Market Overview: Honeywell–Johnson Matthey Deal, Circular Polymer Catalysis, and Refinery Decarbonization Shape Market Expansion

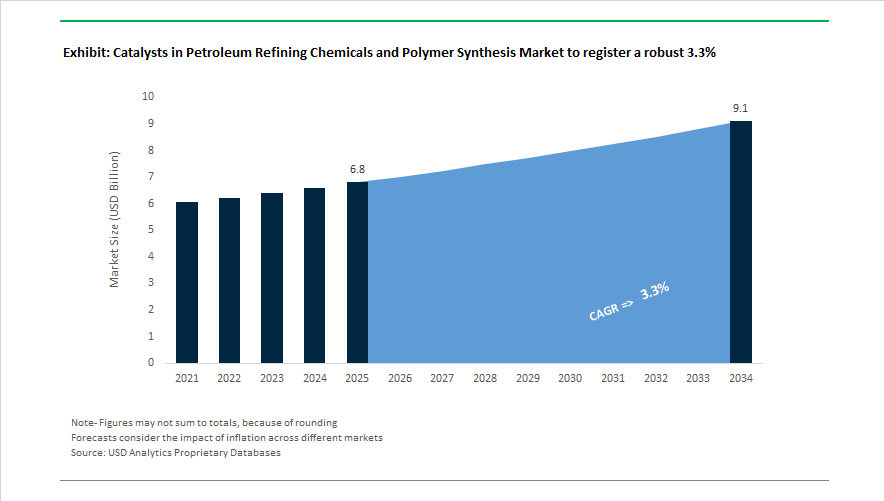

The Catalysts in Petroleum Refining, Chemicals, and Polymer Synthesis Market is projected to grow from USD 6.8 billion in 2025 to USD 9.1 billion by 2034, registering a CAGR of 3.3% as refiners, petrochemical producers, and polymer manufacturers intensify adoption of advanced hydroprocessing catalysts, polymerization catalysts, and catalyst regeneration technologies. In 2024, Advanced Refining Technologies introduced ENDEAVOR, a hydroprocessing catalyst platform designed for Sustainable Aviation Fuel and renewable diesel production using 100% renewable feedstocks, supporting refinery decarbonization strategies. During 2024 to 2025, BASF expanded its X3D® 3D printed catalyst structures, improving mass transfer and lowering pressure drop in refining and chemical reactors, while W. R. Grace & Co. launched next-generation metallocene catalysts for high performance polyethylene used in medical and food packaging.

Circular polymer processing gained momentum in January 2025 when Evonik Industries partnered with Oerlikon Barmag to scale chemical PET recycling through catalyst optimized depolymerization systems. In February 2025, Evonik launched the Purocel catalyst series for upgrading plastic waste pyrolysis oil, enabling its integration into steam crackers as polymer grade feedstock. Capacity expansion followed in August 2025 when Evonik inaugurated a world scale alkoxides catalyst plant in Singapore, reinforcing Asia Pacific supply for biodiesel and specialty chemical synthesis. In October 2025, Clariant introduced AddWorks titanium based catalysts to replace antimony systems in polyester polymerization, improving PET recyclability and addressing raw material supply risk.

Industry consolidation and technology commercialization accelerated in 2025 and 2026. In May 2025, Honeywell agreed to acquire Johnson Matthey’s Catalyst Technologies division, integrating hydrogenation, methanol synthesis, and low carbon fuel catalyst portfolios into Honeywell UOP, with closure targeted for the first half of 2026. Axens moved to become sole owner of Eurecat in October 2025, centralizing catalyst regeneration and rejuvenation capabilities for refinery hydroprocessing units. In February 2026, Lummus Technology and Sumitomo Chemical commercialized PMMA chemical recycling, deploying catalyst enabled depolymerization to convert waste acrylic into high purity MMA monomers. That same month, Mitsui Chemicals formed a global collaboration to build a renewable plastics supply chain using mass balance catalyst systems. Portfolio restructuring also shaped supply dynamics when Ecovyst divested its Advanced Materials and Catalysts segment in January 2026 to concentrate on sulfuric acid catalyst regeneration services.

Trends and Opportunities Reshaping the Catalysts in Petroleum Refining, Chemicals, and Polymer Market

Shift Toward Co-Processing and Multi-Functional Catalysts in Refinery–Petrochemical Integration

The global refinery landscape is undergoing a structural pivot as operators strategically deprioritize traditional fuel output and transition toward petrochemical-enabled profit pools. This shift places catalysts at the center of refinery competitiveness. Fluid Catalytic Cracking (FCC) catalysts and reforming additives are being reformulated to maximize propylene, ethylene, and aromatics while simultaneously supporting bio-feedstock integration.

