpene and fatty acid-based agents for export-only purposes, accelerating international trade flows of Chinese chemical intermediates. Domestic agricultural technology strategies have also elevated caproic acid usage as an intermediate in herbicides and plant growth regulators. This integration of food, agrochemical, and industrial demand segments solidifies China’s diversified consumption base and export competitiveness in the global caproic acid industry.

Caproic Acid Market Report Scope

Caproic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$182.8 Million

|

|

Market Size (2034)

|

$390.5 Million

|

|

Market Growth Rate

|

8.8%

|

|

Segments

|

By Source (Natural, Synthetic), By Purity Grade (Industrial Grade, Food Grade, Pharmaceutical Grade), By Product Type (Pure Caproic Acid, Caproic Acid Derivatives), By Application (Flavor and Fragrance, Animal Feed, Chemical Manufacturing, Personal Care, Pharmaceuticals), By End Use Industry (Food and Beverage, Agriculture and Animal Nutrition, Cosmetics and Personal Care, Automotive and Industrial Lubricants, Healthcare and Pharmaceuticals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Oxea, KLK OLEO, Wilmar International, BASF SE, Musim Mas Group, Eastman Chemical Company, IOI Oleo, Procter and Gamble Chemicals, Pacific Oleochemicals, Hebei Yanuo Bioscience Group, Temix Oleo, Acme Hardesty, Vantage Specialty Chemicals, Universal Preserv A Chem, Platinum Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Caproic Acid Market Segmentation

By Source

By Purity Grade

- Industrial Grade

- Food Grade

- Pharmaceutical Grade

By Product Type

- Pure Caproic Acid

- Caproic Acid Derivatives

By Application

- Flavor and Fragrance

- Animal Feed

- Chemical Manufacturing

- Personal Care

- Pharmaceuticals

By End Use Industry

- Food and Beverage

- Agriculture and Animal Nutrition

- Cosmetics and Personal Care

- Automotive and Industrial Lubricants

- Healthcare and Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Caproic Acid Industry

- Oxea

- KLK OLEO

- Wilmar International

- BASF SE

- Musim Mas Group

- Eastman Chemical Company

- IOI Oleo

- Procter and Gamble Chemicals

- Pacific Oleochemicals

- Hebei Yanuo Bioscience Group

- Temix Oleo

- Acme Hardesty

- Vantage Specialty Chemicals

- Universal Preserv A Chem

- Platinum Industries

*- List not Exhaustive