In 2025, global refiners are accelerating adoption of bio-FCC catalysts optimized for renewable oils and waste-derived lipids, which have demonstrated up to a 15% uplift in renewable gasoline and diesel components compared to traditional FCC formulations. This trend reflects a larger macroeconomic shift: instead of investing tens of billions into new hydroprocessing units, refiners are using catalyst innovation to retrofit and extend the productivity of existing assets. At the same time, sulfur- and nitrogen-trapping technologies embedded within next-generation FCC catalysts now account for over one-third of catalyst demand due to tightening Tier 3 and Euro 6 emissions standards. This makes catalytic performance—not mechanical expansion—the primary avenue for regulatory compliance and long-term margin protection.

Precision Polymer Design via Advanced Single-Site and Post-Metallocene Catalysts

Catalysts are equally strategic in polymer value chains, particularly where high-performance materials differentiate end-use products in medical, photovoltaic, packaging, and EV interior applications. The migration away from bulk Ziegler-Natta catalysts toward single-site catalyst platforms is reshaping polymer capabilities by enabling unprecedented control over polymer branching, molecular weight distribution, and comonomer incorporation.

Two 2025 milestones are accelerating this industry transition. First, LyondellBasell’s technology licensing agreement with SHCCIG Yulin Chemical introduced Metocene PP add-on systems for differentiated polypropylene grades—bringing industrial-scale precision catalysis to Asia’s fastest-growing production base. Second, Indian Oil Corporation’s Paradip complex deployment of Avant Z501 and Z509-1 catalysts under the Hostalen ACP process enables multi-modal HDPE production with improved stiffness-to-toughness ratios. This also eliminates the generation of low-value transition resins during grade switching—a major cost-efficiency advantage for polymer producers.

Catalysts for Converting Captured CO₂ into Fuels, Monomers, and Circular Chemicals

Catalysis is becoming the enabling technology for decarbonization. The industry is now moving from carbon capture to carbon monetization—turning CO₂ into commercial materials rather than treating it as waste.

One of the most significant breakthroughs occurred in May 2025, when EPFL researchers introduced an encapsulated cobalt-nickel catalyst capable of converting CO₂ at 90% energy efficiency with full product selectivity, maintaining stable performance for 2,000-plus hours. If industrialized, this catalyst class could reduce carbon-recycling operating costs by as much as 60–80 percent—an inflection point that could turn CO₂-to-chemicals from a policy-driven segment into a market-driven one.

Commercial traction is already visible. Honeywell UOP is scaling its eFining™ technology, leveraging catalytic CO₂ reduction paired with green hydrogen to produce eMethanol—a critical Sustainable Aviation Fuel (SAF) precursor. SAF decarbonization mandates in Europe and Japan are expected to heavily favor catalytic pathways due to scalability and drop-in infrastructure compatibility.

Selective Catalysts for Plastic Chemical Recycling and Depolymerization

Catalysts are also poised to solve one of the most challenging waste-management problems of the modern era: mixed-plastic contamination. In September 2025, a Northwestern University team unveiled a nickel-based single-site catalyst that maintains activity even in the presence of PVC contamination—a historic barrier that has prevented industrial-scale mixed-polyolefin processing. This development opens the door to true mixed-stream chemical recycling, enabling upcycling of packaging waste into virgin-quality feedstocks.

In parallel, catalytic upcycling is extending beyond polymers into pharmaceutical applications. A December 2025 study at the University of St. Andrews demonstrated that ruthenium-catalyzed semi-hydrogenation can transform household PET into Active Pharmaceutical Ingredient (API) intermediates, reaching turnover numbers of up to 37,000. This creates potential cross-sector value chains where waste plastics become precursors for oncology treatments—signaling an unprecedented opportunity for chemical companies to capture ESG-aligned value at premium margins.

Catalysts in Petroleum Refining, Chemicals, and Polymer Synthesis Market Share and Segmentation Insights

Market Share by Catalyst Type: Refining Leads While Environmental Catalysts Post Fastest Growth

Refining catalysts hold 44% of global catalyst consumption in 2025, encompassing FCC, hydrotreating (CoMo, NiMo), hydrocracking, reforming (Pt, Pt-Re), and alkylation systems. Demand is shaped by refinery utilization, heavier crude slates, and tightening fuel standards such as IMO 2020 and Euro VI, with FCC catalysts contributing the largest physical volumes. Chemical synthesis catalysts rank second, supporting hydrogenation, oxidation, amination, carbonylation, and alkylation across methanol, ammonia, ethylene oxide, and cumene production, with growth aligned to capacity additions in Asia and the Middle East. Polymer synthesis catalysts form a significant and expanding segment, driven by Ziegler–Natta, metallocene, and post-metallocene systems for polyethylene and polypropylene, alongside polyester and polyurethane catalysts as specialty polymers and circular packaging gain traction. Environmental catalysts are the fastest-growing category, spanning SCR for NOx control, VOC oxidation, and automotive aftertreatment, reinforced by tighter global emission regulations and integrated precious metal recovery.

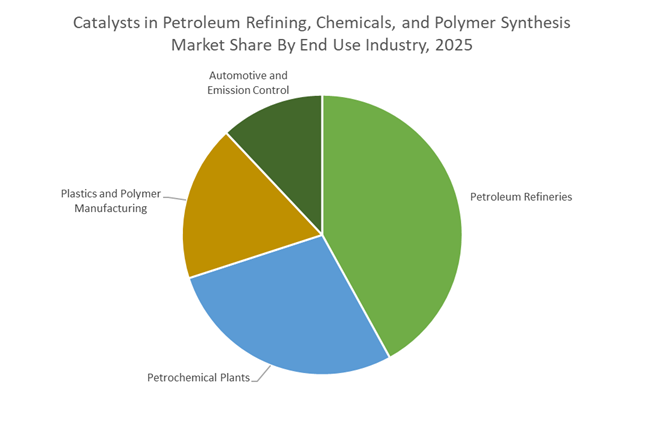

Market Share by End Use Industry: Refineries Anchor Demand as Petrochemicals and Polymers Accelerate

Petroleum refineries represent 42% of catalyst demand in 2025, relying on continuous FCC, hydrotreating, and reforming operations to convert crude into transportation fuels and petrochemical feedstocks, with catalyst cycles influenced by crude quality and product slate optimization. Petrochemical plants are the second-largest and fastest-growing users, driven by steam crackers, aromatics complexes, methanol-to-olefins units, and ammonia/methanol facilities, particularly across China’s coal-to-chemicals projects and US Gulf Coast ethane expansions where catalyst performance directly impacts on-stream factor. Plastics and polymer manufacturing consumes substantial volumes through polyolefin, PET, and nylon production, with bioplastics and chemical recycling introducing new catalyst requirements. Automotive and emission control form a growing downstream segment via three-way catalysts, SCR, DOC, and particulate filters, where precious metal pricing and evolving emission standards continue to shape formulation strategies.

Competitive Landscape of the Catalysts in Petroleum Refining Chemicals and Polymer Synthesis Market

The catalysts in petroleum refining, chemicals, and polymer synthesis market in 2026 is shaped by 3D-printed shaped catalysis, AI-driven digital twins, hydrogen economy platforms, circular polymers, and high-severity hydroprocessing technologies. Competition is intensifying around FCC catalysts, hydrocracking and hydrotreating catalysts, olefin production systems, and next-generation polymerization catalysts, with suppliers differentiating through process-catalyst integration, sustainability-led innovation, and feedstock flexibility. Leading players are investing heavily in energy transition catalysts, SAF enablement, plastic waste depolymerization, and modular process solutions, positioning themselves as strategic partners for refiners and petrochemical producers navigating decarbonization, crude-to-chemicals conversion, and advanced polymer manufacturing.

3D-printed shaped catalysis leadership from BASF SE

BASF has established itself as a 2026 technology leader in shaped catalysis with the commercial launch of X3D® catalysts from its Ludwigshafen facility. These additively manufactured structures reduce reactor pressure drop while increasing surface area, directly improving throughput in refining and chemical synthesis. BASF’s Fourtitude™ FCC catalyst series maximizes butylenes yield from heavy resid feedstocks, supporting petrochemical integration strategies. Through its Catalyst Development and Solids Processing Center, BASF is advancing methane pyrolysis and plastic waste depolymerization via loopamid concepts. Its Global Digital Hub in Hyderabad applies AI-powered digital twins to optimize catalyst run-lengths and predictive maintenance across global refinery networks.

Integrated hydrogen economy platforms by Honeywell UOP

Honeywell UOP remains a dominant force in process-catalyst licensing and hydrogen economy infrastructure. Its acquisition of Johnson Matthey’s Catalyst Technologies business significantly expanded UOP’s footprint in syngas, methanol, and refining catalysts. Distillate Unionfining™ and Oleflex™ catalysts continue to set benchmarks for Euro-V/VI diesel and polymer-grade propylene with minimal hydrogen consumption. UOP’s Everystep™ lifecycle platform integrates catalyst loading, performance analytics via Honeywell Forge, and spent catalyst reclamation. With unmatched zeolite mastery and advanced molecular sieves, UOP enables modular gas processing and aromatics optimization, offering refiners a faster path to profitability through digitally enabled catalyst ecosystems.

Pure-play FCC and hydroprocessing specialization from W. R. Grace & Co.

Following its acquisition by Standard Industries, Grace has sharpened its focus as a pure-play catalyst manufacturer across FCC, hydrocracking, and polyolefins. The full acquisition of ART Hydroprocessing™ gives Grace control over EnRich® guard beds and hydrotreating catalysts critical for renewable diesel in 2026. Its contaminant-tolerant FCC architectures allow refiners to process high-metal, high-sulfur opportunity crudes without rapid deactivation. Grace is also deploying AI-assisted molecular synthesis to accelerate ligand design for specialty polymer catalysts. Strategically, the company is aligning its Advanced Refining Technologies portfolio to support global SAF infrastructure, reinforcing its role in energy transition enablement.

High-severity hydroprocessing innovation from Ketjen Corporation

Ketjen entered 2026 as a standalone catalyst innovator under KPS Capital Partners, redirecting capital toward Refining Catalyst Solutions in Asia-Pacific and the Middle East. After divesting its Eurecat stake to Axens, Ketjen doubled down on high-severity hydrocracking and FCC excellence, enabling refiners to switch flexibly between fuels and chemical feedstock production. Its Performance Catalyst Solutions plant in Pasadena, Texas, anchors custom catalyst manufacturing for advanced polymer synthesis. Ketjen’s strategy emphasizes operational flexibility and entrepreneurial innovation, developing catalysts capable of handling high-metals bio-based and circular feedstocks, positioning the company at the intersection of refining resilience and sustainable petrochemicals.

Heavy-metal-free polymerization breakthroughs from Clariant AG

Clariant leads 2026 innovation in sustainable polymerization catalysts, spearheading the industry shift away from heavy metals. Its upcoming titanium-based polyester catalyst replaces antimony systems, reducing energy consumption and mitigating supply chain risks. The PolyMax® 600 Series polypropylene catalysts deliver up to 100% higher activity while meeting global food-contact compliance. Clariant’s HYDEX E hydro-dewaxing catalyst is gaining traction for converting mixed plastic waste into premium winter-grade diesel. Through its EcoCat expansion, Clariant is advancing circular polymers by upgrading pyrolysis oils into virgin-quality feedstocks, strengthening its leadership in sustainable chemicals and next-generation plastics.

Scale-driven catalyst customization from Sinopec Catalyst Co., Ltd.

Sinopec Catalyst leverages its position within the world’s largest refining group to deliver unmatched scale and application-specific customization. Its integrated feedstock-to-product R&D enables real-world optimization of high-propylene FCC additives and methanol-to-olefins catalysts. In 2026, Sinopec is expanding international service centers across the Middle East and Southeast Asia, offering localized catalyst solutions for mega-integrated complexes. The company is also a major supplier of Ziegler-Natta and metallocene systems for LLDPE and HDPE used in infrastructure and automotive components. Sinopec’s price-performance leadership and modular catalyst platforms make it a regional champion in fast-growing petrochemical markets.

United States: Bayport Hydroprocessing Expansion, SAF Catalyst Commercialization, and CFRP Polymer Innovation

The United States remains a global leader in catalysts for petroleum refining, renewable fuels, and advanced polymer synthesis, supported by infrastructure stability and next-generation technology deployment. In February 2026, Topsoe announced the expansion of its Bayport site in Texas with a new 15,000-ton-per-year hydroprocessing catalyst production facility. The plant will manufacture the TK catalyst family for conventional refining as well as HydroFlex™ technology, specifically engineered for renewable diesel and sustainable aviation fuel (SAF) production. This expansion strengthens North America’s supply chain resilience for hydrotreating, hydrocracking, and renewable feedstock upgrading catalysts.

According to the January 2025 report from the U.S. Energy Information Administration, U.S. atmospheric distillation capacity remained stable at 18.4 million barrels per calendar day. Major refiners such as Marathon Petroleum and Valero Energy are prioritizing catalyst-driven yield optimization rather than expanding physical footprints. In June 2025, the U.S. Department of Energy allocated over $35 million to 42 commercialization projects, including high-energy density SAF blendstocks and bio-derived methanol conversion technologies. Chevron’s ENDEAVOR™ catalyst system, launched in late 2024, has set new performance benchmarks for renewable feedstock processing using EnRich guard and hydrotreating catalysts. Meanwhile, the commissioning of the Pasadena Performance Products facility near Houston in 2025 introduced a next-generation alkylate production model using natural gas liquids, reinforcing demand for specialized polymerization and alkylation catalysts. U.S. specialty chemical leaders are also intensifying investment in Controlled Free Radical Polymerization (CFRP) technologies for advanced dispersants in automotive and industrial coatings.

Saudi Arabia: Direct Crude-to-Chemicals (CTC) Strategy and Smart Refinery Automation Accelerate Catalyst Integration

Saudi Arabia is repositioning itself at the forefront of catalytic innovation through Direct Crude-to-Chemicals (CTC) integration and green hydrogen development. In October 2025, Saudi Aramco, Honeywell, and King Abdullah University of Science and Technology signed a Joint Development Agreement to co-develop next-generation CTC pathways. The initiative aims to bypass traditional refining stages, converting crude oil directly into light olefins and petrochemicals, significantly enhancing carbon utilization and catalyst efficiency.

Jazan Economic City is emerging as a high-tech refining and petrochemical hub in early 2026, integrating IoT-based catalyst performance monitoring systems within smart refinery frameworks. By late 2025, Saudi Aramco reported more than $7 billion invested in clean energy R&D, with over 250 projects targeting hydrogen reformer efficiency and blue hydrogen catalyst optimization. In January 2026, Topsoe was selected to provide advanced catalysts for the Yanbu Green Hydrogen Project, enabling green ammonia exports. Aramco’s Smart Refinery initiative targets 12–15% efficiency improvements and 18–22% carbon emission reductions by 2026, underscoring the strategic role of IoT-enabled catalyst management systems.

China: Catalyst Localization Milestones, Ethylene Surplus, and AI-Driven Performance Monitoring

China’s catalysts market is expanding in response to record polymerization capacity and localization breakthroughs. In 2025, the North China Institute of Chemical Industry successfully calibrated the YS-9010 silver catalyst at the Gulei Petrochemical site, achieving 89.7% selectivity and marking a significant domestic substitution milestone for high-end ethylene oxide catalysts. The Sinopec–Saudi Aramco Gulei Ethylene Project, featuring the world’s largest EO/EG scrubber tower, has contributed to a record ethylene surplus in 2025.

Advanced polymer additive innovation is accelerating. In November 2025, BASF inaugurated a new Nanjing production line for high-performance dispersants utilizing CFRP technology, supporting automotive and industrial coatings growth across Asia. In January 2026, Topsoe signed a technology agreement with Tangshan Jinlihai for a major SAF initiative, reinforcing renewable catalyst deployment. SECCO Petrochemicals entered a 10-year agreement with Clariant to implement the CLARITY™ Prime AI catalyst monitoring platform at its 900-KTA Shanghai ethylene plant. Coal-based ethylene glycol production surpassed 51% of total output in 2025, increasing demand for robust catalysts capable of handling high-impurity syngas streams in coal-to-chemical processes.

India: Ethanol Blending Leadership, Green Hydrogen Deployment, and PGM Circular Economy Push

India’s catalysts in petroleum refining and polymer synthesis market is being reshaped by energy transition policies and refining modernization. The Ministry of Petroleum and Natural Gas highlighted the Oilfields Amendment Act, 2025, streamlining approvals for petrochemical hubs in the Krishna-Godavari and Andaman basins. India achieved a 19.24% ethanol blending rate in the 2024–25 supply year, with a roadmap targeting 1–5% SAF blending by 2027, necessitating large-scale deployment of renewable hydrotreating and alcohol-to-jet catalysts.

The Kakinada project, led by AM Green, began green ammonia deployment phases in late 2025, signaling India’s entry into commercial hydrogen catalyst applications. Bharat Petroleum Corporation Limited and Indian Oil Corporation have committed ₹28,000 crore toward green hydrogen infrastructure and refinery modernization through 2040. Under the National Critical Minerals Mission (NCMM), 2025 regulations emphasize platinum-group metal recovery and domestic catalyst recycling, strengthening India’s circular economy approach to precious metal-dependent refining catalysts.

Germany: Ultra-Low Energy Styrene Catalysts, Hydrogen Breakeven, and Emission Control Leadership

Germany remains a catalyst innovation powerhouse, particularly in energy-efficient polymer precursor production and hydrogen technologies. In April 2025, Clariant and Technip Energies introduced the StyroMax UL-100 catalyst, enabling styrene production at ultra-low steam-to-oil ratios, dramatically reducing energy intensity in polymer synthesis.

At ERTC 2025, European-led advancements such as SiliconTrap™ and HDO catalysts were recognized for extending reactor cycle life by 25–30% in renewable feedstock processing. Johnson Matthey reported Clean Air division margins of 14–15% in late 2025, driven by high-efficiency emission control catalysts for automotive and industrial applications. Hydrogen technology divisions across leading German and UK firms are projected to reach operating profit breakeven by FY 2025/26, signaling commercial maturity of green hydrogen and ammonia catalyst systems.

The Netherlands: Titanium-Based PET Catalysts and YXY®-Driven Renewable Polymerization Platforms

The Netherlands continues to strengthen its leadership in sustainable polymer catalysts and circular plastics infrastructure. At K 2025, Clariant unveiled AddWorks™ titanium-based catalysts for PET production, offering a heavy-metal-free alternative to antimony systems and scheduled for commercial release in 2026.

In late 2025, a consortium of 14 global partners led by Sony Group launched the world’s first large-scale renewable plastics supply chain utilizing advanced Dutch catalytic recycling technologies to process mixed plastic waste. Avantium signed a capacity reservation agreement with Logoplaste in November 2025 for releaf®, a plant-based PEF polymer produced via proprietary YXY® catalytic technology. These developments reinforce the Netherlands’ strategic position as a catalyst innovation hub driving circular economy polymer synthesis and sustainable packaging solutions.

Catalysts in Petroleum Refining Chemicals and Polymer Synthesis Market Report Scope

Catalysts in Petroleum Refining Chemicals and Polymer Synthesis Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.8 Billion

|

|

Market Size (2034)

|

$9.1 Billion

|

|

Market Growth Rate

|

3.3%

|

|

Segments

|

By Type (Refining Catalysts, Chemical Synthesis Catalysts, Polymer Synthesis Catalysts, Environmental Catalysts), By Ingredient (Zeolites, Metals, Chemical Compounds), By Form (Powder, Granules, Extrudates, Structured Shapes), By End Use Industry (Petroleum Refineries, Petrochemical Plants, Plastics and Polymer Manufacturing, Automotive and Emission Control)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Honeywell UOP, Albemarle Corporation, W R Grace and Company, Clariant AG, Axens, Johnson Matthey, Topsoe, Evonik Industries, Sinopec Catalyst Company, Shell Catalysts and Technologies, ExxonMobil Chemical, LyondellBasell Industries, Chevron Phillips Chemical, Nippon Ketjen

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Catalysts in Petroleum Refining Chemicals and Polymer Synthesis Market Segmentation

By Type

- Refining Catalysts

- Chemical Synthesis Catalysts

- Polymer Synthesis Catalysts

- Environmental Catalysts

By Ingredient

- Zeolites

- Metals

- Chemical Compounds

By Form

- Powder

- Granules

- Extrudates

- Structured Shapes

By End Use Industry

- Petroleum Refineries

- Petrochemical Plants

- Plastics and Polymer Manufacturing

- Automotive and Emission Control

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Catalysts in Petroleum Refining Chemicals and Polymer Synthesis Industry

- BASF SE

- Honeywell UOP

- Albemarle Corporation

- W R Grace and Company

- Clariant AG

- Axens

- Johnson Matthey

- Topsoe

- Evonik Industries

- Sinopec Catalyst Company

- Shell Catalysts and Technologies

- ExxonMobil Chemical

- LyondellBasell Industries

- Chevron Phillips Chemical

- Nippon Ketjen

*- List not Exhaustive

Catalysts in Petroleum Refining Chemicals and Polymer Synthesis Market Segmentation

By Type

- Refining Catalysts

- Chemical Synthesis Catalysts

- Polymer Synthesis Catalysts

- Environmental Catalysts

By Ingredient

- Zeolites

- Metals

- Chemical Compounds

By Form

- Powder

- Granules

- Extrudates

- Structured Shapes

By End Use Industry

- Petroleum Refineries

- Petrochemical Plants

- Plastics and Polymer Manufacturing

- Automotive and Emission Control

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)